70 percent of my portfolio is $NVDA (+0,39%) —I’ve never really cared about that before. “I’ll hold onto this at least until 2030” was my motto. Because I consider it one of the best stocks in the world.

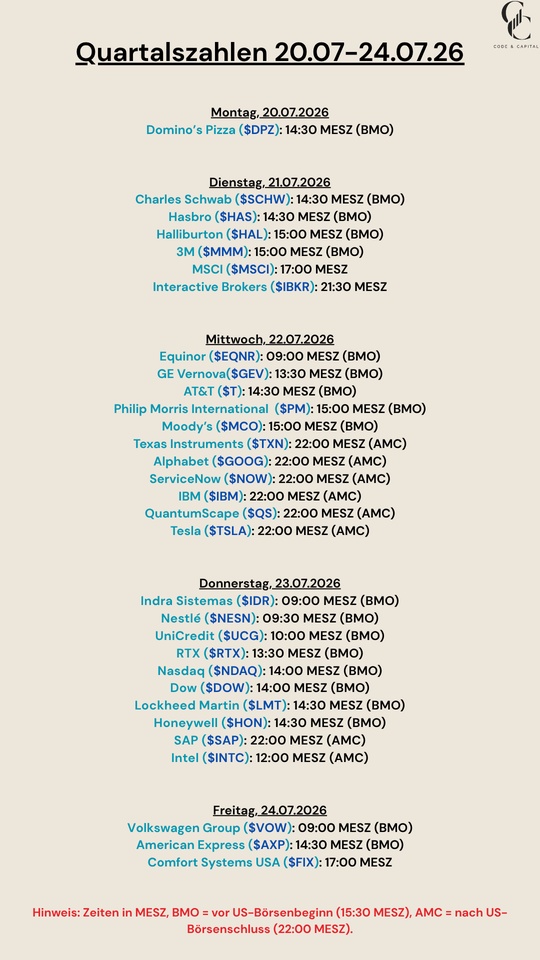

And what did I do yesterday? I sold 20 percent of the position and added three new stocks to my portfolio: $SAP (+6,4%)

$UCG (+0,68%)

$MUFG (+1,25%)

Why?

Because I think the risk is too high that meme stocks like SpaceX will first suck up all the money and then cause the bubble (which we’ve identified) to burst in a way that drags down fundamentally sound stocks as well.

And because I’m too old for that kind of crap: diversify.

Sure, the concentration is still huge, but it’s a start. If the madness on the stock market continues to drive the herd, I’ll keep selling off NVIDIA, but not everything. I’ll keep 40 percent.

I actually wanted to pick up something in the healthcare sector, but couldn’t find anything attractive.