Medtronic

Price

Discussão sobre MDT

Postos

30

Medtronic 2026: Something is finally happening!

Hello everyone, I have had Medtronic $MDT (-1,04%) in my portfolio for a long time and it's just bobbing along. But what is happening now (with announcement) could be a significant turning point.

It's not just that they are taking their diabetes division (MiniMed) public (the announcement was officially published yesterday). This is just the most visible part of a radical strategy that CEO Geoff Martha has been implementing since he took over. He is doing exactly what General Electric has done so successfully - he is filleting the colossus so that the real gems can finally shine.

The MiniMed IPO and the sale of the lame "Respiratory" division (ventilation) are making the portfolio cleaner.

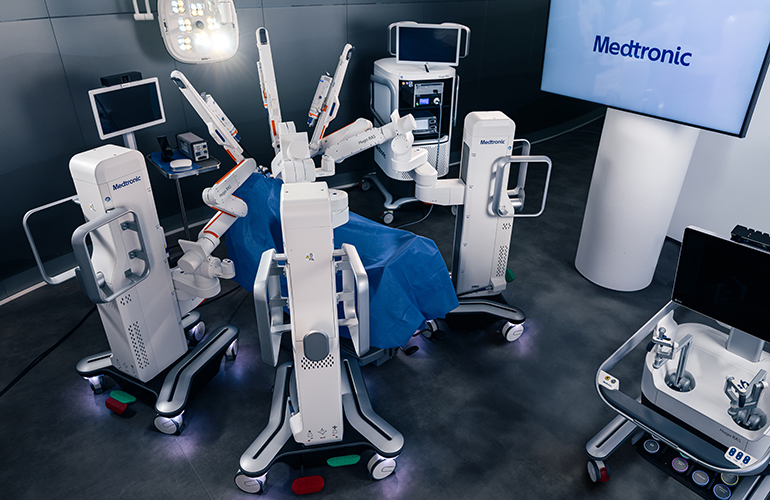

Medtronic is already going on the attack against Intuitiv Surgical with the Hugo system.

Anyone who thinks that Medtronic's Hugo system is only good for "small things" is mistaken. Hugo is modular. While Intuitive Surgical's da Vinci is a solid block, Hugo consists of four flexible individual arms. This is a huge advantage for clinics in terms of logistics and costs. Medtronic can use its market power to put together packages of robotics, pacemakers and suture material that a pure robotics specialist simply cannot match in terms of price. This is the lever that will really cost Intuitive Surgical market share.

The MiniMed spin-off is not about hardware, but about software. The SmartGuard algorithm is the real spearhead. Together with the new Simpler Sync sensor (finally without the hassle of stitching and gluing!), they deliver the complete "artificial pancreas" from a single source. While the competition (Tandem/Dexcom) is always dependent on partners, MiniMed controls the entire system. This is a moat that many still underestimate.

Geoff Martha is now delivering what he promised: He is freeing the growth machines from the ballast of the old divisions.

Medtronic is becoming a highly profitable cash machine for cardiac medicine and robotics (with stable dividends!). And Minimed will become the pure tech bet for all those who believe in automated diabetes cures.

I am delighted that the implementation is actually taking shape. As an idea, you can look at General Electric, for example, and see how the split has led to massively higher individual valuations.

It's getting exciting 🤑🤞🏼

A little quieter next week

$SON (+1,33%)

$MDT (-1,04%)

$LDOS (+4,53%)

$PANW (+0,8%)

$CDNS (+0,02%)

$KRYS (-0,04%)

$HL (+2,85%)

$TOL (+0,48%)

$KVUE (-1,06%)

$DEVON

$ADI (+2,21%)

$GRMN (+0,28%)

$SEDG (+2,1%)

$MCO (+0,36%)

$FVRR (+0,7%)

$PODD (-0,83%)

$CVNA (+1,59%)

$DASH (+0,15%)

$FIGX

$EBAY (-0,87%)

$RELY

$WMT (-1,52%)

$PWR (+1,76%)

$DE (+0,43%)

$LMND (+0,77%)

$KLAR (+0,23%)

$W (+15,89%)

$NICE

$YETI (+1,36%)

$OPEN (+1,4%)

$NEM (+1,78%)

$AKAM (-0,37%)

$SFM (+0,61%)

$TXRH (+0,29%)

$BCPC (+1,23%)

$BKNG (-1,72%)

The 10 best US dividend stocks

$MRK (+0,8%)

$KO (-0,94%)

$PEP (-0,61%)

$COP (-1,45%)

$MDT (-1,04%)

$MDLZ (-0,19%)

$EOG (-1,38%)

$SLB (-1,39%)

$KMB (-1,15%)

$CL (-0,03%)

What should investors look for when it comes to buying the best dividend stocks for 2025?

At Morningstar, we believe that the best dividend stocks are not simply the stocks with the highest dividends or the stocks with the best dividend yields. We recommend that investors look beyond a stock's yield and short-term performance and instead consider stocks with sustainable dividends and buy them when they are undervalued.

"As tempting as they may be, the most attractive returns on the stock market are often illusory," explains Dan Lefkovitz, strategist at Morningstar Indexes. "High dividend yields are often found in risky sectors, industries and companies." Therefore, such high dividend yields are not always sustainable.

David Harrell, the publisher of Morningstar DividendInvestor, empfiehlt,to focus on companies with management teams that support their dividend strategy and to favor companies with competitive advantages or wirtschaftlichen Burggräben to be preferred.

"An economic moat rating is obviously no guarantee of dividends, but we have found some very strong correlations between economic moats and dividend consistency," says Harrell.

Investors looking for good dividend stocks might consider adding undervalued quality dividend stocks to their portfolio.

10 best US dividend stocks to buy

To find the best U.S. dividend stocks, we turn to the Morningstar Dividend Yield Focus Index. The dividend stocks on this list are among the top stocks in the index and were trading in the 4- and 5-star range as of June 13, 2025.

Merck MRK

Coca-Cola KO

PepsiCo PEP

ConocoPhillips COP

Medtronic MDT

Mondelez Global MDLZ

EOG Resources EOG

SLB SLB

Kimberly-Clark KMB

Colgate-Palmolive CL

Below you will find a brief description of the individual low-cost dividend stocks as well as some important Morningstar key figures. All data is valid until October 10, 2025.

Merck

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: High

- Morningstar Uncertainty Rating: Medium

- Expected dividend yield: 3.77

- Sector: Pharmaceuticals - General

Merck tops our list of best dividend stocks with a share price 23% below our estimated fair value of $111 per share. Merck continues to see weak demand for its HPV vaccine Gardasil in China, which has dampened revenues this year. Nevertheless, we believe Merck shares are undervalued. The company's balance sheet is solid and low risk. We expect stable future dividends, supported by a payout ratio of nearly 50% of adjusted earnings per share, according to Morningstar Director Karen Andersen.

Coca-Cola

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 3.04

- Sector: Beverages - non-alcoholic

Coca-Cola is the first Dividendenaristokrat on our list of this month's best dividend stocks. Dividend aristocrats are companies that have increased their dividends for at least 25 consecutive years. The company's impressive brand portfolio, pricing power and relationships with retailers underpin its high Economic Moat rating, says Morningstar analyst Dan Su. We expect the dividend payment to increase in line with earnings growth over the next ten years, with the dividend payout ratio likely to stabilize above 60%, Su adds. We estimate the value of Coca-Cola shares at USD 72.

PepsiCo

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 3.79

- Sector: Beverages - non-alcoholic

Pepsi is the second Dividend Aristocrat on this month's list of best dividend stocks to buy. We estimate the value of the Pepsi-Aktie at $164 and the shares are trading 8% below this value. Despite short-term headwinds due to consumer austerity, we believe Pepsi continues to be able to strengthen its competitive position in beverages and snacks through marketing and product initiatives, reports Morningstar's Su. Over the next decade, we expect Pepsi's payout ratio to remain in the low 70% range on average and its dividend payment to grow in the mid-single digits annually, Su said.

ConocoPhillips

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: High

- Expected dividend yield: 3.56

- Sector: Oil and Gas E&P

ConocoPhillips is the first energy stock on our list of best dividend stocks and is currently trading 19% below our estimated fair value of $108. Morningstar analyst Adam Baker points out that the company has been making large acquisitions at favorable prices without burdening the balance sheet. ConocoPhillips ties cash returns to cash flow and has committed to returning 30% of operating cash flow to shareholders, keeping dividend growth moderate but committing excess cash to buybacks and a variable dividend each year.

Medtronic

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: Medium

- Expected dividend yield: 2.98

- Sector: Medical devices

Medtronic stock is one of the best dividend stocks and is currently trading 15% below our estimated fair value of $112. The largest pure-play medical device manufacturer is an important partner for its hospital customers thanks to its diversified product portfolio for a variety of chronic conditions, explains Morningstar Senior Equity Analyst Debbie Wang. The company aims to distribute at least 50% of its annual free cash flow to shareholders, but has been in the 60% to 70% range in recent years, Wang said. Medtronic is also a dividend aristocrat.

Mondelez Global

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 3.25%

- Sector: Confectionery manufacturer

Mondelez International is one of the five Unternehmen mit breitem Burggraben on our list of the best dividend stocks to buy. "Mondelez has worked tirelessly to further simplify its operations by streamlining its supplier base, divesting unprofitable brands, and continuing to modernize its manufacturing facilities," argues Morningstar Director Erin Lash. We forecast that the company will increase its dividend on average in the high single digits through fiscal 2034. We estimate the value of this top dividend stock at USD 75, and the shares are trading 18% below this value.

EOG Resources

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: Medium

- Expected dividend yield: 3.78

- Sector: Oil and gas production

EOG Resources returns to our list of the best dividend stocks to buy this month. This top dividend stock is trading 21% below our estimated fair value of USD 137. The company aims to return 70% of free cash flow to shareholders via dividends and share buybacks. "Unlike some peers that buy back shares at top valuations when they have ample cash, EOG also returns cash via special dividends," says Morningstar Director Josh Aguilar. EOG's balance sheet is strong, and the company should have no trouble meeting its fixed and variablen Dividenden cover its fixed and floating rate debt.

SLB

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: High

- Expected dividend yield: 3.59

- Sector: Oil and gas equipment and services

SLB, the last energy stock on our list of best dividend stocks, is trading 37% below our estimated fair value of $50. SLB is the world's leading oilfield services company by market share and has built a narrow economic moat based on its cost advantages and intangible assets. Morningstar's Aguilar calls the company's distributions "shareholder friendly" and we expect management to continue to return more than half of free cash flow to shareholders in the form of dividends or buybacks.

Kimberly-Clark

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar uncertainty rating: Medium

- Expected dividend yield: 4.22%

- Sector: Household and personal care products

Kimberly-Clark is the highest yielding stock on our list of best dividend stocks to invest in and is currently trading 15% below our estimated fair value of $140. The company's portfolio of well-known hygiene and tissue brands, including Huggies, Depend and Kleenex, generates significant excess cash, according to Morningstar's Lash. Lash's long-term outlook calls for mid-single-digit annual dividend growth. Kimberly-Clark is also a dividend aristocrat.

Colgate-Palmolive

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 2.67

- Sector: Household and personal care products

Colgate-Palmolive rounds out our list of best dividend stocks and is also a dividend aristocrat. The Colgate brand's solid intangible assets and cost advantages underpin the company's broad economic moat, says Morningstar's Lash. Over the next 10 years, we expect average annual dividend growth in the high single digits with a payout ratio of 55% to 60%, she adds.

Source

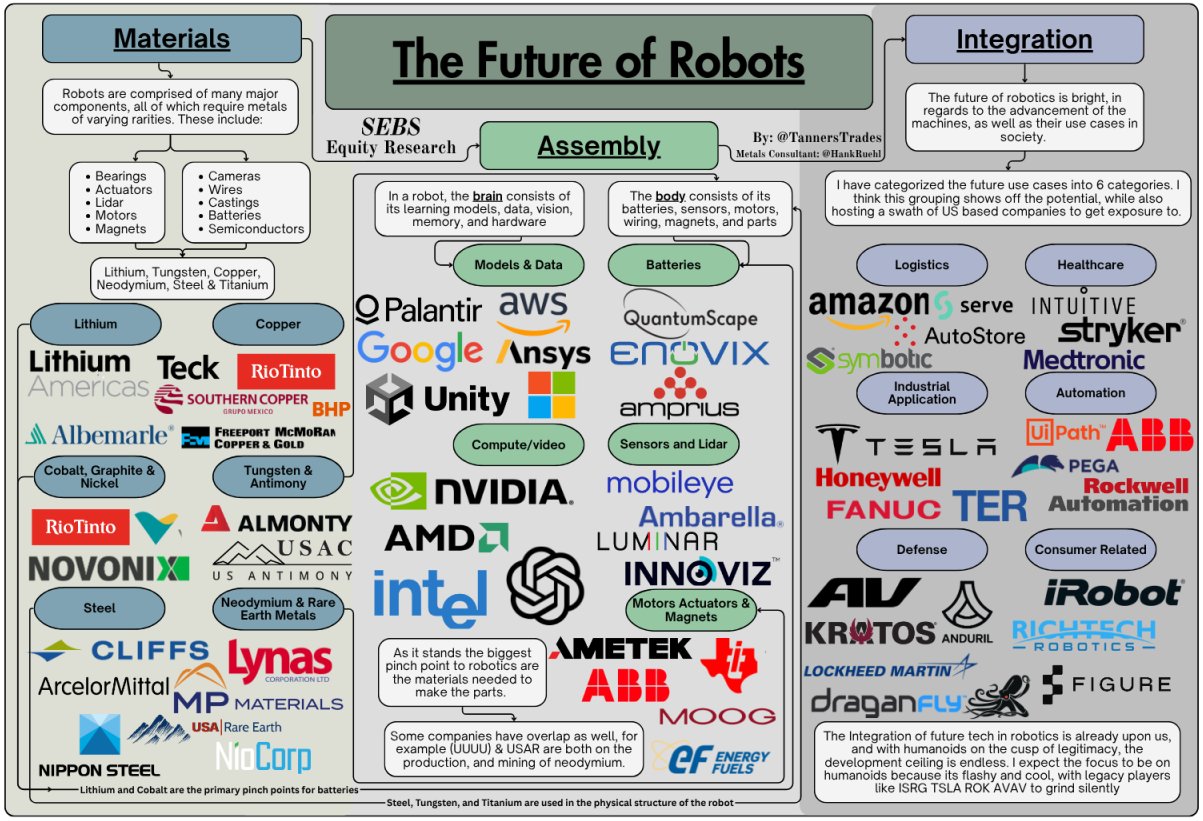

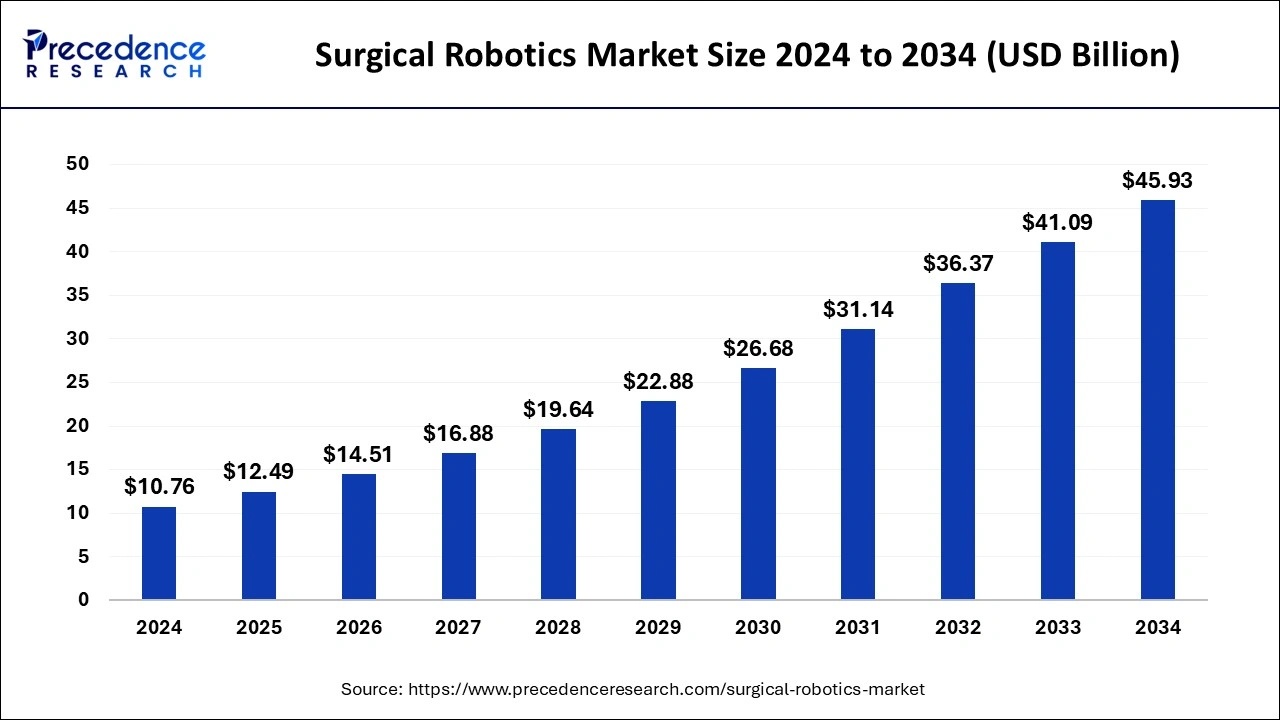

The Future of Robots 🤖🦾🦿

Here is an exciting overview, for me the most attractive in terms of growth/potential of the stocks I know $RR

$PATH (-2,2%) also $ISRG (-0,6%) I would perhaps add to the portfolio again in the event of a correction. However, there are some stocks I don't know either.

What do you think are the most exciting stocks on the list, where should we perhaps take a closer look?

$AMZN (-2,07%)

$MSFT (-2,43%)

$NVDA (+1,69%)

$AMD (+3,27%)

$GOOGL (-1,73%)

$GOOG (-1,62%)

$RIO (+3,14%)

$ALB (+2,22%)

$INTC (+4,69%)

$PLTR (+3,65%)

$IRBT

$SYK (-0,32%)

$MDT (-1,04%)

$LMT (-0,53%)

$DPRO (+1,76%)

Intuitive Surgical — Expensive Robotics Leader with a Wide Moat

1. Executive Summary

Intuitive Surgical has built one of the most impressive business models in healthcare, deeply entrenched within the hospital system. Since its inception 30 years ago, management has done nothing but innovate, scale, and integrate. Starting out with a little prototype developed by founder Dr Frederick Moll, Intuitive turned robotic-assisted surgery from a niche experiment into an indispensable global standard of care, under the leadership of long-term CEO Gary Guthart. The robotic surgery company focuses on developing and manufacturing robots used for minimally invasive surgery, and sits at the clear top of this market. It was not just the first in the market, it is still the most successful, by a great margin.

With its market-leading da Vinci platform, Intuitive built a substantial recurring revenue stream. Once a hospital chooses the platform, switching costs are considerable – not just monetarily but also in the specific training surgeons continually engage with. Doctors and hospitals are locked in Intuitive’s ecosystem, which ensures them as long-term customers.

What makes Intuitive stand out is not only its scale, but the durability of its moat: switching costs are enormous, and competitors seem years behind in development. If advancements are made, then mainly in specific areas such as PROCEPT’s AquaBeam, used for resecting prostate tissue. However, on a broader scale Intuitive’s position remains untouched.

Additionally, the rise of demand for robot-assisted surgeries creates a self-reinforcing cycle: more procedures → more trained surgeons → more demand → more recurring revenue.

The financials reflect this strength: double-digit revenue and earnings growth, gross margins near 70%, operating margins above 30%, and a pristine balance sheet with no debt and steady, growing cash flows. Still, the stock trades at a premium valuation, because the market knows what it owns — a near-monopoly in a growing field. However, as it often is with great companies operating at elevated valuations, they are priced for perfection. Blemishes in earnings reports can lead to sharp selloffs in the stock. Within hours the whole narrative can change and the market leader with stellar prospects becomes an unloved, disrupted business without a future.

The most obvious risk is that competition is rising: from Medtronic’s Hugo to CMR Surgical’s Versius, and the previously mentioned specialty-focused entrants like PROCEPT BioRobotics. None threaten Intuitive’s dominance today, but they could erode pricing power and slow growth at the edges, which might rattle the stock price even more.

Intuitive is therefore not a “value” story but a structural growth one. It is the reference name for exposure to robotic surgery, with a wide moat but growing competitive noise. Valuation remains elevated even after the recent gradual decline and sideways trading.

2. Macro Environment

Healthcare is, and has been for years, in a shift toward digitization and automation. Surgeons are still the gold standard for complex procedures, however robots can improve outcomes for minimally invasive and less demanding surgeries significantly, while reducing manpower needed. Hospitals adopt these systems to not just improve precision and reduce complications, but also to lower lifetime patient costs. Platforms like da Vinci might be expensive at the beginning, but in the long term total costs per patient are expected to go down, due to shorter recovery time and fewer staff, together with relevant training required for the procedures.

An aging population across almost every country worldwide just exacerbates demand, with rising volumes in cancer, cardiology, and surgery in general. To keep costs down while providing the best care possible, robotic systems are very likely to be part of the solution.

On the other hand, hospital budgets are under real pressure. U.S. healthcare providers are squeezed by labor costs and reimbursement cuts, while European systems are dealing with decades of misuse of resources and a shortage of skilled workers across the entire medical field. Europe is fighting with incentives to keep skilled medical professionals, without sacrificing quality. High taxes and bureaucratic hurdles weigh on European publicly funded healthcare systems.

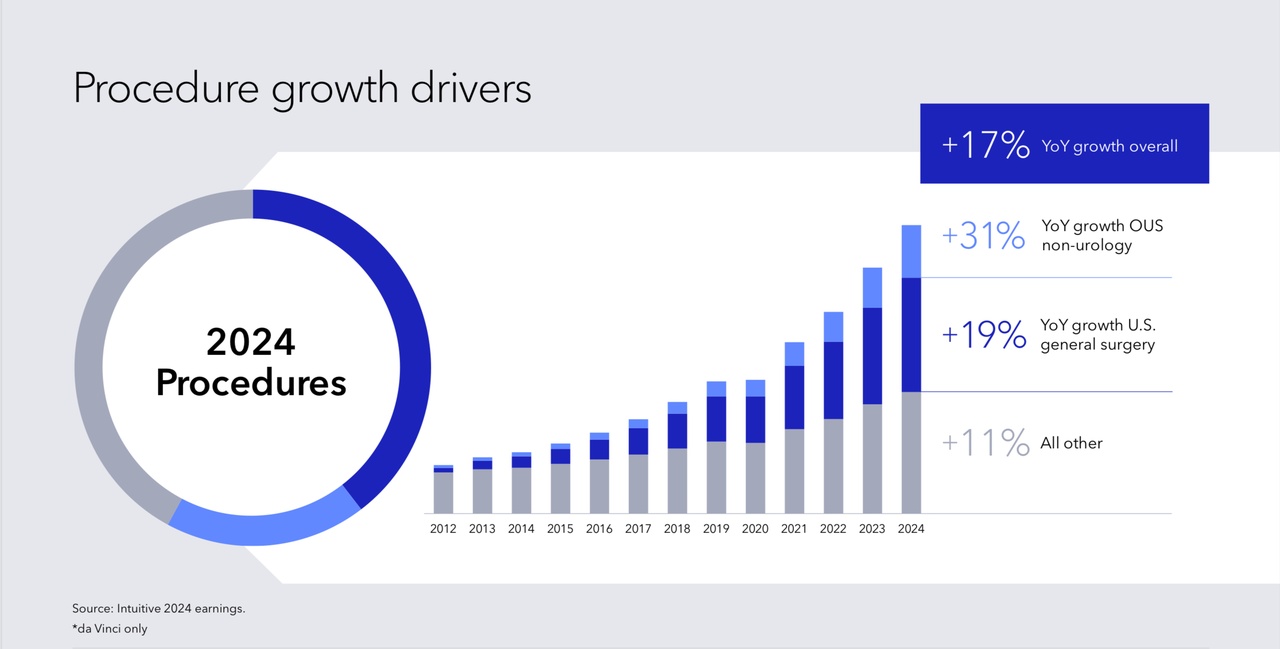

Robotic platforms are expensive upfront, which means adoption can slow in weaker macro environments and economic slowdowns. That is where Intuitive’s installed base matters: even if new system placements decline temporarily, recurring instrument revenue from procedures provides resilience. While new adoption can be cyclical, recurring revenue streams are the compensation.

Regulation is another factor. The FDA is supportive, but reimbursement in international markets can be mixed. Broader coverage in Asia and Europe could materially accelerate adoption. Intuitive reports strong growth across all major regions, however the total addressable market is still huge. With increased pressure, governments are more likely to lower regulatory obstacles rather than tighten them.

3. Company Overview & Segmentation

Intuitive’s business model blends hardware, consumables, and services into a highly profitable ecosystem.

- da Vinci Systems are the company’s flagship platforms, installed in hospitals globally. These carry a high upfront cost, but once in place, they lock institutions into Intuitive’s network. Hospitals are not going to rotate out of Intuitive after they have spent millions on these systems. Currently, Intuitive is the market leader and as they continue to expand, they lock in more and more hospitals worldwide, increasing pressure on competitors significantly.

- Instruments & Accessories are the economic engine. Every da Vinci procedure requires specialized tools, which drives recurring, high-margin revenue. As procedure volumes rise, so does this revenue stream.

- Services provide additional stickiness: hospitals pay for maintenance, upgrades, and surgeon training. This is the safe revenue stream, also in weaker economic cycles.

- Pipeline & Innovation: The da Vinci 5 system, launched in 2024, promises improved ergonomics, imaging integration, and software features. Single-port platforms and future AI-enabled tools extend Intuitive’s reach into new specialties. Intuitive continues to innovate and the perception of new products is excellent.

The key dynamic is utilization. The more procedures each installed system performs, the higher the recurring revenue. This makes procedure growth as important as new system placements. It is a positive feedback loop: an expanding network leads to broader adoption, which leads to an even greater widening of the network and specialized doctors. All that drives recurring revenue in the long term and makes Intuitive a well-positioned company for the future.

4. Financial & Operational Performance

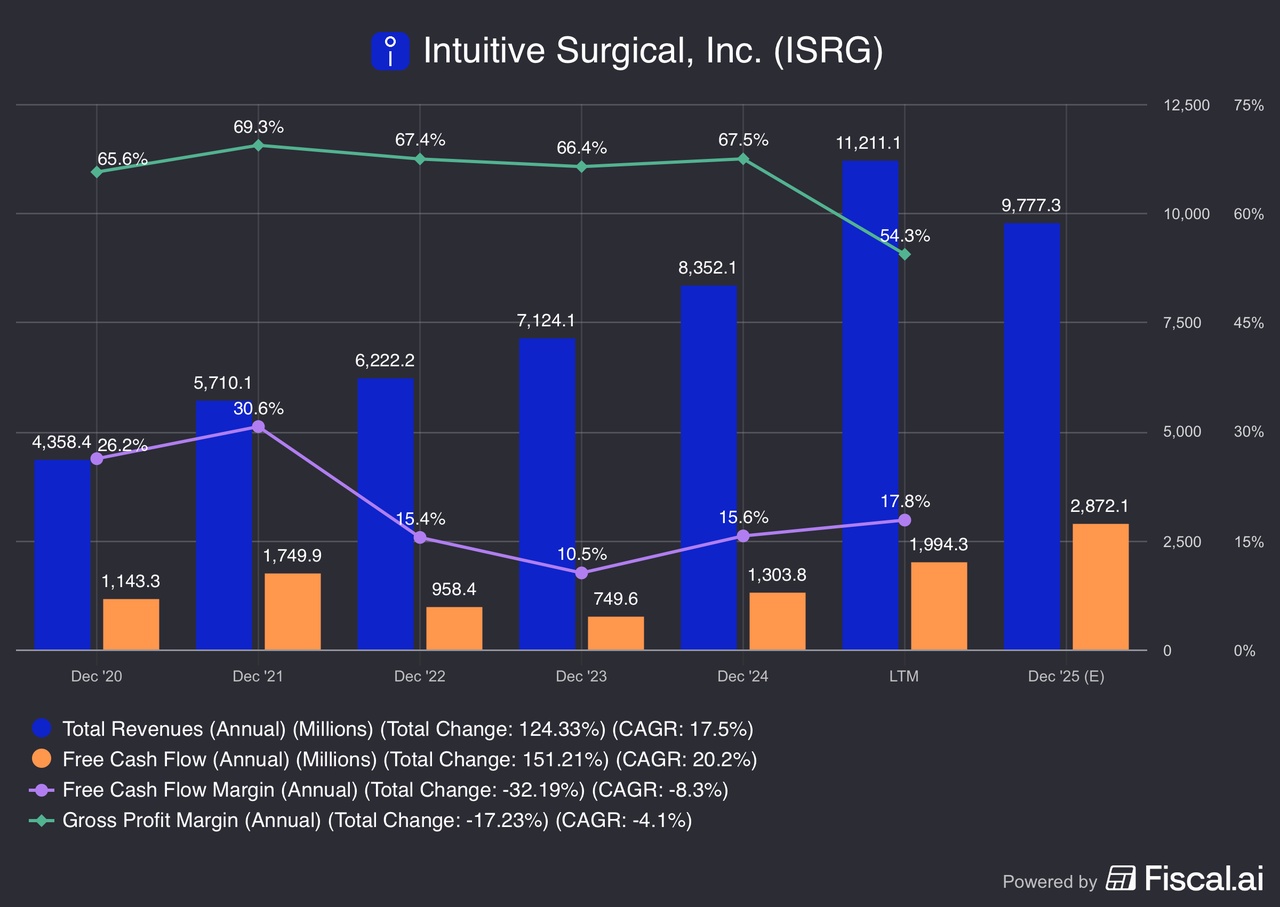

In Q2 2025, Intuitive reported revenue of $2.1 billion, up 12% year-over-year. Procedure volumes grew 15%, highlighting robust demand despite broader hospital budget pressures. Gross margins remained near 67%, while operating income reached $680 million, a margin of about 32%. Free cash flow was comfortably above $500 million for the quarter, and the company continues to run a debt-free balance sheet with over $8 billion in cash.

The financial profile is enviable: recurring revenues account for nearly 80% of sales, margins are consistently high, and the balance sheet gives management flexibility to reinvest or defend against competition. These are the main reasons for the elevated valuation. While maturing and growing into its market-leading position, Intuitive continues to innovate and impress with strong growth numbers. The business is prepared for rapid expansion in good times and can easily survive bad times with its enormous recurring revenue streams.

5. Growth Drivers

The central growth driver is procedure expansion. Urology still remains a core franchise, but demand for general surgery is rising and the shorter recovery times due to minimally invasive robot-assisted surgeries are not to be discounted. Globally the population is aging, which exacerbates demand significantly. Cancer rates are climbing, while robots are advancing. There might be a future in which 95% of all procedures will be, at least, assisted by robots. The initial investment might be hefty for some budget-constrained hospitals, but long-term spend per patient will decrease substantially.

The rollout of the da Vinci 5 is another catalyst. It improves surgeon ergonomics, offers advanced imaging, and is designed for higher throughput, which appeals to hospitals under pressure to do more with fewer resources. Intuitive is addressing concerns about pricing and economic viability through excelling with innovation and making its products “mass-friendlier.” Even more by investing in single-port systems and smaller footprints that can penetrate price-sensitive markets and operating rooms with less space.

International expansion often remains overlooked. The U.S. is relatively mature, especially in the more sophisticated, modern facilities located in urban areas, but Europe, Asia, and emerging markets are still early in adoption. As regulations loosen up, adoption could get a significant boost and further solidify Intuitive as the global market leader.

Finally, longer-term innovation matters. Intuitive is integrating AI and imaging tools into its platforms, with the goal of improving real-time decision-making in the operating room. This optionality keeps the company relevant as digital health evolves.

6. Competitive Landscape

While Intuitive remains dominant, the competitive field is growing more crowded, mainly by small specialized players or large companies trying to take over one particular type of procedure:

- Medtronic (Hugo RAS): The most credible challenger, given Medtronic’s resources and distribution. However, adoption has been slow, regulatory approvals lag Intuitive, and feedback on system performance has been mixed.

- Stryker (Mako): A leader in orthopedic robotics, especially knee and hip replacements. It does not compete directly with da Vinci but shows how specialty robotics can scale. Expansion beyond orthopedics is a risk worth watching.

- CMR Surgical (Versius): A UK-based company offering a modular, portable system with lower upfront costs. Versius has gained traction in Europe and Asia but lacks U.S. approval and the clinical track record of da Vinci. If Versius keeps gaining traction, European systems might prefer it over Intuitive’s products, which could meaningfully erode its sales in that region.

- PROCEPT BioRobotics (AquaBeam): Focused on benign prostatic hyperplasia (BPH), PROCEPT has created a strong niche in urology. While it does not threaten Intuitive across the board, it demonstrates that smaller, focused players can succeed in specialties where da Vinci is less dominant.

The key competing risk at play here is not about one specific rival overtaking it. None of the aforementioned companies compete directly head-to-head with Intuitive, but rather try to snatch small parts of its business individually. This could lead to an erosion in pricing power over the long term, and Intuitive is at risk of becoming the unspecialized legacy company in the middle of very specific competitors. Still, Intuitive’s entrenched base of systems, training cycle, and decades of outcome data and understanding customer needs form an almost insurmountable moat that is difficult to replicate.

7. Risks & Headwinds

Intuitive’s growth strategy stems from hospitals adopting its systems, while the existing network drives recurring cash flows. However, Intuitive’s growth is hindered by hospital budget constraints during downturns. The robot company combats that to some extent through its global engagement and excellence of product, nevertheless a meaningful deceleration of growth prospects might lead to a further decline in the already eroded stock price.

The second and biggest long-term risk is competitive pressure. Regardless of whether one newcomer can ever outshine Intuitive, many new entries in the market could lead to an erosion in its pricing model. Competitive products might never be as advanced, but they could put pressure on the market leader, as smaller hospitals with more constrained budgets might be inclined to choose the “budget-friendly” version.

More broadly, as the field matures, growth rates naturally decelerate, which can be seen in Intuitive’s numbers over the last few years. AI-assisted surgery adoption is still a secular trend, but the likelihood of this happening rapidly and only focusing on one individual company is extremely low.

From an investor’s perspective, it is also crucial to note that the stock is very ambitiously priced at a forward P/E ratio north of 60 and free cash flow yield around 1.9%. This is, in part, justified by an impeccable balance sheet, high recurring revenues, and exceptional market position. However, the stock is priced for perfection, and has fallen almost 30% from its all-time highs, while still being expensive compared to peers. The market is clearly re-rating and re-evaluating the share price at the moment, and negative news could amplify this downward trend substantially.

8. Catalysts & Timeline

Over the next 12 months, the rollout of da Vinci 5 and continued procedure growth will be closely watched. Over the medium term (2–3 years), international adoption and specialty expansion could sustain double-digit growth. Beyond that, the key question will be how Intuitive adapts to a more competitive environment and whether AI integration can create new revenue streams.

Furthermore, the ongoing re-evaluation of the stock price is troubling and might hinder meaningful upside. The market seems to question Intuitive’s recent innovations, leadership changes, and premium valuation. A quality business without a doubt, however the price still matters to investors.

9. Conclusion

Intuitive Surgical is the undisputed leader in robotic-assisted surgery, with a business model built on sticky recurring revenues, exceptional margins, and a balance sheet that removes financial risk. Competitors are eroding the market, but Intuitive has the network and the pricing power to outmatch them. Innovation is still a core part of Intuitive’s culture and its developers continue to dominate the competitive landscape. Some niche alternatives might appear at some points, but the only reason why they can succeed is because Intuitive chooses not to engage. The enormous power this business has held to this day should be appreciated. The landscape is evolving, but Intuitive’s scale and ecosystem remain unmatched.

However, this is not a cheap stock by any metric — it trades at a premium because investors recognize its quality. The question is not whether Intuitive will remain dominant, but whether growth can stay strong enough to justify its valuation as rivals slowly gain ground. There is not much room for disappointments, even after the recent selloff. If investors lose confidence there is still a long way to fall, but Intuitive’s pristine balance sheet might ensure a soft landing. For those looking for exposure to the structural trend of robotics in healthcare, Intuitive is arguably the purest play, combining stability with long-term innovation. The price is only stretched if the company does not deliver, which there is no indication of at this moment.

+ 5

Thanks to bring the Investment idea of procept to me. Could be a Great Chance to be in the Stock from the start. Definitly Need a further Look.

Further conversion

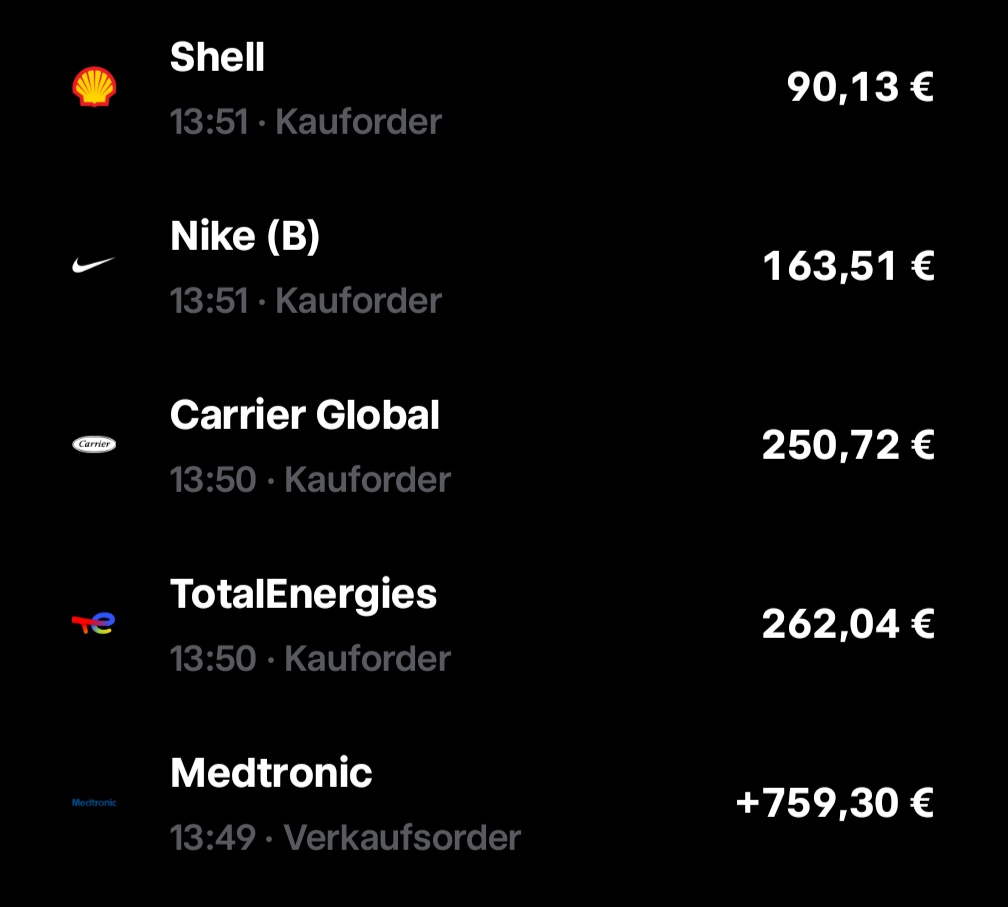

After 4 long years of stagnation and share price decline, I have decided to sell Medtronic and further expand my portfolio in line with my preferences.

To this end, I have reduced my positions

In Shell $SHEL (-0,3%) , Carrier Global $CARR (+0,02%) , Total Energies $TTE (-1,62%) and Nike $NKE (-3,78%) expanded.

With Nike I have now also reached my desired size 😁

There is currently only one single share in the standing order and that is Carrier Global.the standing order on the Vanguard FTSE all-world remains unchanged.

I still intend to $SHEL (-0,3%) , $TTE (-1,62%) , $XYL (+0,29%) , $ECL (-0,89%) and $LIN (-0,64%) to expand.

I am always open to comments and suggestions for improvement 😁

Also really like their business model!

Cells, numbers, doubts: What will BICO print next? (Deep Dive)

🧬 BICO

$BICO (-0,37%) has been on my watchlist since my early days on getquin.

In 2021, the company was on everyone's lips, celebrated as the company of the future in bioprinting.

But what followed was a classic hype cycle: the share price rose rapidly, was cheered by quite a few "finfluencers" and then plummeted just as sharply.

Many people got their fingers burnt back then. What remains is the image of an overvalued tech fantasy, fueled by empty promises and loud voices without substance.

And yet: The company has remained. So has the vision, and in recent months a lot seems to have changed structurally.

Today, more than 80 % below its all-time high, the question arises anew:

Is BICO simply an overrated stock market experiment...

... or is the current valuation realistic for the first time and BICO on the way to translating its technological substance into a genuine business model?

Over the past few weeks, I have been taking a closer look at the company's structure, history and current developments, including the latest figures [1] and the earnings call [2] from 29.04.25.

In this article, I share my collected insights, thoughts and assessments for those who also have the company on their watchlist.

As always:

No investment advice. I don't want to contribute to more burnt fingers, but to encourage reflection.

Have fun!

BICO Group AB (formerly CELLINK) is a Swedish life science company founded in 2016.

The original innovation: a biocompatible ink for 3D printing of living cells, a small revolution in research.

Today, BICO stands for a big goal: Bioconvergence.

This means merging biology, technology, software and automation to make research, diagnostics and drug development faster, cheaper and more efficient.

What is the vision and how does BICO make money?

The vision: The laboratory of the future. Automated, networked, efficient with AI, robotics and bioprinting.

This is how BICO earns money today:

- Bioprinting3D printing of living cells & tissue (CELLINK) read more...

- Diagnostic solutions & microdosing (SCIENION)

- Lab AutomationFully automated workflows through software such as Green Button Go® (Biosero)

- Consumables & services for laboratories and research facilities

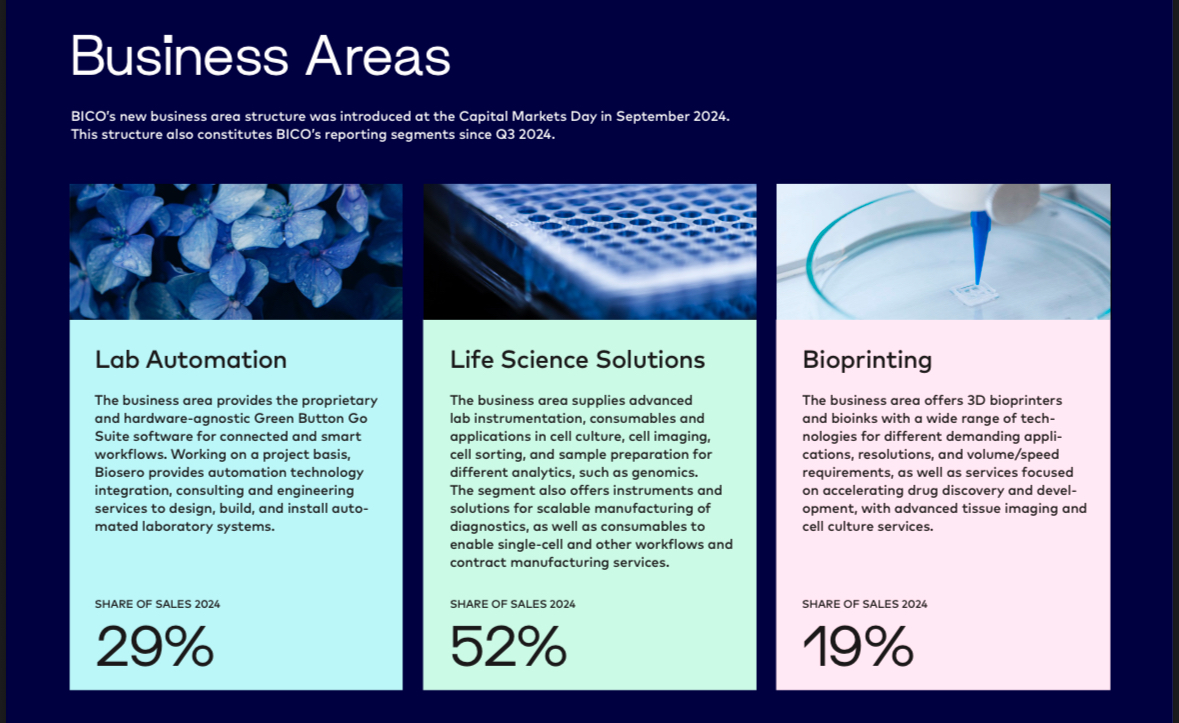

Share of Sales 2024:

Excursus

Bioprinting:

BICO was with CELLINK was one of the first suppliers worldwide to offer bioprinters plus matching "bioinks" commercially.

The basic idea:

- A 3D printer (e.g. the CELLINK BIO X6) prints cells in layers, similar to how a normal 3D printer layers plastic.

- Instead of plastic, a special "ink" is used: Bioink.

Bioink and what it is made of:

Bioink is a gel-like substance that is mixed with living cells. It contains, for example:

- Alginate (from algae)

- gelatine

- collagen

- hyaluronic acid

- Cell nutrient solutions

This matrix keeps the cells alive and makes it possible to print biologically active structures, e.g. tissue samples, tumor models or skin structures.

Is this already being done today or is it all future?

Yes, it is being done, but not clinically.

Bioprinting is currently being used, for example:

- Cell models for drug testing (in research & at pharmaceutical companies)

- printing tumor tissue to better test therapies

- Tissue samples used for toxicology tests (e.g. skin, cartilage, blood vessels)

What is not yet possible:

- Complete organs (hearts, livers, kidneys) for transplants

Because...

- Organs are extremely complex (blood vessels, nerves, functions)

- Currently lack the ability to keep them alive in the long term

- This is also a huge step in regulatory terms

🔮 Future potential: unrealistic or groundbreaking

If bioprinting really breaks through in medicine, we will be talking about one of the biggest breakthroughs of the 21st century:

- organs on demand (no donor needed)

- personalized medicine

- Animal-free drug development

RealisticFirst functional organs could be available in 10 -20 years clinically relevant, but first in small pilot studies or animal models.

Are there any research results or publications on this?

Yes, BICO (especially CELLINK) is a regular co-author or technology partner in publications.

Especially in areas such as:

- Tumor models

- tissue modeling

- biocompatibility

- Skin and cartilage models

Several universities and research institutions use the BIO X printers, including for example MIT and Harvard

Trusted partners:

- Sartorius$SRT (+0,16%) (has taken over MatTek/Visikol, remains cooperation partner)

- AstraZeneca $AZN (-0,82%)

- Pfizer $PFE (+0,09%) (individual case studies)

- Top 20 pharmaceutical companies with Biosero projects (Lab Automation)

- Research centers worldwide

- Cooperation with Sartorius in the APAC region (e.g. Japan, South Korea)

Digression Conclusion

Bioprinting sounds like science fiction and yes, it is a long way from everyday transplantation. But in research and diagnostics it is real, applicable and in demand.

- BICO is not selling promises for the future, but tools that are used in leading laboratories today. The big leap is yet to come, but the foundations have been laid.

__________

History in brief From bioink to platform

- 2016: Founded as CELLINK, the first bioink worldwide

- 2020: Renamed BICO (for Bio Convergence)

- 2021-202315+ acquisitions (including SCIENION, Biosero, MatTek)

- 2024-2025: Streamlining of the structure (sales to Sartorius), withdrawal from non-strategic areas

- 2025: Focus on automation, diagnostics and bioprinting with a clear industry orientation

New CEO since 2024: Maria Forss

- PredecessorErik Gatenholm (co-founder & CEO for many years)

- Change: Gatenholm stepped down in fall 2023, Maria Forss officially became CEO in January 2024

Maria Forss brings decades of experience from leading life science companies:

At Vitrolife (2018 - 2023), she led global expansion and M&A projects, including the billion-euro deal with Igenomix. Prior to that (2014 - 2018), she was at Elekta (radiotherapy, oncology) where she was responsible for global marketing and product strategies.

She started her career at AstraZenecawhere she gained international experience in sales, regulatory affairs and market launch. There she learned what makes large pharmaceutical companies tick, particularly in terms of approval, market launch and regulatory navigation

She is an expert in:

- Business Development

- transformation & strategy

- international expansion

The retirement of founder Gatenholm points to a clear change in strategy, away from visionary, growth-driven development and towards cost control, profitability and integration.

In the Earnings Call Q1 2025 Forss emphasizes several times:

"We have implemented a new operational structure, are harmonizing global functions and are focusing on efficiency and selected growth areas."

📊 Q1 2025 in figures and what's really behind it (Caution currency: Swedish krona, 1 SEK ~ 0.10 USD)

- TurnoverSEK 389 million (-17 %)

- Organic growth: -19 %

- EBITDASEK -12 million

- Cash flow from operating activitiesSEK +77 million

- Net lossSEK -235 million

- Cash positionSEK 684 million

- Convertible bondSEK 1.1 bn outstanding (maturity: March 2026)

Supplement:

Q1 is seasonally weak as many customers (especially in research) do not make large investments at the beginning of the year. At the same time, Q4 was strong, which pulled sales forward.

Comparison of the three previous segments (Q1 2025)

With a view to organic growth:

👩🔬 Life Science Solutions:

- SalesSEK 191 million

- Organic growth: +4 % 👀

- ApplicationsDiagnostics, cell research, microdosing

🧬 Bioprinting:

- Sales105 million SEK

- Organic growth: +41 % 👀

- Applications: 3D cell printing, bioinks, in-vitro models

🔬Lab Automation:

- SalesSEK 94 million

- Organic growth: - 58 %

- ApplicationsAutomation of complete laboratory processes

What do the individual divisions do?

👩🔬 Life Science Solutions:

This is where BICO develops laboratory technologies for diagnostics and cell research, such as devices for high-precision dosing of tiny quantities of liquids, consumables and special analysis platforms.

Examples:

Cancer diagnostics:

- SCIENION devices help to precisely apply tumor markers to test chips, the basis for modern blood tests for early detection.

Allergy tests:

- Using microdosing technology, mini test fields are loaded with allergens to create personalized skin or blood tests.

Genetic testing & DNA analysis:

- Systems from BICO precisely dose minute amounts of liquid onto gene chips, which then analyze intolerances or genetic risk factors, for example.

Point-of-care diagnostics:

- Production of compact rapid test cartridges (e.g. for influenza, RSV, bacterial infections) for home use or the doctor's surgery.

🧬 Bioprinting (see excursus above)

- BICO sells 3D printers for living cells (e.g. from CELLINK) and bioinks, i.e. cell carrier gels for printing tissue.

- ApplicationResearch, drug testing, animal-free toxicology

🔬 Lab automation

This is about the complete automation of laboratories, e.g. robots that create cell cultures, carry out analyses or coordinate samples. Everything is controlled centrally via the Green Button Go® software from Biosero.

💰 How profitable is BICO currently?

BICO is not yet profitable in the traditional sense, as EBIT (operating result) was clearly negative at SEK -290 million in 2024.

However, the operating cash flow a completely different picture: this was 2024 positive at SEK +259 million, as well as in Q1 2025 at +77 MSEK.

This means that BICO is now earning money in its core business, meaning that liquidity is flowing into the company.

The EBIT is still burdened by high depreciation and amortization on earlier acquisitions, research expenditure and, in some cases, one-off restructuring costs.

Conclusion

up to here:

BICO is not yet "through", but the path to operational profitability is recognizable. The company is heading in the right direction, now it depends on whether it can stabilize its operating base and continue to scale its high-margin business areas.

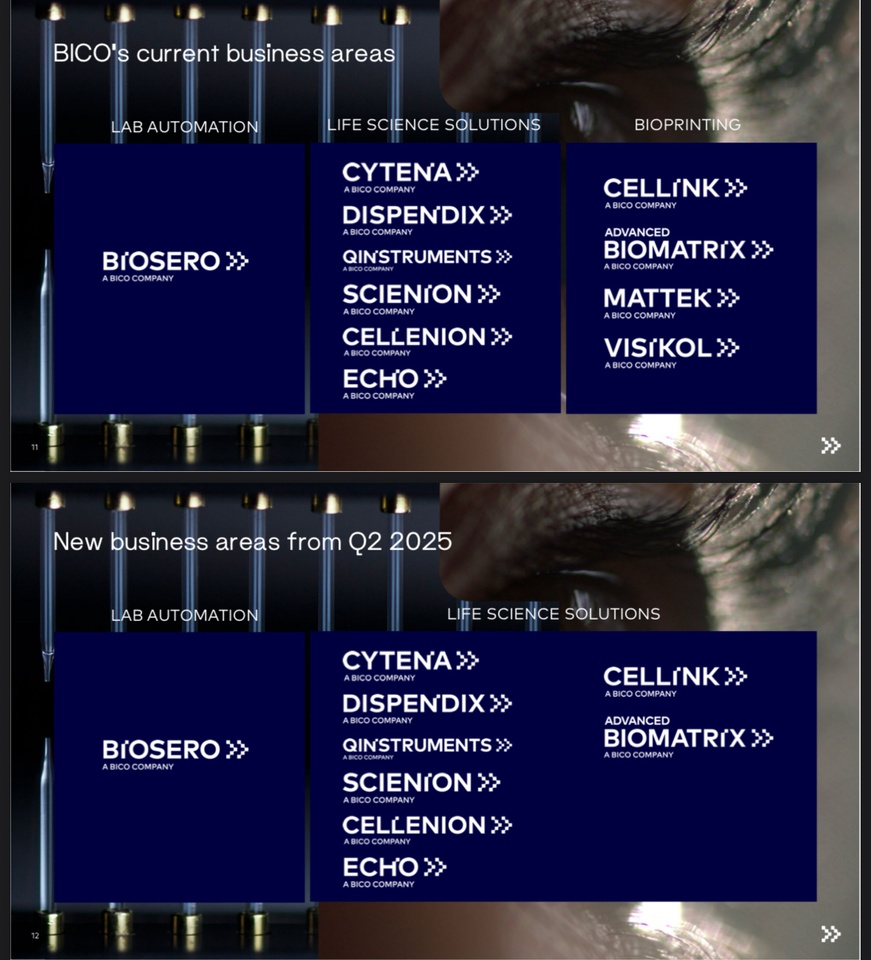

🤝 Business divisions & restructuring (from Q2 2025)

BICO previously operated in 3 segments:

- Bioprinting (e.g. CELLINK)

- Life Science Solutions (e.g. SCIENION)

- Lab Automation (e.g. Biosero)

New from Q2 2025:

Only two divisions, as Bioprinting will be integrated into "Life Science Solutions". Why?

Because CELLINK & Co. are now closely interlinked with diagnostics and consumables. The new setup is intended to increase efficiency, leverage synergies and simplify reporting.

📊 Classification of the figures and why Lab Automation is not growing, even though it is strategically so important

Bioprinting & Life Science Solutions show positive organic growth, while Lab Automationthe third-largest division, shrank massively (-58%).

Automation in particular is one of the main growth drivers in the bioconvergence strategy.

Explanation according to earnings call:

Q1 2024 (PY) was an upward outlier:

- An exceptionally large order from Biosero was booked at that time (project business).

- This effect distorts the basis for comparison, which exaggerates the decline in 2025.

Fewer project starts and completions in Q1 2025:

- Projects in Lab Automation are not distributed linearly, but are completed in phases

- There were simply fewer completed milestones in Q1 = less sales.

Macro-related reluctance on the part of major customers (pharma):

- Investment decisions were delayed, not canceled.

According to CEO Maria Forss:

"The underlying demand for Lab Automation continues to be strong."

"Project cycles are longer - but demand from pharma remains intact."

Project business is naturally volatile:

- Lab Automation is not recurring, but order-based.

- This leads to strong quarterly fluctuations - even with a stable order backlog.

BICO's strategic response

Standardization of project packages:

- Shorter durations, modular solutions to cushion order fluctuations

Strengthening project management:

- To better control time delays and resource commitment

Focus on pharmaceutical customers:

- Cooperation with "Top 20 Pharma Companies" is being expanded, geographically flexible (USA, EU, Asia)

➡️ The decline in sales in Lab Automation looks dramatic, but is primarily due to timing and not a structural problem.

BICO is responding with strategic adjustments to its product portfolio and points to continued strong demand, only with longer lead times.

For investors, this means that the decline is unfavorable but explainable, not alarming

Further statements from the earnings call

CEO Maria Forss:

"Despite a decline in sales, Life Science Solutions and Bioprinting are showing positive development. Our strategy adjustment is taking effect."

- Bioprinting is booming: +41 % organic, CELLINK +130 % (on a low basis)

- SCIENION stabilizes Diagnostics: Miniaturization & home testing drive demand

- USA weakness in research: Reluctance to invest among academic customers due to uncertain NIH funding

- Tariffs & macro volatility: BICO has shifted production out of China, flexed supply chain

- Divestments: MatTek & Visikol sold, enables net cash position in Q2 2025

Why is bioprinting booming right now?

- New regulatory trends: FDA allows animal testing alternatives

- Increasing demand for in-vitro tissue models

- International expansion (e.g. India, Asia)

- Favorable product mix (bioinks, consumables)

Excursus in-vitro tissue models:

"In vitro" means: outside the living body, e.g. in a petri dish, on a chip or in a laboratory device.

Tissue models are replicated biological structures that resemble real human (or animal) tissue.

Example:

A skin tissue printed with cells that is used for cosmetic or drug tests, without animal testing.

What's the point?

- Safety & efficacy tests (e.g. for drugs, chemicals)

- Disease models (e.g. tumor tissue for cancer research)

- Personalized medicine (tissue from own cells)

In vitro tissue models are an ethically and scientifically attractive alternative to animal testing and BICO supplies the printing technology for this, among other things.

Is BICO a unique company in bioprinting?

No, but one of the pioneers with a broad portfolio.

There are competitors such as Allevi, Aspect Biosystems and Organovo, but BICO combines hardware, software and services under one roof - a strategic advantage.

Where does the market currently stand and what does the future look like?

- The market for bioconvergence is still young, provocatively speaking perhaps comparable to the cloud in 2010

- Applications such as automated laboratories, in-vitro models and AI-supported diagnostics are in their infancy

- Long-term demand is enormous for personalized medicine, increased efficiency and ethics (e.g. avoidance of animal testing)

Possible future scenarios

1 . BICO becomes a global playerBICO continues to grow, automates laboratories worldwide

2 . BICO becomes a takeover candidate: Groups such as Sartorius $SRT (+0,16%) , Danaher $DHR (-1,78%) or Thermo Fisher $TMO (-0,69%) could strike

3 . BICO remains niche leader: Focused on profitable segments with high innovation density

Risks & critical voices

- Unprofitable: No sustainable EBIT coverage yet

- Convertible bond (SEK 1.1bn, equivalent to USD 114m): Maturity 2026, repayment depends on cash flow & divestments

- Risk of dilution if convertible bond is serviced via shares

- Strong dependence on projects -> sales fluctuations

- Competitive pressure from large corporations

The topic of the convertible bond has made me sit up and take notice again; here are some more deep dives:

What's the deal with BICO's convertible bonds until 2026?

Convertible bonds are a kind of hybrid between a bond and a share. They work like this:

- Investors lend money to BICO (e.g. SEK 1,000)

- BICO pays interest in return

At the end of the term (March 2026), investors receive either:

- the money back

- or can convert the bond into shares - depending on the agreed price

The whole thing is attractive for companies because they:

- only have to pay interest at first, no return of capital

- and can often offer a lower interest rate because the conversion option is attractive

What this means in concrete terms:

- BICO originally had convertible bonds with a volume of over SEK 1.5 billion

- SEK 394 million have already been repurchased in 2024 & 2025

- Currently open (as of Q1 2025): SEK 1.106 billion (114.5 million USD)

- Maturity date: March 2026

Why is this an issue for investors

1 . Repayment or dilution:

If BICO cannot repay the amount, new shares must be issued, this is called dilution because your stake in the company decreases.

2 . Cash flow burden:

If BICO wants to repay the amount from its own resources, it needs a lot of liquidity, which can slow down other investments.

3 . Refinancing risk:

If the market is weak in 2025/26, refinancing could become expensive or not possible at all.

What is the current situation?

Positive:

- BICO currently has SEK 684m in cash (USD 71m)

- The sale of MatTek & Visikol will put BICO in a net cash position in Q2 2025

- Target: Early extinguishment of convertible bond 2026

Statement on financing / repayment

CFO Jacob Thornberg said:

"The closing of the divestment of MatTek and Visikol for USD 80 million is expected to take place during Q2 2025 [...]

The proceeds from the transaction will be used to resolve the outstanding convertible bond, which matures in March 2026."

Translated:

The entire proceeds from the sale of MatTek & Visikol to Sartorius (USD 80 million) are earmarked for the repayment of the convertible bond.

Management's assessment of the financial position:

"We expect to move into a net cash position during Q2 2025."

This means:

- After the transaction, BICO will have more cash and cash equivalents than debt

- These funds should enable repayment in 2026 without further dilution

Assessment: How credible is this?

Positive:

- BICO shows clear plan: repayment of convertible bond is top priority

- Cash position Q1: SEK 684m

- Sale of MatTek & Visikol: approx. SEK 870m (converted)

-> Repayment can be financed if no new setback occurs

But:

- The operating business is not yet making a stable contribution to financing

- New investments or declining sales could jeopardize the plan

- Market environment remains volatile (interest rates, project delays, etc.)

➡️ Management is actively pursuing the plan to redeem the convertible bond in full before maturity in 2026 without dilution.

The sale of MatTek & Visikol has freed up concrete capital for this.

The direction is right, but BICO remains a risky stock with operational debt.

More on profitability:

In the Q1 2025 Earnings Call BICO's management did not give a specific date for break-even or profitability

... which is typical for growth companies with highly volatile project business.

What was said instead?

On profitability in Q1 itself:

EBITDA was negative (SEK -12m), but:

"Adjusted EBITDA was in line with Q1 2024 due to the positive development in Life Science Solutions and Bioprinting."

-> Improvement due to mix effects and operational measures

- The positive margins from Q4 2024 could not be maintained, mainly due to Lab Automation weakness.

Long-term statements?

No specific annual figure or guidance on profitability. But:

"We have launched a new operating model [...] to achieve improved commercial as well as operational efficiencies."

"We will continue to optimize our cost base and drive efficiency through integration."

Interpretation:

- Management is actively working on profitability

The focus is on the short term:

- Cash flow

- Efficiency gains

- Segment focus

Butunfortunately no clear words like: "We plan to be profitable in 2025 or 2026." 😬

Will BICO be the company that prints organs, or is it more likely to be taken over?

Technologically, BICO is very well positioned today when it comes to bioprinting infrastructure:

- Hardware (BIO X printers)

- Bioinks (cell-compatible inks)

- Software & automation

- Worldwide customer base

ButPrinting fully functional organs for clinical applications is a gigantic leap, not only technologically, but also in regulatory, medical and logistical terms. This is what is needed:

- billions in long-term capital

- Clinical studies over many years

- integration into healthcare systems and transplant networks

These are competencies that are more common in corporations like Johnson & Johnson $JJ, Medtronic $MDT (-1,04%) , GE Healthcare $GEHC (-0,74%)

, Siemens Healthineers $SHL (+0,15%) or Thermo Fisher $TMO not a smaller platform provider like BICO.

Which is more likely?

1 . BICO remains the "toolmaker" of the bioprinting world:

Just like ASML for semiconductors or Illumina for genomics, but without building drugs/organs itself.

2 . BICO will be taken over when the topic becomes clinically concrete:

For example, when the first major organ projects enter the clinical phase, it is likely that a giant will strike to secure access to the technology.

3 . BICO remains an enabler, but not the final provider of clinical bioprinted organs

When organs are actually printed, will BICO become the global market leader?

🏷️ Unlikely.

➡️ More realistic is that BICO becomes one of the key technology suppliers or is taken over by one of the big players beforehand.

This can still be highly attractive for investors. After all, whoever supplies technology will be needed, regardless of who ends up operating on the patient.

Should we now focus on BICO or rather on a large corporation with bioprinting potential? 🤔

1 . Buy BICO for speculative returns

Pros:

- Favorable valuation after the "crash/hype" (more than 80 % below all-time high)

- One of the technology leaders in bioprinting

- Strategic focus, efficiency program, divestments, clear direction

- Enabler position in a highly scalable future market

- Possible takeover candidate = extra share price potential

Contra:

- Not yet profitable, operational risks exist

- Market for organs is still many years away

- Capital structure (convertible bond) is a medium-term uncertainty factor

- If large investors fail to materialize, BICO could be technologically overtaken

2 . Alternatively: back a large corporation for more stability

Which big players have the potential to drive bioprinting forward (or take over BICO)?

Sartorius

- Already has close cooperation with BICO (and acquired MatTek/Visikol)

- Focus on cell biology, diagnostics & laboratory automation

- Strong in APAC region and with biotech customers

-> Best-case candidate for takeover or joint venture

Thermo Fisher Scientific

- Global leader in laboratory equipment, genomics, diagnostics

- Great financial strength, active M&A strategy

- So far, however, more focused on classic diagnostics

-> Comes into play when bioprinting is more closely integrated into pharmaceutical production

Danaher

- Parent company of brands such as Cytiva and Beckman Coulter

- Very active in diagnostics and research technology

- M&A-driven, high margin focus

-> Could strike when the market matures, but rather late and strategically

3D Systems / Stratasys

- Directly active in 3D printing

- Have already acquired bioprinting units (e.g. Allevi)

- Fluctuating in strategy & implementation

-> Riskier than classic medtechs, but a direct bioprinting play

Personal classification: substance or science fiction on credit?

What makes more strategic sense? Which investment is "the right one"?

- High potential return and very high risk tolerance: Then BICO

- Takeover speculation: Then BICO or e.g. Sartorius

- Stable yield and dividend: Then Sartorius, Dabaher or Thermo Fisher

- Bet on "market leader of the future": Then wait and see, today there is no clear bioprinting world leader

OR

Combination strategy:

I invest a small position in BICO as a "moonshot", combine this with a solid underlying position in Sartorius or Thermo Fisher and cover the technology and protect the capital if BICO fails.

The two underlying positions mentioned can of course also represent a global ETF.

My personal assessment of BICO currently fluctuates between cautious optimism and realistic doubt.

On the one hand, I see a clear technological lead and a strategy that, unlike a year or two ago, now appears more well thought-out and focused. Partnerships with established players such as Sartorius also give me the feeling that BICO is not operating alone in a vacuum.

On the other hand, the operational foundation is still shaky. Profitability has not been achieved and the issue of the 2026 convertible bond hangs over the company.

Without sufficient cash flow or fresh capital, the ambitious vision could stumble, and despite all the enthusiasm for bioprinting and automation, we should always be aware of this.

BICO is not a stock for quiet nights, but for visionaries with patience it may be a ticket to the future of medicine.

I am currently waiting for an entry opportunity with a good feeling. The goal could be a portfolio share of up to approx. 3-4%, which then remains in place and is reduced in the future through portfolio growth without selling.

Thanks for reading! 🤝

______________

Sources:

[1] https://storage.mfn.se/5a3030c0-d13b-4177-80d0-94da59c7302d/bico-q1-2025-eng.pdf

[2] https://bico.events.inderes.com/q1-report-2025/register

/ https://web.quartr.com/link/companies/4484/events/247443/transcript?targetTime=0.0

More:

https://www.sartorius.com/en/company/investor-relations

I've been in BICO before and looked into it a bit back then. However, I got in at the wrong time and bought a bit on the dip, as it happens XD. At some point I threw the position out at a loss, BUT I still like it and keep it on my watchlist.

I don't see any "good" reason to get in right now. If you want to gamble, now would of course be a better time than back then. But it is what it is, and if you're looking for excitement and thrills, you've come to the right place. But then don't invest more than you think is appropriate for a rollercoaster for fun....

They don't have a long cash runway, as you describe, and still have a lot to do to reposition themselves after all the acquisitions. They are currently restructuring themselves, that's true, but in my view there's nothing to be said against waiting until there are the first signs that this will lead to something.

You say below that it is not a stock for quiet nights but for "visionary investors with patience". I would question whether the visionary investor "with patience" should not simply stay tuned at this point and patiently inform himself about the company and leave it on the WL until then...

PS: I also have something in my portfolio that has more in it because I enjoy finding out about the company and it's kind of nice to be in it. But it's not an investment case, it's more of a hobby and an emotion, inspired by an interesting idea etc....

Medtronic Q3'25 Earnings Highlights

🔹 Adj. EPS: $1.39 (Est. $1.36) 😐; UP +7% YoY

🔹 Revenue: $8.29B (Est. $8.33B) 🔴; UP +2.5% YoY

🔹 Organic Revenue Growth: 4.1% YoY

🔹 Adj. Net Income: $1.79B (Est. $1.74B) 😐; UP +3% YoY

FY'25 Guidance

🔹 Adj. EPS: $5.44-$5.50 (Est. $5.45) 🟡

🔹 Organic Revenue Growth: 4.75%-5%

Q3'25 Segments

🔹 Cardiovascular Revenue: $3.04B (Est. $3.04B) 🟡; UP +3.7% YoY

- Cardiac Rhythm & Heart Failure: $1.55B (Est. $1.53B) 🟢; UP +5.1% YoY

- Structural Heart & Aortic: $874M (Est. $874.71M) 🟡; UP +3.7% YoY

- Coronary & Peripheral Vascular: $618M (Est. $632.14M) 🔴; UP +0.3% YoY

🔹 Neuroscience Revenue: $2.46B (Est. $2.45B) 🟢; UP +4.4% YoY

- Cranial & Spinal Technologies: $1.25B; UP +3.8% YoY

- Specialty Therapies: $732M; UP +0.8% YoY

- Neuromodulation: $476M; UP +12.0% YoY

🔹 Medical Surgical Revenue: $2.07B (Est. $2.13B) 🔴; DOWN -1.9% YoY

🔹 Diabetes Revenue: $694M (Est. $681.77M) 🟢; UP +8.4% YoY

Q3'25 Geographical Performance

🔹 U.S. Revenue: $4.24B; UP +2.8% YoY

🔹 International Revenue: $4.06B; UP +2.2% YoY

Announcements & Strategic Updates

🔸 U.S. FDA approval for additional PFA manufacturing site in Galway

🔸 CMS coverage for Renal Denervation expected by Oct 11, 2025

🔸 Exclusive distribution agreement with Contego Medical for carotid stenting

Management Commentary

🔸 CEO Geoff Martha: "We delivered strong earnings this quarter, with significant improvements in both our gross margin and operating margin on the back of our ninth quarter in a row of mid-single digit organic revenue growth."

🔸 Interim CFO Gary Corona: "EPS came in above the high end of our guidance range. We were pleased with the operational performance of the business this quarter, turning mid-single digit organic growth into leveraged earnings."

Megatrend: Investment opportunities due to an ageing population worldwide

The world's population is getting older and older, an irreversible demographic change with considerable economic consequences.

This article is intended to provide investment ideas and impetus. The stocks mentioned do not, of course, constitute investment advice, but merely serve as examples of potential beneficiaries of demographic change. Historical developments are no guarantee of future returns.

The main source is the short analysis "How to invest as the global population ages" by Goldman Sachs [1], which, however, does not name any specific stocks.

I have also added additional sources and charts.

__________

🌍 Demographic change: growth and ageing of the world's population

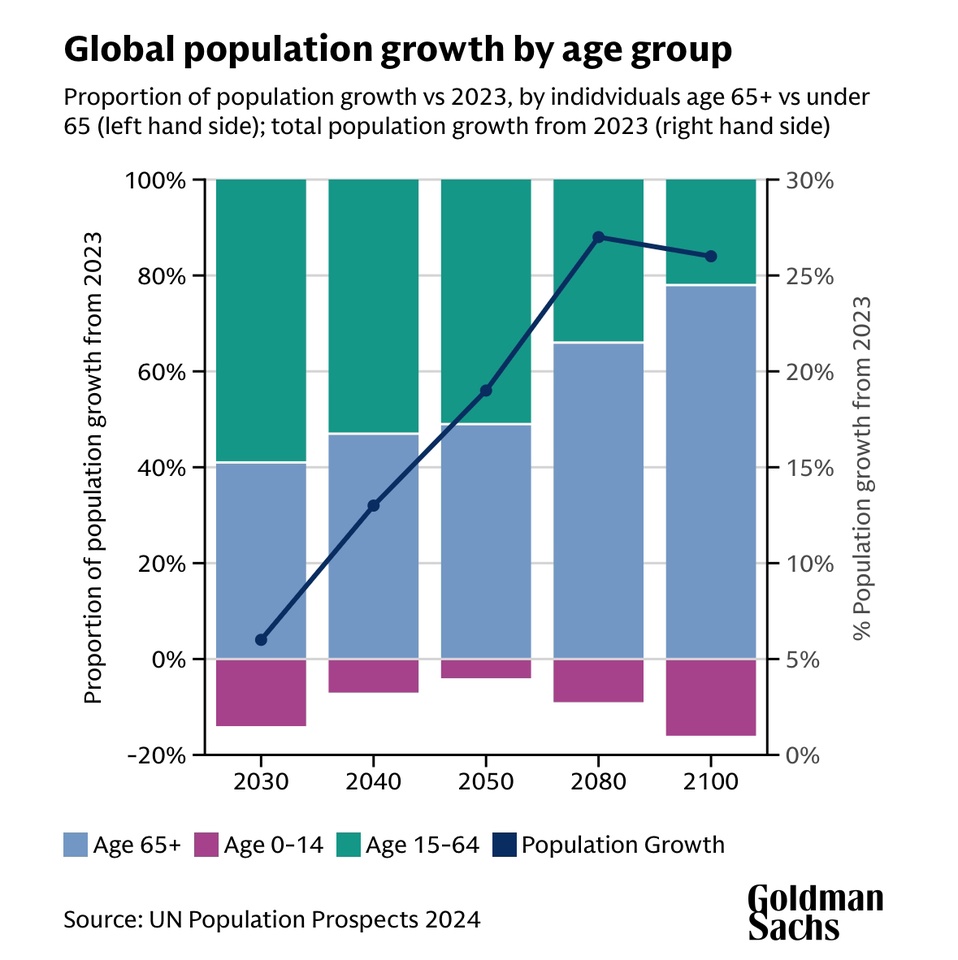

The world's population will grow to almost 10 billion people by 2050. However, it is not just the number of people that is increasing, their age structure is also changing dramatically. [2]

Increase in the older population:

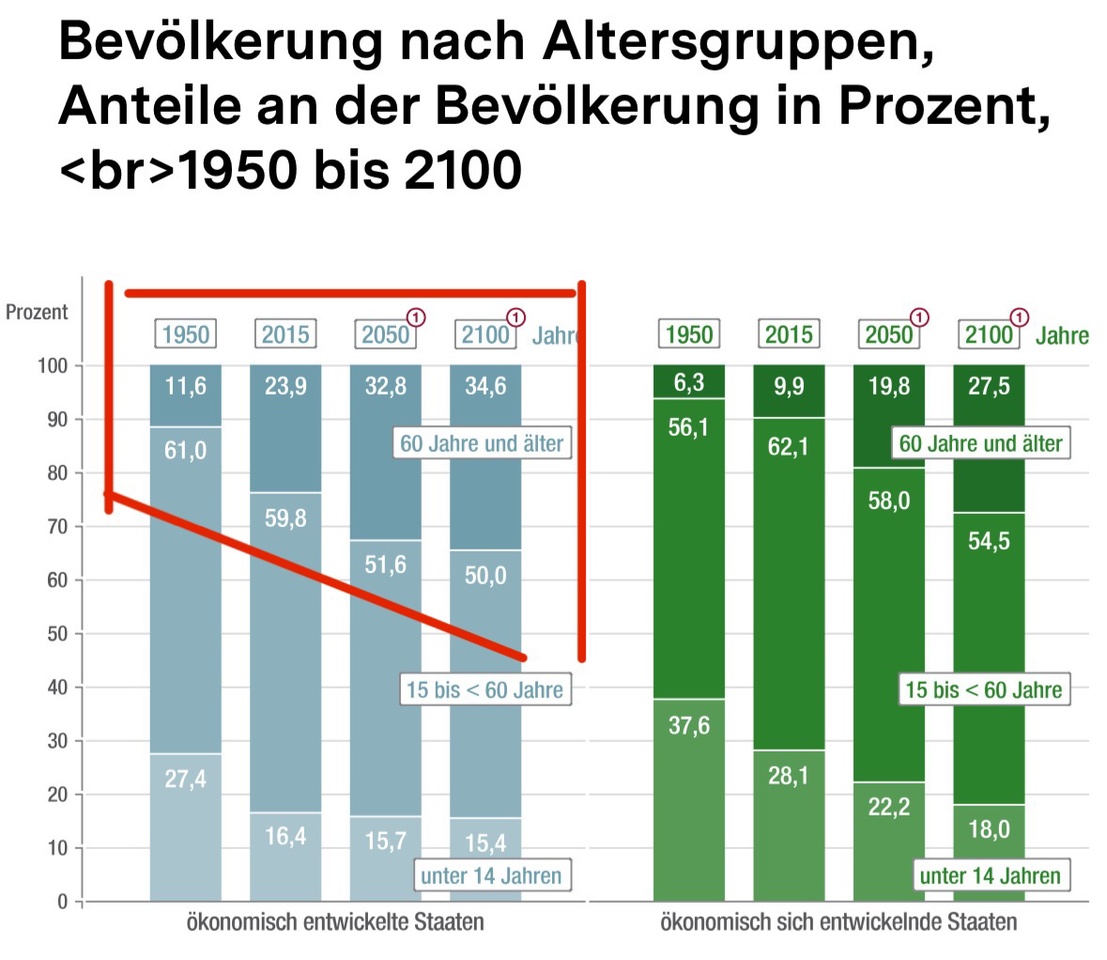

- The proportion of people aged 60 and over is rising from 8% (1950) to 21.5% (2050).

- In 2050, 2.1 billion people will belong to the over-60 age group.

Source: [2]

Regional differences:

Europe & North America have the oldest populations & remain the most affected demographically.

Latin America, the Caribbean & Asia: The proportion of over-60s will more than double between 2015 and 2050, reaching around 25 %.

Africa remains the youngest region: in 2015, there were 21 countries worldwide with a birth rate of 5 children per woman, 19 of which were in Africa. However, it should be noted that current statistics from 2024 show that the birth rate per woman in Africa was already just 4.07 in 2023 and could fall to 2.79 by 2050. [3]

While industrialized countries are struggling with an ageing society, Africa remains the most dynamic and youngest region in the world. This development can also have an economic impact and open up new investment opportunities. [2]

Goldman Sachs also comments in the article with similar figures, according to which the global population is expected to increase by around 20% by 2050 and senior citizens will make up a disproportionate share. The number of people over the age of 65 is expected to double from 800 million to 1.6 billion during this period. [1]

In view of this demographic development, there are opportunities to benefit from precisely this trend. Opportunities lie in targeted investments in sectors that could benefit from the growing proportion of older people.

🚑 Healthcare: A growing market worth billions

Facts:

- In the USA, people over the age of 65 already account for 36% of healthcare expenditure, although they only make up 18% of the population. Age-related diseases such as cardiovascular disease, diabetes and neurological disorders are driving up costs. [1]

- Alzheimer's cases are even expected to double worldwide by 2050.

Possible profiteers:

Medical technology

- Medtronic ($MDT (-1,04%) ) - (cardiac pacemakers, diabetes technology)

- Stryker ($SYK (-0,32%) ) - (orthopaedic implants, surgical devices)

- Siemens Healthineers ($SHL (+0,15%) ) - (imaging, diagnostics)

Pharmaceuticals

- Novo Nordisk ($NOVO B (+1,09%) ) - (Diabetes & Obesity)

- Eli Lilly ($LLY (-0,32%) ) - (Alzheimer's, Diabetes)

- Roche ($ROG (+0,75%) ) - (Oncology, Diagnostics)

🏡 Senior Living & Care: Bottlenecks in nursing homes worldwide

Facts:

The UK has a shortfall of over 30,000 senior units by 2028. [1]

In Germany, France and Italy there is a shortage of nursing home places due to the ageing population. [1]

In the US, only 2% of people over 65 live in nursing homes, leading to an increasing demand for home care and telemedicine. [1]

Potential beneficiaries:

Care providers

- Brookdale Senior Living ($BKD (+0%) ) - (senior living, care facilities)

Homecare

- ResMed ($RMD (+0,32%) ) - (sleep apnea, ventilators)

- Fresenius Medical Care ($FME (-6,41%) ) - (dialysis, home therapy)

- Coloplast ($COLO B (-2,2%) ) - (stoma care, incontinence products)

Telemedicine

- Teladoc Health ($TDOC (-0,5%) ) - (virtual doctor visits, digital health solutions)

- Hims & Hers ($HIMS (+0,19%) ) - (telemedicine & e-health)

Anti-Aging

- L'Oréal ($OR (-0,73%) ) - (skin care, cosmetics)

- Estee Lauder ($EL (-0,68%) ) - (luxury cosmetics, skin rejuvenation)

- Revance Therapeutics ($RVNC ) - (Botox alternative, wrinkle treatment)

🚢 Leisure & consumption: The new "silver economy"

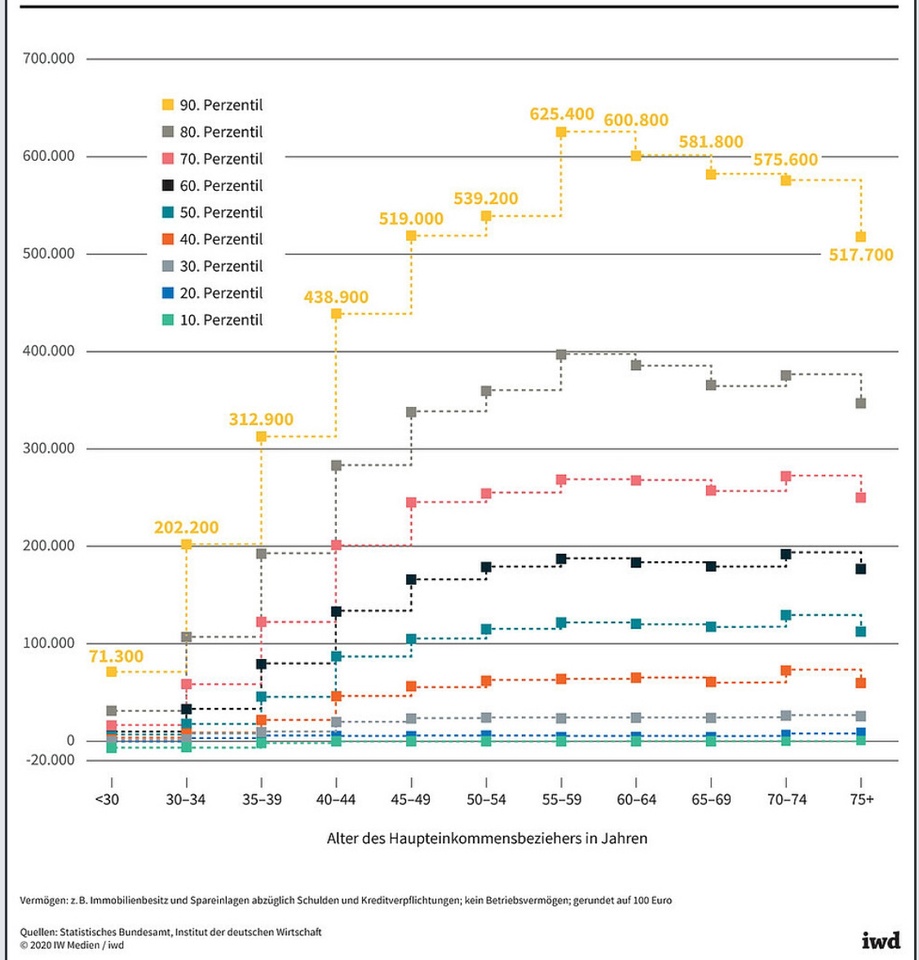

The following chart shows the distribution of wealth in Germany depending on the age of the main income earner. [4]

It is clear that older people tend to have higher wealth than younger age groups. This is reflected in the significantly higher values for the percentiles for age groups aged 50 and over. In particular, the groups aged between 50 and 74 have the highest assets.

The trends are also similar internationally:

- The wealth of older people is 3x that of millennials.

- Over-60s control more than 50% of consumer spending in many developed countries.

- The global silver economy could reach a volume of USD 15 trillion by 2030 (Oxford Economics).

This observation underlines the economic importance of the older generations and their central role in wealth distribution and consumer spending.

Possible beneficiaries:

Luxury

- LVMH ($MC (-1,8%) ) - (fashion, jewelry, wine & spirits)

- Hermès ($RMS (-0,89%) ) - (Exclusive Fashion & Accessories)

- Richemont ($CFR (+0%) ) - (Swiss luxury watches & jewelry)

Cruise (Over 60s book a third of all cruises worldwide [1])

- Royal Caribbean ($RCL (+0,69%) ) - (Cruises for seniors & families)

- Carnival ($CCL ) - (mass market cruises)

- Norwegian Cruise Line ($NCLH (+1,55%) ) - (premium cruises)

Motorhome manufacturers/ recreational vehicles (47% of motorhome users are over 55 years old, In the UK, two thirds of over 55s have a motorcycle license, which may indicate a growing market for motorcycles and accessories. [1])

- Thor Industries ($THO (+1,3%) ) - (motorhomes, campers)

- Winnebago ($WGO (+1,47%) ) - (motorhomes & caravans)

- Harley-Davidson ($HOG (-0,69%) ) - (motorcycles and entry-level electric motorcycles)

🤖 Technology & automation: solution to the labor shortage

Facts:

The labor shortage caused by an aging society is becoming a global challenge. Automation, AI and robotics could help close the skills gap. [1]

Profiteers:

- ABB ($ABBNY (+2,2%) ) - (industrial robotics, automation)

- Fanuc ($6954 (+1,96%) ) - (robotics, factory automation)

- Intuitive Surgical ($ISRG (-0,6%) ) - (robot-assisted surgery)

- Siemens ($SIE (+0,67%) )- (automation & also medical technology)

🧠 Conclusion:

Demographic change offers long-term investment opportunities. Early investment in the right sectors can benefit from rising spending on health, care, leisure and technology.

I myself am still looking for one or two individual investments and am a little annoyed that I didn't get into Hims & Hers earlier, although I have been on the verge of doing so several times. Apart from the luxury segment with LVMH, the portfolio also includes Siemens as a conglomerate in the field of automation.

Do you explicitly take demographic change into account in your investments, e.g. in the form of individual shares?

Which shares do you have in your portfolio or do you still see them as an opportunity?

Thanks for reading!

_________

Sources:

[1] https://www.goldmansachs.com/insights/articles/how-to-invest-as-the-global-population-ages

[2] https://www.bpb.de/kurz-knapp/zahlen-und-fakten/globalisierung/52811/demografischer-wandel/

[4]

https://www.iwd.de/artikel/mit-dem-alter-waechst-das-vermoegen-489710/

Títulos em alta

Principais criadores desta semana