Hello, everyone,

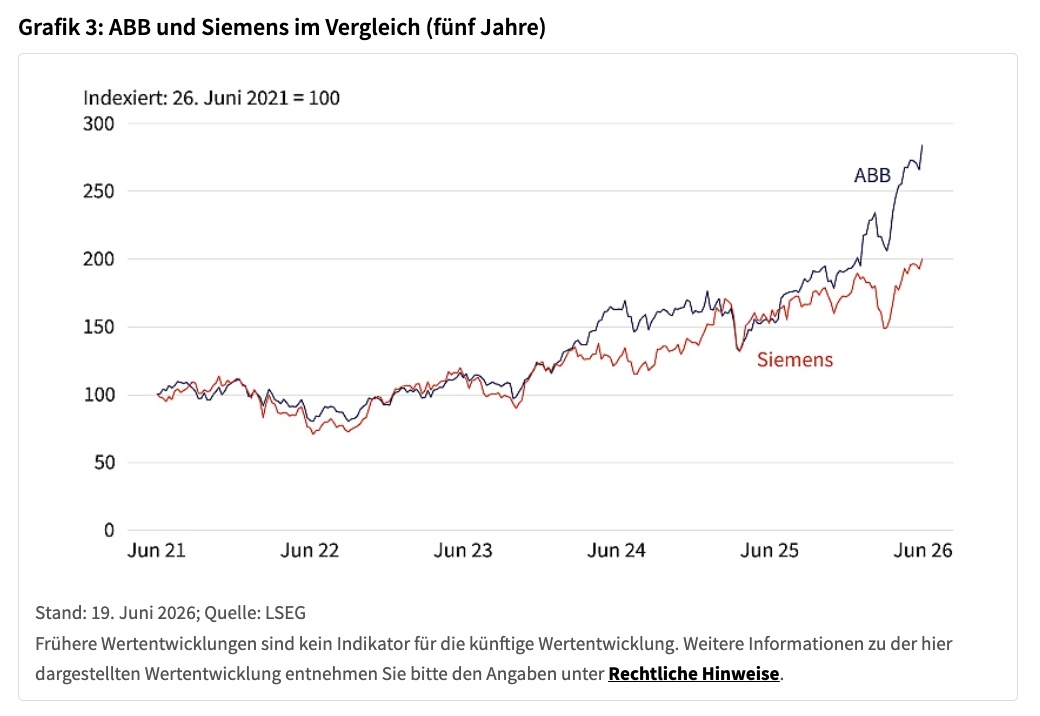

Many of you are investing in relatively unknown and unprofitable companies in the aerospace sector, some of which have high valuations. But you may not realize that Siemens is also an exciting player in this sector. The company is profitable and pays dividends. And it can easily absorb expensive development costs.

- Munich-based startup The Exploration Company aims to make its development work less complex and faster using Siemens Xcelerator

- Aiming to expand the use of reusable components in spaceflight

The European space company The Exploration Company is using software from the Siemens Xcelerator portfolio to make its development work less complex and faster. Founded in 2021 in Gauting near Munich, the company develops reusable, launch vehicle-independent space systems—including the Nyx family of spacecraft—as well as high-performance rocket engines to transport cargo and, eventually, astronauts into space.

“The future of aerospace will be shaped by companies that combine speed, innovation, and technical precision on a large scale,” said Edwin Severijn, Senior Vice President and General Manager for Europe, the Middle East, and Africa at Siemens Digital Industries Software. “Our collaboration with The Exploration Company exemplifies how Siemens Xcelerator helps customers build a connected digital enterprise that accelerates development and enables them to meet the demanding requirements of next-generation space programs,” added Severijn.

“Our mission at The Exploration Company is to facilitate access to space through reusable technologies. This requires an advanced and scalable development and engineering environment,” said Daniel Prudente Martins, Principal EWIS & Electrical Interfaces at Nyx Avionics, part of The Exploration Company. “Collaborating with Siemens and leveraging its industry-leading software helps us integrate our development processes, reduce rework, accelerate development, and make manufacturing more efficient as we continue to expand our operations. For the ‘Bikini’ mission—our demonstration space capsule—we went from initial concept to flight-ready hardware in just nine months. This allowed us to demonstrate the speed at which our integrated engineering approach enables rapid development.”

The integrated software tools from the Siemens Xcelerator portfolio ensure seamless data exchange and complete traceability throughout the entire development process, thereby supporting the aerospace industry’s stringent certification requirements. By bringing together mechanical, electrical, and simulation disciplines in a unified development environment, teams can work more efficiently. For example, when developing its high-thrust Storm rocket engine, The Exploration Company can better simulate and optimize its additive manufacturing processes, so that changes in one area can be immediately reflected in the other disciplines.