$VZ (+0,41 %)

$DPZ (+3,33 %)

$CDNS (-1,28 %)

$BARC (-0,12 %)

$SPOT (-1,8 %)

$BP. (+1,18 %)

$SPGI (-0,48 %)

$KO (-0,27 %)

$UPS (-0,22 %)

$AIR (-0,72 %)

$SBUX (+1,81 %)

$ENPH (+3,93 %)

$NXPI (-0,22 %)

$STX (+2,29 %)

$BE (+0,38 %)

$V (+0,62 %)

$MDLZ (-0,08 %)

$HOOD (-0,09 %)

$MBG (-0,12 %)

$UBSG (-0,19 %)

$DBK (+0,1 %)

$LMND (+0,83 %)

$SOFI (-0,63 %)

$TER (+3,59 %)

$ADS (-2,85 %)

$ABBV (+0,72 %)

$G24 (+1,42 %)

$WM (-0,01 %)

$APH (+0,51 %)

$CMG (+0,9 %)

$GOOG (-3,24 %)

$META (+1,09 %)

$MSFT (-0,66 %)

$AMZN (-1,78 %)

$005930

$BAS (-0,33 %)

$SU (+0,93 %)

$INGA (-0,02 %)

$ULVR (-0,73 %)

$IDR (+1,04 %)

$DHL (+0,4 %)

$CAT (+0,91 %)

$MA (-0,13 %)

$PUM (-1,4 %)

$MRK (-0,17 %)

$CNHI (+0,93 %)

$LLY (-1,27 %)

$FSLR (+0,24 %)

$WDC (-0,2 %)

$RBLX (-1,87 %)

$RDDT (-1,45 %)

$SNDK (+2,79 %)

$AAPL (-0,79 %)

$TWLO (+2,6 %)

$EL (+1 %)

$CL (-0,31 %)

$XOM (+0,14 %)

$CVX (+1,04 %)

UBS

Price

Discussion sur UBSG

Postes

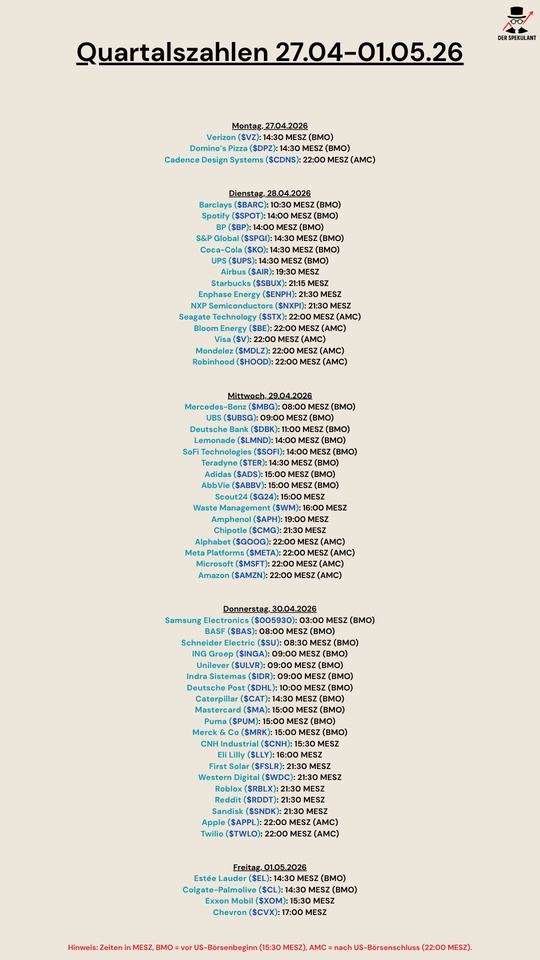

62Quarterly figures 27.04-01.05.26

March 2026 Monthly Portfolio Update - – Navigating Volatility

March has started off as one of the most challenging periods in global markets in recent memory.

The ongoing escalation between the United States, Israel, and Iran has driven widespread risk-off sentiment across equity markets, with oil and energy prices surging and stock indexes under pressure.

As a result, my portfolio is currently down around -2.5% for the month. This reflects the broader market reaction, where indices like the S&P 500 and Nasdaq have shown volatility and downside pressure as geopolitical tensions impact investor sentiment and inflation expectations.

Strategic Adjustments

In response to this environment, I’ve made several tactical adjustments:

Reduced exposure in some positions and closed others to secure partial liquidity

Currently holding approximately 10% in cash, which provides flexibility and optionality

Diversified further across new positions — (e.g., $TCL (-1,44 %)

$LOV (-0,62 %)

$APA (+1,67 %) , and from Swiss market $UBSG (-0,19 %) )

These recent additions reflect my focus on quality names with strong fundamentals, diversified geographies and sectors rather than simply chasing index performance.

What this means for Copiers

We’re in a risk-off market regime, not a bear market per se — volatility is a natural response to major geopolitical uncertainty.

Panic selling is rarely the best course of action — losses can be locked in permanently, whereas disciplined investors can find opportunities in dislocations.

The current cash buffer gives us dry powder to scale into positions at more attractive prices if the market continues to sell off.

Broader Market Backdrop

The current sell-off is driven by the escalation of conflict involving the US, Israel and Iran, which has:

Pressured global equity markets and raised inflation and risk aversion concerns

Pushed oil prices sharply higher amid fears of supply disruptions

Increased demand for safe-haven assets such as gold and the US dollar

Led to broad risk-off behaviour across major benchmarks in Asia, Europe and the US

Moneycontrol

No one can predict with certainty how this geopolitical situation will unfold, or how markets will react in the short term. But history shows that volatility tends to be temporary, and well-selected exposures often recover and outperform when clarity returns.

Final Thought

This isn’t a time to exit the market, but rather a time to reassess where capital can be deployed most effectively, balancing risk with long-term opportunity. I’ll continue adjusting positions as conditions evolve and will keep transparency front and centre.

Let’s stay calm, focused, and strategic.

😎 𝗗𝗶𝘀𝗰𝗹𝗮𝗶𝗺𝗲𝗿: This is my personal opinion and is for informational purposes only. You should not interpret this information as financial or investment advice

$NVDA (-0,8 %)

$CSPX (-0,29 %) $$GOLD

$TSLA (+0,84 %)

$AAPL (-0,79 %)

$PLTR (+0,06 %)

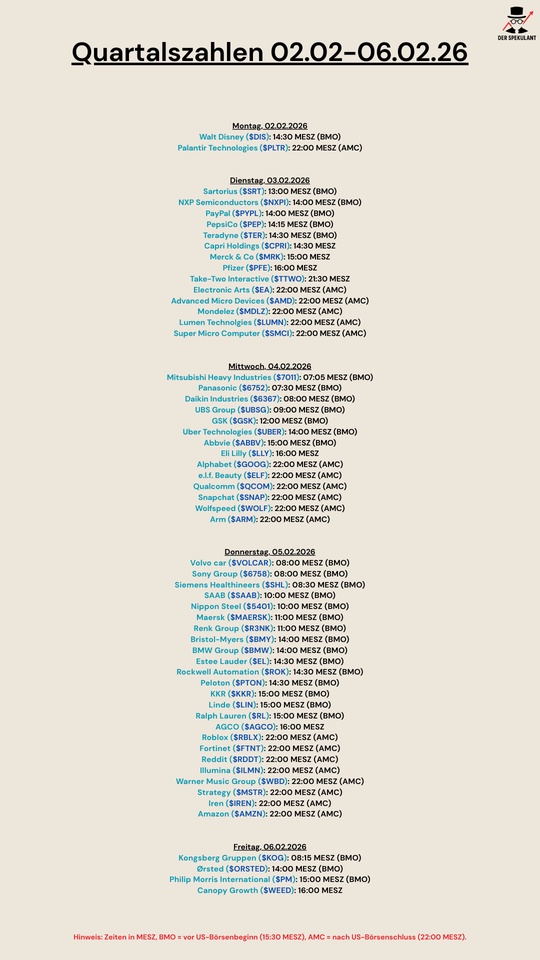

Quarterly figures 02.02-06.02.26

$DIS (+0,36 %)

$PLTR (+0,06 %)

$SRT (-1,03 %)

$NXPI (-0,22 %)

$PYPL (+0,55 %)

$PEP (+0,43 %)

$TER (+3,59 %)

$CPRI (+0,9 %)

$MRK (-0,17 %)

$PFE (-1,53 %)

$TTWO (-1,41 %)

$EA (+0 %)

$AMD (+0,67 %)

$MDLZ (-0,08 %)

$LUMN (-3,48 %)

$SMCI (+8,28 %)

$7011 (+2,87 %)

$6752 (+0,82 %)

$6367 (+1,84 %)

$UBSG (-0,19 %)

$GSK (-2,03 %)

$UBER (+0,72 %)

$ABBV (+0,72 %)

$LLY (-1,27 %)

$GOOG (-3,24 %)

$ELF (+0,29 %)

$QCOM (+0,08 %)

$SNAP (+3,29 %)

$WOLF (+2,58 %)

$ARM (-0,21 %)

$VOLCAR B (+0,39 %)

$6758 (-0,62 %)

$SHL (+0,97 %)

$SAAB B (+0,98 %)

$5401 (+2,26 %)

$MAERSK A (-1,04 %)

$R3NK (-1,59 %)

$BMY (-1,51 %)

$BMW (+1,4 %)

$EL (+1 %)

$ROK (+2,71 %)

$PTON (+2,52 %)

$KKR (+6,37 %)

$LIN (-0,07 %)

$RL (-2,26 %)

$AGCO (+0,55 %)

$RBLX (-1,87 %)

$FTNT (-1,88 %)

$REDDIT (+0,04 %)

$ILMN (+0,94 %)

$WMG (-5 %)

$IREN (+4,56 %)

$MSTR (-0,86 %)

$AMZN (-1,78 %)

$KOG (+2,97 %)

$ORSTED (+1,78 %)

$PM (+0,3 %)

$WEED (+4,32 %)

Rio Tinto hires bankers for Glencore deal

The Rio Tinto Group $RIO (-1,08 %)

$RIO (-0,28 %) has contracted a team of bankers, including renowned dealmaker Simon Robey, to explore a potential transaction with Glencore $GLEN (+0,67 %) with Glencore.

The mining company has enlisted the financial advisory services of Evercore, which recently acquired Robey's London-based boutique Robey Warshaw.

JPMorgan Chase & Co. and Macquarie Group are also advising Rio Tinto on the matter.

Rio Tinto is a leading global mining group focused on exploring, mining and processing the world's mineral resources. The company's mission is to produce materials that are essential for the progress of humanity.

UBS Group, a corporate broker for Rio Tinto, is currently not actively involved in the transaction. Citigroup, which has traditionally been closely linked to Glencore and has been involved in its recent transactions, is reported to have been in talks to secure a role in the potential deal.

Sources familiar with the matter have requested anonymity due to the confidentiality of the information.

In recent days, Citigroup $C (+0,37 %), JPMorgan $JPM (+0,71 %) and UBS $UBSG (-0,19 %) have cut or suspended their ratings on Rio Tinto and Glencore shares, according to data compiled by Bloomberg.

Glencore is a multinational commodities trading and mining company. Its activities include the production and marketing of metals and minerals, energy products and agricultural products.

The potential deal and the appointment of financial advisers underline the strategic importance of the matter for Rio Tinto, although no formal offer has yet been announced. The involvement of top banks underlines the scale and complexity of the potential transaction between the two mining giants.

Which shares have potential for you in 2026?

I am realizing more and more that I am hardly interested in loud promises and short-term hypes anymore. When I think about 2026, I tend to ask myself: which companies will still be in a stable position - no matter what the market environment looks like?

I am currently attracted to companies that work quietly, do their homework and don't need a new story every week. Banks like $UBSG (-0,19 %) or $UCG (+0,05 %) have had difficult years and that's exactly what makes them interesting for me. Companies that get through periods of stress and learn from them often emerge stronger.

At the same time, I find companies whose business you can touch exciting. Raw materials, for example. Nothing works without them - neither industry nor the energy transition. That's not a trend, it's reality.

Ultimately, I'm not interested in predicting the next big thing. For me, it's about consistency, reliability and business models that are sustainable even when things get uncomfortable.

I would really be interested:

Which stock do you have on your radar for 2026 - and why exactly this one?

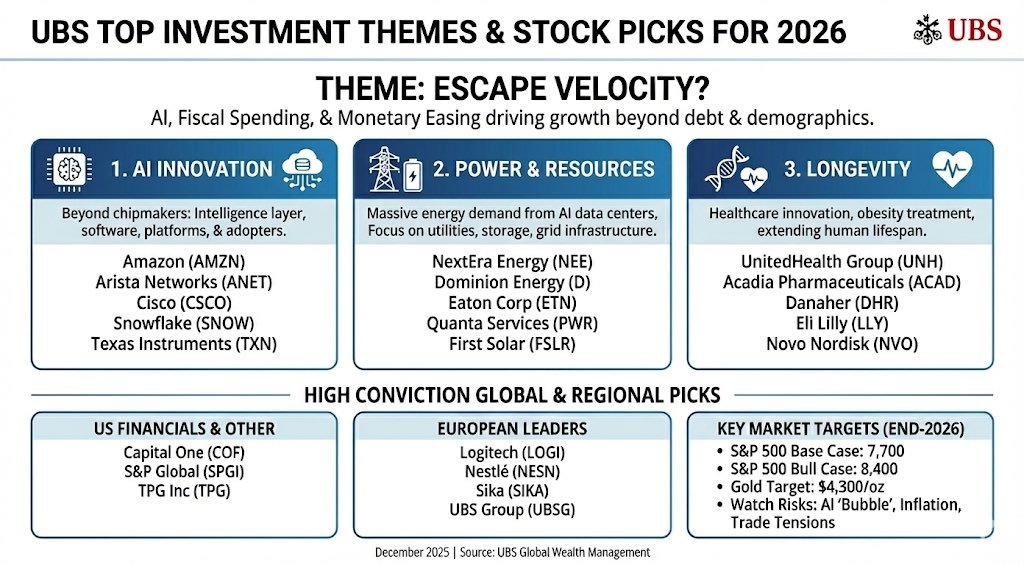

Equities | UBS Top Picks

The best shares for 2026 from the $UBSG (-0,19 %)

$AMZN (-1,78 %)

$ANET (+3,34 %)

$CSCO (-1,98 %)

$SNOW (-0,69 %)

$TXN (-0,14 %)

$NEE (+0,9 %)

$D (+1,17 %)

$ETN (+3,36 %)

$PWR (+0,44 %)

$FSLR (+0,24 %)

$UNH (-1,53 %)

$ACAD (+0,04 %)

$DHR (-0,36 %)

$LLY (-1,27 %)

$NOVO B (-0,01 %)

$COF (+0,7 %)

$SPGI (-0,48 %)

$TPG (+2,43 %)

$LOGN (-1,13 %)

$NESN (-1,07 %)

$SIKA (-0,12 %)

Commodities | Copper on the long lever

Copper is currently continuing its strong rally. Further price increases are now also expected from $C (+0,37 %) expected. Citi expects a structural deficit resulting from strong demand from the USA & Europe, but also from limited supply expansion over the coming years. $UBSG (-0,19 %) & $JPM (+0,71 %) even expect 12-13k tons for the 2nd quarter of 2026. An increase in copper can have an inflationary effect due to the high import costs, while the direct economic benefit for the domestic industry is low. $965275 (+0 %) would be burdened in the medium term under these circumstances, as the US economy benefits more from the positive effects, while Europe suffers more from the negative effects.

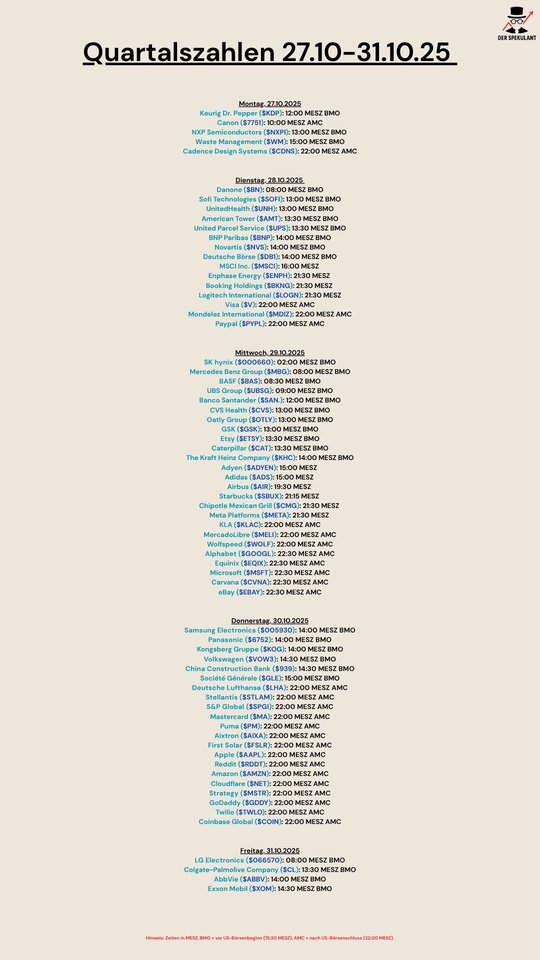

Quarterly figures 27.10-31.10.25

$KDP (-0,06 %)

$7751 (+0,08 %)

$NXPI (-0,22 %)

$WM (-0,01 %)

$CDNS (-1,28 %)

$BN (-0,94 %)

$SOFI (-0,63 %)

$UNH (-1,53 %)

$AMT (+0,41 %)

$UPS (-0,22 %)

$BNP (-0,41 %)

$NVS (-1,48 %)

$DB1 (-0,82 %)

$MSCI (+0,15 %)

$ENPH (+3,93 %)

$BKNG (-0,45 %)

$LOGN (-1,13 %)

$V (+0,62 %)

$MDLZ (-0,08 %)

$PYPL (+0,55 %)

$000660

$MBG (-0,12 %)

$BAS (-0,33 %)

$UBSG (-0,19 %)

$SAN (-0,23 %)

$CVS (-2,46 %)

$OTLY (-1,31 %)

$GSK (-2,03 %)

$ETSY (-0,8 %)

$CAT (+0,91 %)

$KHC (-0,86 %)

$ADYEN (-1,18 %)

$ADS (-2,85 %)

$AIR (-0,72 %)

$SBUX (+1,81 %)

$CMG (+0,9 %)

$META (+1,09 %)

$KLAC (+3,8 %)

$MELI (+6,35 %)

$WOLF (+2,58 %)

$GOOGL (-3,41 %)

$EQIX (-0,89 %)

$MSFT (-0,66 %)

$CVNA (-2,81 %)

$EBAY (-1,82 %)

$005930

$6752 (+0,82 %)

$KOG (+2,97 %)

$VOW3 (+0,59 %)

$GLE (-0,64 %)

$LHA (-0,48 %)

$STLAM (-2,35 %)

$SPGI (-0,48 %)

$MA (-0,13 %)

$PUM (-1,4 %)

$AIXA (+4,07 %)

$FSLR (+0,24 %)

$AAPL (-0,79 %)

$REDDIT (+0,04 %)

$AMZN (-1,78 %)

$NET (-0,45 %)

$MSTR (-0,86 %)

$GDDY (-1,03 %)

$TWLO (+2,6 %)

$COIN (-0,75 %)

$066570

$CL (-0,31 %)

$ABBV (+0,72 %)

$XOM (+0,14 %)

UBS to move to the us?

Colm Kelleher and Sergio Ermotti are secretly talking to members of the us administration. $UBSG (-0,19 %)

https://www.blick.ch/fr/suisse/clash-ubs-vs-suisse-discussions-avec-ladministration-trump-id21231419.html

Titres populaires

Meilleurs créateurs cette semaine