Last week, Siemens was $SIE (+2,58 %) had overtaken SAP $SAP (+3,69 %) then SAP was ahead again on Thursday. The two companies are currently on an equal footing with a market capitalization of around 200 billion euros each.

In the 38-year history of the Dax, which was launched on July 1, 1988, no other company has been at the top as often as Siemens, according to Handelsblatt calculations. One of the Munich-based company's recipes for success is reliability in the form of steadily rising earnings and dividends. Added to this is the ability to constantly adapt to industrial developments.

Ten of the current 40 DAX companies have been represented in the selection index, which originally only included 30 stocks, from the very beginning: Allianz, BASF, Bayer, BMW, Deutsche Bank, Henkel, Mercedes-Benz (then still under the name Daimler-Benz), RWE, Volkswagen and Siemens.

According to calculations by the Handelsblatt Research Institute, Siemens shares have performed best among these Dax veterans, with a price increase of almost 2300 percent. Anyone who has held the share since the Dax was founded has achieved an average price gain of 8.7 percent per year.

This does not include the many dividends paid to shareholders. Siemens shares have risen by around 5,850 percent when price gains and dividends are added together. This results in an average annual return of 11.3 percent.

No share that has been listed on the Dax since the beginning has performed better. By way of comparison, the Dax as a whole, including all dividends, has achieved an average annual return of 8.8 percent since its inception.

This Siemens return does not even take into account a particularly rewarding transaction for investors. Anyone who held Siemens shares at the end of September 2020 automatically received one Siemens Energy share free of charge for every two shares held. $ENR (+0,03 %) booked into the securities account.

With this step, Siemens spun off its power plant division. The new shares ended the first trading day on September 28, 2020 at €21.21 each. One share currently costs 153 euros. This corresponds to an increase of 621 percent in just five and a half years.

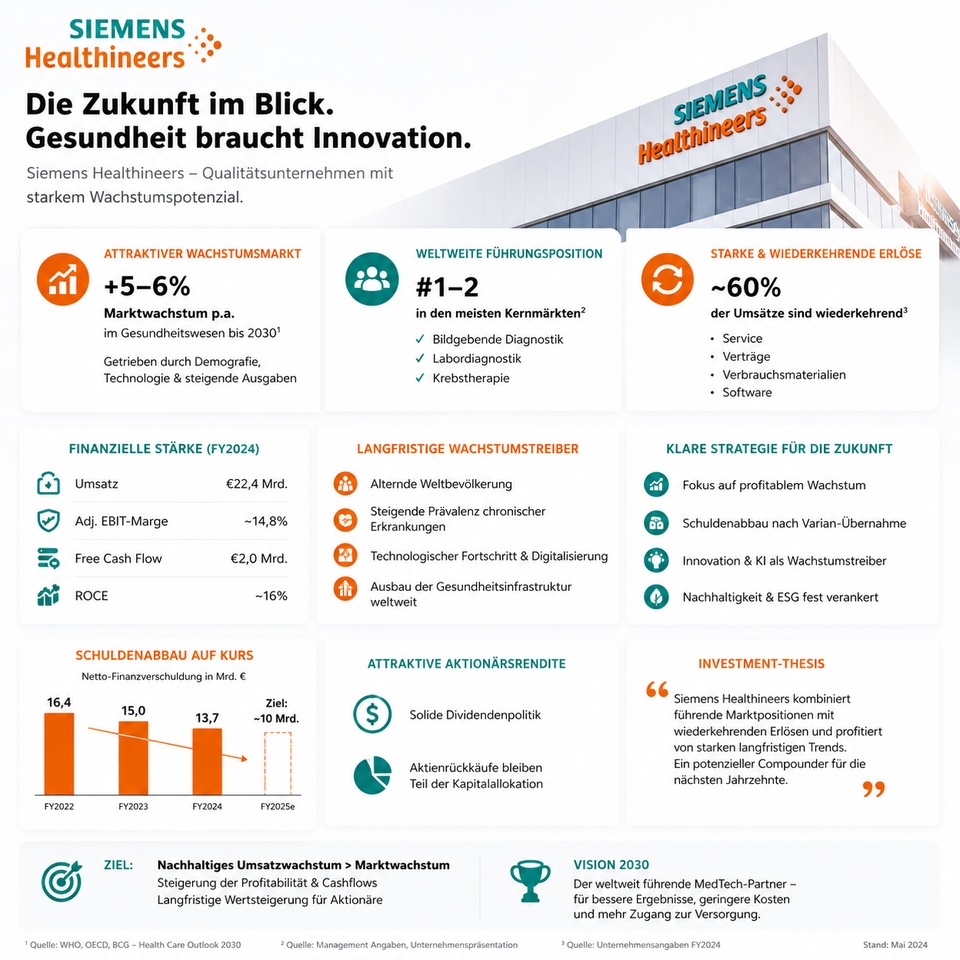

Siemens shareholders will soon receive another substantial bonus. After its power plant business, Siemens is spinning off its medical division. This is already listed on the stock exchange under the name Siemens Healthineers $SHL (+0,56 %) and is also listed on the Dax. However, Siemens currently holds around 67 percent of the shares.

This means that Healthineers is still fully consolidated in Siemens' balance sheet, i.e. Siemens recognizes the profits in its balance sheet. This will soon change, as 30 percent of Healthineers shares are to go to Siemens shareholders in a direct spin-off. They are to receive the new shares in their securities account, similar to Siemens Energy. What the distribution ratio will look like is still open.

With this deconsolidation of the medical technology unit, which has been listed on the stock exchange since 2018, the Siemens Group will lose almost a third of its sales, and the spin-off will also leave its mark on profits. For the current fiscal year, analysts are forecasting an average net profit of €8.1 billion for Siemens, compared to €9.6 billion last year. The reason for this is the loss of Healthineers.

Nevertheless, this strategy makes sense from an investor's point of view, as Siemens' priority is to grow faster and become more profitable. This shareholder-friendly focus is the reason why there are more and more different shares in the Siemens family.

Infineon $IFX (+4,21 %) is one of them, as Siemens floated its semiconductor division on the stock market back in 2000. There are now four Siemens shares in the Dax.

One reason for the many buy recommendations by analysts (currently: 21 buy | 4 hold | 4 sell) for Siemens is, in addition to the ambitious, but compared to its competitors, more favorable valuation, the profit sharing for shareholders. The Managing Board intends to increase the dividend from €5.20 to €5.35 for the past fiscal year, which at Siemens ended on September 30, 2025. This is the fifth increase in a row. The dividend has more than tripled since 2010.

At 2.1%, the dividend yield is rather low by historical standards. In the last 20 years, there has almost always been at least three percent to be had. However, the lower yield is by no means the result of slower rising, let alone falling, dividends, but solely due to the enormous increase in the share price. Over the past three years, the share price has risen by 80 percent.

The dividends have not been able to keep up with this rapid development. As a result, the dividend yield for new entrants has fallen. However, this is not a real problem in view of the sharp rise in the share price.

Source text (excerpt) & image: Handelsblatt, 05.02.2026