$XDEM (+2,77%)

$XDEV (+1,59%)

$WSML (+1,42%)

$CSPX (+1,82%)

$IWDA (+1,58%)

Xtrackers MSCI World Momentum ETF

ETP

ETP

ISIN: IE00BL25JP72

Ticker: XDEM

IE00BL25JP72

XDEM

Price

Discussão sobre XDEM

Postos

27

1Mês·

Simple but maybe brilliant investing idea

I bought $MU (+8,03%) at 65 € per stock and I’m still holding. When I bought the stock, it was the most undervaluaded stock in the $XDEV (+1,59%) and it’s still like this ! Meanwhile something straordinary happened. Now MU it’s also in the first seat of $XDEM (+2,77%) . The best value investors understand that it is not enough to buy a stock simply because it is undervalued. You also need to identify companies that the market is likely to become interested in over time. In other words, the goal is to buy stocks that are both cheap and gaining attention.

My idea is to buy stocks that rank highly in both value and momentum indexes, and then sell them when they fall significantly in either ranking. The reasoning is that, if a stock drops in the value ranking, the market may have already re-priced it closer to its fair value. If it drops in the momentum ranking, it may indicate that investor interest is fading.

It would be fascinating to backtest this strategy by analyzing the historical constituents and rankings of global value and momentum indexes over the past several decades. Unfortunately, I have not been able to find historical holdings data for these indexes. Can you help me in this ?

