$PLTR (+1.92%)

$SNAP (+2.14%)

$HSBA (+0.46%)

$9434 (+1.44%)

$ZAL (+1.28%)

$BOSS (-0.34%)

$BNTX (+0.16%)

$SPOT (+0.23%)

$BP. (-2.79%)

$BAYN (-1.63%)

$DOCN (-0.12%)

$MCD (+1.18%)

$CAT (+1.82%)

$PFE (+0.78%)

$ANET (+1.51%)

$PINS (+1.45%)

$SPCX (+0.66%)

$AMD (+1.53%)

$PARA (+1.03%)

$LUMN (+0.18%)

$KTOS (+1.23%)

$CPNG (+0.76%)

$IFX (+0.17%)

$ENR (-0.5%)

$DHL (+0.21%)

$NOVO B (+0.18%)

$CVS (-0.16%)

$UBER (+0.61%)

$SEDG (+1.05%)

$WULF (+2.7%)

$CRCL (+0.23%)

$SHOP (+0.63%)

$DIS (+0.8%)

$HUBS (+1.47%)

$DASH (+0.69%)

$FSLY (+0.95%)

$SNDK (+3.35%)

$MELI (+0.48%)

$DUOL

$APP (+1.45%)

$SMR

$FIG (+0.71%)

$SIE (+0.94%)

$CBK (+0.82%)

$IOS (-0.51%)

$FI (+0.43%)

$DDOG (+1.29%)

$RHM (+0.4%)

$QBTS (+2.48%)

$G24 (-0.13%)

$AKAM (+0.57%)

$MUV2 (-0.19%)

$UA (+1.65%)

$OKLO

Bayer

Stock

Stock

ISIN: DE000BAY0017

Ticker: BAYN

DE000BAY0017

BAYN

Price

Discussion about BAYN

Posts

26322H·

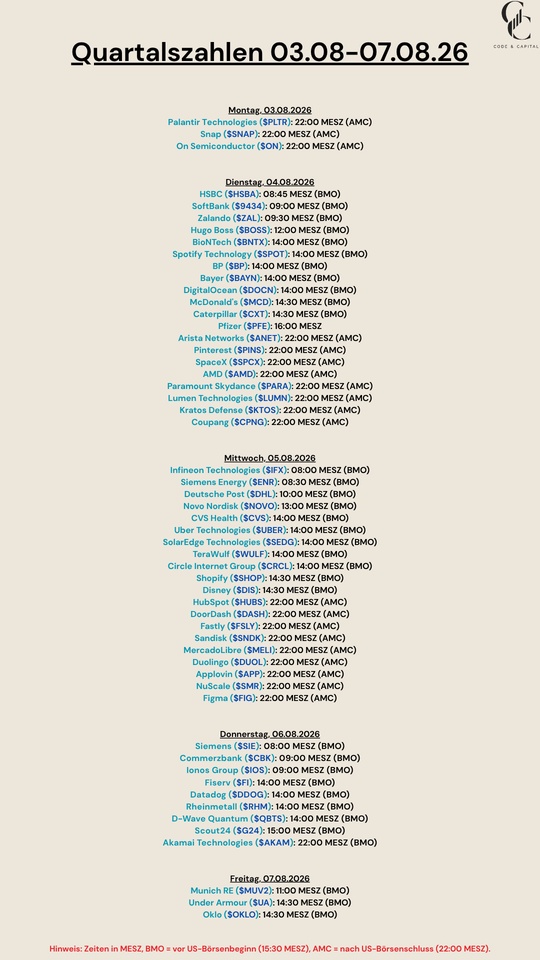

Quarterly Results August 3–7, 2026

1010

4Wk·

Top News Stories from the Past Week

Monday:

Because of the new competitor $SPCX (+0.66%) SpaceX, $DTE (+1.82%) Deutsche Telekom is apparently planning a merger with Telekom US. The new holding company could be headquartered in Ireland or Switzerland, similar to what we’ve already seen with Linde. A move that seems somewhat absurd, considering that we’re talking about Deutsche Telekom. In any case, the plans aren’t going over well on the stock market—or rather, the assessment that competition from SpaceX will be so fierce.

Tuesday:

Partly due to the fuel rebate, which is set to expire on Wednesday, inflation in Germany stood at just 2.3%. This puts it only slightly above the ECB’s 2.0% inflation target.

Nike exceeded expectations for quarterly revenue and posted higher quarterly earnings. This was due, in part, to $NKE (-0.85%) Nike is receiving refunds for overpaid customs duties.

Wednesday:

It was revealed that Donald Trump earned more than $1 billion from crypto projects alone during his first year in office. These included meme coins that have lost significant value. Trump’s earnings have also multiplied compared to 2024.

https://www.bbc.com/news/articles/cvgmv98ez3zo

Thursday:

$BAYN (-1.63%) Bayer is taking the next step to finally distance itself from the glyphosate lawsuits. Glyphosate is being spun off into the new business unit Ruveon.

www.wiwo.deSpekulation um Fusion: Arbeiten Telekom und T-Mobile an einem geheimen Mega-Projekt?

22

1Mon·

Bayer

$BAYN (-1.63%) - Bayer has seen its stock price rise by nearly 100% over the past year. Much of this is due to the court rulings on glyphosate in the U.S.

For me, that means I’m now only down about 38%. 😅 💥💥I think I’ll crack open half a beer tonight to celebrate.

1919

12 CommentsJohannes@Johannes12345

1Mon

•

22

•1Mon·

Top News Stories from the Past Week

As we do every Sunday, here are the top news stories from the past week:

Monday:

Elon Musk may have raked in billions from SpaceX’s $SPCX (+0.66%) SpaceX, but apparently the money isn’t enough for his AI ambitions, so he’s launching a $20 billion bond program. This isn’t going over well with SpaceX investors. The bonds are expected to yield about 5–6% interest.

Tuesday:

DB has once again outdone itself and hit an all-time low. For hours overnight, no trains ran in Germany. Other former state-owned corporations, such as $DHLGY (+0%) Deutsche Post (DHL) or $DTE (+1.82%) Deutsche Telekom, do not face comparable problems. Perhaps we should consider further privatization of DB or follow the Swiss model (where local municipalities also have a say at the regional level).

https://www.tagesschau.de/wirtschaft/unternehmen/deutsche-bahn-stoerung-zugfunk-100.html

Wednesday:

$ADS (+3.24%) Adidas is reportedly selling three times as many DFB jerseys as it did in Qatar in 2022. This may be partly because people can now actually wear the DFB jersey. The switch to $NKE (-0.85%) Nike could also be a factor.

$VOW3 (+1.99%) Volkswagen is selling a majority stake in Everllance to Bain, reaping billions in the process. Everllance has so far been carried on the balance sheet at a value significantly below its market value, which is likely to result in an extraordinary profit of several billion.

Thursday:

$BAYN (-1.63%) Bayer appears to have pulled off a major victory. The agricultural and pharmaceutical company won its case before the U.S. Supreme Court. The court ruled that regulations set by federal agencies take precedence over state laws. As a result, thousands of lawsuits alleging insufficient cancer warnings have lost their legal basis.

www.manager-magazin.deSpaceX: Raumfahrtfirma plant Anleiheemission über 20 Milliarden Dollar

77

1Mon·

Bayer Moon

The U.S. Supreme Court has ruled in favor of Bayer in lawsuits over cancer warnings related to Roundup. The ruling significantly reduces the legal risks for the German pharmaceutical and chemical company. $BAYN (-1.63%)

2Mon·

Most important news of the past week

As every week before the start of the new week, the most important news from the past week.

Tuesday:

Bayer surprises with its agricultural division of all things. The company is still struggling with legal disputes. In the first quarter, the profit of $BAYN (-1.63%) Bayer doubled to 2.76 billion euros. Also because the pharmaceuticals business performed better than analysts had expected.

$G24 (-0.13%) Scout24 raises its growth forecast and dispels AI concerns. The EBITDA margin is set to rise to 64% by 2028. Revenue is expected to grow at a double-digit rate by then.

Wednesday:

$EOAN (+0.76%) Eon presents good figures for the first quarter. Consolidated net profit climbed significantly by 7% to 1.3 billion euros. Eon also invested 1.4 billion euros. Eon is the largest provider of energy networks in Europe.

$EKT (-0.73%) Energiekontor started the year as planned. The Group's own portfolio has increased to around 450 megawatts. Projects with a capacity of 650 megawatts are under construction and construction is proceeding according to plan.

https://www.ecoreporter.de/artikel/energiekontor-liegt-im-plan-aktie-gewinnt-57/

Due to a record order from Ukraine, SFC Energy $F3C (+0.57%) SFC Energy is raising its forecast. Sales are expected to rise to between 163 and 175 million euros. The major order from the Ukraine alone brings in 42.7 million euros; highly mobile fuel cells will be sold.

Thursday:

Cisco raises its forecast significantly, the share price gains substantially. For the full year, Cisco now expects sales of USD 62.8 - 63 billion. In the last quarter, profits rose by almost a third to USD 3.4 billion.

Friday:

Kevin Warsh takes over as Chairman of the Fed this Friday. Many are curious to see what central bank policy will look like under the new chairman. Trump, at least, would like to see interest rates cut. In the past, Warsh was better known for his position on reducing the Fed's balance sheet.

https://www.zeit.de/2026/22/kevin-warsh-federal-reserve-notenbank-donald-trump/seite-3

33

2Mon·

𝐁𝐚𝐲𝐞𝐫: 𝐄𝐁𝐈𝐓𝐃𝐀 𝐬𝐭𝐞𝐢𝐠𝐭, 𝐂𝐫𝐨𝐩 𝐒𝐜𝐢𝐞𝐧𝐜𝐞 𝐬𝐭𝐚𝐫𝐤, 𝐀𝐮𝐬𝐛𝐥𝐢𝐜𝐤 𝐛𝐞𝐬𝐭ä𝐭𝐢𝐠𝐭

📊 𝐄𝐫𝐠𝐞𝐛𝐧𝐢𝐬𝐬𝐞

- Turnover: €13.41B (previous year €13.74B)

- EBITDA before special items: €4.45B (previous year: €4.09B)

- EBITDA margin before special items: 33.2% (previous year: 29.7%)

- EBIT: €3.53B (previous year €2.32B)

- Net profit: €2.76B (previous year €1.30B)

- Core EPS: €2.71 (previous year €2.40)

- Free cash flow: -€2.32B (previous year: -€1.53B)

- Net financial debt: €32.5B

⠀

🎯 𝐏𝐫𝐨𝐠𝐧𝐨𝐬𝐞

- Currency-adjusted Group outlook for 2026 confirmed

- Free cash flow 2026 adjusted for legal settlement payments: €2.0-3.0B expected

⠀

📌 𝐖𝐢𝐜𝐡𝐭𝐢𝐠𝐬𝐭𝐞 𝐏𝐮𝐧𝐤𝐭𝐞𝐭𝐞

- Crop Science drives earnings growth through Soybean Seed & Traits and Corn Seed & Traits

- EBITDA before special items increases by 9% despite negative currency effects

- Core EPS increases significantly by 13

- Net profit more than doubled due to higher operating results and special effects

- Free cash flow strongly negative due to payments for legal disputes

- Pharmaceuticals with stable sales but weaker EBITDA

- Consumer Health continues to grow adjusted for currency and portfolio effects

- Net financial debt below previous year's level, but higher than at the end of 2025

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭-𝐀𝐮𝐬𝐬𝐜𝐚𝐠𝐞

"We confirm our currency-adjusted Group outlook for 2026."

99

2Mon·

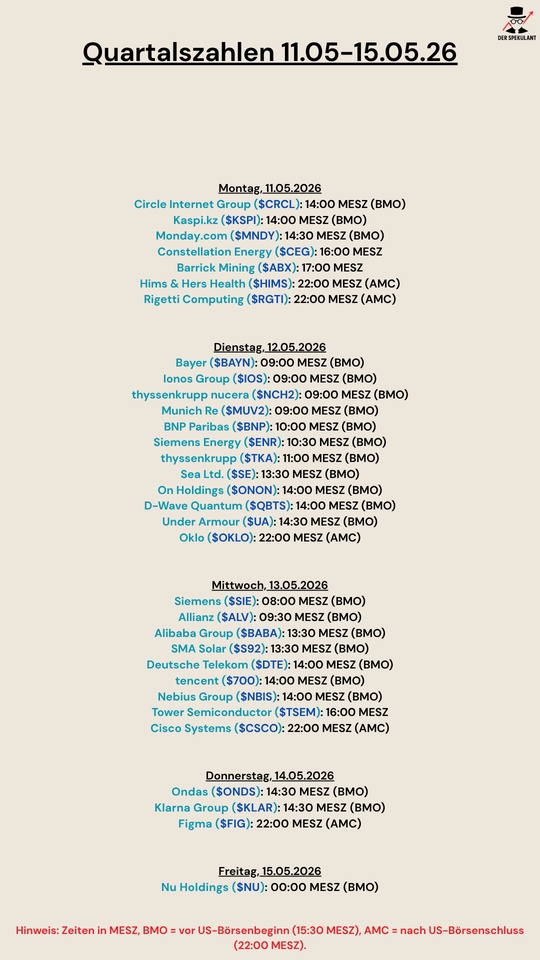

Quarterly figures 11.05-15.05.26

$CRCL (+0.23%)

$KSPI (+1.17%)

$MNDY (+0.33%)

$CEG (+0.83%)

$ABX (+1.02%)

$HIMS (+1.79%)

$RGTI (+2.22%)

$BAYN (-1.63%)

$NCH2 (+0.56%)

$IOS (-0.51%)

$MUV2 (-0.19%)

$BNP (+1.27%)

$ENR (-0.5%)

$TKA (+1.37%)

$SE (+1.3%)

$ONON (-0.55%)

$QBTS (+2.48%)

$UA (+1.65%)

$OKLO

$SIE (+0.94%)

$ALV (+0.17%)

$BABA (+4.43%)

$S92 (-3.81%)

$DTE (+1.82%)

$700 (+2.51%)

$NBIS (+3.07%)

$CSCO (+0.3%)

$ONDS (+1.62%)

$KLAR (+1.29%)

$FIG (+0.71%)

$NU (+0.89%)

3Mon·

Strong dividend season ahead💶

15 increases

13 unchanged

7 reductions

Insurance companies

Banks

Utilities

Car stocks

Type here if you like collecting dividends: https://shorturl.at/83W8R

$MBG (+2.52%)

$ALV (+0.17%)

$VOW3 (+1.99%)

$MUV2 (-0.19%)

$BMW (+1.8%)

$AIR (+2.8%)

$CBK (+0.82%)

$523232

$DTG (+1.1%)

$DHL (+0.21%)

$FME (+0.21%)

$FRE (-0.12%)

$HNR1 (-0.4%)

$MTX (+1.9%)

$RHM (+0.4%)

$SAP (+2.77%)

$ENR (-0.5%)

$BAS (-0.2%)

$BAYN (-1.63%)

$BEI (+0.95%)

$DBK (+0.46%)

$DTE (+1.82%)

$EOAN (+0.76%)

$GEA (-3.55%)

$IFX (+0.17%)

$RWE (-1.27%)

$SY1 (-0.53%)

$ZAL (+1.28%)

$ADS (+3.24%)

$BNR (+0.42%)

$HEN (+0.56%)

$MRK (+0.38%)

$SIE (+0.94%)

$SHL (+3.59%)

Trending Securities

Top creators this week

Real-time data from LSX · Fundamentals & EOD data from FactSet