I had 15 shares of $JNJ (-1,28 %) , but now I own 10.

I have a lot of confidence in JNJ for stable dividends, but I was up 73% and had set myself a target of taking some profit at 70%.

It feels to get realist profits.

I also have more cash on the sidelines until the end of the month. After three months of vacation with no income, I felt uneasy having no cash available. Now I feel more comfortable again, that’s why I’m investing!

I am looking for more energy stock like $TTE (+2,83 %)

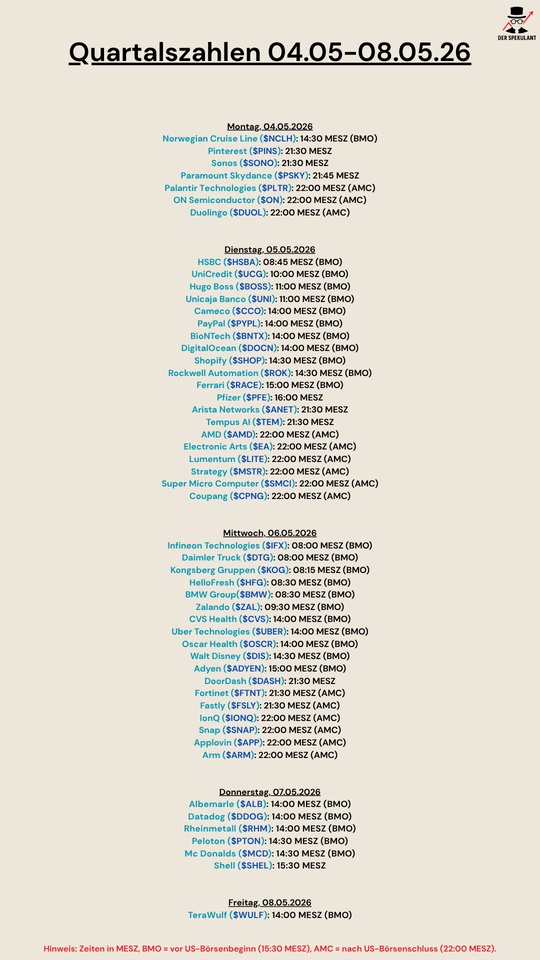

$SHEL (+1,85 %)

$NEE (-2,13 %) . All the AI needs energy !

Are there any energy companies you would recommend?

Cheers,

Daan