66

1Mês·

A doubt of mine

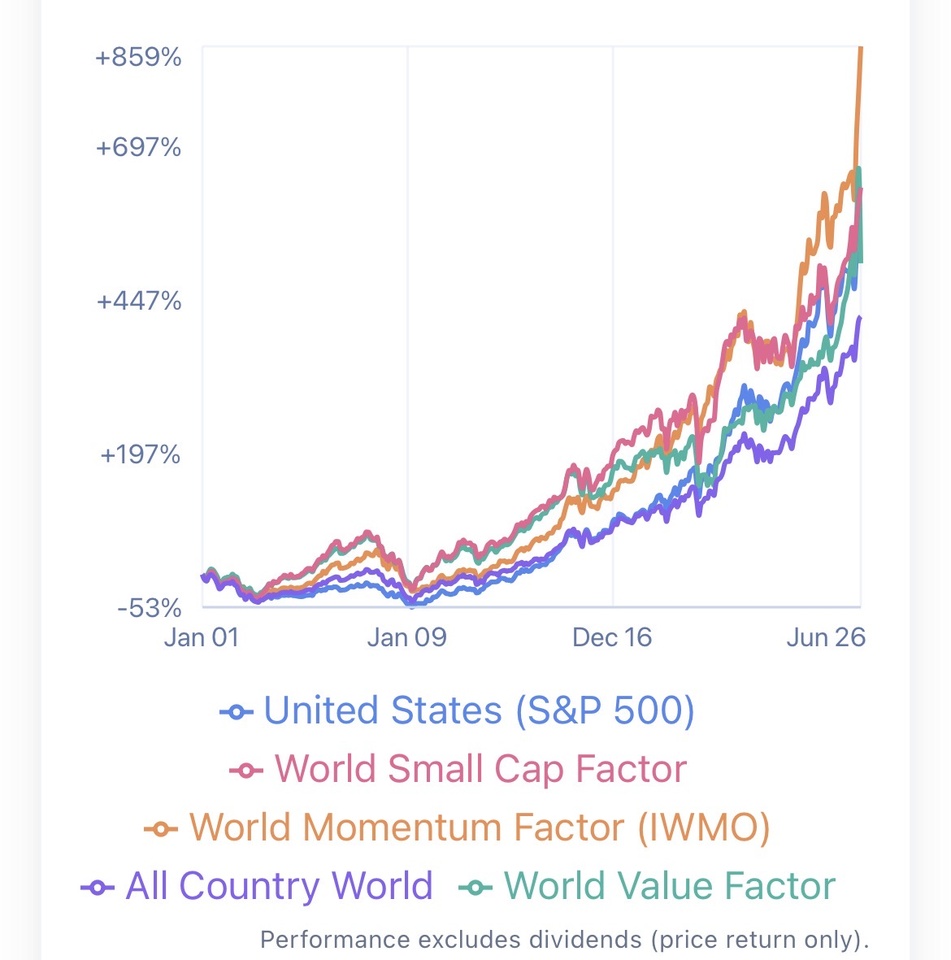

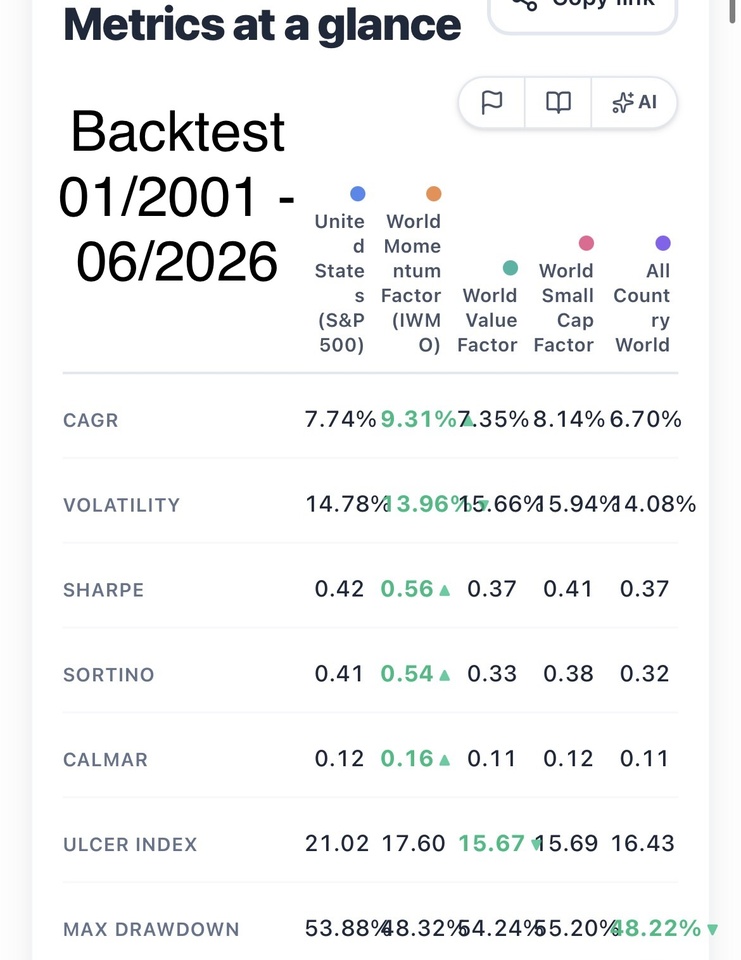

Why people keep on buying $IWDA (+1,58%) or $VWRL (+1,72%) as core of their portafolio when the following index perform way better (in fact they beat even the sp500 on a long range, meanwhile keeping global diversification and diversification from the big7).

1Mês·

MY PLAN TO LIVE OF DIVIDENDS

Hello everyone, I'm 24 y.o. my portfolio is currently worth 55-60 k eur. My plan is to save around 1000 eur per month and invest in growth product for 15-20 years. Specifically:

GLOBAL ETF (50 % allocation):

MSCI WORLD VALUE $XDEV (+1,59%)

MSCI WORLD MOMENTUM $XDEM (+2,77%)

MSCI WORLD SMALL CAP $WSML (+1,42%)

note: they all have had better return (on long range) in comparision with sp500 and ofc msci core world or ftse all word. Plus these etf offer a real diversification from having the big 7 as first positions.

GLOBAL TECH (50 % allocation):

MSCI WORLD INFORMATION TECHNOLOGY $XDWT (+3,84%)

NASDAQ 100 $XNAS (+3,17%)

note: msci world IT it's good bcs with the time it can move towards international technology stocks and not only american, meanwhile the nasdaq it has the advantage of having also companies that are not directly linked to technology but general innovation (plug power, rocketlab ecc.). BOTH ETF HAVE THE SAME RETURNS OVER THE TIME.

Once I'll reach the milestone of 1 million I'll allocate everything in these 2 etf high dividend stocks:

VanEck Morningstar Developed Markets Dividend Leaders

iShares STOXX Global Select Dividend 100

note: these etf are incredible, they have only 20 % of USA, they are super diversified all around the world + no tech sector present (that is usually speculative, volatile and where bubbles can be more likely to happen). Only big worldwide companies that offers high dividend and are super stable.

BE READY FOR IT:

avarage dividend annually: 4.5 %

avarage growth annualy: 8 %

it means that you start to take 45 k (before tax) annually in dividends + your capital of 1 million is growthing at 8 % rate and doing composite interest over the years. Each year your dividend passive income increase and your capital too. If there is a finacial crises ? well for sure these etf will loose way more then sp500, nasdaq and other products. These companies are defensive, they have big cash flow and investors invest in them when they are afraid of the tech market or others speculative sectors.

LET ME KNOW WHAT YOU THINK ABOUT IT !!!!!

Enjoy your day and let's make it.

55

5 Comentários

In theory there is no direct connection between dividend and gained wealth.

You could just stay in your global etf plan and go for it.

Nearly the same goes for sector an Country etfs.

Still everything can go according to plan. Just brace yourself for a smaller crash when high yield stocks cut dividends in half.

You could stay in plan a) and just sell a part of your portfolio. When you need some money.

I plan to hold $XDEM $XDEV $XDEQ $ZPRV $ZPRX and $5MVL for life. Selling small parts of it when I want to spend.

That way I take a more scientific approach and don’t pay unnecessary taxes. At least for me in Germany dividends have high disadvantages anyway

You could just stay in your global etf plan and go for it.

Nearly the same goes for sector an Country etfs.

Still everything can go according to plan. Just brace yourself for a smaller crash when high yield stocks cut dividends in half.

You could stay in plan a) and just sell a part of your portfolio. When you need some money.

I plan to hold $XDEM $XDEV $XDEQ $ZPRV $ZPRX and $5MVL for life. Selling small parts of it when I want to spend.

That way I take a more scientific approach and don’t pay unnecessary taxes. At least for me in Germany dividends have high disadvantages anyway

•

22

•6Mês·

My target portfolio allocation

the idea is a sort of risk parity portfolio that could do well in good times and bad times, using leverage wisely to increase return and decrease the overall risk of the portfolio

- WisdomTree Global Efficient Core $NTSG (+1,34%) - 35%

- iShares Core MSCI World $ISWD (+2,33%) - 10%

- Xtrackers MSCI Emerging Markets $XMME (+2,48%) - 5%

- Xtrackers MSCI World Momentum $XDEM (+2,77%) - 15%

- Avantis Small Cap Value $AVWS (+1,13%) - 15%

- MGP DBi Managed Futures $DBMF - 20%

22

6Mês·

MSCI World with or without momentum?

I am trying to organize my portfolio more clearly and combine several ETFs/funds with the same investment focus, as long as taxes are not too high when I sell them. I now have the pure MSCI World ETF $LWCR (+1,51%) and at the same time the MSCI World ETF of roughly the same size with Momentum $XDEM (+2,77%) . Which of the two would you liquidate? The momentum idea is good, but if you only change stocks every 6 months, the momentum may be long gone in between and you are betting on stocks on the decline. Thank you for your help!

44

12 Comentários

•

44

•

7Mês·

Portfolio feedback

Hello everyone,

I would like to get your feedback on my portfolio strategy. Here are the key data:

Age: 20 years old

Investment horizon: Very long (several decades)

Strategy: First investment then invest via savings plan + B&H

1. the planned portfolio

I am planning the following allocation for my portfolio. Important: The 20% in the dividend ETF will only flow until my exemption order has been fully utilized by the distributions. After that, fresh money will only flow into the other two positions.

- 55% Vanguard FTSE All-World (basis) $VWCE (+1,63%)

25% Xtrackers MSCI World Momentum

$XDEM (+2,77%)

20% VanEck Developed Markets Div Lead

$TDIV (-0,25%)

2. current situation

I took advantage of the "dip" in April and am already invested (mix of ETFs and individual stocks). I am currently considering how I should adjust or structure my portfolio, as the individual stocks have performed extremely well:

- Nvidia: +60%

- Alphabet: +90%

- Others: Amazon, Meta, United Health (all up).

My questions for you:

What do you generally think of my ETF selection and weighting (55/25/20)?

Would you swap one of the ETFs for another product?

Is there anything missing in the allocation (would you add another component, e.g. small caps)?

Individual shares: How would you deal with the winners? Realize profits and shift them into the ETFs, or simply let them run as "satellites", as I am still young?

Many thanks for your feedback!

44

22 Comentários

7Mês

ETFs: I would do without the Momentum MSCI and add a gold or gold producer ETF instead.

In my opinion, these momentum ETFs are always "a bit late" and rebalance too slowly or too rarely. I would then perhaps split 60/20/20.

You can let shares run as long as you like them.

In my opinion, these momentum ETFs are always "a bit late" and rebalance too slowly or too rarely. I would then perhaps split 60/20/20.

You can let shares run as long as you like them.

••

10Mês·

Adapt to market phases

With this sale, I have liquidated virtually my entire buy and hold portion (around 50% of my investments). On the one hand to free up some powder for less expensive courses, but mainly to shift most of it into more flexible strategies that can adapt better to changing market conditions. And, as a nice side effect, usually perform better. The aim is not to miss any further rises and still avoid drawdowns if one should occur soon. According to the theory at least 🫡

22

22 Comentários

The good old market timing lol good luck you are basically gambling.

Going in and out market has been proven countless time to be a losing strategy, I don’t really understand why people still do this

Going in and out market has been proven countless time to be a losing strategy, I don’t really understand why people still do this

••

11Mês·

Deposit of a 19 year old prospective bank clerk

Hello everyone,

After more than a year, it's time to present my portfolio again, as a lot has changed.

I am clearly pursuing a buy-and-hold strategy with quality stocks. As a core I currently have the $GGRP (+1,1%)and the $IWDA (+1,58%) . The $GGRP (+1,1%) will soon leave my portfolio and half of it will be reallocated to the $IWDA and the $XDEM (+2,77%) will be reallocated. This is simply because I think it's a good idea to have an ETF in my more growth-oriented portfolio that doesn't just have dividend payers in its line-up.

I find the $XDEM (+2,77%) in particular, as it focuses exclusively on stocks that have performed well recently. The fact that the excess return naturally drives up volatility somewhat is perfectly okay, as my investment horizon is at least 20 years.

Otherwise, another 57% of my portfolio consists of individual shares. My plan has actually always been a 50/50 ratio, but this has changed somewhat due to the strong equity returns. However, the ETF positions will soon be filled with around 600 euros of my training income. This should then level out a little better, as long as shares don't continue to rise enormously.

If you take a closer look at the shares, I think the strong focus on the classic ETF drivers such as $NVDA (+2,22%) , $MSFT (+1,27%) , $GOOG (+0,54%) and $AMZN (-1,44%) stand out. Of course, the ETFs in the portfolio increase the proportion of these stocks, but that is absolutely intentional. I remain very optimistic about the AI runners and see further growth and sufficient stability in the coming years.

I always find the following particularly noteworthy $EUZ (+0,41%) . It is the only German company in my portfolio. I am very confident in the long term and am excited to see how they will develop. Unfortunately, my $MC (-0,71%) position should also be mentioned. Well, bad luck and I didn't have the courage to sell when the downward trend was clear. But at least I can now offset the taxes from the $GGRP (+1,1%)-sale by selling the LVMH position and then buying it again immediately. As soon as the luxury segment improves again, I am sure that LVMH will be back at the top of the industry.

The bottom part of my portfolio currently consists of $MCD (-0,43%) and $MDLZ (+0,48%) among others. Due to the strong returns of the other shares, these two positions have become somewhat unimportant in my portfolio. At around 2% each, they have simply become too small for me, which is why I will be merging them. However, not again in a stable share with a dividend, but rather in a growth driver. I am currently watching $ANET (+4,17%) and am pretty convinced. The restructuring will probably soon lead to a EUR 4,000 position in Arista and free up another EUR 2,000 for the ETFs.

That should be all. If you have any questions, please feel free to ask, otherwise I'm very happy to receive your feedback :)

(A little info: The sum of the deposit comes from my grandfather's inheritance. The ETF shares I bought early on were bought by my father, as I was of course too young. Then I got involved with shares and was allowed to have more and more of a say. I currently make my own decisions about the portfolio)

16Posições

€ 130.987,98

31,62%

6565

17 Comentários

11Mês

Keep up the good work! Even I or older shareholders can still learn something from you. Respect :)

•

99

•

1Ano·

Portfolio feedback for a Belgian guy !

Hey everyone! After seeing so many portfolio presentations, I decided to share mine today, following the advice of @DonkeyInvestor (link here)! 🚀

1. Investment horizon and goals

I am Belgian guy of 30 years old, already own an apartment, and have a mortgage to repay. I have been investing sporadically since I was 18, but I really started actively managing my investments in March 2024.

My main goal is to maximize my savings, with the flexibility to either buy a house in the future or allocate funds to another project. Because of this, my investment horizon is flexible but at least 5 years.

I then plan to keep investing long-term and see if this could help me achieve a certain level of financial independence. To be honest, in a rational (but admittedly a bit morbid) way, the inheritance I will receive one day could contribute to that goal—although I am not at all counting on it as a part of my strategy.

2. My strategy and how I intend to achieve my goals

A. Introduction

I already have an emergency fund covering six months of expenses, which gives me peace of mind and allows me to invest without short-term financial stress.

My job enables me to invest at save (for investment) €1,500 per month. Any bonus or additional income is either added to my investments, used to replenish my emergency fund, or allocated to vacations and other expenses.

Additionally, I have around €25,000 from selling mutual funds I purchased in my younger years. This gives me flexibility to pick individual stocks or invest in crypto when I see an opportunity.

B. Investment Strategy & Asset Allocation 🎯

I invest around €2,300 per month in a DCA approach in various ETFs. Then I invest in stock or crypto when I see an opportunity.

My goal is to build by end 2025 a portfolio with the following allocation:

- ~40% Individual Stocks (mainly large-cap growth & tech)

- ~7.5-10% Crypto (mainly Bitcoin, possibly some altcoins)

- The remaining ~50% in ETFs, diversified across different regions and themes

C. Diversification & Experimentation 🎢

Within my ETF allocation, I allow myself to include thematic or higher-risk ETFs instead of only focusing on broad market indices.

I fully understand that this approach is not the most straightforward or simplest way to invest (see point 3). However, at this stage, I want to "have fun" with investing, testing stock picking and specific ETFs. Over time, I will assess whether this was a good decision and adjust if necessary (see point 4).

D. Risk-Taking & Adaptability 🔄

Since I am still young, I am willing to take on more risk, fully aware that I could also lose money. As I gain experience and see the performance of my portfolio, I will adapt my strategy if needed (again point 4).

3. My choice for the stocks in my portfolio

A. ETFs

After experimenting with different allocations, I’ve decided to aim for the following ETF distribution by the end of 2025 (as a percentage of my total portfolio, so including stock and crypto):

- 25%$IWDA (+1,58%) → Broad exposure to developed markets.

- 5%$IEMA (+2,31%) → Exposure to emerging markets

- 5%$XDEM (+2,77%) → Performance

- 2-2.5% in $MEUD (+0,8%) & $XNAS (+3,17%) → European and Nasdaq exposure to complement my stock picks.

- 10% in Thematic ETFs → I enjoy sector-specific plays and have selec $RBOT (+2,92%) , $W1TB (+3,43%) , $LCOC (+3,54%) , $SMH (+5,24%), $DFEN (+4,82%) to get exposure to robotics, Cocoa (because why not), semiconductors, and aerospace/defense.

B. Stocks

Like most of you, I love tech 😄, so a significant part of my individual stock portfolio is centered around it. I generally invest €2,000 per stock, sometimes in one go, sometimes split across multiple entries.

- ✅ Tech Giants & AI

- $NVDA (+2,22%) (exception to my €2,000 rule)

- $AMZN (-1,44%), $GOOGL (+0,96%), $MSFT (+1,27%) – Their global impact is massive and they are solid, and I don’t see that changing anytime soon.

- $VST (-6,44%) – AI-driven energy demand is booming, and I chose Vistra Energy over other AI-linked power plays.

- ✅ European Exposure 🌍

- $ENR (+2,92%)

(Siemens Energy) – A standout performer this year in Europe, and AI is a key factor in its growth. - $NOVO B (-6,58%)

(Novo Nordisk) – The obesity epidemic is a growing concern (also in Europe), and Novo Nordisk is a leader in the space. - ✅ More Speculative Plays :

Palantir & Soundhound AI – Both are AI-related but carry higher risk. $PLTR (+14,62%) because of its massive presence in States' affairs. $SOUN is an even more speculative AI bet, but I believe in it for the voice aspects. - ✅ Employee Shares : $ENGI (-1,05%)

C. Crypto

I chose Bitcoin mainly due to its volatility and the potential for "easy profits". I initially invested in July and, seeing Trump getting closer to the White House, I decided to increase my position, anticipating potential market movements linked to his policies and the broader macroeconomic environment. For now, I’m sticking to Bitcoin but might explore XRP and other assets in the future.

4. Insight into how I plan to further expand your portfolio

Based on my calculations, I should reach €100,000 invested by late 2025 or early 2026. My plan is to keep investing consistently to get closer to the allocation I outlined earlier.

A. Expanding My Stock Portfolio 📈

I plan to maybe reinforce some existing positions but overall exploring new opportunities. Some stocks I’m considering include:

- Belgium: Syensqo, D’Ieteren

- France: Schneider Electric

- Banking sector: JP Morgan

- E-commerce & emerging markets: MercadoLibre

- Quantum computing: While highly speculative, I’m keeping an eye on this sector for the future. Since I already have exposure through Alphabet, I might consider IBM later on.

- Biotech & Medical Startups 🧬: I’ve been tempted by some early-stage medical stocks, but the extreme volatility and risk keep me hesitant. A single failed clinical trial can wipe out a stock forever, making this sector too unpredictable for me at the moment.

- I might also allow myself the occasional “easy trade”, but nothing certain yet.

- Finally, I could include new thematic ETF's.

B. Crypto

For Bitcoin, I keep things simple: I invest €100 whenever I see a dip (sometimes multiple times per day or week), staying patient and accumulating over time. I’m curious to hear your views on where Bitcoin is headed.

C. Reviewing My Strategy in Late 2025 🔍

- At the end of 2025, I’ll assess my portfolio, especially my thematic ETFs, by comparing them to the MSCI World. This will help me decide whether to stick with them or simplify my ETF strategy.

- I’ll also review my stock picks to see if any adjustments are needed.

- Given my horizon, I won’t make any rushed decisions.

D. Managing My Biggest Concern – US Exposure 🇺🇸

One of my main concerns is my heavy exposure to the US market, both through ETFs and stocks. However, given the current global economic landscape, it seems difficult to do otherwise while aiming for maximum returns.

For now, I’ll keep an eye on opportunities to diversify while ensuring that my investments remain aligned with my long-term strategy.

5. What I don’t want in my portfolio

I believe that investing inherently carries a level of amorality, especially when investing in broad-market ETFs that include a wide range of companies (but everyone has their own ethical perspective—let’s not start a debate on that! 😄).

That being said, I personally choose not to invest directly in companies involved in alcohol or tobacco. It’s a personal preference.

6. Conclusion 🎯

That’s it for this deep dive into my portfolio and a summary of my thoughts since May 2024, as well as since I started reading your posts in August.

Thanks for all the insightful discussions and shared knowledge—this is an amazing community, and I really appreciate the posts I read since August!

Have a great weekend and thanks you so much for reading so far!

Regards,

A Belgian investor

24Posições

€ 55.285,67

20,16%

1212

15 Comentários

Well done presentation 😎🤞🏼

•

22

•Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet