It’s been a while since I talked about the major aircraft manufacturers. Today it’s about Airbus.

Yes, Boeing might be the hotter commodity at the moment, which represents a role reversal compared to the past few years, but Airbus is the more interesting player for me right now.

The company sits right at the intersection of two powerful secular trends: global expansion in commercial aviation and European rearmament. Roughly 20% of Airbus’ revenue already comes from its Defence and Space segment, and that division is expanding rapidly. With Europe increasing defense budgets and pushing for more strategic autonomy, Airbus is positioned as a core beneficiary.

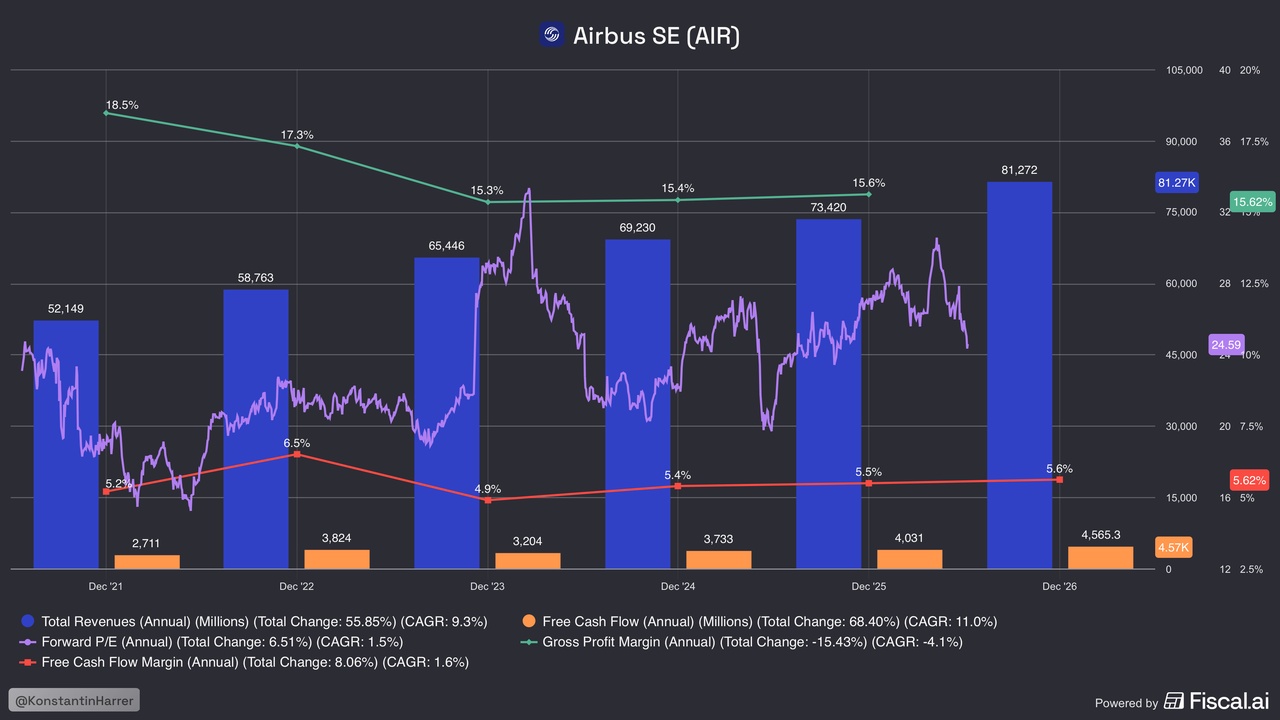

But even if you ignore defence entirely, the core commercial aviation business is performing extremely well. Free cash flow is projected to grow in the 20% range annually through 2028, while top-line growth is expected to stay in the low teens. And these growth assumptions don’t feel heroic. With a backlog of nearly 9,000 aircraft, Airbus doesn’t need blue-sky scenarios. It simply has to execute and work off what is already contracted.

And beyond growth, Airbus is an incredibly safe business. It operates in a practical duopoly with Boeing in commercial aviation. There are no serious new entrants that can realistically challenge that structure anytime soon. The backlog is filled to the sky.

In 2025, Airbus delivered nearly 800 aircraft, yet its backlog still climbed to record highs of almost 9,000 planes by year-end. That’s multi-year revenue visibility. Add to that a balance sheet with no net debt and roughly $14 billion in cash, and the financial position looks very solid. Airbus is also the prime contractor for major future European defence programs like the Future Combat Air System, which could become a cornerstone project over the next decade.

Despite all of this, the stock is down more than 20% from its all-time highs reached in early January. Concerns about permanently elevated energy costs, especially in light of the U.S.-Israel-Iran conflict, have weighed on the sector. A P/E ratio of around 30 times earnings likely added pressure as well. That multiple was roughly the average from 2022 to 2025 following the Russian invasion of Ukraine and seemed fair rather than excessive at the time.

Now the forward P/E sits closer to 23 times, around 19 times based on FY27 earnings, and roughly 16 times on FY28 estimates. For a company with this backlog, this visibility, and these structural tailwinds, that valuation looks much more reasonable and closer to pre-war levels, while being in a more favourable position.

Airbus is firmly on my watchlist and approaching my buy zone as it moves into the $160 range.