I actually had individual stocks like $6861 (+3,04%)

$6920 (+1,74%)

$7012 (-2,09%)

$2802 (-1,23%) on the screen. Why has it now become the $XNKY (+0,78%) become?

ETF instead of individual stocks:

Instead of having to choose between the Japanese tech giants, I wanted to reduce the complexity by adding the 225 largest stocks to my portfolio.

Momentum affinity:

Since I am a fan of momentum (also have Europe Momentum in the core), the price weighting of the Nikkei 225 suits me more than the classic market capitalization.

Although Japan is already included in the $FWRG (+0,88%) I am now deliberately overweighting it. I believe that Japan still has a lot of potential to develop.

My aim is to realize gains from my individual stocks such as $ASML (+2,3%) and $GOOGL (+1,09%) as soon as a return of 200% has been achieved. Then I take the stake out and shift into the ETFs. This is how I prepare myself for times when I have to worry less about my portfolio and it becomes a self-runner.

I've realized that I spend too much time on the stock market and I want to reduce that.

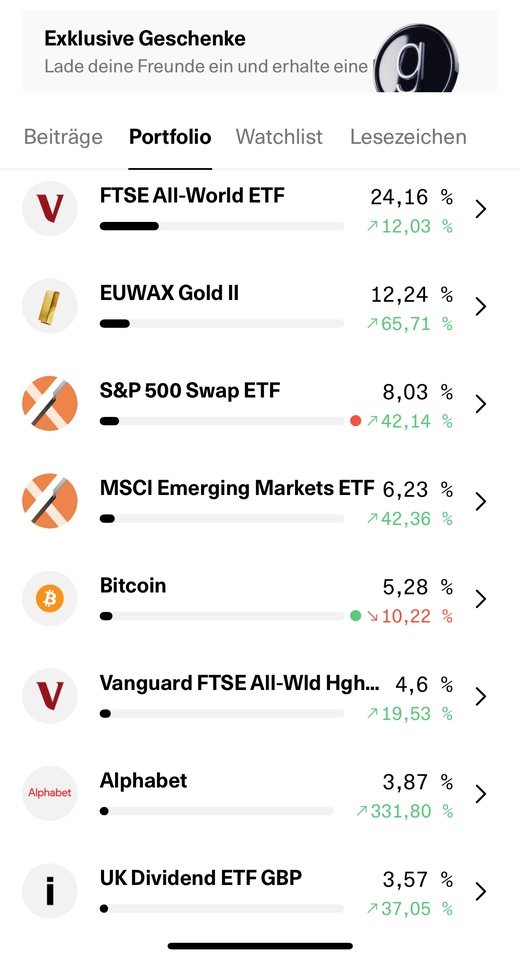

My core should consist of 75% in future

- $FWRG (+0,88%)

- $IEFM (+0,39%)

- $EQAC (+1,24%)

- $XNKY (+0,78%)

- $EWG2 (+0,74%)

- $BTC (+0,65%)

Satellite with the mentioned profits and individual assets or altcoins at 25%.

My USA share is currently 40%, Europe 16%, Asia 12%, gold 12%, crypto 8%. I have the rest in $XEON (+0%) lying around.

The USA share should not exceed 50%, as I believe in Europe, emerging markets and Japan.