Founded by former IBM engineers in the 1970s, SAP rose to become one of the most recognisable and largest companies on the European stock market. In its early days, it was genuinely innovative. Over time, however, the company developed a pattern: it rarely led new waves of technological change. It usually needed a push.

When the internet reshaped enterprise software, SAP clung to its on-premise dominance longer than it should have. When cloud-native systems began taking share, competitors like Microsoft and Oracle moved faster. SAP adapted, but not proactively. Still, to its credit, it ultimately overcame those challenges.

A new era began in 2022. With Christian Klein at the helm, growth re-accelerated, the platform became more deeply embedded in corporate ecosystems, and the stock more than quadrupled at one point. SAP is often described as the backbone of large enterprises, and that description is not exaggerated. Few systems are as deeply entrenched inside global corporations.

Now the company faces the next structural shift: AI.

I’ve already made the case for why I believe Microsoft, Palo Alto, or ServiceNow are unlikely to be disrupted. They integrated AI early and aggressively. Oracle pivoted heavily toward AI infrastructure. SAP, in contrast, appears cautious. Historically, SAP observes innovation, waits, evaluates, and then moves. That strategy has worked before. This time, I’m not sure it will.

AI is developing faster than any technological innovation before it. The pace is unprecedented. If a company hesitates too long, it risks irrelevance. Which is exactly why hyperscalers aren’t hesitant to pour hundreds of billions into AI development, at the risk of suppressing their margins and losing their beloved “asset-light” reputation. It’s absolutely critical to ride this wave. I am not claiming SAP will disappear overnight. Its systems are deeply embedded and costly to replace. Enterprises do not rip out core ERP systems casually. But markets price the future, not the past.

I cannot confidently say whether Salesforce is more future-proof than SAP. Both serve elite global customers. Both are deeply integrated into enterprise workflows. But what I can say is that vigilance matters more than ever. Companies that underestimate the speed of AI risk becoming the next cautionary tale. Blackberry once looked untouchable too.

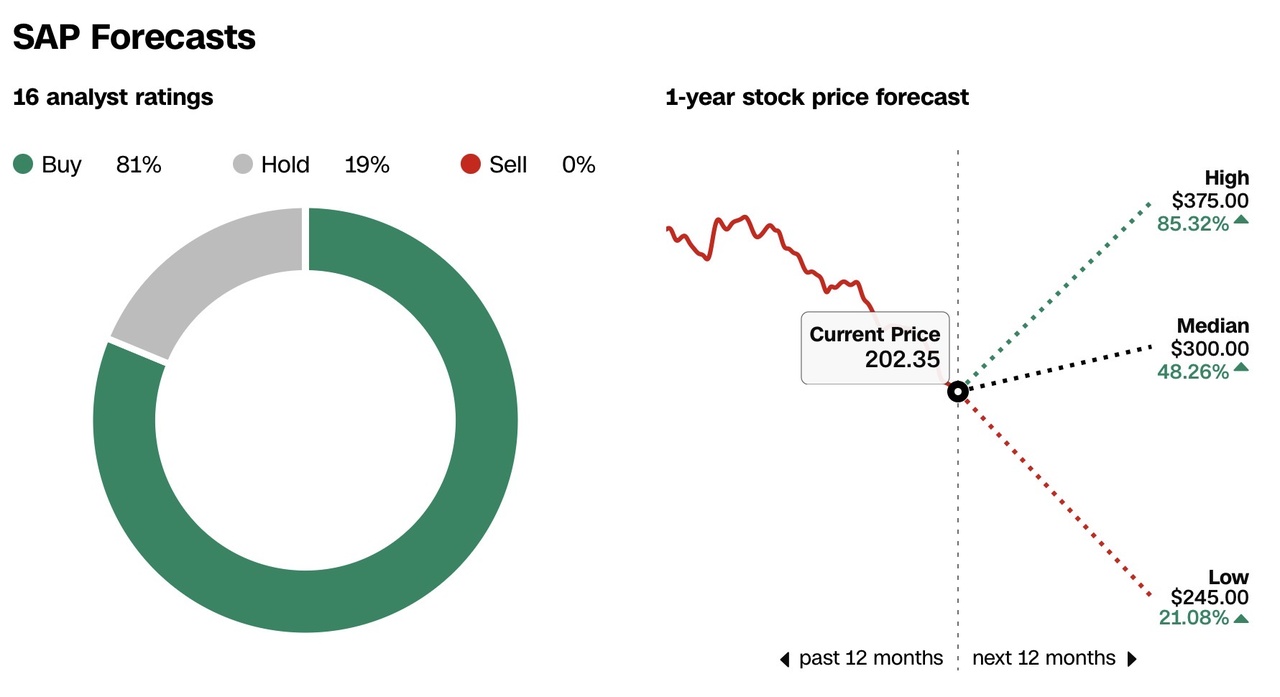

Let’s be realistic. SAP is not going anywhere tomorrow. But as quickly as the stock appreciated over the past few years, it could correct sharply if the AI narrative fails to convince investors. Just look at Adobe. Once a market darling, now trading roughly 60% below its highs and treated like a structurally impaired business.

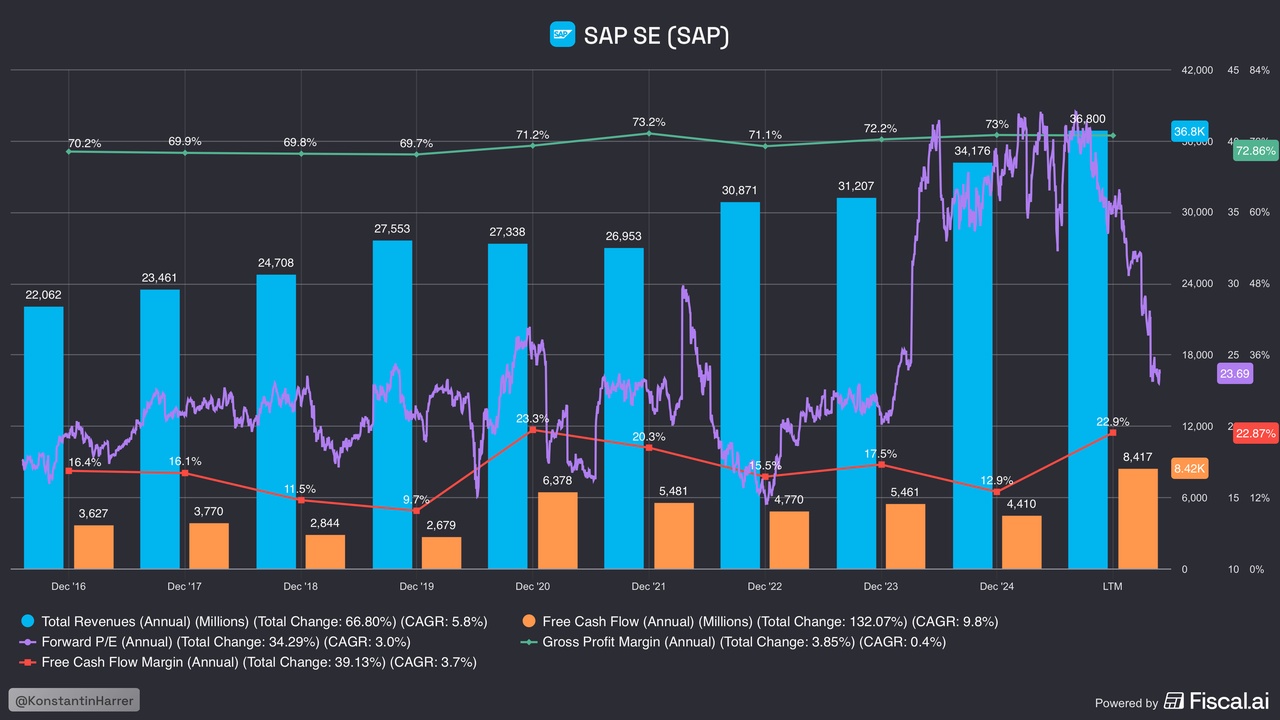

I would not buy SAP at current levels. Even at a forward P/E of 25x, the risk/reward feels off. The company may well adapt again, as it has in the past. But right now, there are clearer, safer ways to gain exposure to AI-driven growth.

$SAP (-1,28%)

$IBM (+0,05%)

$ORCL (-0,7%)

$MSFT (-0,43%)

$PANW (-2,47%)

$ZS (-0,26%)

$CRM (-0,96%)

$ADBE (-0,81%)

$NOW (-1,8%)