$MC (+0,63 %)

$MBG (+0,76 %)

$ULVR (+0,15 %)

$PYPL (+0,08 %)

$NBIS (+4,05 %)

$SPGI (+0,31 %)

$UPS

$KO (-0,26 %)

$GLW (+2,06 %)

$BA (+1,12 %)

$KER (+2,31 %)

$ENPH (+2,4 %)

$NXPI (+1,72 %)

$STX (+2,54 %)

$BE (+3,14 %)

$V

$MDLZ (-0,36 %)

$000660

$P911 (-0,24 %)

$BN (+0,69 %)

$RMS (+2,61 %)

$BAS (-0,49 %)

$AG1 (+3,58 %)

$LMND (+0,3 %)

$SOFI

$NDX1 (-0,43 %)

$TER

$GD (-0,77 %)

$APH (+1,94 %)

$AIR (+2,04 %)

$SBUX

$CMG (+0,27 %)

$META (+1,7 %)

$FTNT (+0,9 %)

$QCOM (+2,04 %)

$LRCX (+3,32 %)

$HOOD

$ARM (+2,51 %)

$MSFT (+1,33 %)

$CVNA (+1,3 %)

$005930

$SU (+2,34 %)

$INGA (+1,97 %)

$OR (+1,14 %)

$BMW (+0,69 %)

$BATS (-0,48 %)

$MA (-0,16 %)

$ADS (+2,75 %)

$SHEL (-2,23 %)

$RACE (+3,1 %)

$RDDT (+1,68 %)

$TEM

$COIN (+2,37 %)

$AAPL (+0,07 %)

$AMZN (+1,46 %)

$CCO (+3,08 %)

$LIN (+0,56 %)

$ABBV (+0,04 %)

$PUM (+2,63 %)

$HAG (+2,07 %)

$XOM (-3,24 %)

$CVX (-2,8 %)

Linde

Price

Discussion sur LIN

Postes

77Quarterly Results: July 27–July 31, 26

What do you think of Linde, or are there better alternatives?

Advantages – Why Linde Is a Clear Beneficiary of the AI & Semiconductor Boom

• Structural Winner — Every new chip fab (TSMC, Samsung, Intel) needs Linde gases: nitrogen, argon, hydrogen, silanes, NF₃.

• AI Data Centers — HPC clusters and AI server farms use Linde’s cooling gases → rising demand.

• Helium Shortage — Global supply constraints are driving up prices → Linde benefits from its strong market position.

• Long-Term Contracts — 10–20-year “take-or-pay” deals ensure predictable, stable cash flows.

• Low Competition — Ultra-pure process gases are extremely difficult to produce → high moat.

• Diversified regions — Americas, EMEA, APAC → no concentration risk like that faced by pure-play semiconductor companies.

• Defensive + growth — combination of infrastructure stability and AI growth → a rare mix.

---

Disadvantages / Risks — primarily from Asia

• China is building its own gas production capacity — could cost market share in the long term, but high-purity production remains challenging.

• Geopolitics in Taiwan — the industry’s dependence on TSMC → systemic risk for all suppliers.

• Helium export controls — China halts exports → global risk, but more of an opportunity for Linde.

• Japanese specialty chemicals — strong competition in chemicals, but not in gases.

• Cyclical semiconductor investments — When Capex declines, gas demand also falls (but less sharply than for equipment companies).

• Regulatory risks — Environmental regulations and energy prices can affect margins.

ASML

Indirectly, I do benefit from Crazy Musk. $ASML (+2,52 %)

Another indirect investment will follow on June 29 with the spin-off of Honeywell Aerospace. (I will only place a first tranche)

Perhaps even my seemingly boring $LIN (+0,56 %) might even find a catalyst again.

As one of the most important strategic partners for commercial space travel, Linde has invested around 100 million US dollars in the construction of a new air separation plant in Brownsville, Texas.

Right next to the SpaceX Starbase.

Space travel is an extremely lucrative market for gas companies like Linde - gases are absolutely vital for the launch of a rocket, but account for only a tiny fraction of the total launch costs. So SpaceX is not cutting corners here.

But, of course, the segment currently only accounts for around 1-2%.

Opinions on the portfolio?

