Here I have secured the profit-taking and put it into my FTSE all world

SLB Limited

Ação

Ação

ISIN: AN8068571086

Ticker: SLB

AN8068571086

SLB

Price

Discussão sobre SLB

Postos

23

6Mês·

Venezuela! Who will win?

So at this late hour, a few more thoughts on the topic and the results of my research.

After I was still clearly in favor of $SLB (+1,37%) I now see the profiteer with the greatest leverage as actually being $COP (+0,12%) ! They were expropriated by Maduro's predecessor Chavez in 2007. Unlike $CVX (+2,08%) they took action against it at the time and were awarded $8.37 billion. The value is now estimated at $10 billion due to interest etc. As Venezuela will certainly not be able to pay the money, it can be assumed that it will be exchanged for real assets such as exclusive production rights, preferential export quotas or joint ventures. This would give $COP access to reserves and cash flows without first having to make large investments like its competitors.

I think if I wanted to play the Venezuela card, I would therefore $COP (+0,12%) as a top pick.

2323

15 Comentários

Hi Chris, that is a sophisticated take on the situation. Your shift from $SLB to $COP tells the difference between a "service play" and a "recovery play." While $SLB wins if people start drilling, $COP wins if the legal architecture of the entire country is rewritten. If you want a steady hand, it's still $CVX. If you want a greater "turnaround" play based on legal restitution, $COP is the smarter pick imo as you said yourself. ;)

•

33

•6Mês·

Profit from the freedom of Venezuela? 🇻🇪

What do you think of buying $CVX (+2,08%)

$SLB (+1,37%) to profit from future oil production?

And what do you think of $ASHM (+0,7%) to profit from the payment of open bonds?

PS:

I am very happy about coins as a donation in the comments, because I would very much like to afford a premium membership or merch :)

44

13 Comentários

I hope that satisfies your hunger for this week.

•

1212

•6Mês·

🇻🇪 Venezuela quake on the oil market - Who are the profiteers of the upheaval? 🛢️🚀💰

Good morning everyone and a green start to the first full trading week of 2026!

The year is barely five days old and there have already been numerous events around the world.

Probably the most eventful event (can you write it like that? 🤔) is the one at the weekend surrounding Maduro's arrest.

While the oil price remains volatile due to the global oversupply, clear winners are emerging today (05.01.2026) from the US intervention.

1. the "top dog": Chevron $CVX (+2,08%)

🏗️

Chevron is the clear favorite today. As the only US company to remain operational in the country, they have the "first mover" advantage.

If the sanctions are lifted, the billions will flow into repairs first.

_________________________

2. the service giants: SLB $SLB (+1,37%)

& $HAL (+2,23%)

🛠️

No matter who is producing: The plants in Venezuela are dilapidated. Schlumberger is currently benefiting massively from speculation on major technology contracts.

Without Western know-how, Venezuela will not be able to significantly increase production.

_________________________

3. the US refineries: Marathon Petroleum $MPC (+0,73%)

& Valero $VLO (+0,74%)

⛽

The US Gulf Coast specializes in "heavy" crude oil from Venezuela. A return of this oil improves the margins of Marathon Petroleum and Valero massively, as expensive import alternatives are eliminated.

_________________________

4. US defense: Lockheed Martin $LMT (+0,18%)

🛡️

Instead of European second-line stocks, the industry leader Lockheed Martin is moving into focus. The US intervention underlines the military presence in the region. very Such geopolitical tensions secure the group's long-term political backup for defense budgets.

_________________________

5. the "safe haven" effect: gold breaks records 🏆✨

Gold is the absolute rock in the surf today. Due to the uncertainty, the spot price fell by over 2 % upwards this morning and has passed the 4,420 USD per ounce!

- Barrick Gold $ABX (-2,6%)

& Newmont $NEM (-2,48%)

: Mining stocks rally strongly.

- Background: Venezuela is sitting on gold reserves worth around USD 22 billion - the question of who will have access to them is also driving speculation.

