I actually wanted to expand that position further.

But from time to time, I just didn't like it anymore.

What do you think of the industry?

Posts

70Text gone again. Thanks GQ. In the meantime I always copy it and then paste it into the edit. Get a grip on that!!! 😡

I had bought TKA before the split with $TKMS to get them allocated. Unfortunately, the allocation was too late for my broker ING to sell at a significant profit immediately after the IPO. Nevertheless, I sold them at the time and kept Thyssen in the hope that the share price would recover. It did, but I wanted more. So I have now sold slightly after the rally. Overall, TKMS is up, but still not the greatest investment.

A quarter of the profits went into $DTE (-2.4%) which I currently see as cheap. Another quarter in $TDIV (-0.53%) and a quarter in $BTC (-0.56%) . The rest remains in cash for the time being.

After 20 minutes the video quality improves. Adobe Studio has apparently failed.

YouTube

https://openyoutu.be/rbWcp0BNRK4

Spotify

https://open.spotify.com/episode/6bgZMA0uhfaIkUUcXeP8ed?si=x6H_k9L_Qb2pVzXgMGxuZg

Apple Podcast

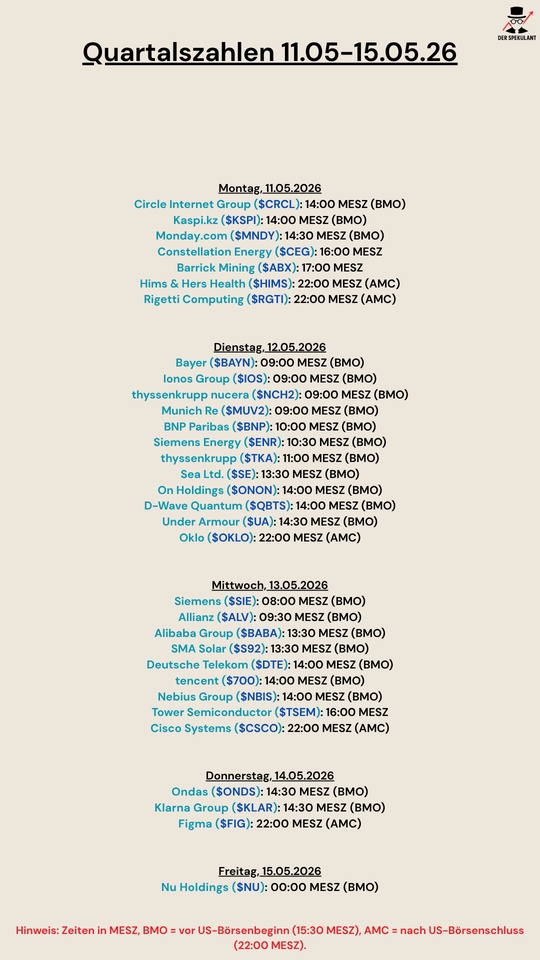

$NVDA (+2.4%)

$HIMS (+0.83%)

$DUOL

$BAS (-0.04%)

$TKA (-0.28%)

$TTWO (-1.67%)

$CRCL (-3.52%)

$KSPI (+1%)

$MNDY (-1.48%)

$CEG (-2.21%)

$ABX (+6.38%)

$HIMS (+0.83%)

$RGTI (-1.93%)

$BAYN (+4.03%)

$NCH2 (-1.17%)

$IOS (-0.41%)

$MUV2 (+0.91%)

$BNP (-0.46%)

$ENR (-1.68%)

$TKA (-0.28%)

$SE (+2.08%)

$ONON (+2.1%)

$QBTS (-1.12%)

$UA (-0.6%)

$OKLO

$SIE (-0.98%)

$ALV (+0.66%)

$BABA (+0.45%)

$S92 (-4.37%)

$DTE (-2.4%)

$700 (-1.1%)

$NBIS (-0.9%)

$CSCO (-3.57%)

$ONDS (+2.2%)

$KLAR (-0.34%)

$FIG (+2.04%)

$NU (-0.04%)

Transportation

Utilities

Social affairs

Digital

Future needs until 2040

Private Markets Infrastructure

Modernization

Infrastructure programs

Link: https://shorturl.at/maYS2

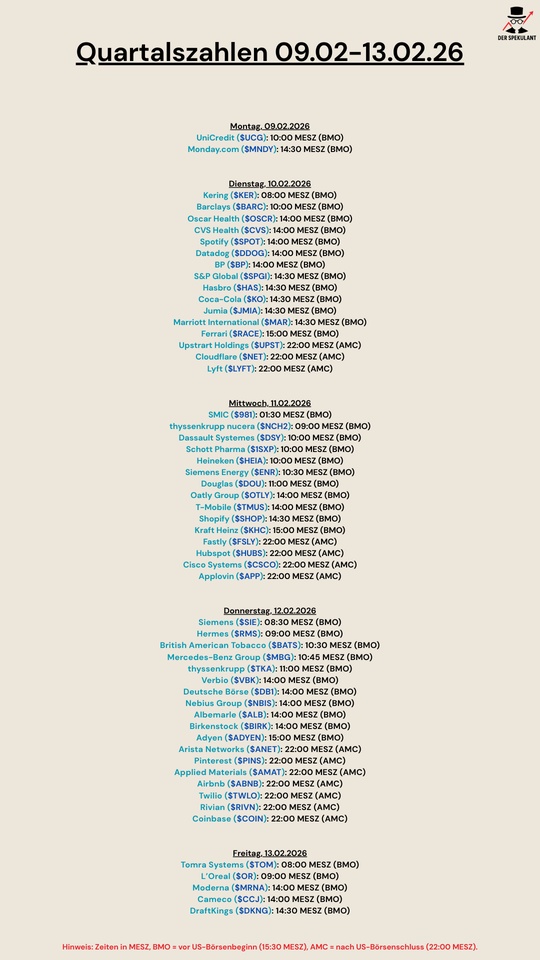

$IFX (-7.59%)

$NDA (+1.96%)

$ENR (-1.68%)

$SIE (-0.98%)

$DEZ (-1.85%)

$TKA (-0.28%)

$CBK (-0.7%)

$NKT (+1.37%)

$DHL (-3.83%)

$NEM (-1.55%)

$BZU (+0.98%)

$DBK (+0.63%)

$SPIE (+0.49%)

$ELI (+1.47%)

$GBF (-0.15%)

Subscribe to the podcast so that there will soon be peace.

00:00:00 Oil and government bonds

00:37:50 Liberty Energy $LBYE

00:48:30 Cheniere Energy $LNG (-1.46%)

00:56:35 Kinder Morgan $KMI (-1.07%)

01:00:52 Iran war losers / Buy The Dip

01:19:20 Bitcoin

Spotify

https://open.spotify.com/episode/7jouQHLiEbfg5QGyZOdZWJ?si=Du2whTFIR7WOE8AFD1RICA

YouTube

Apple Podcast

$TKA (-0.28%)

$SZG (-0.23%)

$SZGPY (-0.45%)

$HLAG (-2.7%)

$VNA (-2.77%)

$CCL

$AAL (+2.28%)

$SMSD (-1.6%)

$005930

$CONTININS

$TUI1 (+0.74%)

$IFX (-7.59%)

$MC (-1.61%)

$BA (-0.3%)

$2330

$CCO (+1.56%)

DZ Bank has raised the fair value for Thyssenkrupp shares from 10 to 11 euros and left the rating at "hold". Thyssenkrupp opened the fiscal year 2025/26 with a mixed picture in the first quarter, Dirk Schlamp wrote on Friday. Adjusted operating earnings (EBIT) were slightly above consensus. Operationally, this showed a stabilization at a level that remains subdued due to the economic situation.

I am selling you due to:

In the first quarter, ThyssenKrupp increased adjusted EBIT by 10 percent to 211 million euros. This shows an operational stabilization. However, the weak point of the figures is the free cash flow before M&A. This fell from -21 million euros to -1.5 billion euros.

The coming quarters must therefore be much better. ThyssenKrupp expects a free cash flow of -300 million euros to -600 million euros for the year as a whole. Adjusted EBIT is expected to be between 500 million euros and 900 million euros.

My trend is out of the low performers with canceled dividends.

Into boring ETFs

$UCG (-1.3%)

$MNDY (-1.48%)

$KER (+0.37%)

$BARC (+2.36%)

$OSCR (+0.72%)

$CVS (-7.19%)

$SPOT (+2.92%)

$DDOG (-1.38%)

$BP. (-2.39%)

$SPGI (-0.31%)

$HAS (-0.33%)

$KO (-0.17%)

$JMIA (-2.06%)

$MAR (+3.1%)

$RACE (+0.63%)

$UPST (-6.99%)

$NET (-1.42%)

$LYFT (-1.03%)

$981

$NCH2 (-1.17%)

$DSY (+0.63%)

$1SXP (-2.95%)

$HEIA (+2.27%)

$ENR (-1.68%)

$DOU (-0.43%)

$OTLY (-3.31%)

$TMUS (-3.75%)

$SHOP (+15.9%)

$KHC (-3.61%)

$FSLY (+4.62%)

$HUBS (+0.47%)

$CSCO (-3.57%)

$APP (+1.37%)

$SIE (-0.98%)

$RMS (-1.5%)

$BATS (-0.74%)

$MBG (-1.22%)

$TKA (-0.28%)

$VBK (-2.35%)

$DB1 (+1.42%)

$NBIS (-0.9%)

$ALB (-0.55%)

$BIRK (+1.84%)

$ADYEN (-0.02%)

$ANET (-8.06%)

$PINS (-2.75%)

$AMAT (-2%)

$ABNB (-0.47%)

$TWLO (+0.21%)

$RIVN (-2.04%)

$COIN (-0.14%)

$TOM (+1.55%)

$OR (+0.4%)

$MRNA (+0.48%)

$CCO (+1.56%)

$DKNG (-4.03%)

Reading time: approx. 5-6 minutes

Many of my recent posts have focused on metrics that have been with investors for decades: EV/EBITDA, free cash flow yield, ROIC, margins. The price-to-book ratio also belongs in this category - but more as a historical relic than as a central management tool. Hardly any other key figure shows so clearly how far capital markets and business models have diverged.

The P/B ratio compares the stock market value of a company with its balance sheet equity. The logic behind this is simple: what do I pay on the market for what is "there" according to the balance sheet? In a world of factories, machines and warehouses, this was plausible for a long time. In a world of software, platforms, brands and data, it is becoming increasingly misleading.

Formally, the calculation is quickly explained. Price times number of shares equals market capitalization. This is set in relation to the equity from the balance sheet. A P/B ratio of 1 means that the market values the company exactly at its balance sheet book value. Below 1 was traditionally regarded as "intrinsic value", above 1 as a premium.

This is exactly where the problem begins: the book value is not an economic value, but an accounting residual item. It results from historical acquisition costs less depreciation - not from a company's ability to generate future cash flows. The more intangible, scalable and knowledge-based business models are, the less this residual item says about the economic reality.

This worked comparatively well in the industrial economy. Steelworks, energy suppliers, banks and insurance companies had large, clearly measurable assets. Machinery, real estate, loan portfolios - they all appeared on the balance sheet. Those who bought below book value were often actually buying substance with a margin of safety. Benjamin Graham and early value investors built entire strategies on this.

Today, this logic is only viable in niches. A modern software company invests massively in research, development, employees and marketing. As a rule, these expenses are immediately booked as costs. Equity capital barely shrinks or grows, even though enormous economic value is created: proprietary software, network effects, customer data, brand trust. The result is an extremely low book value - and therefore an astronomically high P/B ratio. Not because the company is "expensive", but because the denominator is structurally distorted.

A look at $MSFT (-1.06%) (Microsoft) makes this devaluation particularly tangible. Despite decades of profitability, enormous free cash flows and very high returns on capital, equity is comparatively low in relation to market capitalization. Research, software development and cloud infrastructure largely appear as expenses in the income statement. The economic value arises off the balance sheet. The double-digit P/B ratio is therefore not a warning signal, but an accounting artifact.

