Hi there, community! 🚀

While many investors are desperately searching for the next hot stock, we’ve unearthed a Swedish powerhouse for the defensive A-side of our portfolio.

Imagine a stock that’s basically like a hand-picked Scandinavian quality ETF , has outperformed the market for over 100 years, is led by Northern Europe’s most powerful financial dynasty, and has outperformed even Warren Buffett’s Berkshire Hathaway and the S&P 500 over the past 5 years.

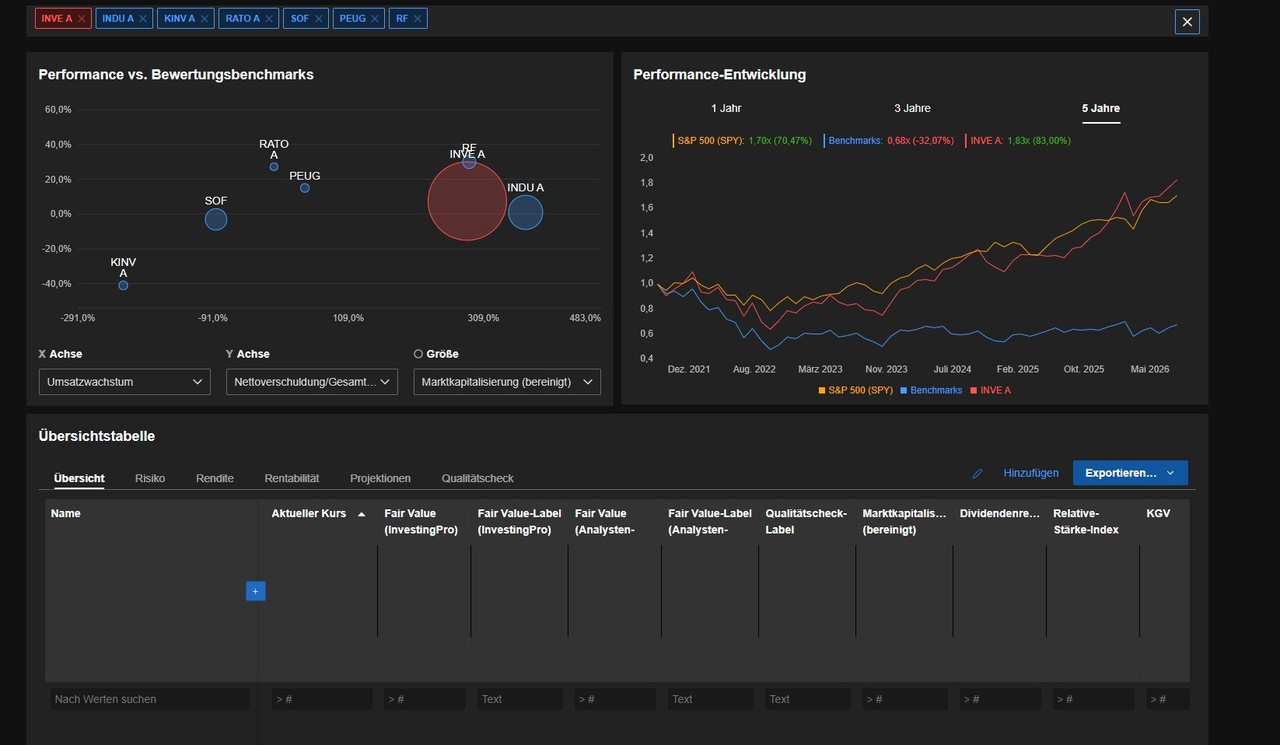

Since the chart for GQ is distorted by the stock split, you’ll find a chart below comparing it to the S&P 500 and others.

That’s exactly what Investor AB $INVE A (+1%)

.

The stock $INVE B (+0.13%) is exactly the same, except that the voting rights here are 1:10.

Let’s fire up the engine room and lay this Scandinavian money-printing machine on the dissection table, following our 15-point template exactly:

Investor AB ISIN: SE0015811955 ~€38.21 / 440.00 SEK

1. What the company does & how it came to be

The origins: Investor AB was founded as early as 1916 by the legendary Swedish industrialist family Wallenberg as far back as 1916. The family’s philosophy has been the same for generations: “Esse non videri” (To be, not to seem). The Wallenbergs have shaped the Scandinavian economy for over a century.

The Business Model – The Ultimate Scandinavian Compounder:

Investor AB is an investment holding company that allocates its capital across three highly profitable pillars:

- Listed Core Holdings: The backbone consists of majority or anchor stakes in global market leaders. These include industrial giants such as $ATCO A (-0.62%)

Atlas Copco (compressed air & vacuum technology), $ABBN (-0.11%)

ABB (robotics & energy), $AZN (+0.38%)

AstraZeneca (Pharmaceuticals), $SEB

SEB (Skandinaviska Enskilda Banken), $EPI A (-0.35%)

Epiroc (mining equipment), $SOBI (+2.66%)

Sobi (biotech), Nasdaq Inc., Wärtsilä, Electrolux and Husqvarna.

- Unlisted companies (Patricia Industries): Wholly-owned subsidiaries in the medical technology and healthcare sector (e.g., Mölnlycke Health Care, Permobil, Laborie). These cash cows are fully consolidated into Investor AB’s balance sheet and generate steady profits.

- Financial investments (EQT): Investor AB is the largest anchor investor and co-founder of the global private equity giant EQT AB. Here, the company benefits directly from the lucrative buyout and infrastructure business.

2. Current Key Figures & Facts

- Market Capitalization: approx. 116.5 billion EUR / ~1,300 billion SEK

- Current share price:

38.21 EUR (52-week range: €25.67 – €38.26) - Revenue (LTM): approx. 29.63 billion EUR

- Net income (LTM): approx. 23.71 billion EUR

- P/E Ratio: 4.9x

(Extremely cheap for a quality compounder) - P/B Ratio:

1.2x

(Close to net asset value) - Return on Equity (ROCE):

27.3% - Net Debt/Total Capital: A meager 7.5%

(Rock-solid balance sheet)

3. Core Quality Formula (Revenue Growth + Margin)

Our target score for solid investments is > 25.

- Revenue CAGR (5 years):

20.1% p.a. (current LTM revenue growth, driven by consolidation, is as high as 285.1%) - Operating EBIT Margin: Massive 82.1%

- Score = Revenue CAGR 20.1% + EBIT margin 82.1% = 102.2 points

- Conclusion:

Phenomenal! A quality score of 102.2 points completely blows our scale out of the water. Since private equity firms have virtually no physical cost of goods sold, nearly the entire gross profit remains as EBIT.

4. Cash Flow Quality Formula

- Free Cash Flow (FCF) Yield:

1.6% - Conclusion: For a holding company, the FCF yield is naturally lower, as profits are directly reinvested to increase the net asset value (NAV) of the portfolio companies. This reinvestment yields a return on equity of over 27%!

5. Dividend Filter (Income-Core)

- Dividend Yield:

1.35% (~€0.4985 per share) - Payout Ratio:

6.36% (Extremely conservative, maximum leeway) - Dividend growth (5 years):

10.1% p.a. - Growth streak: Increased for 6 consecutive years.

- Filter Exception: Although this appears to fall below our 3.5% minimum threshold, our quality exception: The dividend is growing at a double-digit rate, the balance sheet is extremely strong, and net asset growth is easily outpacing the overall market.

- 🇸🇪 Tax Note for Sweden: Sweden levies a 30% withholding tax. Under the double taxation treaty (e.g., with Germany or Denmark), 15% is directly credited, so there are no tax disadvantages.

6. Exclusion Rule Check

Does any of our exclusion rules apply? Not at all!

- The EBIT margin is > 80%.

- No debt problems (net debt at a meager 7.5%).

- A genuine value investment rather than a stock based on an empty narrative.

7. Future and Industry Outlook

The mix of automation (Atlas Copco, ABB), healthcare (AstraZeneca, Mölnlycke), digitalization (Nasdaq, EQT), and mining (Epiroc) addresses the most important megatrends of the coming decades.

Through the Wallenbergs’ active management, $INVE A (+1%) , underperforming holdings are consistently restructured and investments in future-oriented sectors are increased.

8. Competition

Compared to other Scandinavian holding companies (such as Latour, Kinnevik, or Indutrade) and global holding companies, its visual superiority is evident:

- 5-Year Performance: Over the past 5 years, Investor AB has achieved a total return of +83.00% —while the S&P 500 (SPY) returned +70.47% and other European benchmarks stood at -32.07% !

9. Analyst Forecasts & Fair Value

- Fair Value Model (InvestingPro):

42.22 EUR - Upside Potential:

+10.5% from the current all-time high - Quality Check Rating:

4 out of 5 (Very good)

10. Chart Analysis of Recent Months

- Trend: A solid, crystal-clear upward trend from the lower left to the upper right.

- 52-week range: €25.67 to €38.26 (currently at an all-time high).

- Distance from moving averages:

- Current price +7.2% above the 50-day moving average.

- Price is trading +18.4% above the 200-day moving average.

- Volatility: Extremely low volatility.

11. Bargain Hunter List (Entry Zones)

Since the stock is currently trading near its 52-week high, the following zones are suitable for phased purchases:

Zone 1 (Direct Purchase / First Tranche):

- Price range: €37.50 – €38.50 (approx. 430 – 445 SEK)

- Strategy: Current level for starting a savings plan or investing the first tranche.

Zone 2 (First Dip / EMA 50 Support):

- Price range: €34.00 – €35.50 (approx. 390 – 410 SEK)

- Strategy: Healthy consolidation around the 50-day moving average. This presents an ideal buying zone for adding to your position.

Zone 3 (Bargain Hunter / EMA 200 Support):

- Price Range: €30.00 – €32.00 (approx. 345 – 365 SEK)

- Strategy: Strong long-term support around the 200-day moving average. An absolute bargain zone to significantly increase your position.

12. Future Viability

With over 100 years of success, deep roots in Scandinavian industry, and access to exclusive private equity deals through EQT, Investor AB is one of Europe’s most future-proof companies.

13. Potential Alternatives

Those looking for similar investment strategies will find them at $BRK.A (-1.06%)

Berkshire Hathaway (U.S.), $DHR (+2.59%)

Danaher (U.S.) or $MC (-0.32%)

LVMH (France). However, none of them offers this specific focus on Northern Europe combined with such a historically low P/E ratio.

14. Profit Margin Report

- EBIT Margin:

82.1% - Net Income: 23.71 billion EUR in profit on 29.63 billion EUR in revenue.

- Capital Efficiency: Return on capital employed (ROCE) of 27.3% demonstrates excellent capital allocation by management.

15. RaketenToni’s Conclusion & Risk Disclosure

Investor AB $INVE A (+1%) is the ultimate A-share stock!

If you don’t want to deal with the complexities of individual stock risks but still want to outperform the broader market, Investor AB gives you a Scandinavian super-ETF disguised as an individual stock to your portfolio. I’ve already done it!

A P/E ratio under 5, a 27% ROCE, and a 5-year performance that puts Berkshire Hathaway in the shade make this stock a must-have for any long-term wealth-building strategy.

An absolute top-tier compounder for the next 20 years!

As always, I’d love to hear your thoughts :)

Greetings from Denmark

Yours, Raketentoni

@Keineui

@Aktienhauptmeister

@Multibagger

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Stocktective

@Simpson

@WarrenamBuffet

@SAUgut777

@TradingHase

@PikaPika0105

@Derspekulant1

@NichtRelevant

@Klein-Anleger

@Dividendenopi

and, of course, everyone else :)