New month, and a few new trades.

First, I should note that most of my activity happened in the first half of the month. After that, I tweaked my approach and now have a significantly stricter framework in place when it comes to replacing one holding with another.

As I’m 100% invested right now, the focus is clear: avoid overtrading and don’t switch one high-quality long-term compounder for another just because of a recent dip.

The month itself was largely driven by the Iran war and the effective closure of the Strait of Hormuz. But in my own portfolio, I didn’t try to predict the next tweet from Donald Trump. Instead, I focused on picking up high-quality companies at a discount.

On March 2, I mainly added to the e-commerce side of my portfolio, increasing positions in MercadoLibre and Sea Limited after both stocks sold off quite significantly.

Sea reported a strong quarter on the top line and continues to take market share, but profitability remains a concern. For me, however, market penetration is the key objective at this stage. Margins are a nice-to-have for now. MercadoLibre dropped below $1,700, largely driven by geopolitical noise rather than anything business-related.

After that, things stayed relatively quiet until mid-month, when I made a few bigger moves. I sold my Netflix position, along with some fintech exposure, and redeployed that capital into broader asset managers that were caught up in the private credit selloff without being directly exposed: Brookfield and BlackRock.

I’ve already gone into detail on both buys and the Netflix sale in previous posts.

Around the same time, I also rotated my Visa position into Adyen. There are a few reasons behind that move which I’ll break down separately, but at its core it was a choice between “a bit more safety” and “safety plus stronger growth with European exposure.”

Into the second half of the month, the strategy became even clearer: double down on the most compelling opportunities. Risk/reward setups I’d almost call no-brainers.

I honestly didn’t expect to get another chance to buy Meta below $550 or Microsoft below $370. But when the opportunity presented itself, I took it. Both were already my largest positions going into the month, and they’ve only grown further.

The final addition, which I had been waiting on for a while and stayed disciplined for, was Airbus. I explained my reasoning a few weeks ago, but to sum it up, this was a classic case of short-term geopolitical noise overshadowing long-term quality. Airbus is a high-quality business with a backlog stretching years into the future and only one real competitor, which has its own well-documented issues.

Overall, I’m very happy with how the portfolio is positioned. The Iran war didn’t help performance, but I expect those pressures to ease sooner rather than later.

March Performance: -9%

Performance since inception: -5%

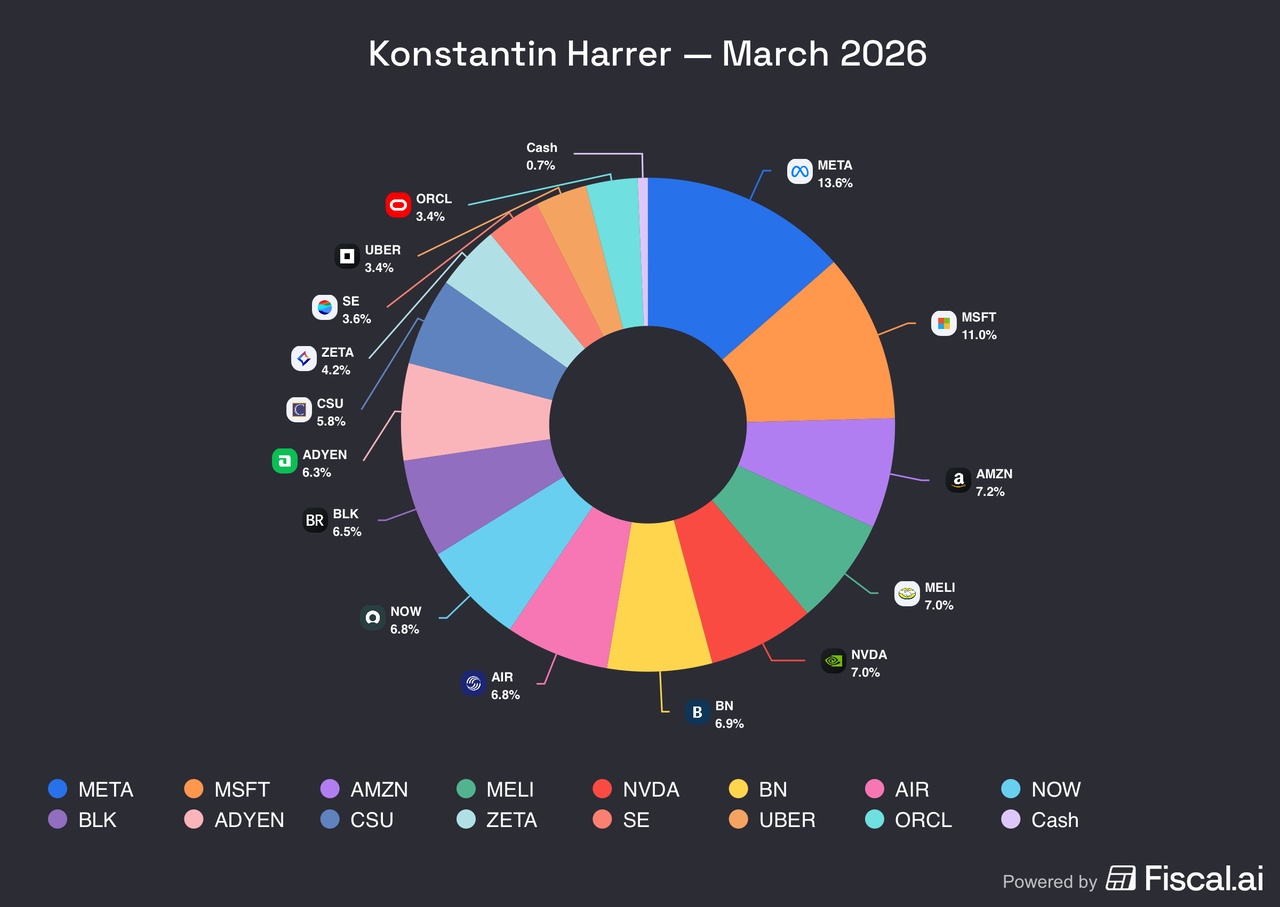

$META (+0,32 %)

$MSFT (+1,21 %)

$AMZN (+1,19 %)

$MELI (+0,25 %)

$NVDA (-1,75 %)

$BN (+0,62 %)

$AIR (-0,05 %)

$NOW (+1,73 %)

$BLK (-0,65 %)

$ADYEN (+1,22 %)

$CSU (+3,48 %)

$ZETA (+3,58 %)

$SE (+1,58 %)

$UBER (+4 %)

$ORCL (+2,74 %)