$MC (+2.51%)

$MBG (+3.08%)

$ULVR (+0.89%)

$PYPL (+1.09%)

$NBIS (-1.8%)

$SPGI (+0.71%)

$UPS (+0.18%)

$KO (-0.31%)

$GLW (+0.01%)

$BA (+1.89%)

$KER (+0.81%)

$ENPH (+0.42%)

$NXPI (-2.08%)

$STX (-2.99%)

$BE (-4.29%)

$V (+1.16%)

$MDLZ (+0.26%)

$000660

$P911 (+3.12%)

$BN (-0.38%)

$RMS (+3.14%)

$BAS (+1.16%)

$AG1 (-0.48%)

$LMND (+0.73%)

$SOFI (+1.1%)

$NDX1 (-0.64%)

$TER (-2.54%)

$GD (+0.57%)

$APH (-0.86%)

$AIR (+1.77%)

$SBUX (+1.19%)

$CMG (+0.31%)

$META (+2.17%)

$FTNT (+1.94%)

$QCOM (-0.67%)

$LRCX (-2.12%)

$HOOD (+0.25%)

$ARM (-1.82%)

$MSFT (+2.09%)

$CVNA (+1.92%)

$005930

$SU (-1.33%)

$INGA (-1.11%)

$OR (+1.01%)

$BMW (+2.24%)

$BATS (-0.34%)

$MA (+0.18%)

$ADS (+4.62%)

$SHEL (-1.4%)

$RACE (+1.73%)

$RDDT (+1.23%)

$TEM (+0.26%)

$COIN (-1.48%)

$AAPL (+0.81%)

$AMZN (+2.14%)

$CCO (+0.86%)

$LIN (+1.4%)

$ABBV (+0.87%)

$PUM (+2.54%)

$HAG (+6.65%)

$XOM (-2.39%)

$CVX (-1.38%)

- Markets

- Stocks

- HENSOLDT AG

- Forum Discussion

HENSOLDT AG

Price

Discussion about HAG

Posts

82Quarterly Results: July 27–July 31, 26

Hensoldt Stock, July 2026: Record Orders, Plummeting Share Price — When Will the Trend Reverse?

Hensoldt posts record results—yet its stock price is plummeting. Order intake has doubled, and the order book is at a historic high of 9.8 billion EUR—and yet the stock is trading 38% below its all-time high. When will the trend reverse? The company reported the strongest quarterly start in its history for Q1 2026 — while the F126 frigate shock has dragged down the entire German defense sector. Executive Board member Oliver Dörre most recently purchased company shares on June 29—a signal that investors should take seriously. Hensoldt builds the eyes and ears of all modern weapons systems—regardless of which manufacturer wins the vehicle contract.

Key points:

- Q1 2026: Order intake up 112% to 1.483 billion EUR—strongest quarterly start in history

- Order backlog: EUR 9.8 billion (all-time high) — book-to-bill ratio of 3.0

- Revenue Q1 2026: +25% YoY — EBITDA margin +90 basis points to approx. 19%

- Share price: approx. 71 EUR — −38% from all-time high (117.70 EUR, October 2025)

- Insider purchase: Executive Board member Oliver Dörre purchased company shares on June 29, 2026

- Analysts’ average price target: 84–90 EUR — up to 27% upside potential

Would this $HAG (+6.65%) already a buy for you?

Armaments check: Which player belongs in the depot? 🛡️

Which stock is your favorite? 🛡️✈️

The sector remains extremely in focus due to the ongoing geopolitical dynamics and rising European defense budgets. But where do you currently see the best risk/reward ratio?

#armament #rheinmetall #hensoldt #leonardo #shares #invest #portfolio

Armor values

All German defense stocks have just fallen quite sharply.

Do you think now would be a good time to get in or is the hype already completely over?

In the short term, however, I am not quite so bullish. You are buying into a falling knife.

If you want to play it safe, you could trade via a savings plan or in tranches.

What happened today?

$HAG (+6.65%) but $RHM (+2.94%) and $R3NK (+1.46%) have not risen that much. I haven't found any news either except that Blackrock seems to have bought shares.

Poland is against arms loan

The EU wants to support its member states with arms loans. Poland's nationalist President Karol Nawrocki sees this as a threat to Poland's sovereignty.

The law in question had previously been passed by Prime Minister Donald Tusk's centre-left coalition and was intended to allow Poland to take out loans of 44 billion euros from the EU to modernize and arm its military.

As part of the so-called Safe Program (Security Action for Europe), the EU is offering low-cost loans totalling 150 billion euros to its member states to help them finance increased arms spending in order to arm themselves against a more aggressive Russia.

The SAFE program in Poland becomes a symbol of the conflict between the government camp and the president.

What does this mean for the arms industry?

How do you see the veto?

So long

🌍 Middle East escalation moves the markets - capital flees to security & defense

The military escalation between the USA, Israel and Iran is causing strong market movements worldwide. Investors are shifting out of cyclical sectors and into security, energy and defense.

_________________________

Bitcoin $BTC (-1.36%) shows surprising stability

- 📈 In the meantime +8,1 %

- 💰 Just over 70,000 dollars

- Stabilization at around 69,000 dollars

Despite geopolitical risks, Bitcoin is apparently being used as a liquidity parking lot in the short term. At the same time, volatility remains high - further escalations could trigger new spikes.

_________________________

🛢 Oil prices up significantly

- Brent: + just under 6 %

- WTI: + a good 5 %

- In the meantime even +13 %

According to the report, the USA is currently no release from the strategic oil reserve. The market is still considered to be supplied, but the situation remains tense.

_________________________

🏦 Banks under pressure

The European banking index loses around 3,5 % - sharpest decline since April 2025.

Particularly affected:

- HSBC - $HSBA (+0.22%)

- Barclays - $BARC (+0.51%)

- Standard Chartered - $STAN (-0.17%)

- Deutsche Bank - $DBK (+1.26%)

- BNP Paribas - $BNP (+1.14%)

- BBVA - $BBVA (+0.88%)

- Commerzbank - $CBK (+2.52%)

In the USA also weaker until the US opening:

- Bank of America - $BAC (+1.13%)

- Citigroup - $C (+0.03%)

Reason: Strong Middle East business of many institutions and general risk aversion of investors.

_________________________

✈️ Travel industry collapses

High oil prices and uncertainty weigh heavily on tourism stocks:

- TUI - $TUI1 (+3.59%) (-11 %)

- Lufthansa - $LHA (+1.51%) (-11 %)

Flights to the region are canceled, travel offers suspended. Investors fear rising costs and falling booking figures.

_________________________

💎 Luxury stocks clearly in the red

The European luxury index loses almost 4 %.

Strongly affected:

- Richemont - $CFR (+1.2%)

- Swatch - $UHR (+0.03%)

- LVMH - $MC (+2.51%)

- Hermès - $RMS (+3.14%)

- Kering - $KER (+0.81%)

- Brunello Cucinelli - $BC (+4.75%)

- Moncler - $MONC (+2.81%)

- Ferragamo - $SFER (+0%)

Background:

Luxury is heavily dependent on global travel. Capital flows out of cyclical stocks.

_________________________

🛡 Defense stocks as clear winners

Geopolitical tensions drive up defense stocks:

- BAE Systems - $BA. (+0.81%)

- Lockheed Martin - $LMT (+1.77%)

- RTX - $RTX (+1.09%)

- Kratos - $KTOS (+1.38%)

- Hensoldt - $HAG (+6.65%)

- Leonardo - $LDO (-0.79%)

- Renk - $R3NK (+1.46%)

- Rheinmetall - $RHM (+2.94%)

Partial price increases of 3-6 %.

The focus is particularly on missile defense systems and possible increases in defense budgets.

_________________________

🚢 Shipping companies benefit

Transport values increase due to detour (avoidance of Hormuz, Suez Canal & Bab al-Mandab):

- Maersk - $MAERSK A (-0.49%)

- Hapag-Lloyd - $HLAG (+0.28%)

- Torm - $TRMD A (-0.19%)

- Frontline - $FRO (+1.87%)

- Hoegh Autoliners $HAUTO (+0.75%)

Reason: Shortage of transport capacity and speculation on rising freight rates.

_________________________

🥇 Gold in demand

- Gold price: +2,5 %

Profiteers in mining stocks:

- Evolution Mining - $EVN (+1.47%)

- Northern Star - $NST (+0.1%)

The sector has been showing relative strength for several days.

$4GLD (+0.01%)

$GOLD

$GOLD (+2.15%)

_________________________

📊 Market logic clearly recognizable

Winner:

🛡 Armaments

🚢 Shipping companies

🥇 Gold

₿ Bitcoin (short-term)

Losers:

🏦 Banks

✈️ Travel

💎 Luxury

_________________________

🔎 Conclusion

The market reaction follows the classic pattern of geopolitical crises:

- Risk is reduced

- Capital seeks security

- Energy prices rise

- Defense stocks benefit

The decisive factor remains whether the situation eases diplomatically - or escalates further.

_________________________

Source:

Reuters: Anleger greifen bei Bitcoin als "Fluchtvehikel" zu (Via TradingView)

Record volume of orders and down it goes

$HAG (+6.65%) actually published great figures yesterday. Sales growth +10% to € 2.46 billion (only slightly below analysts' estimate of € 2.5 billion).

Incoming orders are at a record level of € 4.71 billion, i.e. twice the annual turnover. A plus of 62%. And this is where the stock market is probably taking a closer look, because despite planning certainty, bottlenecks in personnel and electronic components are causing worries when it comes to processing.

For me, this is still a great stock to hold and watch. Margin also strong at +0.3% to 18.4%.

Dividend increases by 10%. I continue to hold and am not worried by the short-term sell-off (6% today). I may also buy more when cash becomes available.

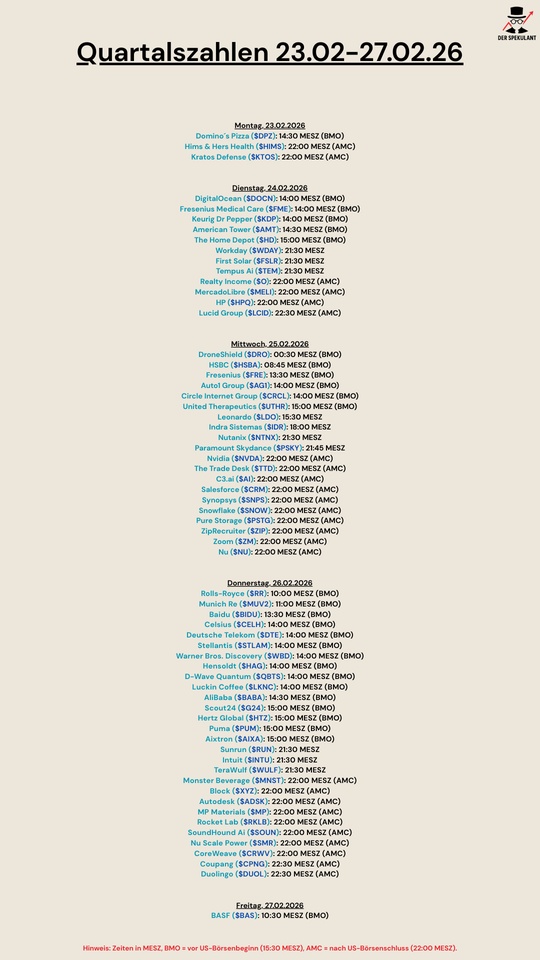

Quartalszahlen 23.02-27.02.2026

$DPZ (-0.17%)

$HIMS (+0.42%)

$KTOS (+1.38%)

$DOCN (-2.06%)

$FME (+0.64%)

$KDP (+0.04%)

$AMT (-0.15%)

$HD (+0.82%)

$WDAY (+7.09%)

$FSLR (+3%)

$TEM (+0.26%)

$O (-0.04%)

$MELI (+1.16%)

$HPQ (+1.49%)

$LCID (+0.47%)

$DRO (+8.47%)

$HSBA (+0.22%)

$FRE (+0.66%)

$AG1 (-0.48%)

$CRCL (-4.95%)

$UTHR (+0.24%)

$LDO (-0.79%)

$IDR (+2.67%)

$NTNX (+1.75%)

$PARA (+1.71%)

$NVDA (-0.65%)

$TTD (+2.14%)

$AI (+2.07%)

$CRM (+3.53%)

$SNPS (+2.3%)

$SNOW (+3.35%)

$PSTG (-1.37%)

$ZIP (+0.76%)

$ZM (+1.82%)

$NU (+0.72%)

$RR. (+2.44%)

$MUV2 (-0.02%)

$BIDU (+0.57%)

$CELH

$DTE (+4.02%)

$STLAM (+1.33%)

$WBD (+0.51%)

$HAG (+6.65%)

$QBTS (+1.22%)

$LKNCY (+1.34%)

$BABA (+3.68%)

$G24 (+0.8%)

$HTZ (+0.07%)

$PUM (+2.54%)

$AIXA (-1.29%)

$RUN (+1.24%)

$INTU (+3.21%)

$WULF (-1.88%)

$MNST (+0.53%)

$SQ (+0.92%)

$ADSK (+2.58%)

$MP (+0.49%)

$RKLB (-0.09%)

$SOUN

$SMR

$CRWV (+0.23%)

$CPNG (+0.6%)

$DUOL

Hensoldt receives orders from KNDS for digital tank optronics

$HAG (+6.65%) Hensoldt has received orders from KNDS to equip combat and infantry fighting vehicles with digital optronics. The MDAX company put the total volume at more than 400 million euros. The focus is on an order worth around 290 million euros to equip the Schakal wheeled infantry fighting vehicle. In addition, Hensoldt is to equip the Leopard 2 A8 main battle tank with digital vision systems. According to further information, this order has a volume of more than 110 million euros.

Trending Securities

Top creators this week