$MC (-0.32%)

$MBG (+0.42%)

$ULVR (-0.74%)

$PYPL (-1.11%)

$NBIS (-3.45%)

$SPGI (-0.17%)

$UPS (+0.98%)

$KO (+0.05%)

$GLW (+5.41%)

$BA (+0.7%)

$KER (-0.22%)

$ENPH (+5.44%)

$NXPI (+2.95%)

$STX (-5.1%)

$BE (-5.89%)

$V (-1.98%)

$MDLZ (-0.66%)

$000660

$P911 (+2.33%)

$BN (+0.26%)

$RMS (+1.31%)

$BAS (+0.77%)

$AG1 (+2.54%)

$LMND (+1.62%)

$SOFI (+1.27%)

$NDX1 (-1.66%)

$TER (-1.51%)

$GD (+1.25%)

$APH (-0.99%)

$AIR (+0.72%)

$SBUX (+0.22%)

$CMG (-2.74%)

$META (+0.42%)

$FTNT (-1.07%)

$QCOM (+4.66%)

$LRCX (+1.56%)

$HOOD (+2.56%)

$ARM (-2.19%)

$MSFT (-0.08%)

$CVNA (+3.3%)

$005930

$SU (+1.17%)

$INGA (-0.73%)

$OR (+0%)

$BMW (+2.08%)

$BATS (+0.63%)

$MA (-2.23%)

$ADS (-0.09%)

$SHEL (-1.3%)

$RACE (+1.37%)

$RDDT (+6.08%)

$TEM (+12.4%)

$COIN (+5.21%)

$AAPL (+0.3%)

$AMZN (+0.63%)

$CCO (+3.2%)

$LIN (+0.14%)

$ABBV (+0.12%)

$PUM (+0.17%)

$HAG (+0.79%)

$XOM (-1.36%)

$CVX (-1.64%)

- Markets

- Stocks

- British American Tobacco

- Forum Discussion

British American Tobacco

Price

Discussion about BATS

Posts

443Quarterly Results: July 27–July 31, 26

Podcast Episode 153: "Buy High. Sell Low." Microsoft, Mastercard, BAT, Bitcoin Tax Hike & Holding Period, Portfolio Review with Marc Moore

Spotify

https://open.spotify.com/episode/0w9Aff2JUG2emrUcXw3bQ2?si=OVHXR8ifRkCRc_1U7fYVQg

YouTube:

https://openyoutu.be/s7TBA0TxFLo

Apple Podcasts

A smooth glide instead of wild swings in value: My June 2026 Portfolio and Cash Flow Review 🪂

A quick note before we begin: I’ve significantly shortened the entire post to make it easier to read. Going forward, you’ll only be able to find some of the key metrics in my YouTube video or on Instagram. I’ve also completely removed the outlook section and the narrative text in between.

I hope you like the shorter version. 😊

I’ve had an eventful month! While things were relatively quiet on the markets, I was able to celebrate some real milestones in my passive income. My financial journey has been solid, calm, and steadily upward, just like hiking in Saxon Switzerland. When the foundation is right and your habits are in place, the daily market noise loses all its fear.

Here are the hard facts and all the key metrics from June:

Portfolio Performance: Stable Returns & Beat the Benchmark 📈

Total performance (TTWROR):

+0.57% for the reporting month (96.80% since inception)

Internal Rate of Return (IRR):

+0.79% (+12.29% since inception)

Delta: A hefty gain of +778.41 €

Benchmark comparison with the TTWROR of the following ETFs:

$VWRL (+0.29%) : -0.33%

$VUSA (+0.18%) : -0.41%

$IMEU (+0.61%) : +3.22%

Largest individual stock positions by volume as a percentage of the total portfolio:

$AVGO (+1.37%) : 2.78%

$WMT (-0.34%) : 1.62%

$GOOGL (-1.31%) : 1.54%

$CSCO (+0.21%) : 1.50%

$FAST (+1.18%) : 1.42%

Smallest individual stock positions by volume as a percentage of the total portfolio:

$GIS (+1.82%) : 0.43%

$NKE (-0.93%) : 0.43%

$NOVO B (+2.59%) : 0.49%

$CPB (+1.73%) : 0.49%

$BATS (+0.63%) : 0.57%

Top-performing individual stocks

$AVGO (+1.37%) : +332.73%

$GOOGL (-1.31%) : +134.74%

$CSCO (+0.21%) : +115.98%

$WMT (-0.34%) : +94.59%

$OHI (-0.17%) : +88.06%

Worst-Performing Individual Stocks

$NKE (-0.93%) : -50.39%

$GIS (+1.82%) : -47.00%

$CPB (+1.73%) : -36.10%

$NOVO B (+2.59%) : -20.48%

$DHR (+2.59%) : -18.41%

Asset Allocation

ETFs and stocks are not quite balanced yet.

ETFs: 43.7% (previous month: 43.4%)

Stocks: 56.3% (previous month: 56.6%)

Investments and Additional Purchases

Planned savings plan amount from fixed net salary: €1,080

Savings rate of the savings plans as a percentage of fixed net salary: 50.60%

Planned savings plan amount from fixed net salary, including reinvested dividends based on plan size: 1,200 €

Additional purchases from various sources: €392.83. This is offset by sales of €286.36 this month (portfolio rebalancing $FDXF (-1.22%) into $FDX (+0.31%) ).

Passive income from dividends and ETF distributions

Dividends and ETF distributions: €174.33 (€152.30 in the same month last year

Change from the same month last year: +14.46%

YTD dividends and ETF distributions: €1,088.83

Annual target: €2,100

Target achievement: 51.85% (Target: 50.00%)

Risk Metrics

Maximum drawdown in the reporting month: 1.15%, since inception: 17.17%

Maximum drawdown duration in the reporting month: 10 days; since inception: 702 days

Volatility in the reporting month: 1.72%; since inception: 28.79%

Sharpe Ratio, for the reporting month: 5.53, since inception: 0.42

Semivolatility, for the reporting month: 1.01%, since inception: 21.33%

Thank you for reading. 🚀

Now please leave me a comment. Is this summary helpful? Is there anything you think is missing? Let me know.

👉 This review is also available as a YouTube video and as Instagram carousel posts, which will be published as follows:

July 8, 2026: Portfolio review on Instagram (performance metrics, stock performance, allocation, sectors, additional purchases, and performance comparisons)

July 9, 2026: Budget review on Instagram (income, expenses, cash flow, ratios, budget adherence, and basic income check)

July 10, 2026: Cash flow review on Instagram (overview, YTD, and actual vs. target comparison for passive income, my top dividend payers, FIRE number, and capital reach)

Sometime during Week 28: Consolidated monthly review on YouTube

📲 You can find regular videos, Shorts, Reels, and carousel posts on the topics of frugalism, mindset, and investing at @frugalfreisein on Instagram and YouTube.

Please pay close attention to the spelling of my alias. Unfortunately, there are too many fake and phishing accounts on social media. I’ve already been “copied” several times.

My Portfolio

Hi everyone,

What do you think of my portfolio? First, a little background info:

About me: I’m in my mid-30s and have been actively trading on the stock market for over 12 years now. So I’ve experienced several market booms and crashes from an investor’s perspective :D

About the portfolio: I follow a core-satellite strategy with additional “income satellites.” The income satellites are used to generate income with the goal of creating a monthly cash flow, which I mainly use for additional purchases to keep the portfolio balanced.

Core: $XDWD (+0.3%) World ETF, $IMEU (+0.61%) EU ETF, $XMME (+0.2%) Emerging Markets ETF, $TDIV (+0.18%) VanEck TDIV

Satellites: $NVDA (+1.81%) NVIDIA, $MSFT (-0.08%) Microsoft, $GOOGL (-1.31%) Alphabet, $AMZN (+0.63%) Amazon, $HO (+0.09%) Thales // NVIDIA and Alphabet are currently being built up. The positions will both be doubled.

Income satellites: $D05 (+4.72%) DBS Group Holding, $KO (+0.05%) Coca-Cola, $BATS (+0.63%) BATs, $O (-0.18%) Realty Income, $VICI (+0.33%) VICI Properties

Others: Small positions for shorting and speculation. (Amgen, Vertex, SpaceX, BTC, Ethereum, ...)

Feel free to share your thoughts :)

The real question is whether this diversification in your core holdings actually makes a difference. At least if you’re taking a long-term view, the simple $IWDA is probably sufficient.

If you want to somewhat mitigate the US and tech concentration risk in these indices (which I think makes sense with a long-term horizon), then perhaps something like this as a core:

https://gerd-kommer.de/etf/vergleich/

Disclaimer: No, I don’t profit from this fund and have nothing to do with it. But that doesn’t change the fact that this is a good approach for people who want to build wealth over the long term while maximizing safety.

Incidentally, Stiftung Warentest also takes this view in its November 2025 ETF issue (I highly recommend reading it—it’s really well done).

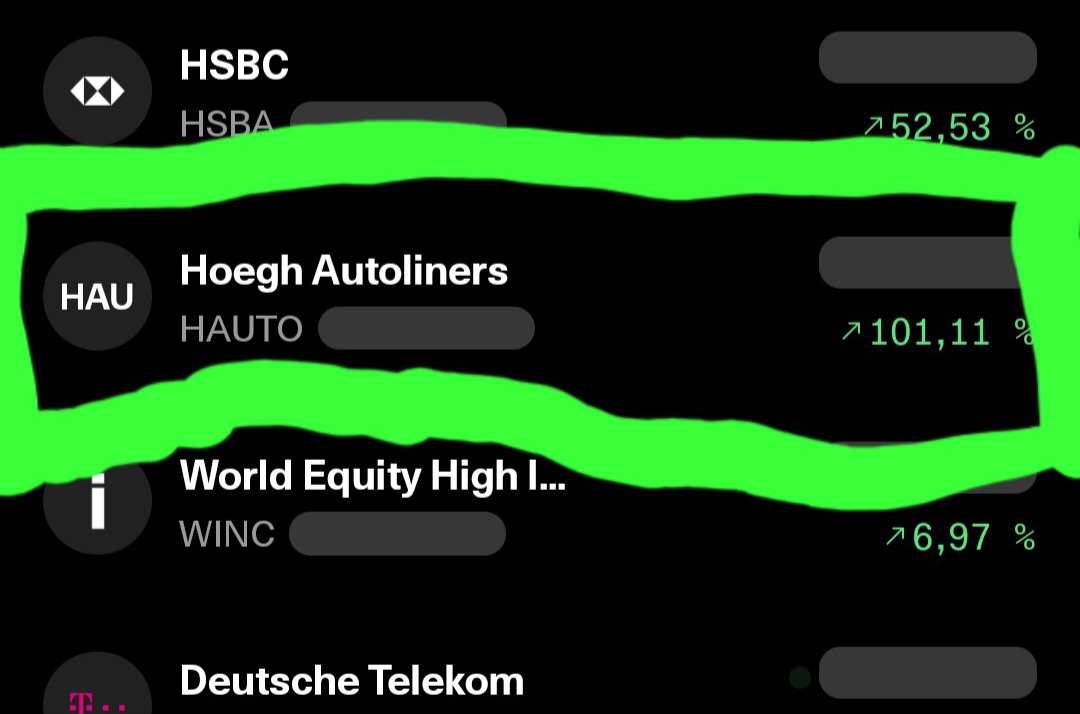

100%

...besides $BATS (+0.63%) and $3750 (+0.38%) the next value has now also -> $HAUTO (+6.15%) the 100% mark 🫠

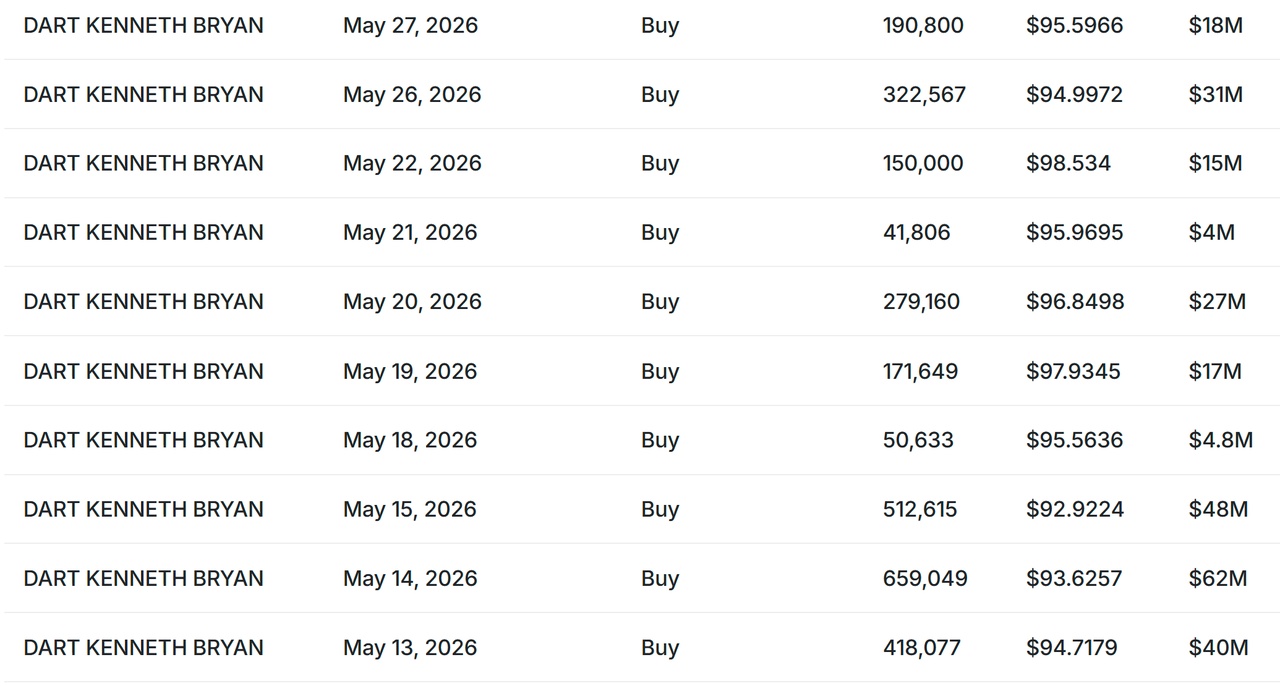

Famous Multi Billionaire Kenneth Dart bought 4.7 billion dollars of Flutter stock!!

He started buyng shares in the open market during march and it is currently increasing is position at a huge pace.

According to Bloomberg he is buyng every single day in the open market million of $ of shares.

Right now he owns 27,6% of $FLTR (+1.24%) and there are speculations of a possible take over.

The most amazing thing is that accoridng to his 13F filing it is the only american company he owns!!

He is betting his fortune only on this company, many speculates that he knows something that the market don't know yet and that's why he is stacking up shares massively.

It is not the first time that he bought a sin stock.

He was famously invested in tobacco companies like $BATS (+0.63%) , but now he has sold that position to increase his stake in the gambling sector.

During his interviews he explained that he like to buy at cheap prices in sectors that are overlooked by the market and $FLTR (+1.24%) right now is cheap on every metric.

He is currently increasing position in another swedish gambling company called Evolution $EVO (+1.11%) and now he owns more than 30%.

https://affpapa.com/billionaire-kenneth-dart-becomes-biggest-flutter-shareholder/

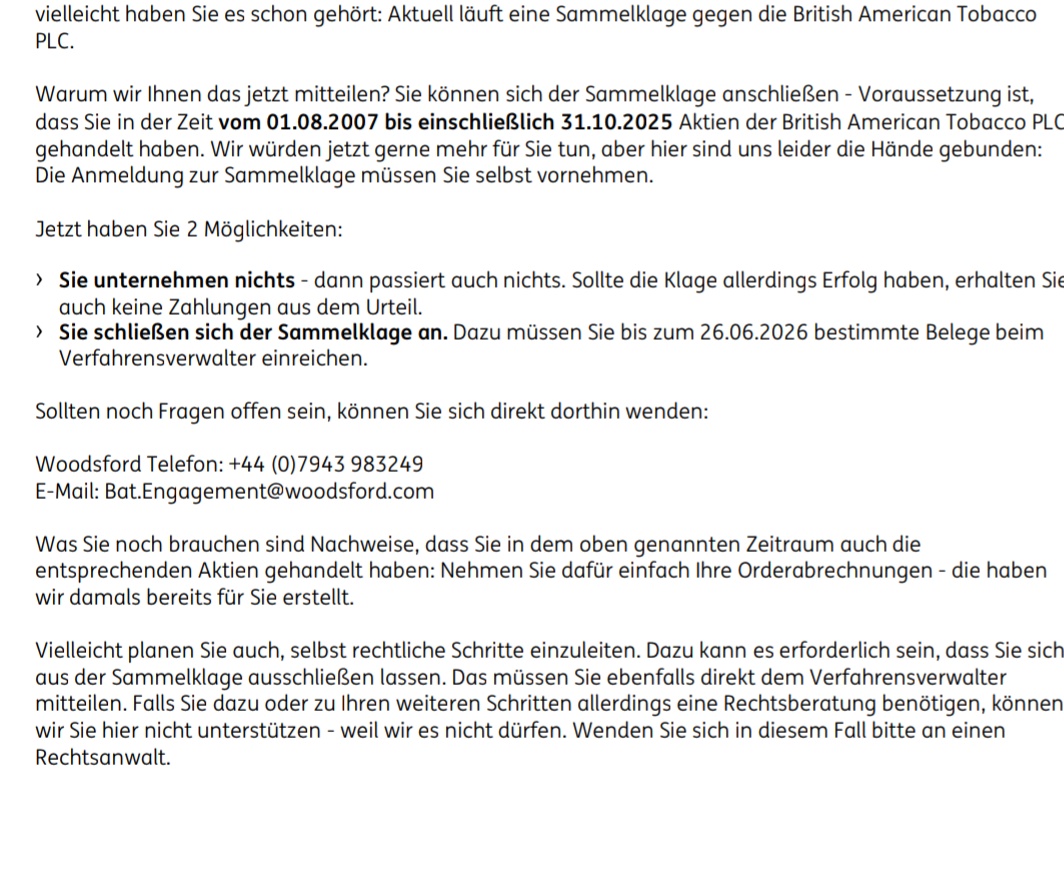

Class action

Hello,

I have received a letter from Diba saying that I can join a class action against BAT.

What is it about?

Is it serious?

What do I have to do?

How boring a securities account can be...

Maybe it's the most boring portfolio here on GQ when my first doublers are just the $ING (-0.96%) & $BATS (+0.63%) are... I started investing in 2023, before that I only tested the $EQQQ (+0.79%) and yes, if I had put 100% in there in 2020 and not let it run in the savings plan, it wouldn't be 94% now but a good 400% profit, but you're always smarter afterwards :-)

BAT ~ 10% price increase in 1 week

3 possible reasons:

1) A US federal judge has finally dropped the criminal proceedings for North Korea sanctions violations.

BAT had paid around 630 million dollars in 2023.

2) Competitor $IMB (+0.17%) is currently deliberately losing market share; the company would rather increase prices than defend volumes. What Imperial leaves behind, BAT can take with it.

3) On top of this, the 1.3 billion pound share buyback program is still running. BAT is continuously buying back its own shares and destroying them. Fewer shares in circulation means that every remaining share automatically becomes more valuable.

Over the year $BATS (+0.63%) is therefore +54%.

I am bullish and will be delighted when we break the ATH from 2016/17.

What is your opinion on BAT?

Happy smoking 🚬

Would be happy to see ATH again, that's when I (unfortunately) got in 😲

There are 2 scenarios for me:

Sell and the share price rises for you.

I hold again for 10 years and the price continues to fall.

Trending Securities

Top creators this week