I. Brief analysis:

The multiplier potential

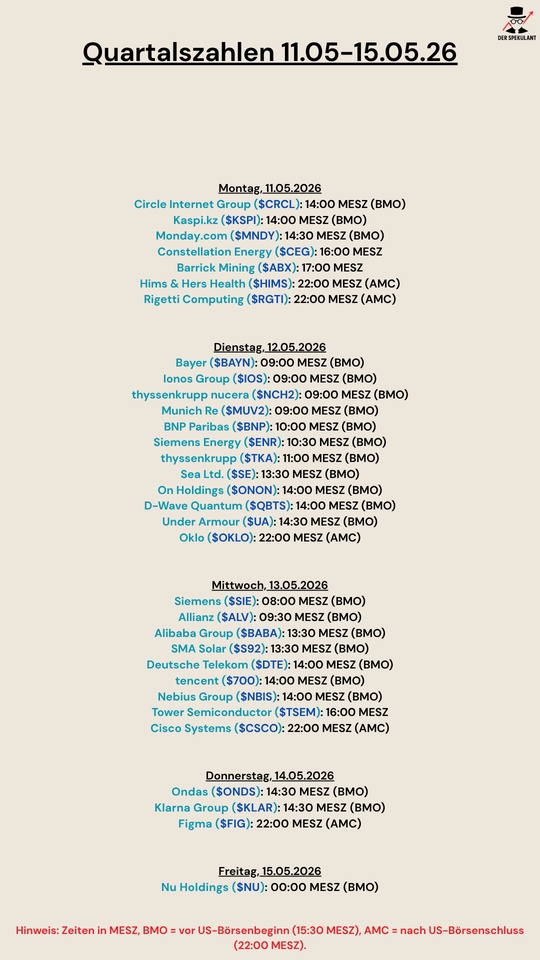

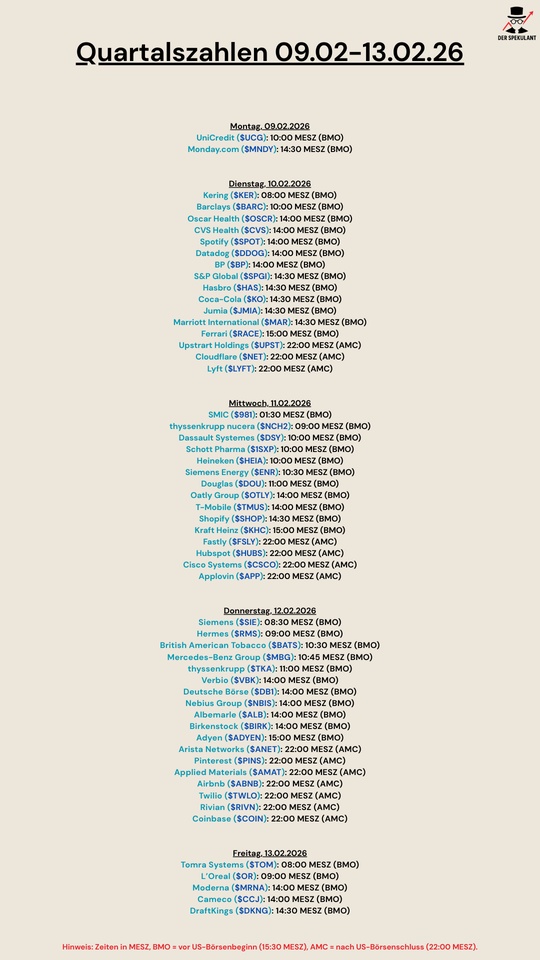

monday.com ($MNDY (-0,97%) ) is a very successful software company that is characterized by excellent business figures. The company works very efficiently and is already earning a lot of real money (cash flow). It has good protection against the competition because customers are reluctant to switch.

Is the investment worthwhile?

The share is an investment in top quality with high growth, but at a high price. The multiplier potential (i.e. the possibility that the share price will multiply) is not because the share is cheap today. It is simply because the company can earn a lot more money in the next few years and, above all, win very large companies as customers.

The strengths lie in the super margin in the core business of almost 90% and the high generation of real money (cash flow margin 26-27%), as well as in the successful acquisition of large corporate customers (46% more major customers). The strong protection against competition due to high switching costs is also a plus. Negatives are the expensive valuation and slowing growth (from 40% in 2023 to planned 26% in 2025), and that the company is still loss-making on paper. There is also strong competition from giants such as Microsoft and Atlassian.

monday.com is a worthwhile long-term investment, but only for investors who are prepared to withstand short-term fluctuations. As the share is already very highly valued, the company cannot afford to make any mistakes, especially if growth slows down.

The business model:

The operating system for work (Work OS)

monday.com was founded in Israel in 2012 and offers software known as Work OS (Operating System). This is a cloud-based, visual system that helps teams to organize their work.

What makes it special is that it is like a construction kit. Customers can easily assemble flexible building blocks to build their own software applications or tools for work management. It serves as a connector for all other digital tools that a company uses. monday.com is therefore not just a project management tool, but a central infrastructure that around 245,000 customers use.

The product offering is broad: there is Monday Work Management (classic organization), Monday Dev (for software developers), Monday CRM (customer management) and Monday Service. This platform strategy is the best protection against the competition.

How the company earns money

The company earns money through recurring monthly or annual subscription fees.

The most important strategy is the focus on large companies ("upmarket"). This is where the company has been most successful: the number of customers paying more than USD 100,000 per year increased by 46% in the last quarter. These large customers already account for 24% of total sales. Management is deliberately foregoing faster growth with small customers in order to achieve more stable and profitable sales with large customers in the long term.

The management: founders with a clear vision

monday.com has been led by the two co-founders Roy Mann and Eran Zinman as co-CEOs since its foundation (since 2012 and 2020 respectively). This continuity at the top is a good sign and shows that a clear strategy is being pursued.

In addition to the founders, the Board of Directors also includes external experts such as Adi Soffer Teeni (from Meta) and Keren Levy (formerly Payoneer). This mix of the founders' vision and the know-how of industry experts helps the company to grow globally.

The moat: Protection from the competition

An economic moat describes advantages that protect a company against the competition in the long term. monday.com has two main sources for this:

The switching costs (The strongest protection)

This is the most important moat. Since monday.com is very deeply built into the daily and important processes of a company (it is a work OS after all), switching to the competition becomes extremely expensive and cumbersome.

Switching costs are: not only fees, but also the high cost of data transfer, employee training and the risk that the new software will not cover all previous processes. This anchoring in the company gives monday.com the power to enforce prices more effectively.

Network effects

The platform is designed for teams to work together. This means that the more departments within a company use monday.com, the more valuable the system becomes for everyone else because communication becomes easier. This makes customers very loyal. Customer loyalty, measured by the "Net Dollar Retention Rate", is a strong 117% for major customers.

Competition is very tough. The main competitors are Microsoft (Teams, Project), Atlassian (Jira, Trello) and direct rivals such as Asana and Smartsheet.

Finances, margins and growth

monday.com shows how well a modern software business can scale as it quickly transitions from growth to real profitability.

While the pace of growth has slowed from 40% (2023) to a planned 26% (2025), it is still very high with 27% revenue growth in the last quarter.

Customer loyalty is particularly strong: If you compare churn with the additional money spent by existing customers through upgrades, the figure is 112% (total) and 117% (key accounts). This means that existing customers automatically pay more and more, which creates very profitable growth.

The scalability of the business model is excellent. The gross margin (the profit that remains after deducting the direct costs of the product) is almost 90%. This shows that the company can sell its software very cheaply to a large number of customers.

The non-GAAP operating margin (the adjusted operating profit) is expected to be around 13% in 2025.

The most important financial point is that monday.com converts revenue into free cash flow (FCF) very efficiently. This is the money that actually ends up in the cash register. The free cash flow margin is a strong 26% to 27%.

Sales growth of around 26% to around USD 1.23 billion is expected for the full year 2025. The gross margin of almost 89.4% reflects the extremely low cost of the software. Customer loyalty (measured by NRR) is 117% for major customers, which means that existing customers are spending more money. The free cash flow margin is expected to be around 26.5%, which shows that a very large part of the turnover ends up as cash in the till.

The combination of 26% growth and 27% cash flow margin (together 53%) is well above the industry standard ("Rule of 40") and proves that monday.com is highly efficient.

Valuation and the multiplier potential

Because monday.com is so good, the share is traded at a premium price. The EV/Sales ratio (enterprise value to sales) is 12 to 13 times, which is much higher than most other software companies. The share is therefore not cheap.

The EV/FCF multiple, which takes cash generation into account, is more meaningful. Based on the forecasts for November 2025, this is approx. 25.6x.

The share is trading at a high premium: The EV/sales ratio is around 12x to 13x , while the peer group (comparable growth companies) is often only 8x to 10x. This shows that monday.com currently has to deliver perfect growth, as the valuation risk is high. The EV/FCF ratio (free cash flow) of around 25.6 times is acceptable for a cash flow margin of 27% and indicates high intrinsic value growth.

The potential for a multiplication of the share price depends on two things:

Management must prove that the company can continue to grow 25%+ going forward and increase the cash flow margin to over 30%.

The share price increases as free cash flow grows strongly.

As the valuation (the purchase price) is so high, there is a risk of so-called multiple compression. If growth suddenly falls below 20% or competition squeezes margins, the market could reprice the stock and lower the multiple from 12x EV/Sales to, say, 8x. Such a discount would cause the share price to fall sharply, even if operating profit increases.

Conclusion on the investment decision

monday.com is one of the best companies in the SaaS space, with a robust moat (switching costs) and excellent financial metrics (90% gross margin, 27% cash flow margin).

The company is a true quality stock. The multiplier potential is there, but is subject to strong conditions: Growth must remain high and management must successfully compete against giants such as Microsoft.

The share is interesting for long-term investors with a high risk appetite. However, due to the high valuation, a staggered entry (i.e. buying in several steps) is recommended. This reduces the risk of investing too much at an unfavorable time.