$RYA (-2,81 %)

$UNH (-0,41 %)

$GM (-0,75 %)

$RTX (-0,19 %)

$UPS (-0,27 %)

$UNP (+0,41 %)

$NOC (+0,29 %)

$BA (-0,26 %)

$MC (-2,08 %)

$TXN (+0,2 %)

$STX (+1,66 %)

$SSAB A (+0,51 %)

$ASML (+1,3 %)

$GEV (+0,88 %)

$SBUX (-0,59 %)

$T (-0,56 %)

$GD (-0,52 %)

$MSCI (-0,8 %)

$META (-0,9 %)

$NOW (-2,37 %)

$IBM (-0,83 %)

$LRCX (+1,88 %)

$TSLA (+0,12 %)

$MSFT (-1 %)

$000660

$005930

$SAP (+0,3 %)

$ABBN (+1,18 %)

$DBK (+0,09 %)

$ROG (+0,03 %)

$DOW (+0,12 %)

$NDAQ (-0,55 %)

$LMT (-0,94 %)

$CAT (+1,09 %)

$TMO (-0,63 %)

$HON (+0,74 %)

$MA (-0,81 %)

$BX (+0,51 %)

$WM (+0,06 %)

$WDC (+2,16 %)

$SNDK (+1,33 %)

$V (-0,31 %)

$AAPL (-0,22 %)

$SOFI (-0,12 %)

$CL (-0,42 %)

$AXP (-0,52 %)

$XOM (-0,25 %)

$CVX (+0,28 %)

Ryanair Holdings

Aktie

Aktie

ISIN: IE00BYTBXV33

Ticker: RYA

IE00BYTBXV33

RYA

Price

Diskussion über RYA

Beiträge

136Mon.·

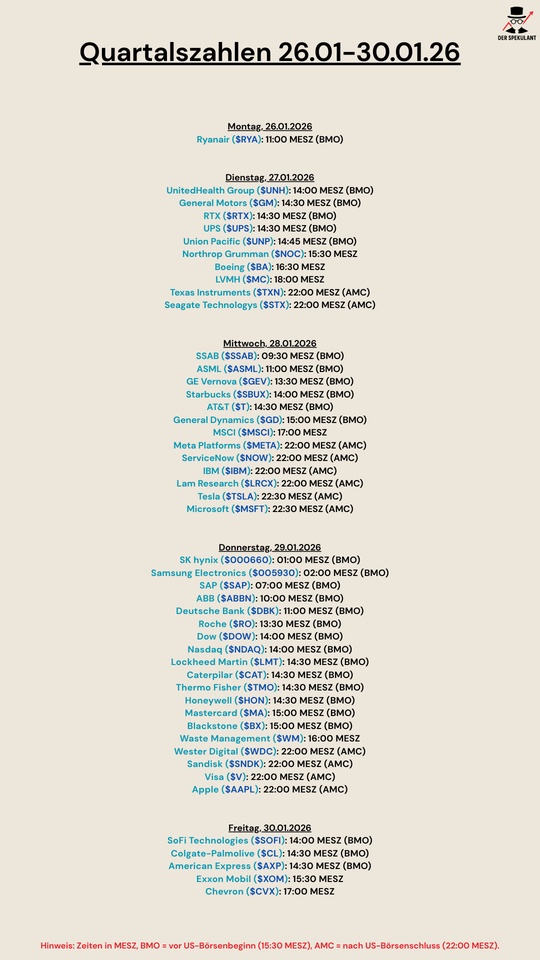

Quartalszahlen 26.01-30.01.2026

1414

7 Kommentare

der_Don@der_Don

6Mon.

•

66

•Alle 3 weiteren Antworten anzeigen

8Mon.·

Aktienanalyse – Europas effizienteste Airline im Bewertungscheck

Lesedauer: ca. 5 Minuten

Viele meiner letzten Beiträge drehten sich um Kennzahlen, Modelle und Bewertungslogiken – und wie man damit Unternehmen systematisch einordnet. Ich überlege schon länger, ob Ryanair eine gute Ergänzung für mein Portfolio sein kann. Genau deshalb eignet sich die Airline besonders gut, um zu zeigen, wie sich ein etabliertes Geschäftsmodell durch HQR-Logik, 10B-Ansatz, fundamentale Kennzahlen und ein klar abgeleitetes Szenariomodell bewerten lässt.

Ryanair $RYAAY (-3,05 %) / $RYA (-2,81 %) gilt auf den ersten Blick als klassisches Low-Cost-Unternehmen. Hinter diesem einfachen Konzept steckt jedoch ein über Jahrzehnte optimiertes Effizienzmodell. Die vollständige Standardisierung auf Boeing-737-Flugzeuge, extrem schnelle Turnarounds, strikte Kostendisziplin und eine stabile Logik aus Zusatzumsätzen – von Gepäck über Sitzplatzwahl bis zu Partnerdiensten – bilden einen operativen Rahmen, der in Europa nahezu konkurrenzlos ist. Die Stärke dieses Modells liegt weniger im Preissetzen als in der konsequenten Umsetzung einer klaren Kostenführerschaft.

Über Tochtergesellschaften in Irland, Malta, Polen und Großbritannien kann Ryanair Kapazitäten flexibel verschieben und Strecken je nach Nachfrage neu gewichten. Mehr als 200 Millionen Passagiere pro Jahr erzeugen Skaleneffekte, die nachhaltig wirken und schwer kopierbar sind. Genau deshalb ist der Burggraben weniger spektakulär als effektiv: eine große, standardisierte Flotte, eine extrem disziplinierte Organisation und ein Geschäftsmodell, das in sich geschlossen funktioniert.

Die aktuellen Geschäftszahlen untermauern diese Konstruktion. Im FY25 erzielte Ryanair 13,95 Milliarden Euro Umsatz und 1,61 Milliarden Euro Gewinn. Im laufenden Halbjahr liegt das Ergebnis bereits oberhalb von 2,5 Milliarden Euro. Die Bilanz weist rund zwei Milliarden Euro Nettoliquidität aus, die Eigenkapitalquote bewegt sich weiterhin im Bereich von 40 Prozent. Die operative Marge liegt bei 14 bis 15 Prozent – und damit spürbar über dem Niveau des Vorjahrs.

Die wichtigsten Kennzahlen im Überblick:

- KGV (TTM): ca. 13,4

- KGV (Forward): ca. 12,5

- KUV: ca. 1,9

- EV/Sales: ca. 1,78

- EV/EBITDA: ca. 7,8

- Free-Cashflow-Yield: ca. 7,4 %

- ROE: ca. 27 %

- ROIC: ca. 13 %

- Debt/EBITDA (brutto): ca. 0,69

- Operative Marge (TTM): ca. 14–15 %

- PEG-Ratio: ca. 0,74

- Rule of 40: ca. 29 %

Das deutsche Listing (ISIN IE00BYTBXV33 / $RYA (-2,81 %)) notiert im Bereich von 25 bis 26 Euro. Das US-ADR-Listing ($RYAAY (-3,05 %) ) liegt zuletzt bei 68,16 US-Dollar und dient als Referenz für die meisten Analystenmodelle, da dort das höchste Handelsvolumen stattfindet. Bewertungskennzahlen wie das KGV sind unabhängig von der Währung, Kursziele werden jedoch in USD berechnet und später auf Euro übertragen.

Für die Gewinnpfade der kommenden Jahre bietet der aktuelle Stand einen brauchbaren Ausgangspunkt. Das Ergebnis je Aktie liegt bei rund 4,25 US-Dollar. Der Verkehr wächst stabil, die Zusatzumsätze je Passagier steigen, und die operative Marge hat sich nach zwei volatilen Jahren wieder gefestigt. Aus diesem Dreiklang ergibt sich ein neutraler Erwartungswert, der im Bereich von rund fünf Dollar liegt. Damit ist gemeint, dass Ryanair sein Kerngeschäft fortführt, ohne zusätzliche positive oder negative Impulse.

Ein bullisches Ergebnisniveau setzt voraus, dass mehrere Faktoren gleichzeitig konstruktiv wirken: ein stabileres Treibstoffumfeld, unveränderte oder nur moderat steigende Gebühren in Italien, Spanien und Großbritannien sowie eine verlässlichere Lieferperformance bei Boeing. Dies würde der Marge zusätzlichen Spielraum geben und die Nachfrageentwicklung am oberen Rand der bisherigen Erwartungen verankern. In einem solchen Umfeld sind Ergebnisse zwischen 6,0 und 6,4 US-Dollar pro Aktie realistisch.

Auf der anderen Seite gibt es die zyklischen Risiken, die Airlines verlässlich begleiten. Höhere Kerosinpreise, regulatorische Eingriffe oder erneute Verzögerungen im Flottenprogramm können die operative Marge belasten und das Wachstum temporär drücken. Unter diesen Bedingungen bewegt sich das Ergebnis eher zwischen 3,8 und 4,2 US-Dollar – ein Bereich, der historisch gut durch vergleichbare Jahre gedeckt ist.

Die drei Szenarien führen mich in der Summe durch Gewichtung der 3 Szenarien zu einem Zielwert nahe 66 bis 67 US-Dollar:

- Bullish (25 %, Eintrittswahrscheinlichkeit: eigene Einschätzung):

- EPS 6,0–6,4 USD → Kursziel 90–102 USD

- Neutral (50 %, Eintrittswahrscheinlichkeit: eigene Einschätzung):

- EPS 5,0–5,3 USD → Kursziel 60–70 USD

- Bearish (25 %, Eintrittswahrscheinlichkeit: eigene Einschätzung):

- EPS 3,8–4,2 USD → Kursziel 35–42 USD

Aus HQR-Perspektive ist Ryanair eindeutig als Qualitätswert einzustufen: hohe Kapitalrenditen, robuste Bilanz, starke operative Struktur. Das Under-the-Radar-Potenzial bleibt gering, da der Markt das Unternehmen seit Jahren kennt und die Kennzahlen weitgehend transparent sind. Im 10B-Modell zeigt sich das gleiche Muster: ein klarer Burggraben, aber kein struktureller Hebel für eine Neubewertung. Ryanair ist effizient, stabil und vorhersehbar – aber nicht strukturell unterbewertet.

Für mich ergibt sich daraus kein unmittelbarer Kauf. Die Bewertung ist fair, nicht günstig. Die operative Stärke ist sichtbar und wird entsprechend honoriert. Ryanair bleibt ein hochwertiger Wert, der erst bei einem attraktiveren Einstiegsniveau mit einem ausreichenden Sicherheitspuffer interessant wird. Bis dahin bleibt die Aktie für mich ein Watchlist-Kandidat.

1616

8 Kommentare

Mein Lieber,

Deinen Beitrag lese ich mir später durch.

@SAUgut777 hat eine Idee um Beiträge zu sammeln. In einer Art Lexikon.

Darf er deine tollen Beiträge auch integrieren und würdest du ihm vielleicht helfen.

Dann setz dich bitte mit ihn in Verbindung.

Desweiteren habe ich dich auf die Berater Liste , für Multiples und Kennzahlen gesetzt . Bist du damit einverstanden?

Deinen Beitrag lese ich mir später durch.

@SAUgut777 hat eine Idee um Beiträge zu sammeln. In einer Art Lexikon.

Darf er deine tollen Beiträge auch integrieren und würdest du ihm vielleicht helfen.

Dann setz dich bitte mit ihn in Verbindung.

Desweiteren habe ich dich auf die Berater Liste , für Multiples und Kennzahlen gesetzt . Bist du damit einverstanden?

•

11

•

1J.·

Analysten-Updates, 05.11.

⬆️⬆️⬆️

- ODDO BHF erhöht das Kursziel für BIONTECH von 110 USD auf 130 USD. Outperform. $BNTX (-0,66 %)

- BARCLAYS erhöht das Kursziel für AIRBUS von 161 EUR auf 165 EUR. Overweight. $AIR (+0,7 %)

- CITIGROUP erhöht das Kursziel für SCOUT24 von 91 EUR auf 94,50 EUR. Buy. $G24 (-1,09 %)

- WARBURG RESEARCH erhöht das Kursziel für REDCARE PHARMACY von 174 EUR auf 176 EUR. Buy. $RDC (-1,28 %)

- DEUTSCHE BANK RESEARCH erhöht das Kursziel für RYANAIR von 17 EUR auf 17,50 EUR. Hold. $RYA (-2,81 %)

- BERNSTEIN stuft EBAY von Market-Perform auf Outperform hoch. Kursziel 70 USD. $EBAY (+0,4 %)

- ODDO BHF erhöht das Kursziel für SALZGITTER von 14 EUR auf 15,50 EUR. Underperform. $SZG (+1,41 %)

- BARCLAYS erhöht das Kursziel für COMMERZBANK von 16 EUR auf 17 EUR. Equal-Weight. $CBK (+0,72 %)

- BARCLAYS erhöht das Kursziel für MTU von 295 EUR auf 340 EUR. Equal-Weight. $MTX (-0,74 %)

- MORGAN STANLEY stuft LUFTHANSA auf Equal-Weight hoch. Kursziel 7 EUR. $LHA (-10,84 %)

- BERENBERG erhöht das Kursziel für DEUTSCHE KONSUM REIT von 3,50 EUR auf 5 EUR. Hold.

⬇️⬇️⬇️

- GOLDMAN senkt das Kursziel für MERCEDES-BENZ von 65 EUR auf 63 EUR. Buy. $MBG (-1,09 %)

- UBS senkt das Kursziel für 1&1 von 21,60 EUR auf 21 EUR. Buy.

- WARBURG RESEARCH senkt das Kursziel für GFT TECHNOLOGIES von 40 EUR auf 37,50 EUR. Buy. $GFT (-0,74 %)

- HAUCK AUFHÄUSER IB senkt das Kursziel für ECKERT & ZIEGLER von 63,50 EUR auf 55 EUR. Buy. $EUZ (+0,66 %)

- BARCLAYS senkt das Kursziel für BNP PARIBAS von 90 EUR auf 85 EUR. Overweight. $BNP (-0,65 %)

- BERENBERG stuft SCHNEIDER ELECTRIC von Buy auf Hold ab und senkt Kursziel von 261 EUR auf 255 EUR. $SU (+1,42 %)

- BERENBERG senkt das Kursziel für BEFESA von 41 EUR auf 31 EUR. Buy. $BFSA (-0,57 %)

77

2J.·

Wie jeden Sonntag die wichtigsten Nachrichten der letzten Woche, sowie die wichtigsten Termine der kommenden Woche.

Auch als Video:

https://youtube.com/shorts/N2Ux73t4Z70?si=qkahQMBuwcfTOfpx

Montag:

Erneutes Auftragsplus für die deutsche Industrie, im September zogen die Aufträge um 0,2 % an. Erwartet wurde ein Rückgang von einem Prozent. Allerdings mussten die Augustzahlen deutlich nach unten korrigiert werden. Zudem entwickeln sich verschiedene Branchen sehr unterschiedlich. Beim Maschinenbau läuft es deutlich besser als beim Fahrzeugbau.

Die Stimmung in den Unternehmen sackt auf das niedrigste Niveau seit 2020 ab. Der Einkaufsmanagerindex fiel auf den Wert von 46,5 Zähler. So schlecht wie seit 35 Monaten nicht mehr. Weniger als 50 Punkte signalisieren eine wirtschaftliche Schrumpfung.

$RYA (-2,81 %) Ryanair erzielt einen Rekordgewinn und führt eine reguläre Dividende ein. Es sollen zukünftig immer 25 % des Gewinns ausgeschüttet werden. Bisher gab es nur Sonderdividenden. Das Unternehmen profitiert von einer hohen Nachfrage und erwartet für das Geschäftsjahr einen Gewinn zwischen 1,85 und 2,05 Milliarden EUR.

$BNTX (-0,66 %) Biontech bleibt trotz einem Einbruch der Nachfrage nach Impfstoffen profitabel. Im Q3 konnte ein Gewinn von 161 Millionen EUR erzielt werden. Die Umsatzprognose für 2023 wird von 5 auf 4 Milliarden EUR reduziert.

Dienstag:

$EVK (+2,38 %) Evonik macht mit 4,9 Milliarden EUR 23 % weniger Umsatz als im Vorjahresquartal. Unter dem Strich stand ein Verlust von 96 Millionen EUR. Die Prognose wird aufrechterhalten.

Im Gegensatz zu den anderen westlichen Industrienationen erhöht Australien die Leitzinsen auf 4,35 %. Die Inflation bleibt hartnäckig und ist noch nicht in dem Bereich von 2 - 3 %.

https://www.ft.com/content/60aa314b-b8e2-4299-ac0e-d212f6d1ae0b

$O2D (-0,89 %) Telefonica Deutschland wird von der Muttergesellschaft vollständig übernommen. Dadurch springt die Aktie nochmal an. Die spanische Mutter bietet den Minderheitaktionären in diesem Squeeze-Out einen Preis von 2,35 EUR pro Aktie. Ein Premium von mehr als 37 % auf den vorherigen Kurs.

Mittwoch:

$BAYN (+3,66 %) Bayer enttäuscht bei den Quartalszahlen. Statt einem erwartetem EBITDA von 1,725 wurden es nur 1,685 Milliarden EUR. Der Umsatz bricht um 8 % wegen der schlechter laufenden Agrarsparte ein. Bayer hält trotzdem weiter an der Prognose fest. Wir halten weiter an Bayer in unserem öffentlichen Portfolio fest, schlechter kann es fast nicht mehr laufen.

Der $DHL (+0,09 %) DHL Group wurden von Analysten konservative Prognosen unterstellt. Allerdings waren sie wohl nicht konservativ genug. Die Gruppe musste die Prognose kürzen. Das maximale EBIT liegt für 2023 jetzt nur noch bei 6,6 Milliarden EUR. Der Umsatz sank im dritten Quartal fast um ein Fünftel auf 19,4 Milliarden EUR.

Die Einzelhandelsumsätze in der EuroZone gehen weiter zurück. Im September waren es 0,3 % weniger, erwartet wurden 0,2 % weniger. Trotzdem konnte die Börse heute eine bisher erfolgreiche Trendwende fortsetzen.

https://stock3.com/news/eur-usd-eu-einzelhandelsumsaetze-gehen-zurueck-13542061

Donnerstag:

In China bleibt die Inflation weiterhin auf einem niedrigen Niveau. Laut dem Nationalen Statistikamt bei einer Kerninflation von 0,6 % (ohne Lebensmittel und Kraftstoffe). Zudem stiegen die Importe deutlich an, die Exporte schrumpften. Zum ersten Mal überhaupt waren die ausländischen Direktinvestitionen negativ. Die Zeiten, in denen chinesische Investoren jede Woche ein neues Unternehmen aufkaufen, scheinen vorerst vorbei zu sein.

https://www.n-tv.de/wirtschaft/der_boersen_tag/Anstieg-der-Inflation-in-China-article24519017.html

Die Ankündigung von $ADYEN (+2,16 %) Adyen profitabler zu werden, beflügelte am Donnerstag die Aktie.

Der Fed Chef Jerome Powell erklärte bei einer Rede auf der IWF-Tagung, dass die Währungshüter nicht überzeugt sind, dass die Zinsen ausreichend restriktiv sind. Heißt es kann durchaus weitere Zinserhöhungen geben. Das drückte die Stimmung an der Börse.

Freitag:

Die $ALV (+0,03 %) Allianz macht deutlich weniger Gewinn. Der operative Gewinn brach um 14,6 % auf 3,5 Milliarden EUR im abgelaufenen Quartal ein. Hauptursache sind Unwetter im Alpenraum im Sommer.

$JUN3 (+0,48 %) Jungheinrich nur noch mit leicht steigendem Auftragseingang. Analysten hatten mehr erwartet. Das EBIT sank um 1 % auf 103 Millionen EUR.

Schlechte Verbrauchervertrauendaten aus den USA, der Wert lag bei 60,4, erwartet wurden 63,7. Grund sind vor allem höhere Inflationserwartungen der Verbraucher.

Die wichtigsten Termine der kommenden Woche:

Montag: 11:00 Wachstumsprognose (EU)

Dienstag: 11:00 Konjunkturerwartungen (DE)

Mittwoch: 03:00 Einzelhandelsumsätze (China)

Donnerstag: 14:30 Herstellungsindex (USA)

Freitag: 14:30 Baugenehmigungen (USA)

33

2 Kommentare

2J.

Montag

Q3: Bilfinger, Hypoport, Talanx, Energiekontor, Jost Werke, Encavis

Dienstag

US/Verbraucherpreise Oktober

DE/ZEW-Index Konjunkturerwartungen November

DE/Produktion im produzierenden Gewerbe September

Q3: TAG Immobilien, K+S, RWE, Varta, Delivery Hero, Adesso, Indus Holding, Eckert & Ziegler, Allgeier

Mittwoch

Q3: SFC Energy, Dermapharm, Leifheit

Q4: Siemens Energy, Infineon Technologies

Donnerstag

Q4: Siemens

London Stock Exchange Kapitalmarkttag (2 Tage)

Freitag

EU/Verbraucherpreise Oktober

DE/Baugenehmigungen September

DE/Kleiner Verfallstag für Aktien- und Indexoptionen

Q3: Bilfinger, Hypoport, Talanx, Energiekontor, Jost Werke, Encavis

Dienstag

US/Verbraucherpreise Oktober

DE/ZEW-Index Konjunkturerwartungen November

DE/Produktion im produzierenden Gewerbe September

Q3: TAG Immobilien, K+S, RWE, Varta, Delivery Hero, Adesso, Indus Holding, Eckert & Ziegler, Allgeier

Mittwoch

Q3: SFC Energy, Dermapharm, Leifheit

Q4: Siemens Energy, Infineon Technologies

Donnerstag

Q4: Siemens

London Stock Exchange Kapitalmarkttag (2 Tage)

Freitag

EU/Verbraucherpreise Oktober

DE/Baugenehmigungen September

DE/Kleiner Verfallstag für Aktien- und Indexoptionen

•

22

•2J.·

Jooo,

Wollte mal wissen welches Unternehmen ihr interessanter findet und allenfalls investiert seid. Und zwar geht es um die Fluggesellschaften $LHA (-10,84 %) und $RYA (-2,81 %) . Es würde mich einfach mal interessieren was ihr von den Unternehmen haltet und was ihr über die Konzerne denkt. Vielen Dank für eure Antworten und einen wunderschönen Abend.

mfG

3J.·

Wie jeden Sonntag die wichtigsten Nachrichten der letzten Woche und die Termine der nächsten Woche.

Die Termine der nächsten Woche als Video:

https://youtube.com/shorts/Z2rjD3rE6NY?feature=share

Montag:

$RYA (-2,81 %) Ryanair profitiert von der wieder steigenden Reiselust. Im 2. Quartal legte der Gewinn deutlich zu. Auf einen Überschuss von 663 Millionen Euro. Vor einem Jahr lag der Gewinn noch bei 188 Millionen Euro. Trotzdem rechnet Ryanair mit weniger Gästen im Gesamtjahr. Grund seien Liefer-Verzögerungen neuer Jets von Boeing.

Schlechte Gewerbedaten aus Deutschland, es läuft aktuell einfach nicht mehr. Der Einkaufsmanagerindex fällt noch schlechter aus als gedacht. Der Index beim verarbeitenden Gewerbe fällt auf 38,8 (Prognose: 41). Der schlechteste Wert seit 38 Monaten. Auch im Dienstleistungssektor fällt das Ergebnis schlechter aus als gedacht. Die Industrie verkleinert nun die Belegschaft, im Dienstleistungssektor wird zumindest weniger eingestellt.

https://finanzmarktwelt.de/deutsche-wirtschaft-industrie-weiter-im-freien-fall-277800/

Neues Logo für $0QZBl Twitter, statt dem Vogel zukünftig das ‚X‘. Elon Musk hat mal wieder den Vogel abgeschoßen. Twitter gerät unter anderem durch den erfolgreichen Start von Threads unter Druck. Der Meta-Konzern konnte mit dem Twitter Pendant in kürzester Zeit mehr als 100 Millionen Nutzer gewinnen.

$ADS (-3,27 %) Adidas schneidet wohl besser ab als gedacht. Der Konzern erhöht jetzt die Prognose, Grund war ein erfolgreicher Ausverkauf der Yeezy-Kollektion. Der Umsatz wird weniger stark sinken als gedacht, der Betriebsverlust weniger groß als gedacht.

$BAYN (+3,66 %) Bayer bricht kurzfristig ein. Die Prognose musste wegen den Glyphosat Verkäufen eingestampft werden. Glyphosat bleibt das größte Risiko für Bayer. Der FCF soll dieses Jahr auf 0!!! statt 3 Milliarden Euro sinken.

Allerdings ist so ein Verhalten typisch nach einem CEO Wechsel. Auch bekannt als ‚Cleaning the Desk‘ der neue CEO packt alles Schlechte ins Antrittsjahr, schiebt die Schuld auf den Vorgänger und steht dann im Nachhinein richtig gut da, weil man das Unternehmen auf Kurs gebracht hat.

dpa-AFX ProFeed

Dienstag:

Das Geschäftsklima in Deutschland verschlechtert sich deutlich. Das ifo-Barometer sank auf 87,3 Punkte, 88 Punkte waren erwartet worden. Bereits jetzt befindet sich Deutschland in einer Rezession. Für Donnerstag wird trotzdem mit einer weiteren Zinserhöhung durch die EZB gerechnet. Allerdings könnte diese, bei solchen Daten, erstmal die Letzte gewesen sein.

#china aktien ziehen deutlich an. Grund ist nicht das plötzliche Verschwinden des Außenministers Qin Gang, der durch den Vorgänger Wang Yi ersetzt wird. Sondern ein angekündigtes Konjunkturprogramm. So soll der Konsum angekurbelt werden, Hilfen für Unternehmen sollen zur Verfügung gestellt werden und der Immobiliensektor soll stabilisiert werden. Exakte Details sind allerdings bisher nicht bekannt.

https://amp.cnn.com/cnn/2023/07/25/economy/china-politburo-economy-hnk-intl/index.html

Als Folge der Zinswende haben Unternehmen deutlich weniger Kredite aufgenommen. Das geht aus einer EZB-Survey hervor. Vor allem Investitionsdarlehen gingen stark zurück. Ein weiteres Alarmsignal aus der Wirtschaft. Am stärksten betroffen vom Rückgang bei den Krediten unter den vier großen Volkswirtschaften in der EU war Italien. Banken rechnen im dritten Quartal mit einem weiteren Rückgang.

Prognoseerhöhungen der $DB1 (+0,28 %) Deutschen Börse und von $RWE (+0,26 %) RWE. Beide Unternehmen erwarten ein besseres Ergebnis für das Gesamtjahr.

Auch $GOOGL (-0,75 %) Alphabet und $MSFT (-1 %) Microsoft liefern Zahlen über den Erwartungen.

Mittwoch:

Auch die $DBK (+0,09 %) Deutsche Bank übertrifft die Analystenerwartungen. Im 1. Halbjahr wurde ein Vorsteuergewinn von 3,3 Milliarden EUR erzielt, das beste Ergebnis seit 2011. Es wurde zudem ein Aktienrückkaufprogramm über 450 Millionen EUR angekündigt.

$P911 (-1,57 %) Porsche verdient etwas mehr als gedacht, allerdings verkauft sich der Taycan nicht gut in China. Auch der elektrische Macan kann noch nicht verkauft werden. Trotz guter Zahlen und Prognosebestätigung geht es daher erstmal etwas runter an der Börse.

$VOW3 (-1,3 %) Volkswagen beteiligt sich mit 5 % bei XPENG, die Aktie macht einen gewaltigen Sprung nach oben. Mit XPENG möchte man Autos entwicklen, insbesondere für den chinesischen Markt. Audi hat in den letzten Tagen bereits eine Kooperation mit SAIC verkündet. Die Beteiligung hat sich auf jeden Fall schonmal gerechnet für VW. Nach Verkündung legte die Aktie um 30 % zu.

Die #fed at den Leitzins auf eine Spanne von 5,25 - 5,50 % erhöht. So hoch wie seit 22 Jahren nicht mehr. Die Inflation liegt in den USA mittlerweile auf 3,0 %. Nur 1 Prozentpunkt von der Zielmarke 2,0 % entfernt. Zunächst gab es keine wirkliche Reaktion. Auch in der Pressekonferenz ließ Jerome Powell das weitere Vorgehen offen. Es kann also auch im September zu einer weiteren Zinserhöhung kommen.

Auch $MBG (-1,09 %) Mercedes erhöht die Jahresprognose und dürfte damit einige Anleger auf dem falschen Fuß erwischt haben. Viele Marktteilnehmer haben eher mit Prognosesenkungen im Automobilsektor gerechnet.

Auch $META (-0,9 %) Meta liefert ab. Der Konzern steckt noch im Winter im Dornröschenschlaf, jetzt scheinen die Wachstumsfantasien wieder erwacht zu sein. Auch hier wurde die Prognose erhöht.

https://stock3.com/news/meta-uebertrifft-die-erwartungen-12783323

Donnerstag:

Anders als bei Mercedes ist die Situation bei VW. Der Gewinn steigt zwar weiter an, allerdings wird die Absatzprognose gekappt. Gewinn und Umsatz sollen so wie geplant erreicht werden. Im 2. Quartal hat der Umsatz um 15 % auf 80 Milliarden EUR zugelegt.

$KGX (+0,8 %) erhöht die Prognose erneut. Das EBIT legt um 11,7 % im Vergleich zum Vorjahr zu. Der Umsatz steigt um 1,5 %. Auch der Cash Flow ist deutlich verbessert, es konnten Schulden reduziert werden. Eine Kapitalerhöhung scheint damit vom Tisch.

https://www.nebenwerte-magazin.com/kion-group-steigert-profitabilitaet/

Auch die EZB erhöht den Leitzins um 0,25 Prozentpunkte. Damit liegt der Leitzins im Euro-Raum bei 4,25 %. Die Kurse legten direkt nach der Verkündung deutlich zu. Vermutlich wurden einige Shorts als Absicherung aufgelöst.

Die Präsidentin lässt offen was im September passieren wird. Sie betont allerdings, dass basierend auf neuen Daten entschieden wird. Sie betont ebenfalls, dass man dieses Mal bewusst sagt, dass man nicht noch weitere Schritte gehen muss. Der aktuelle Leitzins könnte also ausreichen um die Inflation einzuschränken. Ob es wirklich schon die letzte Zinserhöhung war hängt von der weiteren Inflationsentwicklung ab. Viel spricht dafür, dass es die letzte Zinserhöhung in diesem Zinszyklus war. Vielleicht kommt es allerdings noch überraschend zu Preistreibern in den nächsten Wochen.

https://www.ecb.europa.eu/press/pressconf/press_conference/html/index.de.html

Freitag:

Keine wirkliche Zinserhöhung in Japan 🇯🇵 allerdings ein Schritt weg von der ultralockeren Zinspolitik. In Japan steuert die Zentralbank die Zinsen der Staatsanleihen. Offiziell liegt die Zinskurve hier bei 0,5 %, jetzt will man Zinsen bis 1,0 % zulassen. Der Leitzins bleibt weiter bei -0,1 %.

$INTC (+2,97 %) Intel überzeugt bei den Quartalszahlen. Sowohl Umsatz- als auch Gewinnrückgang lagen unter den Erwartungen. Die Aktie konnte daher deutlich zulegen.

Wichtigste Termine der kommenden Woche:

Montag: 11:00 Verbraucherpreise (EURO)

Dienstag: 16:00 Gewerbedaten (USA)

Mittwoch: 14:15 Beschäftigungszahlen (USA)

Donnerstag: 13:00 Zinssatzentscheidung (UK)

Freitag: 11:00 Einzelhandelsumsätze (EURO)

www.handelsblatt.comRyanair mit Gewinnsprung

1111

3J.·

In den letzten Wochen ist die Debatte, ob man lieber mit dem Zug oder Bus in den Urlaub fährt, statt mit dem Flieger, nochmal größer geworden. Umso erstaunlicher sind die Zahlen von Ryanair für das 2. Quartal!

Im 1. Geschäftsquartal erzielte Ryanair einen Gewinn von 663 Millionen Euro - das war sogar noch mehr als von den Analysten erwartet! Der hohe Gewinn ist unter anderem von den gestiegenden Ticketpreisen erzielt worden. Die Ticketpreise sind im Jahresvergleich um durchschnittlich 42% gestiegen.

Auch die Auslastung der Flugzeuge hat sich verbessert und der Umsatz ist um ganze 40% auf 3,65 Milliarden Euro gestiegen.

Aber trotz dieser guten Zahlen ist die Ryanair-Aktie zeitweise um knapp 4% gesunken. Vielleicht hat das mit den gedämpften Aussichten für das Gesamtgeschäftsjahr bis Ende März 2024 zu tun, da sie nun nur noch mit einem Wachstum auf 183,5 Millionen Fluggäste rechnen, statt den zuvor angepeilten 185 Millionen.

RyanAir wäre für mich trotz der guten Zahlen kein Invest. Wie seht ihr das? Findet man die $RYA (-2,81 %) Aktie in eurem Portfolio?

3 Kommentare

Fluglinien Aktien sucht man bei den meisten glaub ich vergebens -

•

11

•

3J.·

Zeit, die $RYA (-2,81 %) Aktien zu verkaufen... 😏

Achtung Message Control 😉

www.derstandard.atEx-Ministerin Köstinger heuert bei Ryanair an

44

5 Kommentare

Die Netzwerke scheinen noch intakt zu sein 🫣🥺

•

22

•

3J.·

+++ Am Bevölkerungswachstum profitieren +++

Servus Börsianer,

Weltweit sind wir mittlerweile 8. Milliarden Menschen die täglich Konsumieren, und es kommen jährlich 80 Millionen hinzu. Zusätzlich durchleben viele Nationen einen demographischen Wandel, welches erneut Chancen und Risiken mit sich bringt.

Wie kann man an diesem Trend profitieren?

Grundsätzlich profitiert, nahezu jeder Sektor von einer wachsenden Bevölkerung, jedoch gibt es Sektoren die an diesem Trend stärker profitieren.

Gesundheitsbranche:

Demographischer Wandel und ein stetiger Ausbau vom Gesundheitssystem führt zu einem starken Wachstumssektor in der Zukunft.

Hieran profitieren beispielsweise Unternehmen wie $PFE (-0,25 %) durch ihre Impfstoffe in der Zukunft oder $HIMS (+0,04 %) durch die Digitalisierung des Gesundheitswesens. Zusätzlich steigt die Nachfrage von Krankenhäuser hierdurch profitiert $MPW (+0,33 %) oder eine steigende Anzahl von Diabetes - Patienten mit $NVO (+0,59 %) und einer Nachfrage von Medikamenten $BAYN (+3,66 %) .

Lebensmittelindustrie (Konsumbranche):

Durch eine steigende Anzahl der Bevölkerung wird mehr Konsumiert bsp. Lebensmittel von $PEP (-0,3 %) & $KO (-0,59 %) oder Hygieneartikel von $ULVR (-1,05 %) & $PG (-0,58 %) .

E-Commerce:

Höhere Bevölkerung = mehr potenzielle Käufer $SHOP (-0,71 %) & $AMZN (-1,13 %)

Reisebranche:

Dazu gibt es zahlreiche Unternehmen die am Tourismus profitieren wie $RYA (-2,81 %)

$TUI1

$LHA (-10,84 %)

Diese Liste, kann man weiterhin ausbauen, aber die Kernaussagen ist erkennbar.

(Negative Schlußfolgerung -> Bevölkerungsrückgang)

Investiert ihr bereits in die Gesundheitsbranche?

🦍 = Ja, klar

🆘 = Nein

66

9 Kommentare

Man kann aus einer bestehenden Nachfrage nicht automatisch Profit bestimmter Firmen folgern. Da gibt es ja auch eine Reihe von Begleitumständen, die erst mal erfüllt werden müssen, um eine Nachfrage zu bedienen.

Tatsächlich findet beispielsweise in den USA gerade ein Krankenhaussterben statt, weil die steigenden Kosten teilweise nicht mehr bezahlt werden können. Hinzu kommt, dass ebenso wie hier ein massiver Mangel an Gesundheits- und Pflegepersonal herrscht. Da kann also noch so eine große Nachfrage an Krankenhäusern bestehen - wenn die Kosten dafür nicht getilgt werden können und kein Personal da ist, dann gibt es auch keine neuen Krankenhäuser.

Tatsächlich findet beispielsweise in den USA gerade ein Krankenhaussterben statt, weil die steigenden Kosten teilweise nicht mehr bezahlt werden können. Hinzu kommt, dass ebenso wie hier ein massiver Mangel an Gesundheits- und Pflegepersonal herrscht. Da kann also noch so eine große Nachfrage an Krankenhäusern bestehen - wenn die Kosten dafür nicht getilgt werden können und kein Personal da ist, dann gibt es auch keine neuen Krankenhäuser.

•

55

•Meistdiskutierte Wertpapiere

Top-Creator dieser Woche

Echtzeitdaten von LSX · Fundamental- & EOD-Daten von FactSet