🌤 October review 2025

October was a month of upheaval, adjustment and small decisions with a big impact. With just two months to go until the IPQ's annual target, it currently stands at 97

📊 Performance & markets

An exact monthly performance cannot currently be calculated, but the robo-advisor is holding up well with an overall performance of +33,75 %.

Hot factor favorite

Allianz.

King Midas Factor

Xpeng.

1 Swiss franc quoted at 1.07 euros

₿ Crypto & alternative investments

There were minor adjustments and partial sales in the crypto sector. The share must be further reduced to 10%.

With Timeless was quiet, with only two Pokémon TTBs being sold.

Also with NFTs and music rights remained quiet - no new purchases, no sales, no drama.

🍷 Winery

The vineyard is also at a standstill. No new news, but sometimes calm is also a form of maturity.

📈 Individual shares, ETFs & savings plans

In the equities sector, on the other hand, things have been really busy.

$SLI (+2,09%) and $IBU (-1,67%) went through the roof - reason enough to take a few profits. In return $OTEX (+5,24%) was added to the portfolio. In addition $AAPL (+0,88%)

$MSFT (+2,65%) and $RWE (-1,96%) sold. Back in the depot: $AWK (+0,11%)

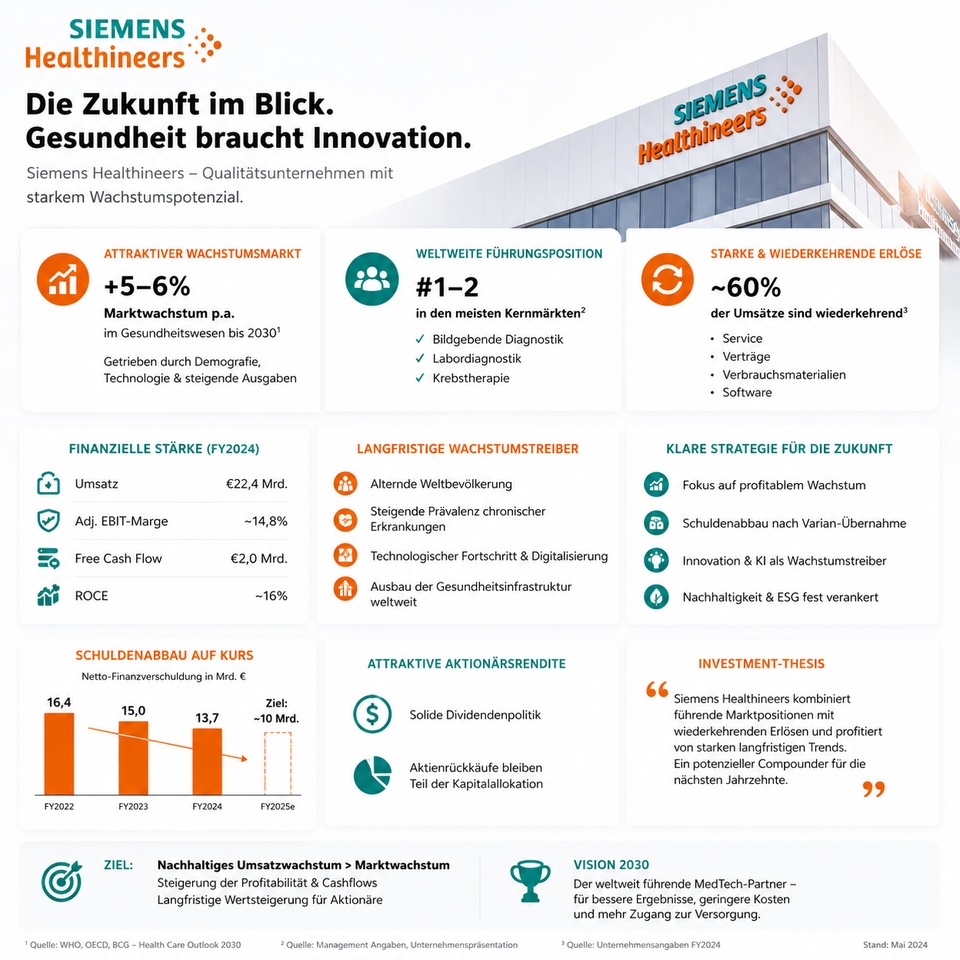

$SHL (+1,96%) and $CAKE (+1,5%) received an extra portion of capital.

The $XEON (+0%) was sold completely and shifted into the $bnp Paribas Easy Overnight - perhaps a mistake, perhaps a stroke of luck. Time will tell.

🚀 Crowdcube & Startups

It's been quiet here - no new projects.

🧠 Nao - a test run with hurdles

Curiosity is sometimes the best guide. After listening to a podcast about Nao I wanted to test the platform for myself. So I started eight savings plans on various assets on offer.

After just a few days, I had several exchanges with the support team Interest on the clearing account, confusing savings plan overviews and a strange booking logic: instead of being debited from the clearing account, the amounts were debited directly by direct debit.

When I wanted to withdraw the money, it turned out that it would remain blocked for a whole eight weeks. Not ideal.

Nevertheless, Nao remains exciting and the vision is convincing, even if the start was bumpy. Today a new product arrived, tradable via TR, so I sold my overnight rate swap with a yield of 6.2 % and reallocated. Was it the right decision? We'll see.

Do any of you also have experience with Nao?

🌴 Review October

I am currently on vacation for a week between October and November.

I've started my therapy, but I haven't felt any change yet. My biggest concern at the moment is the cost after the trial ends. A monthly dose costs around €250 and health insurance probably won't cover it. The trial will run until January, after which we will see what happens next.

On the positive side: the savings plan and the budget for 2026 are in place! In future, 10% of my gross salary plus reinvestments will go into individual shares. I have to plan a little more carefully because I have an unpaid vacation coming up in March 2026. I'm giving up my salary and 2.5 vacation days for this. I currently have my second readley test subscription in a row thanks to the Lidl app.

And yes, sorry to @christian

@TheRealRapha

@Leonard

@Gqnina I was at a wedding near Berlin and spontaneously spent two days at Tropical Island on the side. The headquarters had to wait, next time it will definitely work out! This week I'm treating myself to the fall fair and good food. And next week I'm off to Bavaria.

🎧 Interest rates, podcasts & real estate

With Vivid there was no news.

Podcast is in season 3 episode 1 is about financial goals

And also about real estate a small ray of hope: Service charges will fall by 5 euros in 2026.

🔮 Outlook for November

The coming month will probably be a little more expensive - a few purchases should finally be made. After all, you don't just live to make a profit. 😉

And you? How was your October?

If you want to find out more, feel free to follow me and if you don't like my investments: The block function works wonderfully. 😄

Thanks for reading - until the next review! 🙌