_________________________

What's your situation? Have you already invested in one of the stocks? Or are you planning to?

7Mês·

Equities | Jeffries best sectors ideas

$JEF (-0,92%) Top picks per sector for 2026

$APP (-2,64%) , $UBER (+0,59%) , $SPOT (-4,04%) , $RDDT (-0,04%) , $ROKU (+0,03%) , $Z (+2,93%) , $NOW (+1,39%) , $SHOP (-4,31%) , $TWLO (+3,59%) , $HUBS (+0,99%) , $DNTH (-5,12%) , $TSHA , $TYRA , $TNGX , $SLB (+1,37%) , $ORIC (-1,64%) , $IONQ (+1,35%) , $QBTS (+0,32%) , $FCX (-1,29%) , $GLEN (+1,66%)

1111

26 Comentários

@Tenbagger2024 Jefferies therefore prefers $FCX 😉. Btw that would also be my favorite copper pick from your idea.

••

9Mês·

The 10 best US dividend stocks

$MRK (+0,04%)

$KO (+0,1%)

$PEP (-0,38%)

$COP (+0,12%)

$MDT (+0,18%)

$MDLZ (-1,1%)

$EOG (+2,14%)

$SLB (+1,37%)

$KMB (-0,02%)

$CL (-0,05%)

What should investors look for when it comes to buying the best dividend stocks for 2025?

At Morningstar, we believe that the best dividend stocks are not simply the stocks with the highest dividends or the stocks with the best dividend yields. We recommend that investors look beyond a stock's yield and short-term performance and instead consider stocks with sustainable dividends and buy them when they are undervalued.

"As tempting as they may be, the most attractive returns on the stock market are often illusory," explains Dan Lefkovitz, strategist at Morningstar Indexes. "High dividend yields are often found in risky sectors, industries and companies." Therefore, such high dividend yields are not always sustainable.

David Harrell, the publisher of Morningstar DividendInvestor, empfiehlt,to focus on companies with management teams that support their dividend strategy and to favor companies with competitive advantages or wirtschaftlichen Burggräben to be preferred.

"An economic moat rating is obviously no guarantee of dividends, but we have found some very strong correlations between economic moats and dividend consistency," says Harrell.

Investors looking for good dividend stocks might consider adding undervalued quality dividend stocks to their portfolio.

10 best US dividend stocks to buy

To find the best U.S. dividend stocks, we turn to the Morningstar Dividend Yield Focus Index. The dividend stocks on this list are among the top stocks in the index and were trading in the 4- and 5-star range as of June 13, 2025.

Merck MRK

Coca-Cola KO

PepsiCo PEP

ConocoPhillips COP

Medtronic MDT

Mondelez Global MDLZ

EOG Resources EOG

SLB SLB

Kimberly-Clark KMB

Colgate-Palmolive CL

Below you will find a brief description of the individual low-cost dividend stocks as well as some important Morningstar key figures. All data is valid until October 10, 2025.

Merck

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: High

- Morningstar Uncertainty Rating: Medium

- Expected dividend yield: 3.77

- Sector: Pharmaceuticals - General

Merck tops our list of best dividend stocks with a share price 23% below our estimated fair value of $111 per share. Merck continues to see weak demand for its HPV vaccine Gardasil in China, which has dampened revenues this year. Nevertheless, we believe Merck shares are undervalued. The company's balance sheet is solid and low risk. We expect stable future dividends, supported by a payout ratio of nearly 50% of adjusted earnings per share, according to Morningstar Director Karen Andersen.

Coca-Cola

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 3.04

- Sector: Beverages - non-alcoholic

Coca-Cola is the first Dividendenaristokrat on our list of this month's best dividend stocks. Dividend aristocrats are companies that have increased their dividends for at least 25 consecutive years. The company's impressive brand portfolio, pricing power and relationships with retailers underpin its high Economic Moat rating, says Morningstar analyst Dan Su. We expect the dividend payment to increase in line with earnings growth over the next ten years, with the dividend payout ratio likely to stabilize above 60%, Su adds. We estimate the value of Coca-Cola shares at USD 72.

