$PLTR (+14,84%)

$SNAP (+5,46%)

$HSBA (-1,3%)

$9434 (-1,71%)

$ZAL (-13,64%)

$BOSS (+0,39%)

$BNTX (-1,53%)

$SPOT (-1,41%)

$BP. (-3,82%)

$BAYN (+1,64%)

$DOCN (+0,31%)

$MCD (-0,11%)

$CAT (+4,97%)

$PFE (+0,58%)

$ANET (+2,9%)

$PINS (+4,23%)

$SPCX (+8,78%)

$AMD (+6,04%)

$PARA (+2,11%)

$LUMN (+3,72%)

$KTOS (+2,79%)

$CPNG (+1,92%)

$IFX (+3,93%)

$ENR (+3,4%)

$DHL (+0,43%)

$NOVO B (-6,23%)

$CVS (-1,49%)

$UBER (-0,02%)

$SEDG (+7,64%)

$WULF (-1,02%)

$CRCL (+4,55%)

$SHOP (+4,06%)

$DIS (-0,78%)

$HUBS (+3,1%)

$DASH (+0,78%)

$FSLY (+7,98%)

$SNDK (+9,78%)

$MELI (-0,57%)

$DUOL

$APP (+2,21%)

$SMR

$FIG (+8,16%)

$SIE (+0,96%)

$CBK (+1,81%)

$IOS (+1,9%)

$FI (+2,06%)

$DDOG (+3,95%)

$RHM (+1,32%)

$QBTS (+9,09%)

$G24 (+0,63%)

$AKAM (+4,1%)

$MUV2 (-1,47%)

$UA (+0,78%)

$OKLO

Munich Re

Ação

Ação

ISIN: DE0008430026

Ticker: MUV2

DE0008430026

MUV2

Price

Discussão sobre MUV2

Postos

2132D·

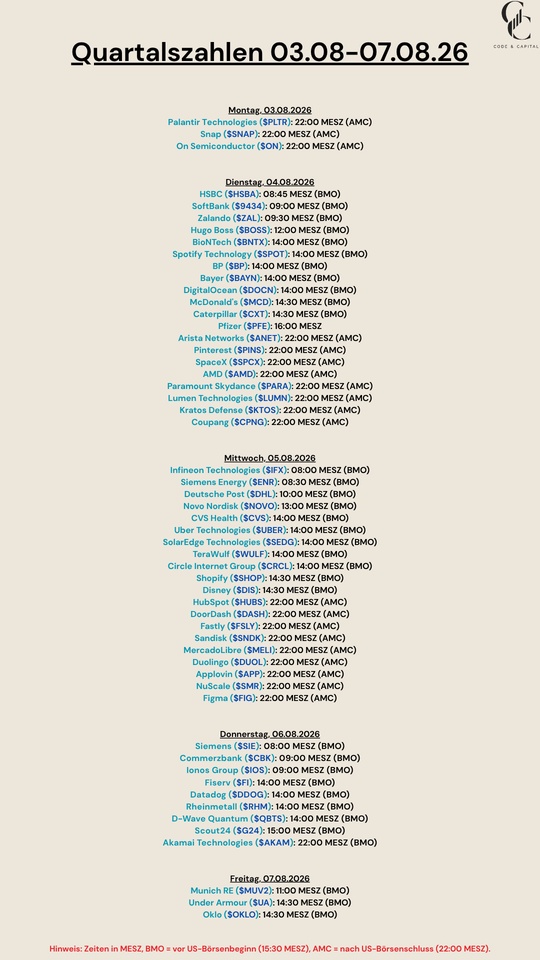

Quarterly Results August 3–7, 2026

1212

3D·

Monthly Review 07/2026

Another month has passed, and it’s time once again to take a quick look into the engine room...

...actually, not much has changed in the big picture, except that after 38 months of consistent performance, the 40k mark has been broken, and so the final sprint of the first half has now begun...

...it’s not a high-flyer portfolio, but so far it’s been a solid growth story, and as the saying goes, every little bit helps...

...which is why YTD hasn’t changed much either...

...nor has it since the very beginning...

...the structure, however, is a different story, and so there were a few changes to the portfolio this month...

》New Additions《

$WINC (+1%) 244.01x

$AII (+4,85%) 101x

》Exits《

$EVD (-0,21%) 25x

》Top 3《

$HAUTO (-1,03%) +24.42% (+122.67%)

$VAR (-0,45%) +19.82% (+60.72%)

$DTE (-0,75%) +10.61% (-1.53%)

》Flop 3《

$3750 (+4,66%) -10.58% (+128.32%)

$ASWM (+2,25%) -9.86% (+17.84%)

$YYYY (+2,47%) -7.01% (-4.80%)

》Dividends《

This month, there were €252.24 in net dividends, representing a 12.24% increase year-over-year.

》CONCLUSION《

Everything’s business as usual, so we can relax and prepare for next Friday’s upcoming DATEV certification 👍🏻

I wish everyone continued success, and may dividends and growth be on our side 🫡

3434

7 Comentários

Brian@Aktienhauptmeister

3D

•

66

•

3D·

Partial sale: 50%

I had bought the stock back then during the Trump tariff dip. I didn't foresee how things would turn out now either, but I certainly thought the bashing of Dell at the time was completely over the top.

Half of it has $MUV2 (-1,47%) gone

1Semana·

Munich Re Significantly Exceeds Expectations in Q2 – €2.2 Billion in Profit

• Preliminary Q2 net income of approximately €2.2 billion clearly exceeded the analyst consensus of €1.786 billion.

• This was driven by very low major loss charges in property and casualty reinsurance and very strong investment results. ERGO posted a net profit of approximately €0.3 billion.

• With a first-half profit of approximately €3.9 billion, Munich Re believes it is on track to achieve its annual profit target of €6.3 billion for 2026.

3333

6 Comentários

Great news! My algo considers it cheap for some time. And I am invested since march-april, currently at +10%

Let's hope the up trend continues.

Let's hope the up trend continues.

•

22

•

3Semana·

Hasen's Investment in a Reinsurer

Dear gq community,

Today I munched on my remaining carrots and added 2 more shares of $MUV2 (-1,47%) for €508.80, thereby doubling my investment.

As soon as I have fresh carrots again after buying a car, I’ll increase the position to a total of 3% of the portfolio’s value. 🥕🥕🥕

Your Bunny

4343

9 Comentários

3Semana

I actually have Allianz in my portfolio myself, but I think you definitely can't go wrong with $MUV2! And you get a nice dividend on top of that 😉

•

66

•

3Semana·

Munich Re Stock in 2026: Down 19% from All-Time High — Is the Market Ignoring the World’s Most Profitable Insurer?

Munich Re (known internationally as Munich Re) is the world’s most profitable reinsurer—and the market seems to be simply ignoring it. P/E ratio of 9, dividend of 24 EUR per share, profit target of 6.3 billion EUR confirmed, Moody’s upgrades the financial strength rating to Aa2 — and yet the stock is trading 19% below its all-time high. Is this a classic case of market overreaction? Q1 2026 was historically strong: consolidated net income up 57% to 1.714 billion EUR, return on equity 19.7%, market capitalization 71.2 billion EUR. The headwinds are real—$805 billion in excess capital is weighing on premiums. The July renewal cycle, which has just begun, will determine the stock’s price performance over the coming months. A first positive sign: On June 29, the stock crossed above the 50-day moving average. Munich Re has already repurchased over 1.1 million of its own shares since May.

Key points:

- Q1 2026: Group profit of EUR 1.714 billion (+57% YoY) — well above expectations

- Combined ratio: 66.8% — exceptionally strong

- Full-year forecast: EUR 6.3 billion net income — confirmed

- Share buyback: EUR 2.25 billion total program — over 1.1 million shares already repurchased

- Moody’s upgrade: Financial strength rating raised from Aa3 to Aa2

- Share price: approx. 495 EUR — −19% from all-time high (609.40 EUR, April 2025)

- Market capitalization: 71.2 billion EUR

- June 29, 2026: Crossed above the 50-day moving average — first technical buy signal

What are your current thoughts on $MUV2 (-1,47%) ??

2525

7 Comentários

3Semana

Hey Christian,

Great summary—you’ve raised an extremely interesting point here! Munich Re is and remains an absolute powerhouse in the insurance sector. When you look at the raw fundamentals from the first quarter, you really do have to rub your eyes in disbelief—why is the stock trading at nearly a 20% discount to its all-time high?

Let’s set aside the typical market noise and put the stock through a rigorous quality and cash flow check:

1. Operational Excellence & Risk Management

A combined ratio of 66.8% in Q1 isn’t just “strong” for a reinsurer—at this level, it’s absolutely world-class. It shows that Munich Re underwrites claims excellently and remains profitable even when the world is on fire. Moody’s upgrade to Aa2 underscores this almost frightening balance sheet strength. The fact that management has confirmed the profit target of 6.3 billion EUR actually provides the market with a solid safety net.

2. The Cash Flow and Shareholder Perspective

The EUR 2.25 billion share buyback program is a game-changer. The fact that over 1.1 million shares have already been repurchased since May provides sustained support for earnings per share (EPS) from the bottom up. Coupled with a dividend of 24 EUR, Munich Re delivers exactly the massive, reliable cash flow that long-term investors want to see as the foundation of their portfolio.

Why the Market Is Hesitating (The Macroeconomic Fly in the Ointment):

You’ve hit the nail on the head: The $805 billion in excess capital in the global reinsurance industry is a double-edged sword. The market is simply afraid of a “soft market” in which too much capital on the sidelines puts downward pressure on prices. The ongoing July renewal cycle is indeed the deciding factor here. If Munich Re can assert its pricing power there, the current discount is fundamentally hard to justify.

Conclusion:

The stock is currently a classic, oversold value opportunity. The fact that the 50-day moving average was broken to the upside on June 29 provides the appropriate technical momentum to complement the fundamental discount. Anyone looking for an absolutely boring but highly profitable cash asset for their income portfolio is, historically speaking, doing very little wrong at these prices.

Great summary—you’ve raised an extremely interesting point here! Munich Re is and remains an absolute powerhouse in the insurance sector. When you look at the raw fundamentals from the first quarter, you really do have to rub your eyes in disbelief—why is the stock trading at nearly a 20% discount to its all-time high?

Let’s set aside the typical market noise and put the stock through a rigorous quality and cash flow check:

1. Operational Excellence & Risk Management

A combined ratio of 66.8% in Q1 isn’t just “strong” for a reinsurer—at this level, it’s absolutely world-class. It shows that Munich Re underwrites claims excellently and remains profitable even when the world is on fire. Moody’s upgrade to Aa2 underscores this almost frightening balance sheet strength. The fact that management has confirmed the profit target of 6.3 billion EUR actually provides the market with a solid safety net.

2. The Cash Flow and Shareholder Perspective

The EUR 2.25 billion share buyback program is a game-changer. The fact that over 1.1 million shares have already been repurchased since May provides sustained support for earnings per share (EPS) from the bottom up. Coupled with a dividend of 24 EUR, Munich Re delivers exactly the massive, reliable cash flow that long-term investors want to see as the foundation of their portfolio.

Why the Market Is Hesitating (The Macroeconomic Fly in the Ointment):

You’ve hit the nail on the head: The $805 billion in excess capital in the global reinsurance industry is a double-edged sword. The market is simply afraid of a “soft market” in which too much capital on the sidelines puts downward pressure on prices. The ongoing July renewal cycle is indeed the deciding factor here. If Munich Re can assert its pricing power there, the current discount is fundamentally hard to justify.

Conclusion:

The stock is currently a classic, oversold value opportunity. The fact that the 50-day moving average was broken to the upside on June 29 provides the appropriate technical momentum to complement the fundamental discount. Anyone looking for an absolutely boring but highly profitable cash asset for their income portfolio is, historically speaking, doing very little wrong at these prices.

•

1919

•

4Semana·

New buys: Uber, Marriott, Waste Management, Arista Networks

New buys yesterday: $UBER (-0,02%)

$WM (-0,76%)

$MAR (-1,12%)

$ANET (+2,9%)

All four were already on my watchlist and are among the few quality names that, in my view, haven't run too hot or become excessively extended yet.

The common theme: solid relative strength, healthy price behaviour and more reasonable entry points than many of the market's strongest stocks right now.

I'm trying to avoid chasing extended leaders and instead build positions where the risk/reward still looks attractive.

Waiting for pullbacks: $LGEN (+0,25%)

$BRK.B (+0,43%)

$MUV2 (-1,47%)

Holding: $CGNX (+5,96%) (robotics)

33

1Mês·

Roast My Portfolio

A lot has happened since the last "Pants Down" post.

Portfolio grew from 70k to 125k

$BTC (-0,92%) has been sold off

Instead, individual stocks were purchased starting at 100k from the ETF portfolio

The goal of the individual stocks is to fill “gaps” in the ETFs

For example, $MUV2 (-1,47%) reinsurers are underrepresented in my portfolio

My criteria are

A very strong moat

Preferably an oligopoly or duopoly market structure

The company should be able to generate long-term earnings and have strong cash flow

After the $BTC (-0,92%) adventure, I’m simply investing in a boring and consistent manner

P.S.: The allocation of individual stocks has not yet reached target weights, and not every position has been included yet

P.P.S.: I’m aware that I’m excluding South Korea; honestly, when I look at the South Korean market, I don’t think that’s a bad thing

8Posições

€ 125.101,71

16,40%

1717

19 Comentários

Why choose the expensive MSCI World? A 0.5% TER is just not acceptable anymore 😢

•

55

•1Mês·

Too hot to ignore: Europe’s summer becomes a market signal

About an hour ago, I read a great article on my broker’s website here in Denmark (Saxo Bank), which I don’t want to keep from you, since I think it addresses an issue that many people may not be aware of.

Key Takeaways

- Europe’s heat wave is driving up demand for cooling and putting power grids to the test.

- The winners could include appliance manufacturers, grid equipment suppliers, and select utility companies.

- The risks lie in electricity prices, insurance claims, and the financial strain on households.

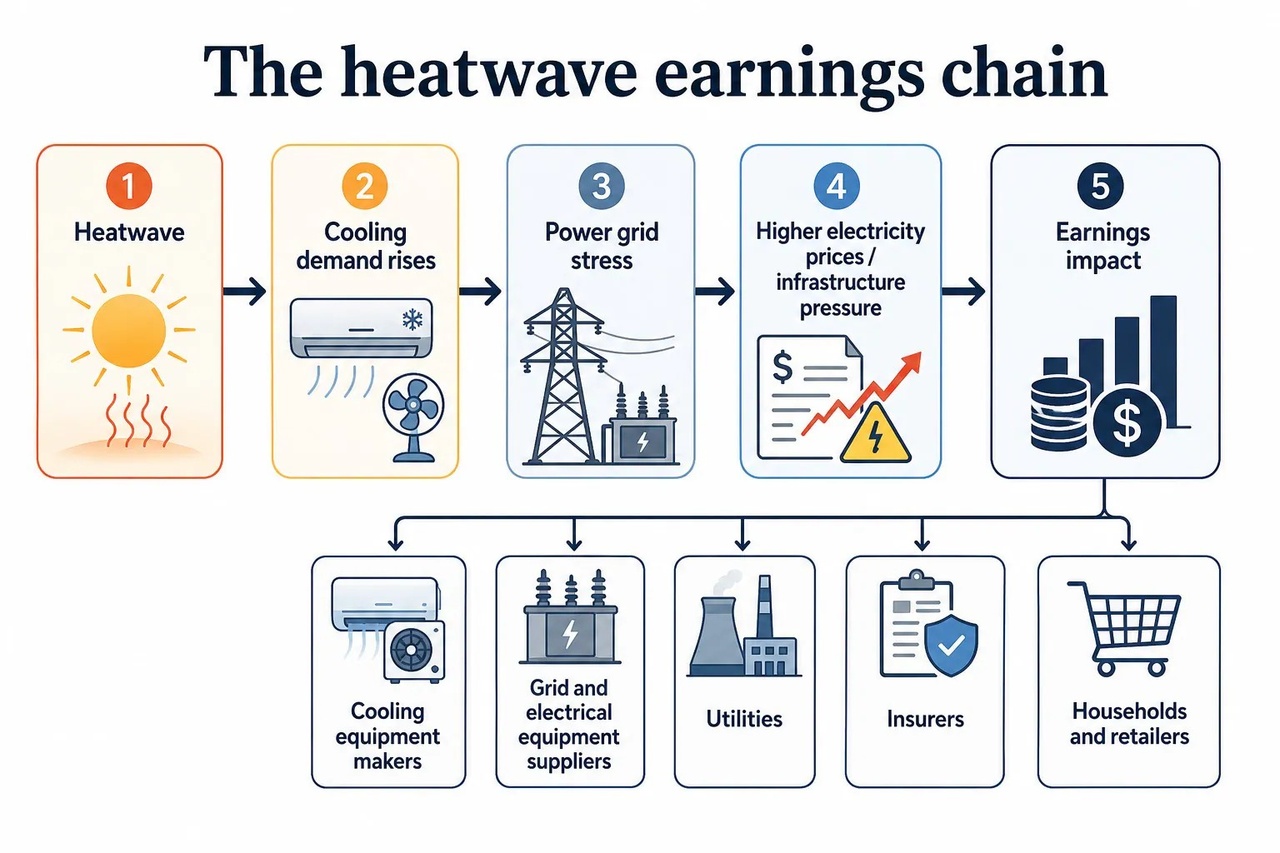

In late June 2026, Western Europe faced record-breaking heat, with countries such as France, Spain, Italy, and the United Kingdom under strain. Schools closed, traffic slowed, power systems were overloaded, and consumers rushed out to buy fans and air conditioners. Out on the streets, it’s simply unbearable. In the markets, this creates a simple chain of events: heat increases the need for cooling, cooling increases electricity consumption, electricity demand strains the grids, and grid strain alters earnings expectations.

For investors, it’s not about trading the thermometer. That’s a very small desk with a very hot seat. The point is to understand how extreme weather can translate from the weather map into revenue, costs, margins, and insurance losses.

The first winner is the power outlet The most obvious heat wave trade starts with cooling. Daikin $6367 (-4,58%) , Samsung Electronics $005930 and LG Electronics $066570 are clear examples. Daikin is a Japanese specialist in heating, ventilation, and air conditioning (HVAC). Samsung and LG are South Korean electronics conglomerates with large divisions dedicated to home appliances. When European households realize that a south-facing apartment can turn into a small oven, demand for cooling products rises rapidly.

That doesn’t mean every summer heat wave will lead to a sustained profit boom. Portable air conditioners are often low-margin products. Supply chains can become overburdened. End-consumer demand may wane when the weather changes. But the overall trend is hard to ignore. In the past, Europe has had a lower penetration rate of air conditioning compared to many warmer regions. As hot summers become more frequent, cooling could shift from a luxury purchase to a basic comfort product.

This also explains the building perspective. Legrand $LR (+2,74%) manufactures electrical and digital building infrastructure. Assa Abloy $ASSA B (+1,19%) manufactures locks, doors, and access systems. Kingspan produces insulation and building materials.

These companies are not purely “heat wave plays.” They are tied to the deeper question: How can buildings become more livable, efficient, and resilient?

A good building needs more than just a larger air conditioning system. It needs better insulation, smarter wiring, efficient controls, shading, doors, ventilation, and energy management. Otherwise, Europe risks solving the heat problem by creating an electricity bill problem. Very elegant—much like fixing a leaky roof by simply buying more buckets.

The grid is becoming a bottleneck

The second part of the story is electricity. Schneider Electric $SU (+3,31%) and Siemens Energy $ENR (+3,4%) are right at the center of this pressure point. Schneider Electric sells equipment for energy management, automation, and energy efficiency. Siemens Energy supplies grid technology, turbines, and energy infrastructure. When power grids are confronted with higher peak loads, more renewable energy, increasing electrification, and higher cooling demand, the value of grid investments is easier to justify.

For utilities, the picture is more mixed. E.ON $EOAN (+0,05%) and National Grid $NG. (+0,49%) are primarily grid operators. They earn their revenue mainly through the ownership and operation of regulated electricity and gas infrastructure. Heat waves can increase investment needs, as the grids must cope with higher peak loads, localized strains, and more complex power flows. For regulated utilities, the long-term opportunity lies in the fact that investments in resilient grids can support future asset growth. Those boring power lines suddenly take center stage.

RWE $RWE (-0,39%) , Enel $ENEL (+0,49%) and Iberdrola $IBE (+1,07%) have greater exposure to power generation. They own power plants and renewable energy facilities. High electricity prices can bolster the revenues of some generators, especially when supply is tight.

But heat can also be harmful. Nuclear power plants may have to curtail their output if river water becomes too warm for cooling. Low wind speeds can reduce renewable production. Droughts can impact hydropower. Gas-fired power plants can become the marginal source, meaning they dictate the price when demand is high and cheaper supply is insufficient.

So heat waves don’t simply mean “utilities win.” The details are crucial. Grid operators could benefit from the investment cycle. Generators could benefit from higher prices during certain hours, but face operational risks during others. Retail utilities could run into trouble if customers are hit with high bills and political pressure mounts. The weather may be hot, but the analysis must remain cool.

Insurance Companies Will Foot the Bill Later

The third level involves insurance companies. Munich Re $MUV2 (-1,47%) and Swiss Re $SREN (+0,34%) are reinsurers. Reinsurers insure insurers—which sounds like financial plumbing, because that’s exactly what it is. They help spread major risks (storms, wildfires, floods) across the system.

Heat waves can affect insurers in various ways. They can increase risks in the areas of health, agriculture, and business interruption. They can heighten the risk of wildfires. They can also expose weaknesses in infrastructure. For reinsurers, this can mean higher claims payouts in some years, but in the long run, it also leads to higher prices as risks become more visible and insurance buyers accept higher premiums.

That’s the strange logic of insurance: Bad weather hurts in the short term, but it supports better pricing later on. The umbrella industry doesn’t like storms, but storms remind everyone why umbrellas cost money.

Risks to Keep an Eye On

- Investors might overreact to a hot summer.

- Political risks: High electricity prices can trigger government intervention (excess profit taxes).

- Cost risks: Grid expansions, cooling equipment, insulation, and insurance all cost money. Customers might push back if household budgets are already stretched thin.

The Bottom Line Under the Sun

The “heat wave trade” isn’t about guessing next week’s temperature. It’s about recognizing where resilience translates into revenue, where strain leads to costs, and where the old European assumption of mild summers is no longer a reliable forecast. In the markets, just as in homes in July, heat is rarely dispelled simply by ignoring it.

Source: Saxo Bank / Saxo Trader – Ruben Dalfovo, Investment Strategist

and, of course, everyone else :)

2222

4 Comentários

Thank you so much for the great post.

I definitely know that I’ll be investing in an air conditioner for next season 😵💫🔥🔥. I took a look yesterday, but right now the units I need are basically all sold out or won’t be available for a long time. With this heat, I can barely think straight.

There are some interesting stocks in your portfolio, but right now I’m only invested in $MUV2 —and quite heavily there.

I got my fingers badly burned with the utilities (electricity) a very long time ago. Back then, I thought electricity would always be needed—and in increasing amounts. Then came the politically mandated phase-out of nuclear and coal power, and I ended up taking a big hit. My E.ON $EOAN and RWE $RWE investments completely tanked back then; only CEZ $CEZ, which was based abroad, fared better.

For my new foray into the utilities sector, I’m now focusing on water and building a position in Veolia $VIE. I expect this to be a good investment in the medium and long term—especially because water and wastewater networks, including supply lines and treatment plants, etc., exist only once in each locality. Therefore, I don’t really see the kind of competition here that exists among electricity providers.

I definitely know that I’ll be investing in an air conditioner for next season 😵💫🔥🔥. I took a look yesterday, but right now the units I need are basically all sold out or won’t be available for a long time. With this heat, I can barely think straight.

There are some interesting stocks in your portfolio, but right now I’m only invested in $MUV2 —and quite heavily there.

I got my fingers badly burned with the utilities (electricity) a very long time ago. Back then, I thought electricity would always be needed—and in increasing amounts. Then came the politically mandated phase-out of nuclear and coal power, and I ended up taking a big hit. My E.ON $EOAN and RWE $RWE investments completely tanked back then; only CEZ $CEZ, which was based abroad, fared better.

For my new foray into the utilities sector, I’m now focusing on water and building a position in Veolia $VIE. I expect this to be a good investment in the medium and long term—especially because water and wastewater networks, including supply lines and treatment plants, etc., exist only once in each locality. Therefore, I don’t really see the kind of competition here that exists among electricity providers.

•

33

•Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet