Today we are not going to look at a single share, but take a look in a completely different direction. Into the defense sector.

Of course, the most well-known Etf in this sector, the VanEck Defense UCITS Etf, has caught my eye. Its annual performance is around 50%, and it has already posted a return of around 15% this year.

So today we want to take a closer look at what it really contains and whether an investment would be worthwhile, purely on the basis of the fundamental data.

$DFEN (+0,23%)

The fund volume currently amounts to €7.278 billion with annual costs of 0.55%. The Etf is an accumulating fund.

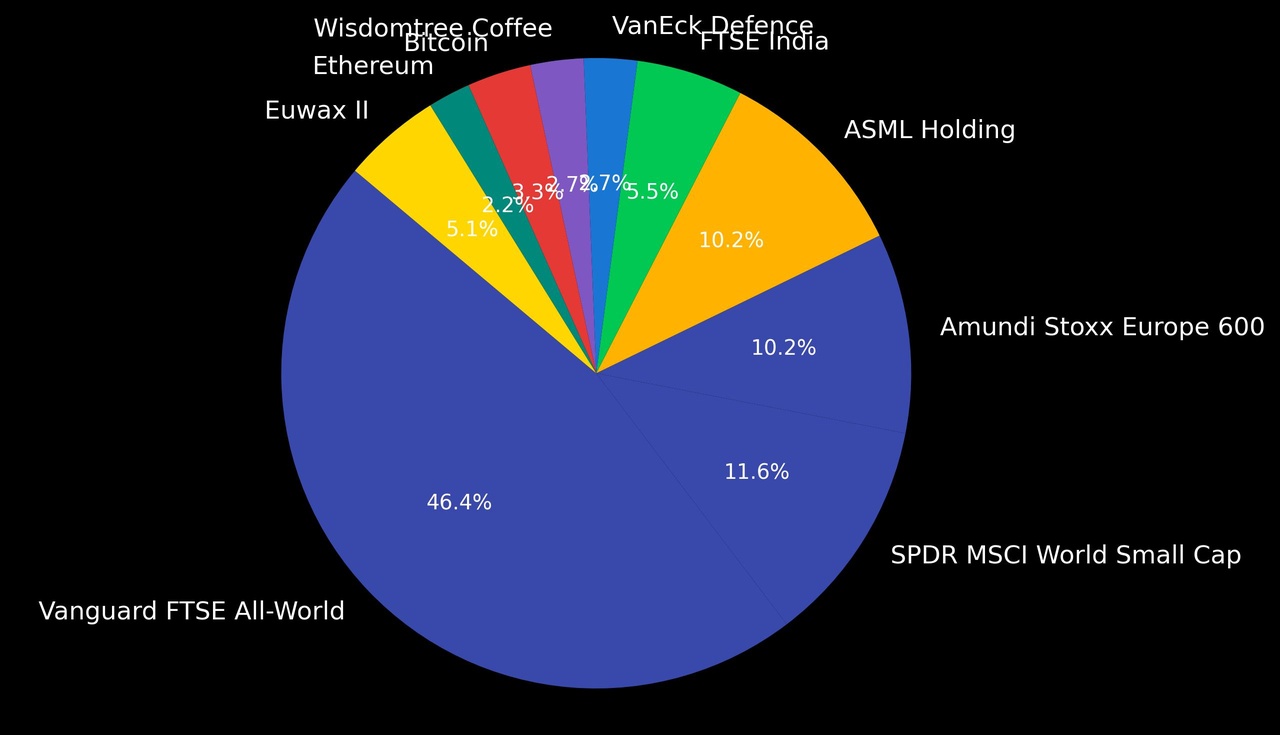

Company distribution:

Palantir Technologies 8% $PLTR (+0,05%)

RTX Corporation 8% $RTX (+0,13%)

Thales 7% $HO (+1,85%)

Leonardo- Finmeccania 7% $LDO (+1,2%)

Hanwha Aerospace Co Ltd ORD 6% $012450

Elbit Systems 6% $ESLT (+2,89%)

Saab 6% $SAAB B (+1,19%)

Curtiss Wright 5% $CW (+1,17%)

Leidos 4% $LDOS (+3,35%)

=57%

The remaining 43% is distributed in smaller shares among other companies, such as Planet Labs $PL (+0,57%) (approx. 2%) or Ondas $ONDS (-0,46%) (1%).

Country distribution:

USA 49%

South Korea 11%

Europe 30%

Israel 7%

Singapore 3%

1 Palantir Technologies (USA)

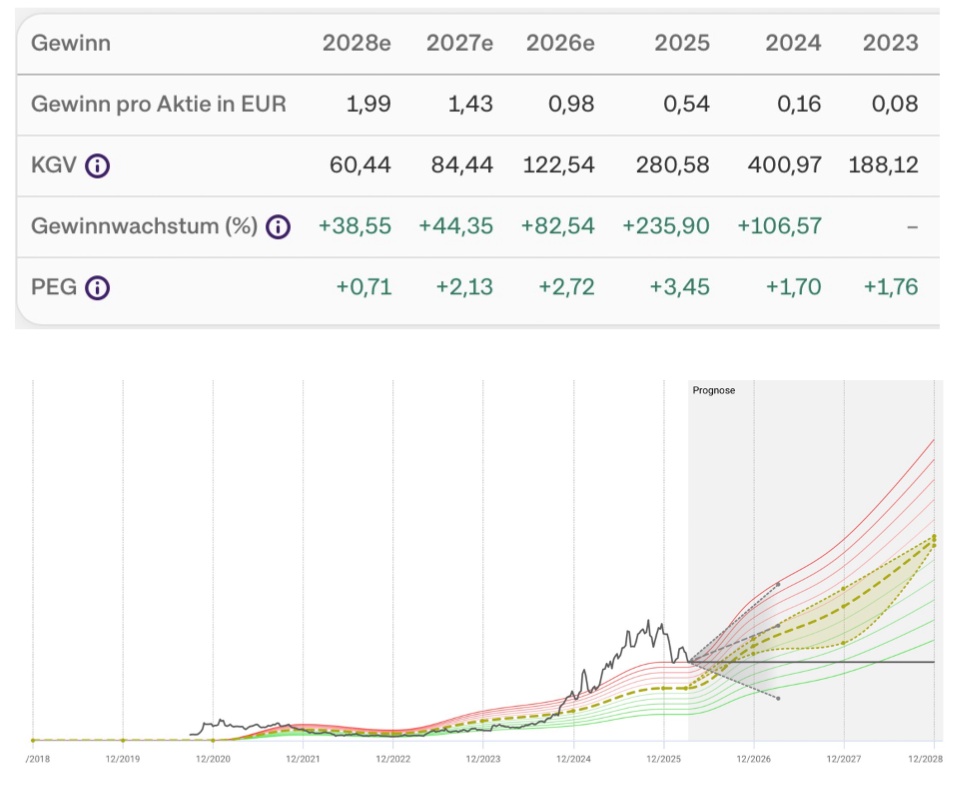

Conclusion: Palantir is not a normal stock

Palantir has developed impressively from a speculative bet to a fundamental force in the S&P 500. The company is more profitable than ever before: massive profit and sales growth meets software margins that are unparalleled in the industry.

But quality has its price on the stock market: this success has already been fully recognized and priced in by the market. With a current P/E ratio of almost 300, the share is extremely expensive and leaves little room for disappointment. Palantir is therefore a highly profitable, exceptional company, but its valuation already anticipates the perfection of the coming years.

This can also be clearly seen in the analysts' estimates: some say there is still plenty of room for improvement with a price target that is almost twice as high, while others say the fair value is half the current price.

That's why I personally can't really get on board with Palantir. The share as a whole is not a buy for me at the moment.

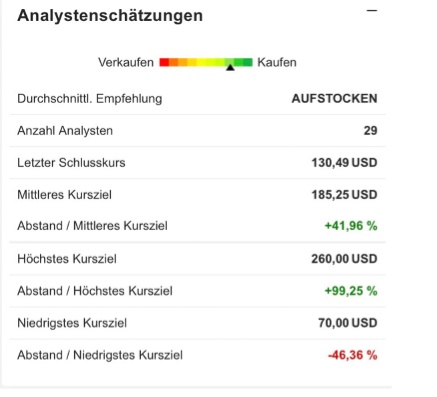

2. RTX corporation(USA)

Conclusion: RTX - The operational bulwark

RTX (formerly Raytheon) is the definition of stability and predictability in April 2026. With a gigantic order backlog of USD 268 billion, the business is secured for years to come. The company has solved the technical problems of the past and is now converting its dominant position in aerospace and defense into record-breaking cash flows.

While Palantir thrives on the AI fantasy, RTX delivers the physical reality: a moderate P/E ratio of around 36 compared to Palantir, rising dividends and a fundamental safety that is rare in the current market environment. It is not a speculative high-flyer, but a highly profitable basic investment for the security age.

However, perfection is priced in here with very high valuation premiums, so I am also skeptical.

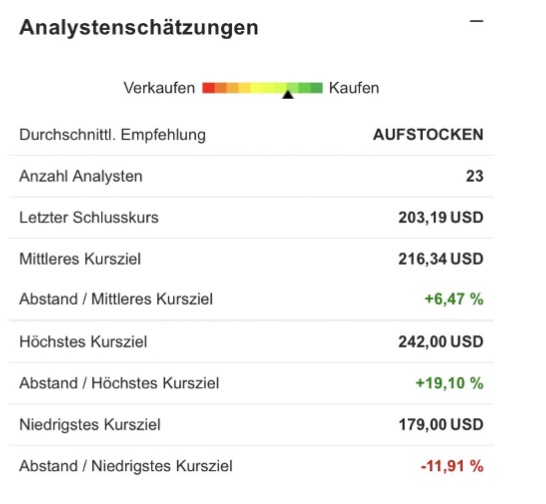

3. thales (France)

Conclusion: Thales - the European "all-rounder"

Thales established itself as the technological backbone of European defense and digital infrastructure in April 2026. With a record order backlog of over EUR 53 billion, the company offers "visibility" for production that extends well beyond 2028.

- Financial performance: 2025 closed with sales of EUR 22.1 billion (+9% organic) and record cash flow. The target for 2026 is clearly defined: A jump in sales to up to EUR 23.6 billion with an improved EBIT margin of around 12.7 %.

- Strategic breadth: Unlike pure defense companies, Thales benefits from three engines simultaneously:

Defense: massive growth through the modernization of European armies.

Aerospace: The recovery in civil aviation is driving demand for avionics.

Cyber & Digital: Through the integration of Imperva, Thales is now one of the world's largest players in the field of data security - a market that is growing completely independently of military budgets.

With a Kgv of 29, we find the most favorably valued company to date.

4 Leonardo Finmenncania (Italy)

Conclusion: Leonardo - the efficiency champion

Leonardo is the "value tip" among the large defense stocks in April 2026. While competitors such as Rheinmetall or Palantir often struggle with extremely high valuations, Leonardo has done its homework in terms of profitability and is now benefiting massively from the European arms race.

- Financial turnaround: Leonardo has beaten all expectations with its figures for 2025. Sales rose to EUR 19.5 billion (+11%), while operating profit (EBITA) increased by a strong 18%. Particularly impressive: net debt was almost halved, giving the Group massive scope for new investments.

- Strategic focus: Under the new industrial plan (2026-2030), Leonardo is fully committed to digitalization and cyber security. With the "Michelangelo" project (an AI-supported air defense system), Leonardo occupies a lucrative niche in the NATO security architecture.

- Valuation as a trump card: Despite a share price rally of almost 190% since 2024, the share is still "reasonably" valued compared to the sector with a forward P/E ratio of around 27. It is significantly cheaper than many US rivals, although Leonardo has similar growth rates for incoming orders (+15%).

We have now briefly analyzed the 4 largest companies in this ETF, which account for around 30%.

How do you rate these companies? Please take a look at the other companies that have not been presented here.

And of course, are you invested in the etf or do you intend to be?

Would it be an investment case for you or do you think the defense sector is largely overvalued?

@Raketentoni

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Multibagger etc. ....