Hi there, I would like to share my portfolio here to hear opinions and feedback. XLK is my core which I believe will continue to grow over the longterm. Alphabet is my second biggest position, for the same reason as my XLK holding. 6 other stocks make up the rest, mainly to have a defensive side plus the dividends are also nice. I’m thinking of adding $KTY , but I prefer to hold no more than what I currently have unless it’s very compelling or if it’s temporary.

Let me know what you think! All opinions are welcome.

$XLKS

$GOOGL (+1,1 %)

$D05 (+1,6 %)

$WM (-1,02 %)

$LIN (+0,56 %)

$ALV

$BK (+0 %) ( now BNY) $DG

Linde: Profiting from the growing aerospace industry

- Rising demand for industrial gases due to more satellite launches and larger launch vehicles

- Industrial gases are essential for rocket propulsion, cryogenics, testing and launch operations

- The expansion of commercial space travel could become a long-term growth driver

- UBS expects demand for industrial gases from the space sector to accelerate by the end of the decade

Portfolio conversion ⚠️🏗️🚧

Hello Getquin Community,

as I have been wanting to thin out my portfolio and make it more compact for some time now, I have been thinking about the best way to do this over the last few days.

I started today, $KO (-0,26 %) sold and exchanged for $MAIN (+0,4 %) exchanged. 🏦 🔄 🥤

The background to this is that I am currently very focused on basic consumer goods and am not yet very well positioned in the area of finance (apart from Visa).

My savings plans for individual shares $SHEL (-2,23 %) , $WM (-1,02 %) , $8001 (+1,6 %) , $MCD (+0,19 %) , $LIN (+0,56 %) and $ALV have been stopped and the positions will be liquidated as soon as they are positive.

Individual stocks that are still being invested in on a monthly basis are $NOVO B (+1,36 %) , $PG (+0,32 %) , $PEP (-0,17 %) , $V and $DTE (+1,09 %) due to the currently attractive valuations.

The sum of the removed savings plans is added to the $IWDA (+0,86 %) and $FLXI (+1,03 %) will benefit. I am also adding the $LDGL (+0,77 %) ETF into my custody account as a "cash cow". 💸

What do you think of my restructuring?

@DonkeyInvestor has written a good article on this.

Reallocations & profit taking

Swap: Linde $LIN (+0,56 %)

for Ferrari $RACE (+3,1 %)

I have thrown Linde completely out of the depot. (had it for about 2.5 years)

The entire sum went directly 1:1 into Ferrari.

Profit taking: Intel $INTC (+1,45 %)

& NVIDIA

$NVDA (+0,48 %)

Intel is currently up around 300% in my portfolio. I have used this to clean up a bit:

- I pulled out the original stake completely.

- I am now simply letting the pure profits continue. (maybe with a stop loss, let's see)

- The capital released from the stake is now invested in NVIDIA.

Small quarterly update: portfolio build-up phase

Hello to the GQ community ✌️

My first post after being kicked about 4 weeks ago - who would have thought that solidarity towards one of the members (@Klein-Anleger ) would lead to a ban so quickly? But the goodwill of getquin was so BIG (and above all "on trial") that they graciously let me back into the holy grail of the GQ community 😉

So guys, learn from my mistakes: the goodwill here is not an Infinite Money glitch ! Save your solidarity, reduce your commitment to other members to zero and the most important thing 🚨: No surreptitious advertising for alternative financial platforms like "Cisdord" 😉😂.

Sorry, the side blow after 4 weeks of abstinence had to be 🤝

so joking aside...

⏳The first three months of 2026 have passed. Time for a brief interim summary of the current status of my reconstruction.

Before I started rebuilding the portfolio, I naturally thought about what strategy I wanted to pursue in the coming months and years - especially with regard to stock selection and weighting.

To be honest, my original plan was to keep a portfolio with a maximum of 20 shares. In the course of time, however, I realized that it will probably not stay at 20 stocks, but that the number is more likely to increase to around 30 positions (+/-).

♟️Mein Focus & my strategy:

In a nutshell: The clear focus is on growth 🚀. Dividends tend to play a subordinate role. Here I show you my shopping list and what my portfolio should look like in the future. The stocks I have already bought are marked with a green tick and without a tick, I'm still waiting ⏳

🤖TECH:

- AMAZON $AMZN (+1,46 %) ✅

- MICROSOFT $MSFT (+1,33 %) ✅

- CROWDSTRIKE $CRWD (+1,97 %) ✅

- SYNOPSYS $SNPS (+1,22 %) ✅

- INTUIT $INTU (+1,74 %) ✅

- CONSTELLATION SOFTWARE $CSU (-0,99 %) ✅

- SERVICENOW $NOW (+2,74 %) ✅

- ALPHABET $GOOGL (+1,1 %)

- NVIDIA $NVDA (+0,48 %)

- ASML $ASML (+2,52 %)

- MONOLITHIC POWER SYSTEMS $MPWR (+3,07 %)

- ARISTA NETWORKS $ANET (+2,15 %)

- KEYENCE $6861 (+2,8 %) ✅

- TSMC $TSM (+1,55 %)

- MARUWA $5344 (-0,65 %)

- LASERTEC CORP $6920 (+1,74 %)

- NETCOMPANY $NETC (+2,77 %) ✅

- CELLEBRITE DI $CLBT (+1,39 %) ✅

🏦💸FINANCE:

- SOFI TECHNOLGIES $SOFI ✅

- S&P GLOBAL $SPGI (+0,31 %) ✅

- VISA $V ✅

- MUNICH RE $MUV2 (+1,51 %) ✅

- GERMAN EXCHANGE $DB1 (+1,12 %) ✅

- PARTNERS GROUP $PGHN (+0,8 %) ✅

- BROOKFIELD CORP $BN (+0,74 %) ✅

- HOULIHAN LOKEY $HLI (+0,97 %) ✅

- BROADRIDGE $BR (-0,8 %) ✅

- CBOE GLOBAL MARKETS $CBOE (-0,6 %)

🏥🩻HEALTHCARE:

- NOVO NORDISK $NOVO B (+1,36 %) ✅

- INTUITIVE SURGICAL $ISRG (+0,84 %)

- STRYKER $SYK (-0,05 %)

- BOSTON $BSX (+0,47 %)

- CATALYST PHARM $CPRX

🏭🏗️INDUSTRIE & REST:

- WASTE MANAGEMENT $WM (-1,02 %) ✅

- GRAB HOLDINGS $GRAB (+1,58 %) ✅

- CINTAS $CTAS (-0,31 %) ✅

- MonotaRO $3064 ✅

- ITOCHU $8001 (+1,6 %) ✅

- HERMES $RMS (+2,61 %) ✅

- MERCADOLIBRE $MELI (+0,59 %) ✅

------------------------

this is my extended watchlist:

IN TECH:

RAMBUS $RMBS (+1,04 %) , QNITY ELECTRONICS $Q (+1,26 %) ,

INNODATA $INOD (+2,43 %) , NETFLIX $NFLX (+0,49 %) ,

VERTIV $VRT (+2,33 %) , PALANTIR $PLTR (+1,82 %) , VAT GROUP $VACN (+1,47 %) , BROADCOM $AVGO (+2,16 %) , AMADEUS IT $AMS (+2,24 %) , DISCO CORP $6146 (+5,94 %) , A10 NETWORKS $ATEN (+1 %) , RORZE $6323 , CAMTEK $CAMT (+4,9 %)

FINANCE:

APOLLO GLOBAL $APO (+1,3 %) / BLACKSTONE $BX (+0,59 %) , ALLIANZ $ALV , FIRSTCASH $FCFS (+0,49 %) , BLACKROCK $BLK (+0,65 %) SKYWARD SPECIALITY INSURANCE $SKWD , VERISK ANALYTICS $VRSK (+1,42 %) PRIMERICA $PRI (+1,09 %) , ERIE INDEMNITY $ERIE (+2,86 %)

HEALTHCARE:

MERIT MEDICAL SYSTEMS $MMSI (+1,15 %) , REGENERON PHARM $REGN (-0,49 %) , UFP TECHNOLOGIES $UFPT (+0,86 %) , COLLEGIUM PHARM $COLL (+1,29 %) , LIGAND PHARM $LGND (+1,13 %) , HOYA CORP $7741 (+0,57 %) , SHIONOGI $4507 (+1,92 %) , IRADIMED $IRMD (+0,9 %)

REST:

MISUMI GROUP $9962 (+2,6 %) , KANEMATSU $8020 (+0,88 %) , APPLIED INDUSTRIAL TECH $AIT (+0,56 %) , BADGER METER $BMI (-1,15 %) , CEMENT ROADSTONE HOLDING $CRH (+1,9 %) , KADANT $KAI (+0,36 %) , INTERTEK GROUP $ITRK (+0,07 %) , IDEX CORP $IEX (+1,59 %) , ORLA MINING $OLA (+2,35 %) , NEWMARKET CORP $NEU (-0,36 %) , ROTORK $ROR (-1,29 %) , POWER INTEGRATION $POWI (+1,61 %) , LINDE $LIN (+0,56 %) , GAZTRANSPORT & TECHNIGAZ $GTT (-2,06 %)

This is not yet my final stock selection/watchlist. Of course, there can always be changes if, for example, the @Tenbagger2024 continues to present such undiscovered gems 🙏🏽🧐

------------------------

What should the sector/country weighting look like?

Let's start with the "desired"

🌍country weighting:

🇺🇸🇨🇦USA ~60%

🇪🇺EUROPA ~20%

🇯🇵JAPAN/ASIA ~15%

Rest ~5%

Sector weighting should be as follows:

💻TECHNOLOGY: ~30-35%

💸FINANCE: ~ 20-25%

HEALTHCARE: ~ 10-15%

🏭INDUSTRY: ~ 10-15%

REST: ~ 5-10%

So, what has happened since the beginning of the year?

Of course there were no sales 😬

There have been a few purchases where I have a finger in the pie.

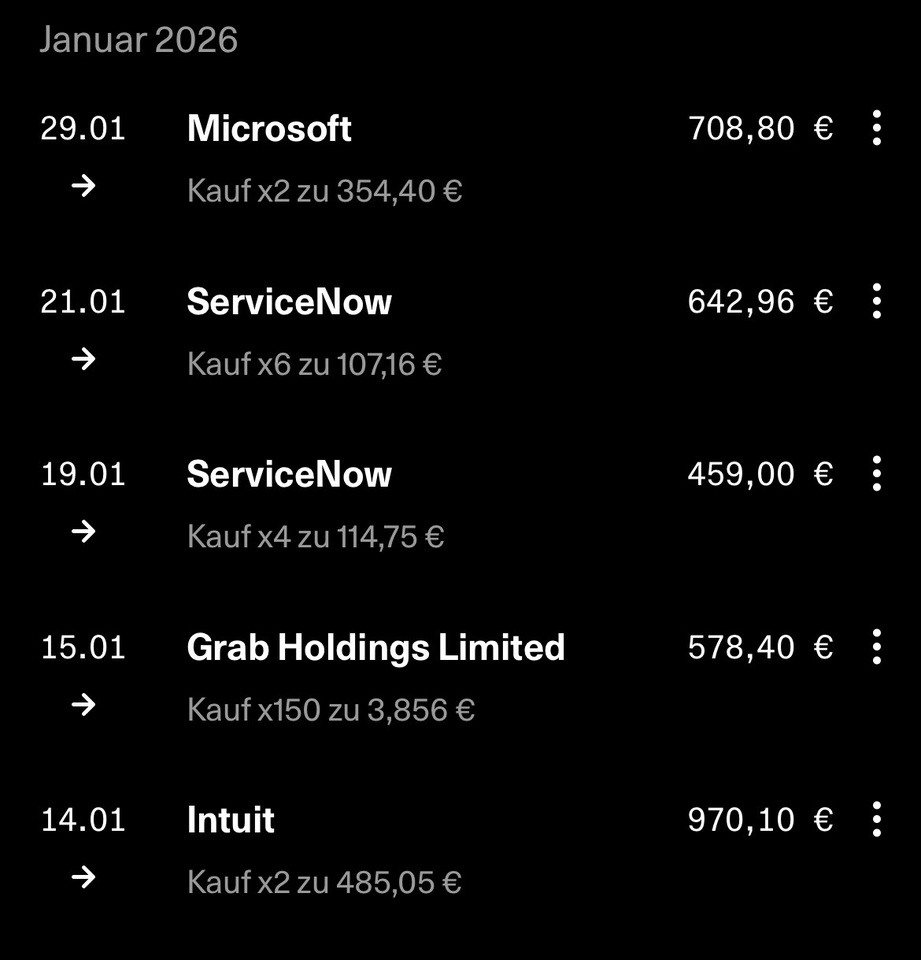

JANUARY PURCHASES

$INTU (+1,74 %)

$GRAB (+1,58 %)

$NOW (+2,74 %)

$MSFT (+1,33 %)

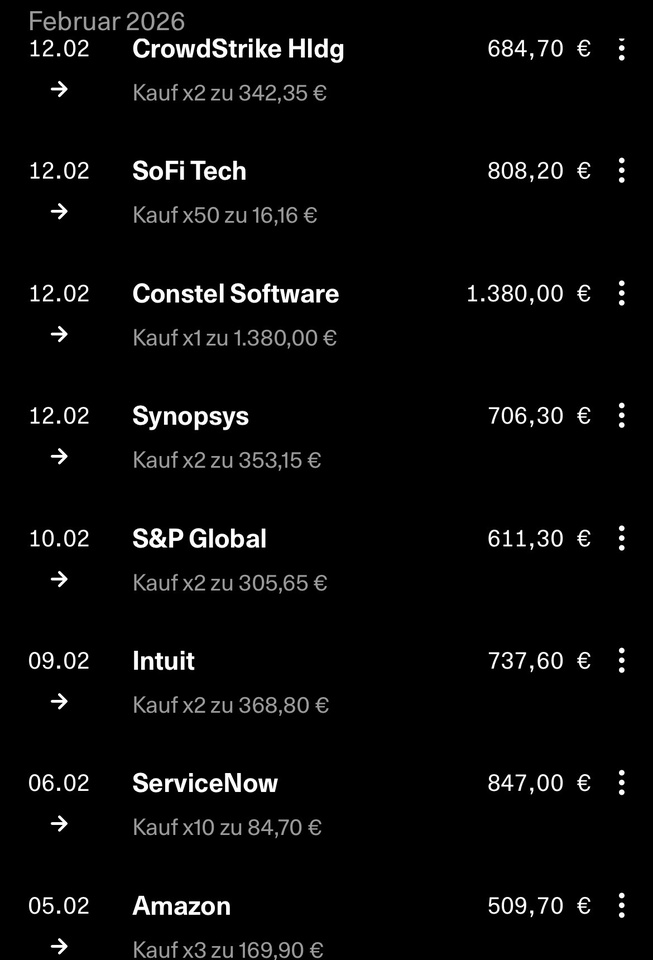

FEBRUARY PURCHASES

$NOW (+2,74 %)

$INTU (+1,74 %)

$SPGI (+0,31 %)

$SNPS (+1,22 %)

$CSU (-0,99 %)

$SOFI

$CRWD (+1,97 %)

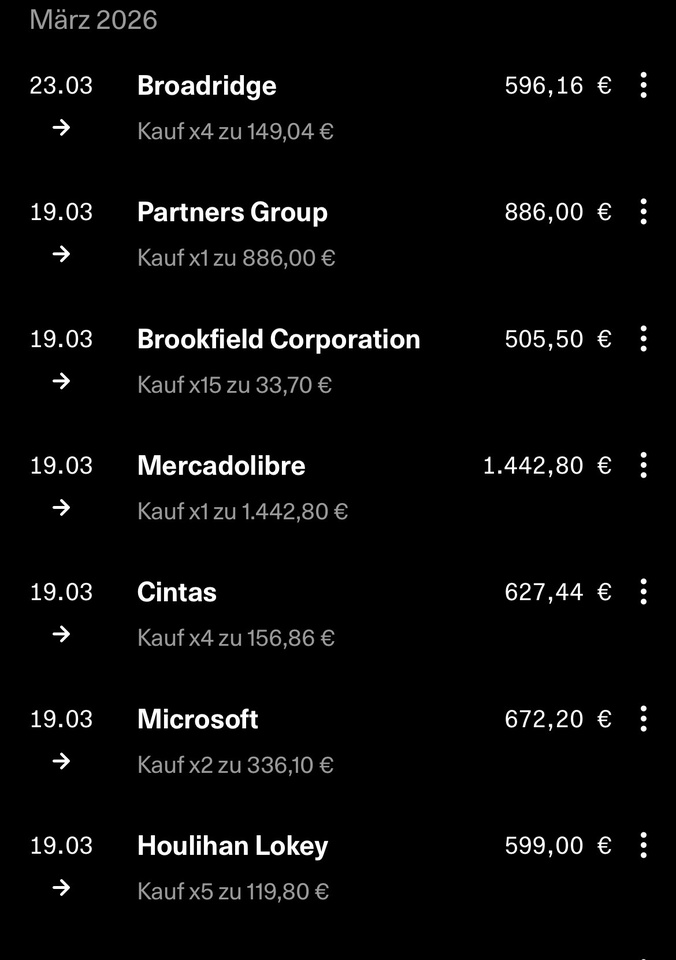

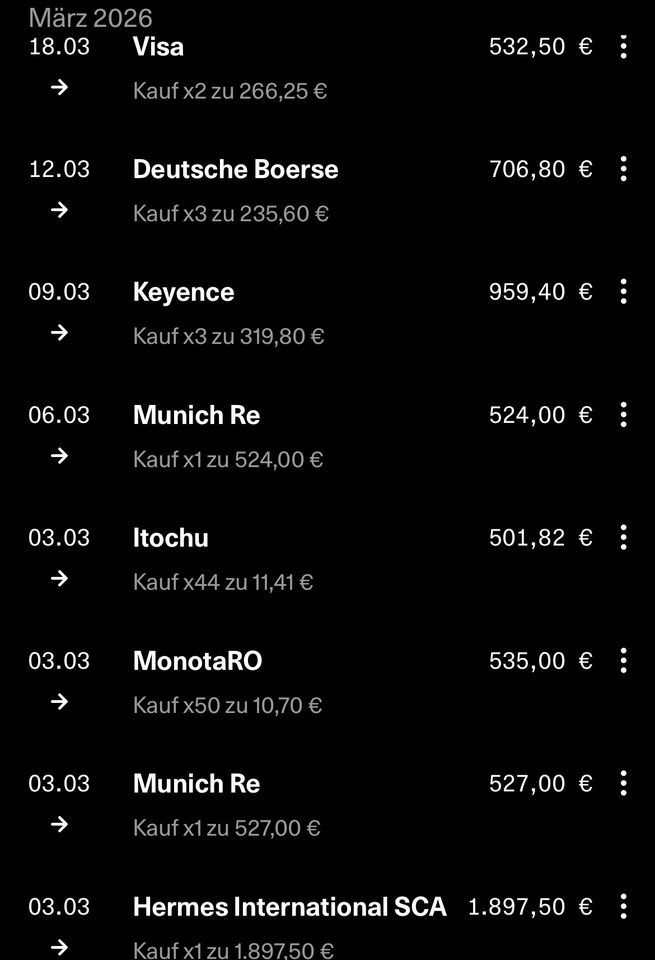

MARCH PURCHASES

$MUV2 (+1,51 %)

$3064

$8001 (+1,6 %)

$6861 (+2,8 %)

$DB1 (+1,12 %)

$V

$HLI (+0,97 %)

$MSFT (+1,33 %)

$CTAS (-0,31 %)

$MELI (+0,59 %)

$BN (+0,74 %)

$PGHN (+0,8 %)

$BR (-0,8 %)

Due to the global political situation - especially because of this 🍊 in the White House, whose tweets cause more tsunamis 🌊than real natural disasters - and the current drawdown in the S&P 500 (which is very convenient for me right now and gives me a lot of pleasure 🤩), I am accordingly under water💦🫧 with some of my purchases so far.

but hey, we're investing for the long term, aren't we? So easy going, all relaxed 🥱 I will most likely not make any more purchases in the next few days or weeks, park my cash position elsewhere or put it in overnight money and wait and see which zone the market settles in or wait for it to stabilize.

What do you have on your watchlist?

Are you currently waiting or how are you dealing with the current situation?

@Get_Rich_or_Die_Tryin

@Tenbagger2024

@Max095 and of course all other members

Ok, that's enough now 😂

that's it from me for now ✌️

your stock master

I am currently fully invested in Amazon, Microsoft, ServiceNow and Alphabet and am gradually increasing my positions. My budget doesn't allow for more at the moment, so I'm focusing on the top stocks.

Titres populaires

Meilleurs créateurs cette semaine