A similar picture can be seen at $V (-0.64%) (Visa). The company operates a global payment network, requires hardly any physical capital and still achieves exceptionally stable margins. At the same time, continuous share buybacks reduce equity, although they increase the shareholders' stake in the company. The P/B ratio rises - although neither the competitive position nor the cash flow stability deteriorate. Anyone focusing on the book value here is completely missing the point of the business model.

Conversely, a high book value can be misleading. A classic industrial group such as $TKA (-0.28%) (Thyssenkrupp) has large property, plant and equipment, long depreciation cycles and therefore a high balance sheet equity. At times, this results in very low P/B ratios, which appear favorable at first glance. In practice, however, they often reflect structural challenges: cyclical demand, low returns on capital and limited pricing power. The book value is there - the economic quality often is not.

At $GOOGL (-0.18%) (Alphabet), the discrepancy between book value and economic value is clear. Despite enormous cash flows, high ROIC values and one of the strongest brands in the world, equity is only growing moderately. Data, algorithms and network effects form the core of value creation, but hardly appear on the balance sheet. A P/B ratio comparison with traditional media or industrial companies is therefore meaningless.

Banks such as $DBK (+0.63%) (Deutsche Bank). Here, equity is central for regulatory purposes, the assets consist mainly of financial items and value adjustments have a direct impact on profitability. A P/B ratio below 1 can actually indicate undervaluation - or doubts about the quality of the assets. In this segment, the P/B ratio is not obsolete, but highly context-dependent. Without a deep understanding of the balance sheet risks, the multiple alone remains inadequate here too.

All these examples lead back to the core message: the P/B ratio does not measure value creation, but capital commitment. This is precisely why it has lost its explanatory power in the digital economy. It is backward-looking, while markets price in expectations about future cash flows, growth and risks.

This effect has become particularly apparent in recent years. Companies with high returns on capital and scalable models received valuation premiums - regardless of their book value. With rising interest rates, the focus shifted more towards profitability and cash flow quality, but not back to the book value. The benchmark changed, the P/B ratio remained marginal.

Does this mean that the P/B ratio is worthless? No. But its field of application is narrow. It can be useful for banks, insurance companies or genuine asset-heavy turnaround cases where substance can actually be liquidated. It is unsuitable for platforms, software and data-driven business models and is not suitable as the sole selling point.

Modern analyses therefore focus on something else: returns on capital such as ROIC, free cash flow yield, margin stability and growth. These key figures measure how efficiently capital is deployed - not how much of it is historically tied up.

This also closes the meta-circle of this series. Many traditional balance sheet ratios date back to a time when value creation was physical, linear and capital-intensive. Today, value is increasingly created through knowledge, software, networks and scaling. These values defy traditional balance sheet logic.

As a result, book value is not only becoming less important - it often tells the wrong story. Those who use it uncritically run the risk of confusing substance with quality or growth with overvaluation.

The decisive thought at the end: good investors do not ask what is on the balance sheet, but what a company will earn in the future - and at what risk. The KBV looks back. The market looks forward. That is precisely why it hardly counts any more.

In the end, the question is less about the "right" key figure and more about the right analysis tool. Which key figures do you primarily use today to classify the quality and valuation of a company? Where do traditional balance sheet figures still provide you with real added value - and where do you consciously turn to cash flow, return or growth figures? And more specifically: which key figures or correlations would you like to see more in-depth coverage of in the series?

Thyssenkrupp expects a high loss of EUR 400-800 million for the financial year 2025/26, caused by extensive provisions for the restructuring of the steel division. The market environment remains difficult; adjusted EBIT is only expected to reach EUR 500-900 million, which is at the lower end of the forecast range.

At the same time, the Group expects a decline in sales. The focus is also on new statements on the ongoing takeover talks with Jindal Steel regarding the steel division. The share reacted significantly weaker.

Top creators this week