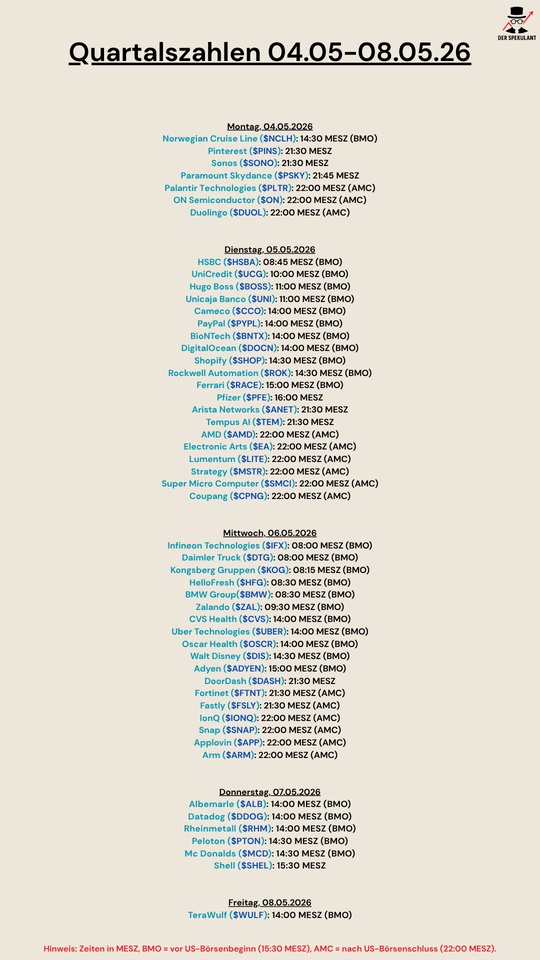

⠀

📊 𝐑𝐞𝐬𝐮𝐥𝐭𝐬

• Adjusted earnings: $9.84B vs. $6.92B QoQ and $4.26B YoY

• Adjusted EPS: $1.76 vs. $1.22 QoQ and $0.72 YoY

• Adjusted EBITDA: $20.71B vs. $17.74B QoQ

• Operating cash flow: $21.43B

• Free cash flow: $17.52B

• Income attributable to shareholders: $10.82B

⠀

💰 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬

• Q2 shareholder distributions: $5.2B

• Share buybacks completed: $3.0B

• Cash dividends paid: $2.2B

• Dividend declared: $0.3906 per share

• New buyback programme: $4.2B, including $3.0B of new repurchases and $1.2B carried over

⠀

📌 𝐊𝐞𝐲 𝐓𝐚𝐤𝐞𝐚𝐰𝐚𝐲𝐬

• Higher realised prices, LNG trading, refining, chemicals and oil-products optimisation supported earnings

• Net debt fell to $41.8B from $52.6B QoQ, while gearing declined to 18.7% from 23.2%

• Shell has delivered $5.8B of structural cost reductions since 2022, including $0.7B in H1 2026

• Production declined to 2.46M boe/d, partly reflecting the impact of the Middle East conflict on Qatari volumes

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 𝐅𝐨𝐜𝐮𝐬

Shell continues to prioritize performance, capital discipline and portfolio simplification while maintaining substantial shareholder distributions.