Reducing concentration risk a bit. I’ll make another, more significant reduction early next year, once the three-year holding period for the employee shares is over. Airbus still accounts for 17.5% of my portfolio.

Airbus

Ação

Ação

ISIN: NL0000235190

Ticker: AIR

NL0000235190

AIR

Price

Discussão sobre AIR

Postos

159

5D·

News from Last Week

As we do every Sunday, here are the top news stories from the past week.

Tuesday:

$AIR (-0,55%) Airbus and $BA (-1,84%) Boeing are delivering more aircraft, though Airbus’s lead is shrinking. Among other orders, Saudi Arabia’s Riyadh Air ordered six new A350-1000 aircraft.

Wednesday:

Following somewhat mixed results from $TSLA (+0,79%) Tesla—which didn’t go over so well on the stock market—Musk is fueling rumors of a possible merger between $SPCX (-4,26%) SpaceX and Tesla. It wouldn’t be the first time Musk has merged his companies …

$GOOGL (+6,31%) Alphabet reported earnings above expectations but increased its investments to a new record level. In Q2, revenue rose 24% to $120 billion. Profit came in at an incredible $112 billion, primarily due to paper gains from its stakes in SpaceX and Anthropic. Alphabet also plans to invest nearly $200 billion in AI infrastructure. This means a single corporation is investing more than the German government is through its special fund. As a result, overall cash flow was negative, which didn’t go over well on the stock market.

https://www.tagesschau.de/wirtschaft/unternehmen/google-cloud-ki-zahlen-investitionen-100.html

Thursday:

$ROP (-0,77%) Roche reported a 2% decline in revenue for the first half of the year, primarily due to negative currency effects. On a currency-adjusted basis, revenue would have grown by 6%. However, the Swiss franc has continued to appreciate. At 23.6 billion Swiss francs, the pharmaceuticals division remains the most important business segment, ahead of diagnostics (6.7 billion Swiss francs).

$INTC (+0,29%) Intel is benefiting from the AI boom and increased its quarterly revenue by 25%. At $16.1 billion, revenue was $1.5 billion above expectations. Profit was even twice as high as expected.

Friday:

VW’s profit $VOW (-0,85%) VW plummeted again to 1.5 billion euros, down from 2.3 billion euros the previous year. VW’s revenue rose by 2%. For the full year, VW expects revenue to decline by 1–3%.

https://de.finance.yahoo.com/nachrichten/nettogewinn-volkswagen-zweiten-quartal-um-062011552.html

www.handelsblatt.comFlugzeugbau: Airbus und Boeing überraschen mit Lieferzahlen

55

5D·

Quarterly Results: July 27–July 31, 26

$MC (+0,93%)

$MBG (-0,99%)

$ULVR (-1,69%)

$PYPL (-0,48%)

$NBIS (-2,1%)

$SPGI (+0,31%)

$UPS (-1,03%)

$KO (-0,87%)

$GLW (+2,44%)

$BA (-1,84%)

$KER (-2,07%)

$ENPH (+0,62%)

$NXPI (-4,98%)

$STX (+1,6%)

$BE (+0,27%)

$V (+0,12%)

$MDLZ (-1,22%)

$000660

$P911 (-3,19%)

$BN (-1,31%)

$RMS (-0,79%)

$BAS (-1,36%)

$AG1 (+2,46%)

$LMND (+1,02%)

$SOFI (-0,18%)

$NDX1 (-1,62%)

$TER (+1,88%)

$GD (-0,81%)

$APH (+1,13%)

$AIR (-0,55%)

$SBUX (-0,16%)

$CMG (-1,87%)

$META (+1,65%)

$FTNT (+4,83%)

$QCOM (-1,86%)

$LRCX (+0,1%)

$HOOD (+1%)

$ARM (+0,24%)

$MSFT (+3,07%)

$CVNA (-0,08%)

$005930

$SU (+1,71%)

$INGA (+1,1%)

$OR (-1,81%)

$BMW (-1,65%)

$BATS (-0,64%)

$MA (-0,4%)

$ADS (+1,58%)

$SHEL (+1,33%)

$RACE (-1,1%)

$RDDT (-13,68%)

$TEM (-0,03%)

$COIN (-2,66%)

$AAPL (-5,06%)

$AMZN (+6,44%)

$CCO (-2,12%)

$LIN (-6,37%)

$ABBV (-2,33%)

$PUM (-2,5%)

$HAG (-4,42%)

$XOM (-1,86%)

$CVX (+1,66%)

1414

1Semana·

M/21 Dual Student enjoys roasting

Hey everyone, I'm really looking forward to hearing your thoughts.

My core holdings consist of ETFs, supplemented by individual stocks like Airbus and TotalEnergies, which are intended to counterbalance the overweighting of U.S. and tech stocks in the ETFs.

$TTE (+0,96%) I bought these before the Iran crisis as stocks offering a reliable dividend and a favorable valuation, based on the investment thesis that they would grow steadily due to the long-term shift toward renewable energy.

$AIR (-0,55%) I built up this position due to a price pullback and the thesis that Europe is gaining structural importance in the aerospace and defense sectors, driven in part by rising European defense spending and growing strategic independence from the U.S. The position has since grown to about 21% of my portfolio, which I accept as a deliberate concentration risk, as I remain convinced of the thesis.

$NVDA (+1,65%) And $BTC (-2,79%) I’m simply keeping this unchanged, as I currently see no reason to adjust it, and the $MSFT (+3,07%) warrants are just a bit of fun.

9Posições

€ 51.039,37

30,30%

1414

1Mês·

Airbus and Kawasaki Plan to Equip Eurodrone for Submarine Hunting

According to a company press release, Airbus signed a memorandum of understanding (MoU) with the Japanese conglomerate Kawasaki Heavy Industries on June 26, 2026, to jointly explore the possibilities for a Japanese version of the U950 Eurodrone unmanned aerial system for anti-submarine warfare (ASW).

Japan has been participating in the European four-nation program as an observer since 2023. The program is sponsored by Germany, France, Italy, and Spain and managed by the defense agency OCCAR. India also holds observer status.

The Eurodrone is ideally suited for monitoring vast maritime areas

The Eurodrone, whose maiden flight is scheduled for 2029, features a flight duration of up to 40 hours and a payload capacity of up to 2.3 metric tons. This puts it well ahead of its direct competitors and makes it ideally suited for monitoring vast maritime areas. For Japan, the platform offers the option to supplement its manned anti-submarine fleet highly efficiently and independently with an unmanned system that can be equipped with sonar buoys and torpedoes.

Strengthening European-Japanese Defense Initiatives

In the next step, Airbus and Kawasaki will develop concrete design, development, and marketing options. These include the integration of Japanese sensors and effectors, as well as the definition of industrial work shares for production and maintenance in Japan, to guarantee unrestricted, sovereign use.

The cooperation strengthens the Eurodrone program, deepens European-Japanese defense initiatives, and provides valuable insights for future European naval variants.

Gerhard Heiming

esut.deAirbus und Kawasaki wollen Eurodrone zur U-Boot-Jagd befähigen

3434

3 Comentários

I'm holding my position in Kawasaki and expanding it slightly.

•

55

•

1Mês·

Multiple reinforcements 💹

Today, we reinforced 4 positions for a total of $18,873, allocated as :

- +15 $SNPS (+3,48%) shares for $6,872

- +50 $NOW (+1,67%) shares for $5,256

- +200 $ALKAL (-4,77%) shares for $2,700

- +20 $AIR (-0,55%) shares for $4,045

The majority of these companies are structurally coherent and strong companies, deeply embedded in their respective industries.

33

3Mês·

𝐀𝐢𝐫𝐛𝐮𝐬: 𝐖𝐞𝐚𝐤 𝐃𝐞𝐥𝐢𝐯𝐞𝐫𝐢𝐞𝐬, 𝐄𝐁𝐈𝐓 𝐃𝐫𝐨𝐩, 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧, 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐔𝐧𝐜𝐡𝐚𝐧𝐠𝐞𝐝

📊 𝐑𝐞𝐬𝐮𝐥𝐭𝐬

• Revenue: €12.7B (−7%)

• Adj. EBIT: €0.3B (vs €0.6B)

• EBIT: €0.2B

• Net income: €0.6B

• EPS: €0.74

• Free cash flow: −€2.5B

• Deliveries: 114 aircraft

⠀

🎯 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

• Deliveries FY: ~870 aircraft

• Adj. EBIT FY: ~€7.5B

• Free cash flow FY: ~€4.5B

⠀

📌 𝐊𝐞𝐲 𝐓𝐚𝐤𝐞𝐚𝐰𝐚𝐲𝐬

• Revenue and EBIT declined driven by lower aircraft deliveries

• Commercial aircraft margin heavily pressured

• Defence & Space showed strong growth and profitability

• Massive negative free cash flow from inventory build-up and delivery timing

• Supply chain issues (Pratt & Whitney engines) remain key bottleneck

• Order intake strong with backlog above 9,000 aircraft

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 𝐂𝐨𝐦𝐦𝐞𝐧𝐭𝐚𝐫𝐲

“Operating environment remains dynamic and complex.”

88

3Mês·

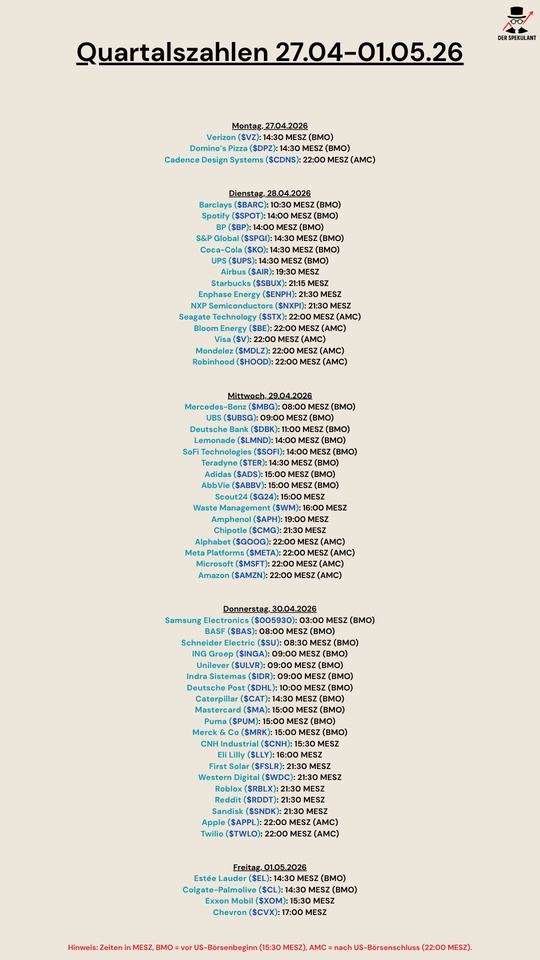

Quarterly figures 27.04-01.05.26

$VZ (+1,16%)

$DPZ (-0,65%)

$CDNS (+1,72%)

$BARC (-0,7%)

$SPOT (-2,88%)

$BP. (+1,62%)

$SPGI (+0,31%)

$KO (-0,87%)

$UPS (-1,03%)

$AIR (-0,55%)

$SBUX (-0,16%)

$ENPH (+0,62%)

$NXPI (-4,98%)

$STX (+1,6%)

$BE (+0,27%)

$V (+0,12%)

$MDLZ (-1,22%)

$HOOD (+1%)

$MBG (-0,99%)

$UBSG (-1,36%)

$DBK (-0,59%)

$LMND (+1,02%)

$SOFI (-0,18%)

$TER (+1,88%)

$ADS (+1,58%)

$ABBV (-2,33%)

$G24 (-3,67%)

$WM (-0,13%)

$APH (+1,13%)

$CMG (-1,87%)

$GOOG (+6,29%)

$META (+1,65%)

$MSFT (+3,07%)

$AMZN (+6,44%)

$005930

$BAS (-1,36%)

$SU (+1,71%)

$INGA (+1,1%)

$ULVR (-1,69%)

$IDR (+0,5%)

$DHL (+0,3%)

$CAT (+1,04%)

$MA (-0,4%)

$PUM (-2,5%)

$MRK (+0,69%)

$CNHI (-0,39%)

$LLY (-0,82%)

$FSLR (+0,6%)

$WDC (+1,56%)

$RBLX (-19,3%)

$RDDT (-13,68%)

$SNDK (-5,24%)

$AAPL (-5,06%)

$TWLO (+3,23%)

$EL (+0,25%)

$CL (-0,63%)

$XOM (-1,86%)

$CVX (+1,66%)

2121

2 ComentáriosLemonade will be interesting and may already point the way forward.

Mercedes could hurt...

Mercedes could hurt...

•

22

•

3Mês·

Apr 22 / Time to Buy More Defence?

War is ubiquitous right now. Whether you look at Ukraine, Iran, the Gulf, Pakistan, or not so long ago Venezuela. And that’s despite Trump’s claims that he supposedly ended eight wars since he came into office. While nobody knows which wars he ended, most people definitely know which he has begun. And that’s not to critique the engagement in Iran or Venezuela. Trying to overthrow evil dictators is not an inherently bad cause, however the method might be more than questionable.

At this point, the standoff between Trump and whoever is in charge of Iran seems more like two kids fighting in the playground over who opens the Strait of Hormuz first and finally gives the Gulf nations some breathing space again.

But one thing is undoubtedly clear in all this. The defence sector is booming everywhere. In Europe, the US and Asia, countries are rearming themselves, for very different reasons. Europe because the American security guarantee is no longer completely reliable, with NATO seemingly in question. Asia because China continues to expand its dominance and push to become the leading world power. And the US because it still wants to play “World Police,” even if that might not be the most popular approach domestically anymore. But I guess we’ll find that out in the midterms.

Considering all of this, nobody can doubt the importance of defence companies, and their backlogs are as full as you would expect. The poster child of European rearmament is Rheinmetall, growing at unprecedented rates with order books stretching years into the future. And that is definitely reflected in the stock price. Since the start of the Ukraine War five years ago, the stock has risen by more than 2,200%. Yes, that’s right, if you invested $10k then, they would be worth $220k now.

But we all know that Europe’s defence industry has been historically underfunded, so it’s no surprise that it eventually caught up. What about the US then?

The sector is doing well, as always, but the stock performance hasn’t been as extraordinary. Around 110% over the last five years for the SPDR U.S. Aerospace & Defense ETF is solid, but not exactly record-breaking. So is now the time to invest? After all, Trump did announce a massive hike in the defence budget from currently $901 billion to more than $1.5 trillion.

Whether that actually goes through is a different question, considering the already massive national debt and Trump’s midterm concerns. But we also know he can take a different approach.

Just a few months ago, the President floated the idea of a pay cap for defence executives and even proposed restricting share buybacks and dividends. Our wonderful “businessman” of a president wants to cut incentives for both management and investors. How encouraging.

So ultimately, whether you should invest in defence right now is a matter of opinion. Personally, I think the European sector is overbought, but demand is clearly there, so I wouldn’t be too worried about holding names like Rheinmetall or others. For the US, it seems the market doesn’t fully believe in the trillion-dollar budget, given current valuations and revenue expectations of the major players.

But again, it’s still one of those sectors where you probably can’t go too wrong, and there is definitely still some upside left.

$ITA (+0,86%)

$LMT (+1,25%)

$GD (-0,81%)

$NOC (+1,9%)

$RTX (+0,57%)

$LHX (+2,32%)

$BA (-1,84%)

$AIR (-0,55%)

$RHM (-0,51%)

3Mês·

Market levels are getting crazy. Where’s the value? 📈🤔

Let’s be real: finding quality companies at a fair price right now is a goddamn nightmare. Everything feels overpriced, and I’m not willing to sacrifice my margin of safety just because of the hype.

I’m sitting on cash and being patient. I know what I want, I’m just waiting for the market to give me a better entry point. These are the fortresses on my Watchlist:

Expanding current positions: $GOOGL, (+6,31%)

$META (+1,65%) .

New targets: $AMZN (+6,44%) , $MEDP (-0,16%) , $ASML (+0,13%) , $AIR (-0,55%) (Airbus), $RMS (-0,79%) (Hermès) and the Greek gem $KRI.AT (Kri Kri Milk).

What about you? Which companies are you stalking right now?

33

5 Comentários

3Mês

I think ASML is slightly undervalued therefore i will increase my position at the end of the month

••

Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet