$MC (+0,2 %)

$MBG (-1,23 %)

$ULVR (-1,03 %)

$PYPL (+2,71 %)

$NBIS (-10,18 %)

$SPGI (-0,9 %)

$UPS (-3,91 %)

$KO (+0,03 %)

$GLW (+1,22 %)

$BA (-3,06 %)

$KER (+1,05 %)

$ENPH (+1,99 %)

$NXPI (+1,07 %)

$STX (+5,08 %)

$BE (+0,25 %)

$V (+0,44 %)

$MDLZ (+0,5 %)

$000660

$P911 (-0,91 %)

$BN (+0,22 %)

$RMS (+4,79 %)

$BAS (+0,73 %)

$AG1 (-5,01 %)

$LMND (-0,4 %)

$SOFI (-0,26 %)

$NDX1 (+2,59 %)

$TER (-1,47 %)

$GD (+0,96 %)

$APH (-1,85 %)

$AIR (-0,71 %)

$SBUX (-0,95 %)

$CMG (-2,26 %)

$META (+0,05 %)

$FTNT (-2,13 %)

$QCOM (+2,39 %)

$LRCX (-1,33 %)

$HOOD (-1,56 %)

$ARM (+5,02 %)

$MSFT (+2,67 %)

$CVNA (-1,55 %)

$005930

$SU (-0,54 %)

$INGA (+0,12 %)

$OR (+0 %)

$BMW (-1,46 %)

$BATS (-0,29 %)

$MA (+1,39 %)

$ADS (+1,11 %)

$SHEL (+2,06 %)

$RACE (+0,35 %)

$RDDT (-1,5 %)

$TEM (-0,22 %)

$COIN (-2,18 %)

$AAPL (+0,27 %)

$AMZN (-0,12 %)

$CCO (-0,43 %)

$LIN (-0,35 %)

$ABBV (-0,7 %)

$PUM (+1,33 %)

$HAG (+3,24 %)

$XOM (+2,16 %)

$CVX (+1,68 %)

BASF

Price

Discussion sur BAS

Postes

308Quarterly Results: July 27–July 31, 26

Top News Stories from the Past Week

As we do every Sunday, here are the top news stories from the past week.

Monday:

Politically explosive developments on the supervisory board of $VOW (-0,55 %) VW. Shareholder Qatar is blocking the sale of VW plants to an Israeli defense contractor, which could use them to manufacture parts for the Iron Dome. The German federal government itself uses the Iron Dome as part of its defense strategy.

Tuesday:

Weak figures from $IBM (-0,42 %) IBM are dragging the entire software sector down. Revenue fell significantly short of expectations. In particular, anticipated software investments appear to have failed to materialize.

Wednesday:

$BAS (+0,73 %) BASF raises its forecast, but the stock still falls. This is primarily due to the outlook for the second half of the year, in which BASF continues to see risks. In Q2, revenue rose by 16%. The earnings forecast was raised to a range of 6.9–7.7 billion euros.

https://www.deraktionaer.de/artikel/aktien/basf-hebt-prognose-an-aktie-sinkt-dennoch-20404774.html

Friday:

The inflation rate in the eurozone fell to 2.8% in June. Nevertheless, inflation remains well above 2.0%. The ECB is therefore caught in a dilemma between inflation and growth concerns. The next interest rate decision is due in just six weeks.

Trump wants to sell faster access to his posts on Truth Social. The reason is that his posts often move the markets. To put it bluntly, one could say Trump now wants to bring insider trading to market maturity.

Is BASF Heading for a Mega-IPO? Could the Agricultural Division Soon Be Worth More Than Half the Company?

Following the previously reported sale of the coatings business of $BAS (+0,73 %) it appears that the restructuring is continuing to move forward. Financial circles are currently speculating about a valuation of the $BAS (+0,73 %)agricultural division ranging from 20 to 30 billion euros. What is remarkable about this is that $BAS (+0,73 %) the company as a whole is currently valued at only about 45 to 50 billion euros on the stock market. In other words: A business unit that makes up only a portion of the conglomerate could, on its own, be worth nearly half of the current market capitalization.

In my view, this highlights a problem that many large conglomerates face. The stock market often applies a valuation discount (conglomerate discount) to them. Different business segments with varying growth profiles are often valued lower under one umbrella than they would be as standalone companies. This very point was discussed in the latest Handelsblatt podcast. An independently listed agricultural business could therefore command a significantly higher valuation multiple than it would within the $BAS (+0,73 %)group.

Of course, there are also risks. The agricultural division is one of the faster-growing and higher-margin segments of $BAS (+0,73 %) . A partial spin-off could lead to the remaining group being perceived as more cyclical. At the same time, $BAS (+0,73 %) the IPO would bring in fresh capital, while the group would remain the majority shareholder and thus continue to participate in the agricultural division’s future performance. It is precisely this mix of value unlocking and further upside that makes the move interesting, in my view.

Many are also wondering whether existing $BAS (+0,73 %)shareholders will automatically receive shares in the new company. As things stand, that is not planned. $BAS (+0,73 %) The group is planning a partial IPO, will remain the majority shareholder, and has not yet announced any allocation of shares to existing $BAS (+0,73 %)shareholders. Anyone wishing to invest later would likely have to purchase the new shares on the open market.

Personally, I view the planned IPO rather positively so far. If it $BAS (+0,73 %) succeed in reducing the group’s valuation discount while remaining the majority shareholder of an agricultural company valued higher on its own, this could also benefit us $BAS (+0,73 %)shareholders in the long run.

What do you think? Is the group divesting itself of one of its most attractive business units, or do we see a clever move here in the form of an IPO that could lead to a revaluation of both the individual division and the group as a whole?

~ Not investment advice ~

𝐁𝐀𝐒𝐅: 𝐒𝐭𝐚𝐫𝐤𝐞𝐬 𝐐𝟐, 𝐄𝐫𝐠𝐞𝐛𝐧𝐢𝐬𝐚𝐮𝐬𝐛𝐥𝐢𝐜𝐤 𝐟𝐮̈𝐫 𝟐𝟎𝟐𝟔 𝐚𝐧𝐠𝐞𝐡𝐨𝐛𝐞𝐧

📊 𝐄𝐫𝐠𝐞𝐛𝐧𝐢𝐬𝐬𝐞

• Revenue: €17.2B (+16%, consensus: €16.5B)

• EBITDA before special items: €2.4B (consensus: €2.1B, prior year: €1.6B)

• EBIT before special items: €1.5B (consensus: €1.1B, prior year: €0.7B)

• Net income: €4.1B (consensus: €2.4B, prior year: €79M)

• Free cash flow: -€0.2B (vs. +€0.5B)

⠀

🎯 𝐀𝐮𝐬𝐛𝐥𝐢𝐜𝐤

• EBITDA before special items now expected to be €6.9B–€7.7B (previously: €6.2B–€7.0B)

• Free cash flow still expected to be €1.5B–€2.3B

⠀

📌 Key Points

• Earnings significantly exceed analyst consensus

• Higher prices and sales volumes drive revenue growth

• Gain on disposal from the Coatings transaction contributes significantly to consolidated earnings

• Free cash flow impacted by higher capital tied up due to increased raw material prices

BASF is selling its Coatings division—what does that mean for us shareholders?

With the completion of the sale of the Coatings division to the new company Surventis, $BAS (+0,73 %) an important step in the “Winning Ways” strategy. $BAS (+0,73 %) It will receive approximately €5.8 billion in cash, while retaining a 40% stake in Surventis. This means the Group is not completely divesting itself of a profitable business but will continue to participate in its future value growth.

In my view, that is precisely the interesting part of the deal. $BAS (+0,73 %) It will be able to focus more strongly on its core business in the future, while simultaneously freeing up capital and still retaining the opportunity to benefit from Surventis’s successful development. Should the company continue to gain value under the new ownership structure, $BAS (+0,73 %) continue to benefit through the 40% stake.

For us shareholders, the key question now will be how $BAS (+0,73 %) the company uses the freed-up funds. Possible options include further debt reduction, investments in the core business, or additional capital returns. In any case, the ongoing share buyback program through 2028 gains additional potential financial flexibility thanks to the inflow of funds.

I therefore view the deal positively overall: $BAS (+0,73 %) it simplifies the group’s structure, strengthens the balance sheet, and at the same time keeps a foot in the door in case Surventis continues to gain value in the coming years.

How do you assess this move? Is it a successful allocation of capital, or would you have preferred a complete sale?

https://www.basf.com/cn/en/media/news-releases/asia-pacific/2026/07/apac-26-74

~ Not investment advice ~

Podcast episode 146 "Buy High. Sell Low." Nvidia, Hims & Hers, Take Two / GTA 6, Duolingo, Thyssen, BASF

After 20 minutes the video quality improves. Adobe Studio has apparently failed.

YouTube

https://openyoutu.be/rbWcp0BNRK4

Spotify

https://open.spotify.com/episode/6bgZMA0uhfaIkUUcXeP8ed?si=x6H_k9L_Qb2pVzXgMGxuZg

Apple Podcast

$NVDA (-0,21 %)

$HIMS (-5,65 %)

$DUOL

$BAS (+0,73 %)

$TKA (+0,06 %)

$TTWO (-0,78 %)

BASF under pressure - sales weak, profits stabilized

$BAS (+0,73 %) presented its quarterly figures and delivered a mixed but slightly better than expected picture overall.

- Turnover (expected): EUR 15.76 billion

- Turnover (reported): EUR 16.02 billion

- EPS (expected): EUR 1.06

- EPS (reported): EUR 1.32

The reported figures were therefore slightly above expectations, while profit was also more stable than feared. Operationally, however, the picture remains challenging. Sales are down slightly year-on-year, mainly due to falling prices and negative currency effects, while sales volumes were even stable to slightly higher in some cases. This clearly shows that the problem currently lies less on the demand side than primarily in price pressure and the weak industrial environment. At the same time $BAS (+0,73 %) At the same time, we were able to stabilize profits thanks to income from investments and internal efficiency measures, among other things, which will provide relief at least in the short term. Overall, the quarter thus confirms the company's current transition phase. The operating basis is in place, but margins remain under pressure. This is particularly evident in the development of the chemicals segments, which are heavily dependent on energy and raw material costs as well as global industrial demand.

In this context, the role of $BAS (+0,73 %) as an early indicator of economic development, particularly in Germany. The chemical industry is at the beginning of many value chains, which is why rising demand is often the first sign of an economic recovery. At present, however, only cautious signs of stabilization can be seen here. The slight increase in volumes suggests that industrial demand is not collapsing any further, but there is still no sign of a clear, broad-based recovery. On the contrary, the continuing price pressure shows that the environment remains weak and that companies have not yet regained their pricing power.

For me, the decisive factor in the coming quarters will be whether $BAS (+0,73 %) whether it will be possible to stabilize the ongoing price pressure and at the same time benefit from a possible recovery in industrial demand (particularly in China). Equally important for me is the extent to which the ongoing cost and restructuring programs actually have an impact on profitability. In my opinion, the development of energy prices will also continue to play a key role. Overall, the big question for me remains whether this is already the start of a cyclical recovery in the chemical sector or whether we are only seeing a short-term stabilization in a persistently difficult environment.

~ No investment advice ~

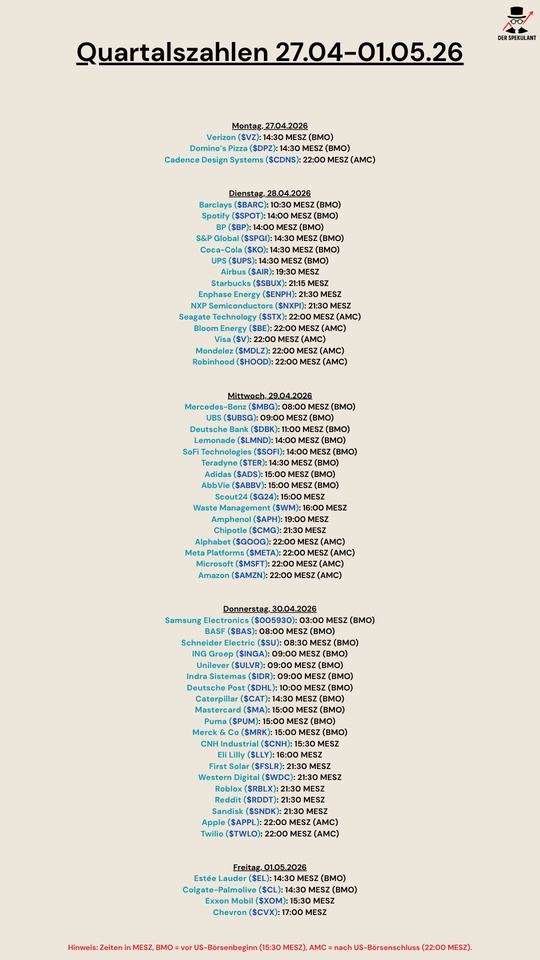

Quarterly figures 27.04-01.05.26

$VZ (+1,5 %)

$DPZ (-1,26 %)

$CDNS (+0,65 %)

$BARC (-1 %)

$SPOT (-0,54 %)

$BP. (+2,27 %)

$SPGI (-0,9 %)

$KO (+0,03 %)

$UPS (-3,91 %)

$AIR (-0,71 %)

$SBUX (-0,95 %)

$ENPH (+1,99 %)

$NXPI (+1,07 %)

$STX (+5,08 %)

$BE (+0,25 %)

$V (+0,44 %)

$MDLZ (+0,5 %)

$HOOD (-1,56 %)

$MBG (-1,23 %)

$UBSG (-1,26 %)

$DBK (-0,58 %)

$LMND (-0,4 %)

$SOFI (-0,26 %)

$TER (-1,47 %)

$ADS (+1,11 %)

$ABBV (-0,7 %)

$G24 (-5,54 %)

$WM (+2,31 %)

$APH (-1,85 %)

$CMG (-2,26 %)

$GOOG (-0,78 %)

$META (+0,05 %)

$MSFT (+2,67 %)

$AMZN (-0,12 %)

$005930

$BAS (+0,73 %)

$SU (-0,54 %)

$INGA (+0,12 %)

$ULVR (-1,03 %)

$IDR (+0,33 %)

$DHL (-0,29 %)

$CAT (-1,61 %)

$MA (+1,39 %)

$PUM (+1,33 %)

$MRK (+0,17 %)

$CNHI (+0,75 %)

$LLY (+2,47 %)

$FSLR (+3,65 %)

$WDC (-2,09 %)

$RBLX (+0,64 %)

$RDDT (-1,5 %)

$SNDK (-1,78 %)

$AAPL (+0,27 %)

$TWLO (+17,15 %)

$EL (-2 %)

$CL (-0,09 %)

$XOM (+2,16 %)

$CVX (+1,68 %)

Mercedes could hurt...

Strong dividend season ahead💶

15 increases

13 unchanged

7 reductions

Insurance companies

Banks

Utilities

Car stocks

Type here if you like collecting dividends: https://shorturl.at/83W8R

$MBG (-1,23 %)

$ALV (+0,95 %)

$VOW3 (-1,31 %)

$MUV2 (+1,18 %)

$BMW (-1,46 %)

$AIR (-0,71 %)

$CBK (-1,73 %)

$523232

$DTG (+0,4 %)

$DHL (-0,29 %)

$FME (+1,33 %)

$FRE (+0,59 %)

$HNR1 (+1,29 %)

$MTX (-1,77 %)

$RHM (-4,99 %)

$SAP (+1,35 %)

$ENR (+1,53 %)

$BAS (+0,73 %)

$BAYN (-0,33 %)

$BEI (-0,07 %)

$DBK (-0,58 %)

$DTE (+6,04 %)

$EOAN (+0,33 %)

$GEA (-0,66 %)

$IFX (-0,97 %)

$RWE (+1,68 %)

$SY1 (+0,02 %)

$ZAL (+2,5 %)

$ADS (+1,11 %)

$BNR (+2,44 %)

$HEN (+2,52 %)

$MRK (+0,17 %)

$SIE (-4,52 %)

$SHL (-0,33 %)

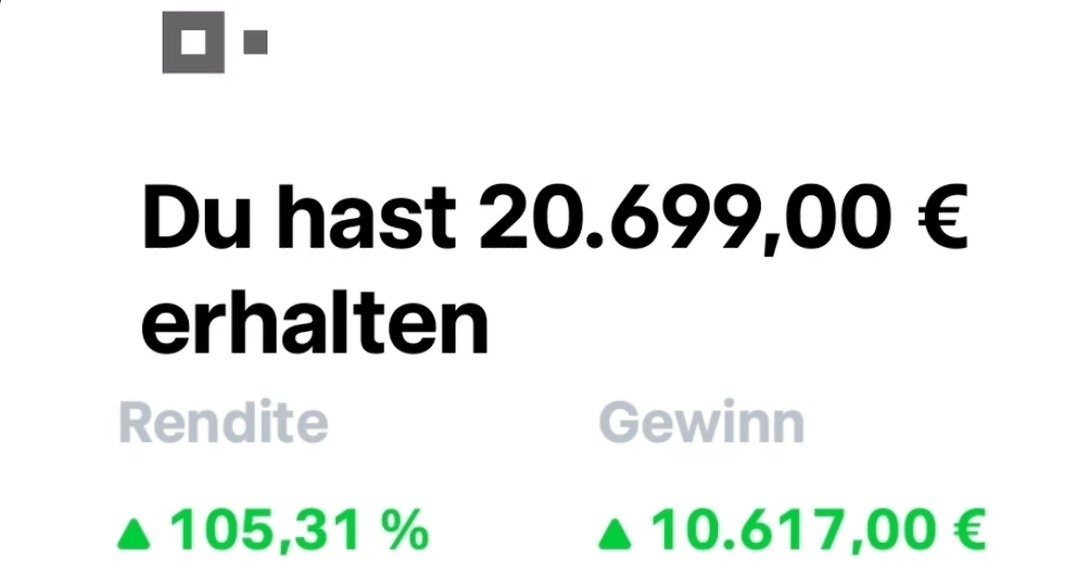

Sale of BASF warrant SU9LGD with +105% / + 10.600€ on 27.03.

four months after the follow-up purchase. New subsidies, tax cuts and a good forecast have brought the share close to a 52-week high. I am now securing profits before there is a possible gas emergency in Germany in April. The Federal Network Agency is preparing to declare an "alert level" (stage 2 of the gas emergency plan). From April, the first cuts could be made for large industrial consumers in order to ensure that storage is filled for the next winter despite the import ban. BASF would be affected as it requires a minimum load (often around 50%) for its complex chemical Verbund sites. If the allocation falls below this, there is a risk of irreparable damage to the plants. It has been a long time since I traded a German share. $BAS (+0,73 %)

Titres populaires

Meilleurs créateurs cette semaine