PepsiCo

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 3.79

- Sector: Beverages - non-alcoholic

Pepsi is the second Dividend Aristocrat on this month's list of best dividend stocks to buy. We estimate the value of the Pepsi-Aktie at $164 and the shares are trading 8% below this value. Despite short-term headwinds due to consumer austerity, we believe Pepsi continues to be able to strengthen its competitive position in beverages and snacks through marketing and product initiatives, reports Morningstar's Su. Over the next decade, we expect Pepsi's payout ratio to remain in the low 70% range on average and its dividend payment to grow in the mid-single digits annually, Su said.

ConocoPhillips

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: High

- Expected dividend yield: 3.56

- Sector: Oil and Gas E&P

ConocoPhillips is the first energy stock on our list of best dividend stocks and is currently trading 19% below our estimated fair value of $108. Morningstar analyst Adam Baker points out that the company has been making large acquisitions at favorable prices without burdening the balance sheet. ConocoPhillips ties cash returns to cash flow and has committed to returning 30% of operating cash flow to shareholders, keeping dividend growth moderate but committing excess cash to buybacks and a variable dividend each year.

Medtronic

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: Medium

- Expected dividend yield: 2.98

- Sector: Medical devices

Medtronic stock is one of the best dividend stocks and is currently trading 15% below our estimated fair value of $112. The largest pure-play medical device manufacturer is an important partner for its hospital customers thanks to its diversified product portfolio for a variety of chronic conditions, explains Morningstar Senior Equity Analyst Debbie Wang. The company aims to distribute at least 50% of its annual free cash flow to shareholders, but has been in the 60% to 70% range in recent years, Wang said. Medtronic is also a dividend aristocrat.

Mondelez Global

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 3.25%

- Sector: Confectionery manufacturer

Mondelez International is one of the five Unternehmen mit breitem Burggraben on our list of the best dividend stocks to buy. "Mondelez has worked tirelessly to further simplify its operations by streamlining its supplier base, divesting unprofitable brands, and continuing to modernize its manufacturing facilities," argues Morningstar Director Erin Lash. We forecast that the company will increase its dividend on average in the high single digits through fiscal 2034. We estimate the value of this top dividend stock at USD 75, and the shares are trading 18% below this value.

EOG Resources

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: Medium

- Expected dividend yield: 3.78

- Sector: Oil and gas production

EOG Resources returns to our list of the best dividend stocks to buy this month. This top dividend stock is trading 21% below our estimated fair value of USD 137. The company aims to return 70% of free cash flow to shareholders via dividends and share buybacks. "Unlike some peers that buy back shares at top valuations when they have ample cash, EOG also returns cash via special dividends," says Morningstar Director Josh Aguilar. EOG's balance sheet is strong, and the company should have no trouble meeting its fixed and variablen Dividenden cover its fixed and floating rate debt.

SLB

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar Uncertainty Rating: High

- Expected dividend yield: 3.59

- Sector: Oil and gas equipment and services

SLB, the last energy stock on our list of best dividend stocks, is trading 37% below our estimated fair value of $50. SLB is the world's leading oilfield services company by market share and has built a narrow economic moat based on its cost advantages and intangible assets. Morningstar's Aguilar calls the company's distributions "shareholder friendly" and we expect management to continue to return more than half of free cash flow to shareholders in the form of dividends or buybacks.

Kimberly-Clark

- Morningstar rating: 4 stars

- Morningstar Economic Moat Rating: Low

- Morningstar uncertainty rating: Medium

- Expected dividend yield: 4.22%

- Sector: Household and personal care products

Kimberly-Clark is the highest yielding stock on our list of best dividend stocks to invest in and is currently trading 15% below our estimated fair value of $140. The company's portfolio of well-known hygiene and tissue brands, including Huggies, Depend and Kleenex, generates significant excess cash, according to Morningstar's Lash. Lash's long-term outlook calls for mid-single-digit annual dividend growth. Kimberly-Clark is also a dividend aristocrat.

