I added to my position again today $NU (-0,26%) I added to my position. I still see a lot of long-term growth here. Are you invested too?

Have a great evening, everyone!

Postos

348I added to my position again today $NU (-0,26%) I added to my position. I still see a lot of long-term growth here. Are you invested too?

Have a great evening, everyone!

Hello, community,

I could really use some help from the smart folks in the community.

I’d like to downsize my portfolio, but unfortunately, I’m really having a hard time choosing—and I’m wondering if I should sell a few shares of some tech stocks and use the cash to further increase my holdings in the ones I already own.

After much thought, these 6 candidates are on my shortlist:

$3350 (-3,66%) Metaplanet (it was pure FOMO), but also the smallest speculative position

What do you think of my selection, or which stocks would you have chosen instead?

I’d love to hear lots of opinions.

Best regards

Today, one year ago I made my first investment with no real strategy, 20/06/2025 I bought my first share of S&P500, started small, €20 here, €50 there, just feeling my way through, buying whatever caught my eye, chasing hype, following trends without any real conviction or framework behind the decisions.

A lot has changed since then. Over the past year I’ve been gradually restructuring, learning what kind of investor I actually want to be, reducing complexity, cutting positions that didn’t serve a clear purpose, and building something I can genuinely stick to for the next 10+ years.

The strategy going forward

Long-term growth portfolio, anchored in global indices, with active conviction in selected factors and companies.

The core is simple: 50% in broad market ETFs

Everything else is built around it with the intention to boost the overall portfolio performance.

Target allocations:

Core = 50-55% $FWRG (-0,64%) + $AVWS (-0,24%) (90%/10%)

World Value ETF = 8-10% $XDEV (+0,15%)

Semiconductor ETF = 6-8% $SEMI (-0,74%)

Emergent Markets = 6-8% $5MVL (-0,29%)

Quality = 3-4% $IUIT (+0,13%)

Mega caps = 3-5% $MSFT (-1,29%)

$AMZN (-2,12%)

$META (-1,61%)

$GOOGL (-4,79%)

Others = 1-3%

$ASML (-1,06%)

$NOW (-1,3%)

Gold = 5-7% $4GLD (+3,33%)

Bitcoin = 3-5% $BTC (-0,61%)

I’ve some names in my watchlist in case the opportunity appears: $TSM (+0,7%)

$MU (+3,5%)

$NBIS (+0,81%)

$PNG (+2,5%)

$NU (-0,26%)

$SOFI (+0,13%)

$IREN (-0,42%)

$PLTR (-0,69%)

$MA (-0,6%)

Main goal and top priority is to bring my Core

Position as close as possible to the target allocation and Emergent Markets as well, however I’ll keep an eye on market’s volatility.

Special thanks to @Wealth-Accelerator and everyone else that helps me daily in this amazing platform, replying to my posts or comments.

We finding direction. Year two is about executing with discipline and letting time do the work.

Open to questions and feedback, always learning 🚀

Since my last public update of my portfolio in February 2025, over a year has already passed, and a lot happened in my portfolio.

When I last time my portfolio , $HIMS (-1,87%) still by far my largest position and the top performer. But that changed quickly when GLP-1 medications were removed from the list of scarce drugs and the stock went into a nosedive. My portfolio plummeted within weeks from over 200k to just 120k. It really stung, and I decided to close my $HIMS (-1,87%)

position at the next “high.”

No sooner said than done: I did just that in early August 2025 and was able to enjoy a hefty return . (The government was also happy to collect 15k capital gains tax...) It also felt good to have minimized concentration risk. Over 50% of his capital in a single stock like $HIMS (-1,87%) really gives you a headache in the long run.

I then steadily invested the freed-up capital in new stocks like $AMD (+1,37%) , $NBIS (+0,81%) or $META (-1,61%)

invested. I also held onto existing positions such as $GOOG (-4,51%) , $NVDA (+2,34%) , $SOFI (+0,13%) or $NU (-0,26%) were also added to.

In addition, I made some serious mistakes during that time that still hurt. In January 2026, I—actually purely out of boredom, sold my $TXRH (+0,3%) shares to $AEHR (-3,12%) reallocate my portfolio.

Looking in hindsight seems like a awesome trade, things turned out quite differently for me. After about two weeks of indecision , $AEHR (-3,12%) I closed out the €8,000 position with a small profit and, completely without a second thought, put the money into a $META (-1,61%)

long certificate, which then dropped to zero due to the Iran crisis—while $AEHR quadrupled during that time...

-->That was definitely a painful lesson. I hope I never touch a leveraged product again in my life.

Currently, I’m trying to expand my $AMZN (-2,12%) and $MA (-0,6%) positions :)

But since the rest of my portfolio has performed great again this year, I can over it. Last night, for the first time, time since February 19, 2025. I had to wait a full 485 days for that.

That’s what prompted me to write another post here.

What do you think of my portfolio? What were your most instructive experiences on the stock market?

Cheers, Bubu ;)

I've $PEP (-1,23%) held this stock in my portfolio for about 4 years now, and including dividends, I’m just barely breaking even. Even though the dividends are nice, I don’t think Pepsi will outperform the market in the long run either. Since my core portfolio consists mainly of $LYPS (-0,34%) and $MEUD (-0,17%) , I’m considering closing out this position and putting most of it there—partly because my satellite holdings can handle more risk than Pepsi. For one thing, I’d likely get a better return there in the future, and I’d also have a more streamlined portfolio. I might even put a portion of that into riskier stocks like $SOFI (+0,13%)

$NU (-0,26%)

$NOW (-1,3%) . I think those are more likely to outperform the market.

What do you think, and how would you handle this?

Every now and then, I like to share my portfolio with you to get your feedback and tips :-)

I’ve further consolidated it to 26 holdings (if you exclude the duplicate ETFs, which exist for historical and tax reasons, and the very small positions that I can’t sell).

I’m currently contributing $IEMA (+0,13%)

$TDIV (-0,51%) and $EQAC (-0,55%) contributing 250/month, $IWDA (+0,12%) 1,000/month, and $MELI (+1,27%) and $NU (-0,26%) 200/month.

I plan to liquidate my $VOW (-1,35%) position in the next few days, but I don’t know yet where the money will go.

Tips, feedback, etc. are urgently needed :-)

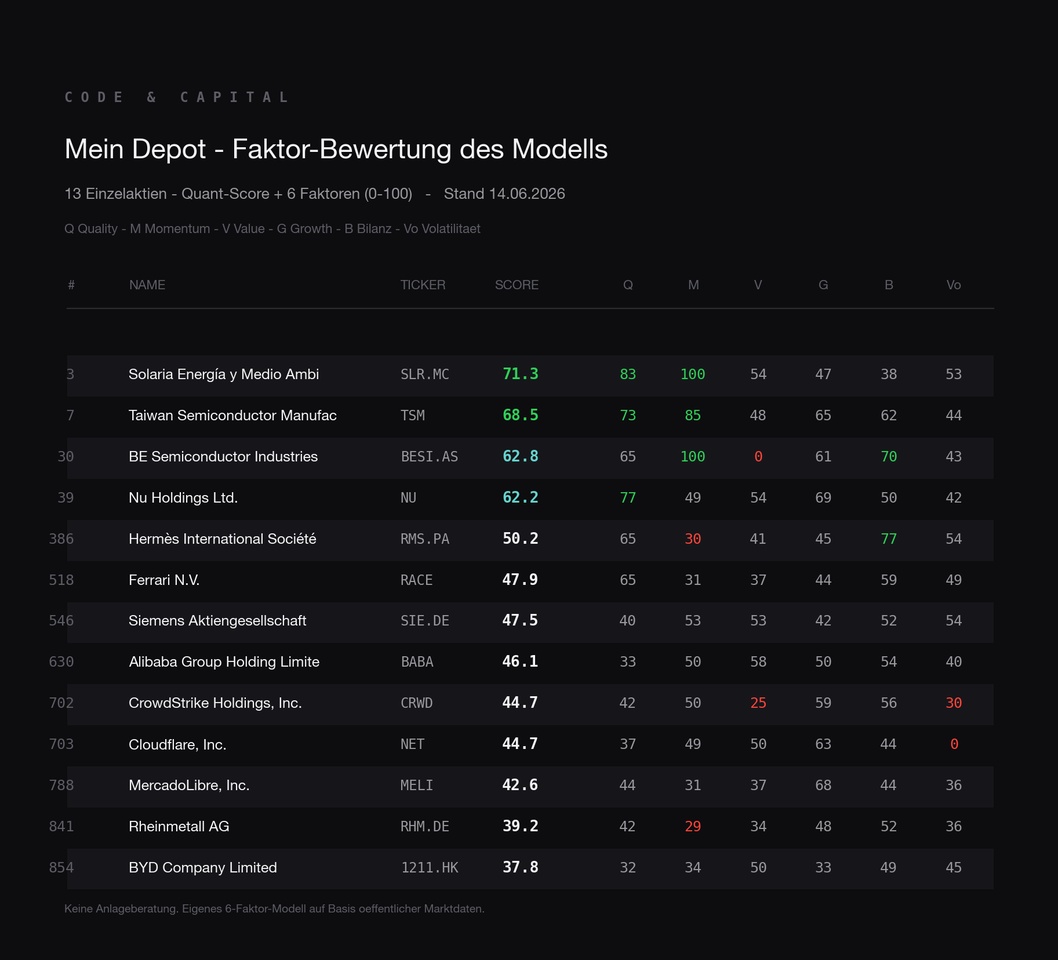

I evaluate around 1,400 stocks using a multidimensional factor model, with each dimension on a scale from 0 to 100. Recently, I’ve started applying this analysis to my own portfolio as well—so each of my positions receives the same score as every other stock in the universe. The results are revealing, especially where the model rates my stocks poorly.

Let’s start at the top:

$SLR (-2,14%) Ranked 3 out of 865, $TSM (+0,7%) at 7, $BESI (-1,39%) at 30, $NU (-0,26%) at 39. At BE Semiconductor, I find the breakdown particularly instructive: an extremely strong momentum score meets a valuation score of practically zero, with a P/E ratio of around 149. So the model doesn’t say “good stock” or “bad stock,” but describes exactly what you’re holding—a strong trend at a high price. This distinction is more important to me than a single overall score.

Now for the bottom half:

Because that’s actually the more interesting part. $RHM (+0,23%) It’s way down the list, $1211 (-0,36%) almost at the end of the universe, $MELI (+1,27%) and also deep. The reason is almost the same everywhere: The 12-month momentum has collapsed following the correction, and at the same time, valuations are high. So two factors are pulling it down at the same time. With Rheinmetall, there’s the added factor that the stock is simply no longer cheap after its strong run—the model sees this objectively, regardless of the story surrounding it.

My software stocks are a special case:

$NET (-1,82%) , $CRWD (+0,1%) and $NOW (-1,3%) . They also end up in the lower range because their high stock-based compensation weighs on quality and balance sheet metrics. This is a well-known issue with growth-oriented software companies: A large portion of employee compensation is paid in stock, which dilutes and burdens margins when factored in honestly. I tested exactly that—I built a variant that excludes the SBC burden and thus rates these stocks more leniently. The backtest yielded a worse result. So I discarded it again and am sticking with the stricter approach. I’d rather have a consistent model that measures all stocks the same way in a verifiable manner than one I tweak for individual favorites. It’s precisely this tweaking that’s the fastest way to a model that looks great in backtesting but doesn’t work in real-world trading.

Bottom line:

for me, these are two types of positions. I bought some because of their scores—Solaria and BESI, for example; the model is what led me to them in the first place. I hold the others deliberately against the score, out of my own conviction. But I want to see the number and take it seriously, rather than pretending it doesn’t exist. That’s the whole point of the exercise.

The purely systematic version—that is, strictly the top-scoring stocks, excluding my conviction-based positions—has been running as a Wikifolio (ISIN: DE000LS9V052) since March and became tradable this week.

What do you think:

Do you tend to trust your own thesis, or the system behind it?

Today I bought an additional €2,000 worth of shares in Nubank $NU (-0,26%) . For me, this remains an exciting growth stock in the fintech sector, especially given its strong position in Latin America and its steadily growing customer base. I continue to see good long-term potential here, even though short-term fluctuations are, of course, to be expected

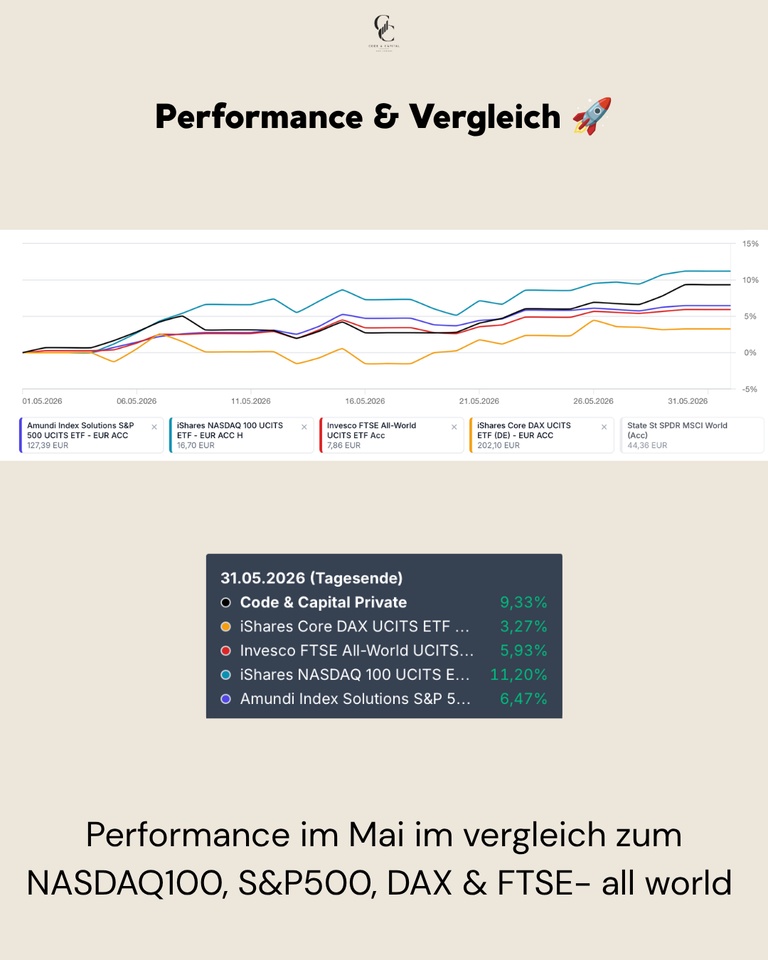

May was dominated by strong figures and a massive rally in the tech and cloud sector. While April was still characterized by a general recovery, excellent quarterly figures and the unbroken AI boom continued to fuel the markets in May. The Nasdaq in particular benefited greatly from this and reached new highs. Even though volatility was noticeable in isolated cases, investors made strong gains in growth stocks.

My portfolio was able to take advantage of this strong momentum and achieve an outstanding performance, but was narrowly beaten by the extremely strong performance of the Nasdaq 100:

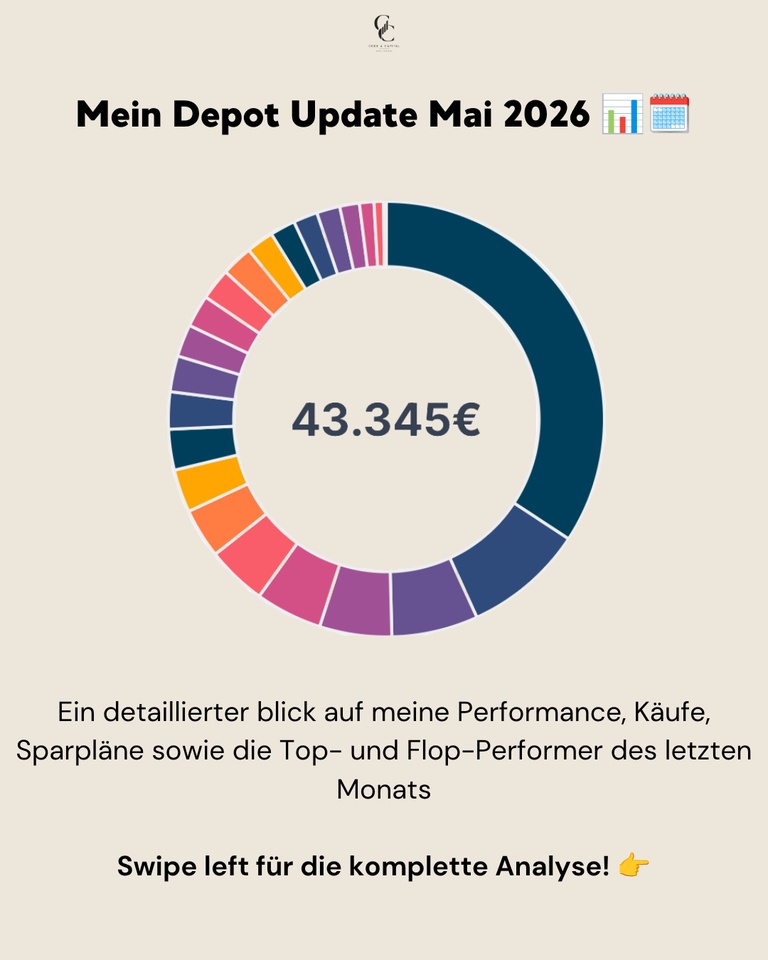

📊 Monthly performance: +9,33%

📊 Portfolio value: ~43.345 €

📊 Performance max. (06.01.2022): +43,84%

📊 Performance YTD: ~+10,44%

Performance & comparison 🚀

Performance in May was exceptionally strong, driven by my high weighting in US tech stocks. While European indices such as the DAX made rather moderate gains, US stocks dominated the action. My portfolio did extremely well with a whopping gain of over 8 % and clearly outperformed the broad market.

Performance in comparison (01.05.-31.05.2026):

My portfolio: +9,33%

NASDAQ 100: +11,20%

S&P 500: +6,47%

FTSE All-World: +5,93%

DAX: +3,27%

Buying, selling & allocation 💶

In the month of May, € 300.00 flowed into the MSCI ACWI USD (Acc)

$ACWI and € 50.00 in the MSCI World Small Cap

$WSML (-0,03%). In addition, smaller savings plan tranches were invested in Solaria Energia

$SLR (-2,14%) (150,30 €), Rheinmetall $RHM (+0,23%) (14,00 €), Ferrari

$RACE (+0,24%) (€6.00) and Hermes

$RMS (-1,55%) (€ 3.01) were invested.

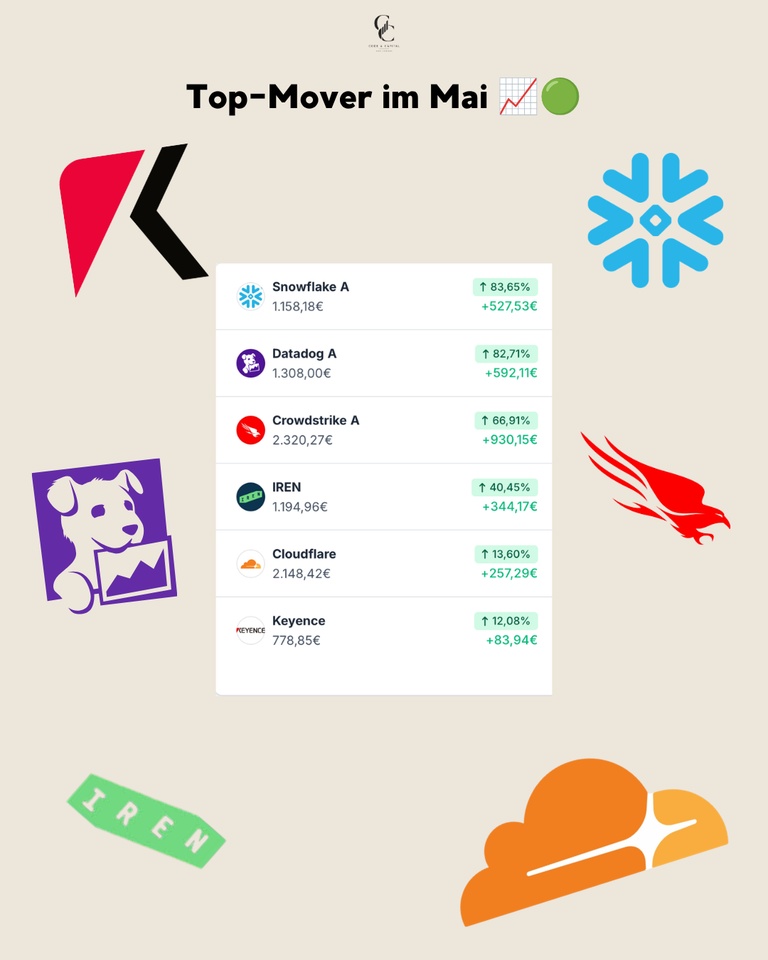

Top movers in May 🟢

The list of winners in May is led by outstanding developments in the cloud and cybersecurity sector - an absolute feast for tech investors.

The absolute frontrunner was $SNOW (-0,36%) with a veritable price explosion of +83,65% (+€ 527.53), closely followed by $DDOG (-1,98%) with +82,71% (+592,11 €). Both values showed incredible momentum. Also $CRWD (+0,1%) was convincing across the board and delivered a strong +66,91% (+€ 930.15), which was the biggest gain in the portfolio in absolute terms. $IREN (-0,42%) continued its strong trend and recorded a further +40,45% (+344,17 €). The outstanding tech performance was rounded off by $NET (-1,82%) with a solid +13,60% (+€ 257.29), while Keyence also $6861 (+4,58%) with +12,08% (+€83.94) also developed extremely positively.

Flop movers in May 🔴

Despite the generally extremely strong sentiment, there were also some stocks that consolidated or showed weakness in May.

American Lithium was the worst performer, falling by -13,16% (-46.03 €), still unable to find a bottom in the current market environment. With $1211 (-0,36%) the minus of -12,13% (€ -190.62) was due to falling EV sales and the ongoing price war in China. $NU (-0,26%) After the strong previous months, the share price fell by -8,90% (-99.30 €) after the strong previous months. Also $TEM (+1,28%) also recorded a slight setback of -8,49% (-7.90 €), similar to $BABA (+0%) with -5,15% (-40,59 €). $RHM (+0,23%) also lost ground and lost -4,60% (-77.14 €), indicating further profit-taking in the defense sector.

Conclusion 💡

May was an outstanding month that impressively demonstrated how much a targeted positioning in the tech and cloud sector can pay off.

❓ Question for the community

This was my month in numbers, what was your best buy in May? Which stock surprised you the most?

👇 Write it in the comments!

➡️ Follow @codeandcapital for transparent portfolio updates!

🔗 Link in bio: Wikifolio, Getquin & Parqet Portfolio

🗞️ Newsletter: codeandcapitalquant.beehiiv.com

+ 2

Principais criadores desta semana