Colgate-Palmolive

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Broad

- Morningstar Uncertainty Rating: Low

- Expected dividend yield: 2.67

- Sector: Household and personal care products

Colgate-Palmolive rounds out our list of best dividend stocks and is also a dividend aristocrat. The Colgate brand's solid intangible assets and cost advantages underpin the company's broad economic moat, says Morningstar's Lash. Over the next 10 years, we expect average annual dividend growth in the high single digits with a payout ratio of 55% to 60%, she adds.

Source

66

4 Comentários

9Mês

The "Dogs of the Dow" used to be called what the dividend yield paid was. Until the dividend was canceled. I've (unfortunately) been through all that.

•

55

•

11Mês·

📈 August 2025 Portfolio Recap – First Month in Review

Introduction

It has now been a little bit over a month since I published my first portfolio review. I started this portfolio on July 23 and will continue to share monthly recaps from now to, hopefully, a very long time. My goal with these updates is simple: transparency. They are to document performance regularly, explain my investment process, and create a track record of decisions that I can learn from and reflect on over time. I will focus on what worked and what did not, while keeping the macro picture and long-term perspective over short-term volatility in mind. As I pointed out in my last review, I strive to become a hedge fund manager, and while there is still a long way to go, and many lessons to be learned, this portfolio will be my primary credential for the future.

Unlike a traditional investor letter, this recap is designed to be professional yet approachable, so it can serve as a portfolio log and as a resource or inspiration for anyone interested in equity investing. Yes, I am doing this primarily because I love investing and diving into company reports and stock market news, but I also want to share my journey and hopefully be able to use my passion in a professional setting. Every month, I will share performance vs. benchmark indices, most suitable to asset allocation, highlights of the strongest and weakest performance, and any changes I have made to my portfolio. This is not about sugarcoating results. Since I genuinely want to improve, there is no point in trying to sweet talk mistakes and slip-ups. Over time, this series should build a narrative of my investing journey, through wins, theses, and most importantly long-term performance and improvement. My daily commentary usually serves as an opinion piece on companies on my watchlist or the most recent macro news, while these monthly recaps are intended to provide a comprehensive guide on my investing principles and execution.

Portfolio Performance

For the month of August, my portfolio delivered a strong +5.25% total return. Not a bad start for month one, but it is always important to remember that short-term gains are not the most meaningful metric. Consistency is key. Nevertheless, to put this month’s return in perspective, here are important benchmarks:

- S&P 500: +3.33%

- Nasdaq 100: +2.42%

- MSCI ACWI: +3.84%

This means the portfolio outperformed both global and U.S. benchmarks in its first full month, which is encouraging.

However, the performance was not linear. The first few days were negative, but as the month progressed, companies reported earnings and news surfaced, several key holdings – particularly those in healthcare and fintech – drove strong upward momentum. This led to an intersection between my portfolio performance and benchmarks around the middle of the month. Since then, the portfolio has outpaced the market’s broader rally.

The outperformance cannot be attributed to one single stock, but rather a combination of multiple holdings reacting strongly. This is exactly how I want my portfolio to behave: diversified enough to avoid cluster risk, but concentrated enough to benefit meaningfully from each of my highest-conviction ideas. It is crucial to strike the balance between diversification and conviction, without sacrificing returns or risk management.

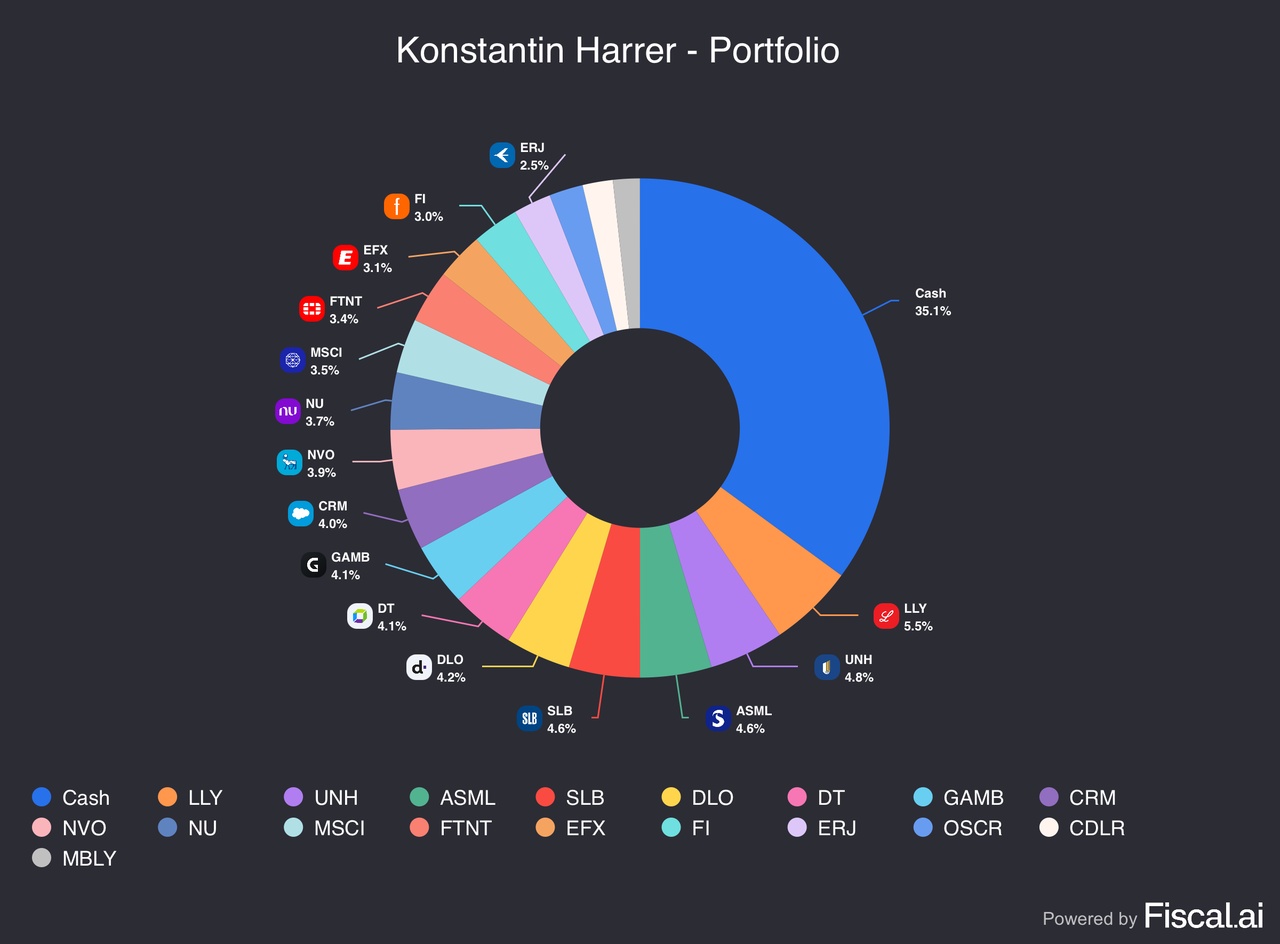

Allocation Snapshot

The portfolio currently consists of 18 equity holdings plus cash, with cash representing the single largest allocation at 35.1%.

This is a short breakdown of my portfolio:

- Cash: 35.1%

- Largest equity holding: Eli Lilly (LLY) at 5.5%

- Other top allocations include: UNH (4.8%), ASML (4.6%), SLB (4.6%), DLocal (4.2%), Dynatrace (4.1%), Gambling.com (4.1%), Salesforce (4.0%), Novo Nordisk (3.9%), and Nu (3.7%).

The high cash balance is intentional. As this is the first month of the portfolio, it is important not to rush into not-well-enough researched positions only to reduce the cash quota. Even for my highest-conviction positions, like LLY or ASML, I want to remain disciplined with entry prices and only buy on pullbacks, after I initiate my first tranche. As I emphasized in my last report, I aim to invest opportunistically in great companies at discounts, and reduce my cash balance to below 10% by the end of the year. In fact, over the course of August I already reduced my cash position from 56% to 35%, by adding to and opening new positions, especially during the first half of the month.

However, I am not in a rush to close my cash holding right now, since I am convinced that this rally off the April lows is highly unsustainable, considering the economic tensions and tariff regime in place. AI hype is driving this rally, and if the enthusiasm cools down, some interesting opportunities could present.

Since I aim for high returns with acceptable risk management, the exposure to fast-growing industries like fintech and software comes naturally. However, I also own more defensive players in the energy and healthcare spaces that, in my opinion, offer a healthy risk/reward ratio not recognized enough by the market. Indeed, some of the companies I hold fall on the more expensive spectrum, but they also boast immense growth and potential for the future. My focus does not lie on momentum or trends, but rather fundamentals and underlying prospects.

Strongest & Weakest Performers

Strongest performers:

- DLocal posted strong earnings in a volatile market environment, which led to a jump in the stock of more than 40% the day after. I remain extremely bullish on the company, with a forward P/E ratio of 23, reflecting a more than fair valuation even after the recent rally. The fintech disruptor is revolutionizing payment solutions across emerging markets, with still a massive TAM left.

- UnitedHealth recovered more than 30% from the lows hit at the beginning of the month, due to improving sentiment and the news of several super-investors, most notably Buffett’s Berkshire Hathaway, opening a position in the healthcare giant. The company has a very healthy balance sheet and a strong moat as the largest health insurer worldwide, and that is not even taking into account all its other ventures.

- Nubank outperformed on strong user growth (over 127 million customers across Latin America) and rising profitability. As the leading neobank in Latin America, Nu delivers >25% annual growth and holds a stellar position. The TAM is hard to overlook, as the neobank operates in one of the most underbanked regions worldwide.

Weakest performers:

- Salesforce slightly recovered from recently hit lows, while still underperforming the broader tech sector due to a perceived lack of AI implementation. However, Salesforce is the largest provider of CRM services worldwide and in a very good position for a recovery if any good news hits. The company has not taken part in the recent rally and could be in for a rebound.

- Gambling.com sold off after solid earnings due to a cautious outlook. Online betting is inherently cyclical, and the current economic situation does not look great. However, Gambling.com is already trading at an extremely cheap valuation. Somehow, the market still finds a way to send the stock further down.

In both cases, I view the weakness as sentiment-driven rather than structural. Investors’ confidence is shattered at the moment. However, my theses on these companies have not changed. I think both of them are misunderstood and victims of short-term focus, rather than the broader picture.

Portfolio Activity

Because this was the first month, most activity was centered around building initial positions. I deliberately capped position sizes at ~3–5% each, which allows me to add more over time if conviction grows or valuations improve.

- New Buys: SLB, FTNT, DT, CDLR

- Adds: CRM, GAMB, LLY, UNH

- Sells: M12

- Cash: Meaningfully reduced from >55% to ~35%

My portfolio is still “under construction.” While I reduced my cash position and invested aggressively, especially after earnings hit, I still hold a significant chunk of my portfolio in cash, which I plan to reduce by the end of the year. When I decide to buy into a company, I always do it in tranches and build a position over time, rather than buying all at once. Take Lilly for example: I opened an initial position in July and then bought multiple times this month after the earnings-related dip, and now I am almost 10% in the green with the position.

Market & Macro Context

Markets in August were shaped mainly by speculation around interest rate cuts and the earnings season, both of which contributed positively to my return. Several of my holdings jumped after stellar earnings, while others fell and therefore created opportunities to add, increasing long-term upside. Economic data was two-edged: while unemployment continued to increase, so did GDP, and tariff impacts were largely absorbed by corporations. My portfolio specifically profited from improving sentiment around some beaten-up healthcare names and increasing momentum for fintech and Latin American stocks. August has also been a good month for many tech investors due to continued growth and AI momentum.

Outlook

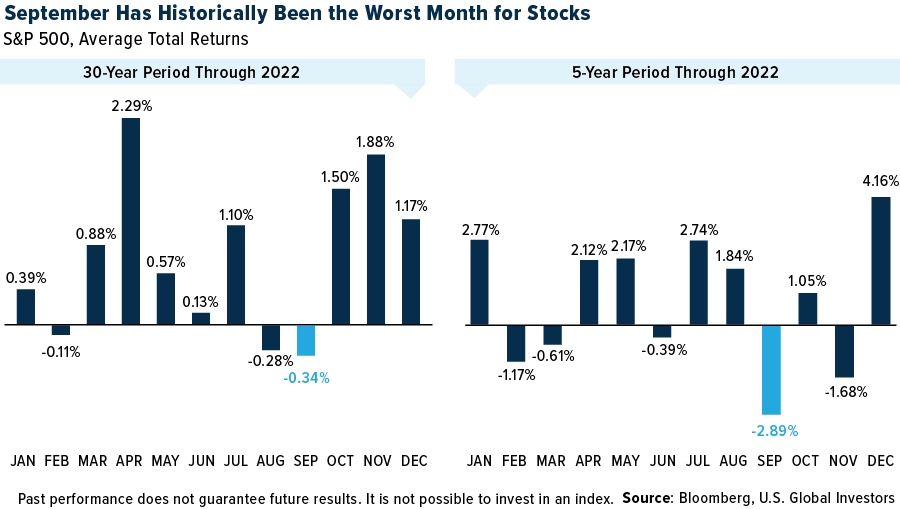

September historically is a very difficult month for markets. These are the key catalysts I will be looking at over the next month:

Jerome Powell has hinted at a possible rate cut at the next meeting, which the market has now priced in. It seems likely, at this point, that interest rates will be falling. However, if the Fed has a sudden change of heart, it could mean a cold awakening for stocks across the board.

On the other hand, if the most likely scenario – a rate cut – comes in, the already started shift from tech stocks to more cyclical industries profiting from lower interest rates could get a boost in September.

Apart from that, I still wholeheartedly believe that the current recovery rally from April lows is highly unsustainable and will eventually cool down, which could create buying opportunities. Whether that will be in September or a later month, I cannot determine. However, it seems strange to have such bullish sentiment ruling the markets, considering the tariff-inflicted strain on the economy. If signs of a cooling cycle thicken, markets could tumble very quickly.

Nevertheless, I am not worried about a broader pullback, since conviction is unwavering for the holdings in my portfolio. If anything, selloffs create possibilities to add to existing holdings or initiate new positions at attractive entry prices.

Closing Thoughts

This first month has been a promising start, with outperformance vs. benchmarks, and multiple adds to my highest-conviction positions. My strategy of investing opportunistically has proven correct so far. However, it has only been one month and I understand that markets fluctuate, which means that patience is key. While it is tempting to deploy cash all at once in order to ride the rally, that is not how I play the game.

In my daily comments I talked about many companies on my watchlist, some of which I will probably never own, because they do not reach my entry prices. That is not important. I have my eyes on countless stocks and continue to research new companies every day. There are always opportunities in the market, and often they are the ones most under fire.

Furthermore, I look forward to continuing this series monthly. Transparency, accountability, and consistency are the main goals. I strive to be the best investor I can possibly be, and this is my log. The target is as clear as ever: beating the market consistently and transforming that experience into the real world.

$ACWU (+0,18%)

$LYPS (+0,25%)

$CSNDX (+1,79%)

$LLY (-0,1%)

$UNH (-0,19%)

$ASML (-0,01%)

$ASML (+0%)

$SLB (+1,37%)

$DT (+0,52%)

$DLO (+1,15%)

$CRM (+1,57%)

$GAMB (+3,51%)

$NOVO B (-8,09%)

$NVO (-7,24%)

$NU (-1,35%)

$NU

$MSCI (-0,02%)

$FTNT (+5%)

$EFX (-2,03%)

$FI (+0,27%)

$ERJ (+1,02%)

$OSCR (-0,81%)

$CDLR (+0%)

$CADLR (+1,44%)

$MBLY

+ 5

19Posições

US$ 155.179,63

4,21%

11Mês·

The investment bank sees these stocks as the big beneficiaries of AI adaptation

$AAPL (-2,89%) Apple, Inc. (ISIN: US0378331005)

$ADBE (+1,12%) Adobe Inc (ISIN: US00724F1012)

$AES (-1,18%) AES Corp (ISIN: US00130H1059)

$AMZN (+6,74%) Amazon.com Inc (ISIN: US0231)

$APP (-2,64%) AppLovin Corp (ISIN: US03831W1080)

$AXON (+0,93%) Axon Enterprise, Inc. (ISIN: US05464C1018)

$BE (-3,13%) Bloom Energy Corp. (ISIN: US09

$CRM (+1,57%) Salesforce.com, Inc. (ISIN: US79466L3024)

$GOOGL (+6,34%) Alphabet Inc (Class A) (ISIN: US02079K3059)

$GTLS Chart Industries, Inc. (ISIN: US16115Q3083)

$HUBS (+0,99%) HubSpot Inc (ISIN: US4435731009)

$JCI (+1,88%) Johnson Controls International plc (ISIN: IE00BY7QL619)

$NEE (-1,08%) NextEra Energy, Inc (ISIN: US65339F1012)

$NVDA (+2,15%) NVIDIA Corp (ISIN: US67066G1040)

$SLB (+1,37%) Schlumberger N.V. (ISIN: AN8068571086)

$SPGI (+0,17%) S&P Global Inc (ISIN: US78409V1044)

$TSLA (+0,25%) Tesla Inc (ISIN: US88160R1

$TT (+3,5%) Trane Technologies PLC (ISIN: IE00BK9ZQ967)

$$VRTX (+0,29%) Vertex Pharmaceuticals Inc (ISIN: US92532F1003)

$VERTEX (+0,26%) Vertex, Inc (ISIN: US92538J1060)

$VST (-0,94%) Vistra Corp (ISIN: US92840M1027)

$WIX (-2,34%) Wix.com Ltd (ISIN: IL0011301780)

Morgan Stanley expects these companies to benefit greatly from the global trend towards AI integration, whether through leading chips such as NVIDIA, cloud and software solutions such as Amazon, Alphabet or Salesforce, or specialized applications in energy, industry and biotechnology. With tech giants expected to invest almost 400 billion US dollars by 2026, demand in many of these segments could explode. But while the list reads impressively, there is still the intriguing question of who will ultimately benefit not only from the hype, but also from the sustainable use of this technology.

Source: Boerse-Online (Morgan Stanley report on AI-related stocks)

Image material: Techa Tungateja/iStockphoto

1Ano·

Iran Israel geopolitical tensions

$OXY (+2,48%)

$OD7F

$OOEA

$XOM (-0,25%)

$BRNT (+2,9%)

$SLB (+1,37%)

$COP (+0,12%)

$WENS (+0,48%)

$EXH1 (+1%)

$SHEL (+1,08%)

$PETR4 (+2,44%)

The tensions will be resolved quickly. High oil prices hurt American consumers. Trump wants to prevent that. He also wants to reach an agreement with China. China imports a lot of oil from Iran, which will hurt them. The same goes for India, with which Trump also wants to reach an agreement.

Trump is pro-Israel and wants to help Israel achieve its military goals. Nevertheless, he won’t give Israel much time to do so. It will be over either as quickly as the Six-Day War or within two weeks at the latest, forced by Trump.

22

12 Comentários

And we have seen what influence DT has on conflict resolution! Russia/Ukraine, Israel's genocide in Palestine, etc. If you find irony, you can keep it!

•

33

•Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet