Will probably replace it by iShares Global Water UCITS ETF.

CWCO

Stock

Stock

ISIN: KYG237731073

Ticker: CWCO

KYG237731073

CWCO

Price

Discussion about CWCO

Posts

73Mon·

Easter special 🐰 Easter special 🐇 What is the importance of desalination plants?

Hello my dears,

so that you have something to read and analyze for Easter. There's another one for you in the evening:

EASTER special

If this unnecessary war is about the destruction of important infrastructure that ensures the survival of humans and animals. It is certainly not a pleasant and enjoyable topic.

The Pope has taken a stand on this war today and has found clear words.

I hope that these words have reached the right people.

But as investors, we are of course also concerned about this issue. From the perspective of who are the specialists here and who can rebuild this important infrastructure.

Ladies and gentlemen, let's discuss this in the comments. I'm looking forward to it.

Is a war over water looming in the Middle East?

Attacks on water facilities are rather rare in wars, but they have dramatic consequences. In Bahrain and Iran, authorities recently reported an attack on a desalination plant - such facilities are vital for millions of people in the Middle East. Water economist Esther Crauser-Delbourg warns of a war "far more devastating than the current one" in the event of targeted attacks on water.

What is the significance of desalination plants?

The Middle East is one of the driest regions in the world and is therefore dependent on desalination for water production. According to a study published in the journal Nature, 42 percent of the world's desalination capacity is located in the region. In the United Arab Emirates, 42 percent of drinking water comes from such plants, in Kuwait it is 90 percent, in Oman 86 percent and in Saudi Arabia 70 percent, according to a study by the French research institute Ifri. "Without desalinated water there is nothing",

Desalination plants play an important role in Kuwait's drinking water supply. An Iranian attack has now severely damaged two power plants with such facilities.

05.04.2026

Wichtige Kraftwerke getroffen: Schwere Schäden in Kuwait durch iranischen Angriff - ntv.de

On Sunday, an Iranian drone hits a seawater desalination plant in Bahrain. Millions of people in the Gulf States depend on such facilities. An escalation of the attacks would have devastating consequences.

10.03.2026

Entsalzungsanlagen im Visier: Droht im Nahen Osten ein Krieg um Wasser? - ntv.de

🌍 What happens if desalination plants in the Middle East are damaged?

Destruction of such plants leads to:

- Acute water shortage

- Need for emergency supplies

- Need for reconstruction

- Need for engineering expertise

- Need for spare parts, membranes, pumps, control technology

🧩 Industries that are typically in greater demand in such situations

1️⃣ Engineering & consulting companies

They are needed for damage analysis, reconstruction planning and environmental assessments.

Examples (neutral, without rating):

- Tetra Tech

- AECOM

- WSP Global

These companies supply planningnot construction.

2️⃣ EPC companies (Engineering, Procurement, Construction)

They are contracted for repair and reconstruction.

Typical players in the Middle East:

- Doosan Enerbility

- Hitachi Zosen

- Acciona

- Metito (not listed)

- Veolia / Suez (for operation & modernization)

3️⃣ Manufacturer of membranes, pumps, control technology

When RO systems are damaged, components need to be replaced.

Typical global suppliers:

- DuPont Water Solutions (membranes)

- Toray Industries (membranes)

- Xylem (pumps, sensors)

- Grundfos (pumps)

- ABB / Siemens (control technology)

🌊 Listed companies with a focus on planning

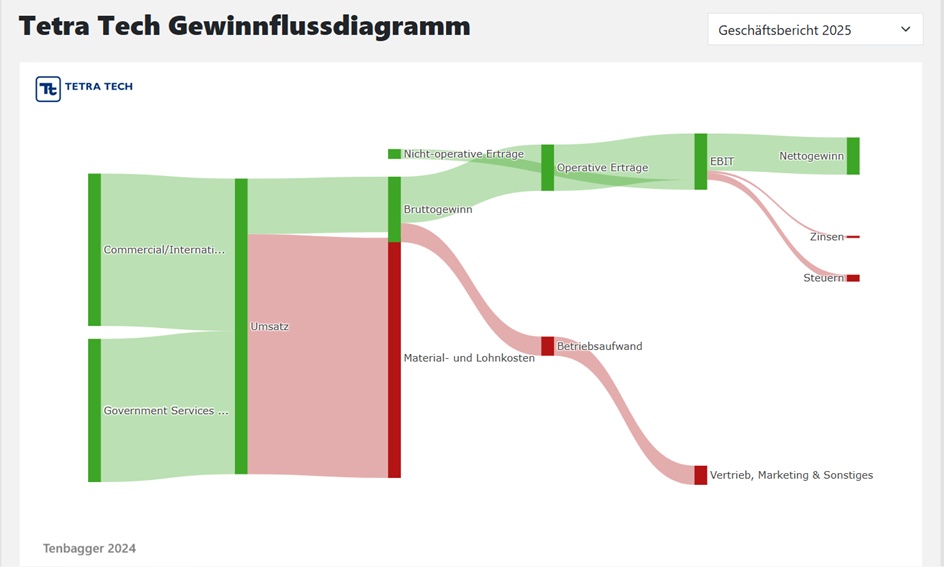

1.🔹 Tetra Tech - (Ticker TTEK) $TTEK (+0.94%) (@Simpson )

- Leading consulting and engineering company focusing on water, environment, infrastructure and high-end engineering.

- Asset-light business model: provides planning, analyses, environmental assessments, digital water solutions - but does not build plants itself.

- Strong in the area of "Digital Water": data analysis, monitoring, SCADA systems, optimization of water infrastructure.

- Active worldwide, including projects in the Middle East (feasibility studies, environmental assessments, technical consulting).

- High margins for the industry (EBITDA ~10-12%) and stable demand from long-term infrastructure and government projects.

- Role in desalination market: enabler/consultant - supports planning & optimization, but not EPC contractor or operator.

Year Earnings p share Earnings growth

2025 0,80

2026 1,33 +65,59 %

2027 1,47 +12,01 %

2028 1,58 +6,09 %

Year P/E ratio PEG

2025 36,08 +0,55

2026 20,11 +1,91

2027 18,20 +2,54

2028 16,98 +1,83

Year Dividend Yield

2025 0,21 0,72 %

2026 0,22 0,82 %

2027 0,26 0,97 %

2028 0,29 1,09 %

(in euros)

2.🏗️ AECOM - (Ticker ACM) $ACM (+0.8%)

- One of the largest engineering and infrastructure consulting firms in the world, focusing on large-scale projects in water, transportation, energy and environment.

- Strong in water infrastructure, including planning, optimization and modernization of desalination plants, waterworks and distribution networks.

- Not an EPC contractor but, like Tetra Tech, a high-end engineering and consulting player (feasibility studies, design, project management).

- Very active in the Middle East, especially in government and mega projects in Saudi Arabia, UAE and Qatar (water, energy, smart cities).

- Asset-light business model with stable, recurring revenues from long-term infrastructure and government contracts.

- Market positioning: One of the top 3 global engineering service providers, often leading the planning & management of large water and desalination projects.

Year Earnings p share Earnings growth

2025 3,63

2026 4,61 +34,68 %

2027 5,65 +14,88 %

2028 6,11 +8,66 %

Year P/E ratio PEG

2025 22,64 +0,84

2026 15,84 +0,71

2027 12,94 +1,59

2028 11,97

Year Dividend Yield

2025 0,66 0,80 %

2026 0,74 1,01 %

2027 0,83 1,13 %

2028 1,23 1,68 %

(in euros)

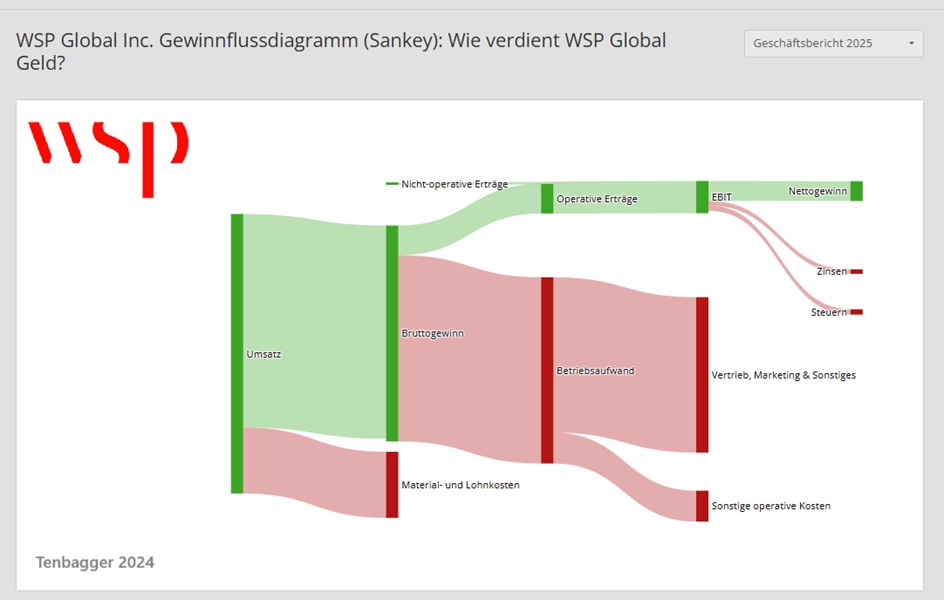

🌐 WSP Global - (Ticker WSP) $WSP (+2.83%)

- One of the largest engineering and consulting service providers worldwide, with a focus on infrastructure, environment, water, energy and urban development.

- Very strong in water & desalination, especially in planning, optimization, hydraulic modelling and technical studies for large scale plants.

- Not an EPC contractor but, like AECOM and Tetra Tech, a high-end engineering and consulting player with a focus on design, project management and technical expertise.

- Active worldwide, including the GCC region (Saudi Arabia, UAE, Qatar), where WSP is frequently involved in mega projects - from water infrastructure to smart city systems.

- Asset-light business model with stable, recurring revenues from government and infrastructure projects; margins typically solid for the industry.

- Market positioning: One of the top 3 global engineering groups, often leading complex water and environmental projects, including desalination.

Year Earnings p share Earnings growth

2024 3,36 22,45 %

2025 4,59 +36,67 %

2026 5,34 +17,26 %

2027 7,08 +34,76 %

Year P/E ratio PEG

2024 48,84 +1,28

2025 33,67 +2,05

2026 25,57 +0,79

2028 19,30

Year Dividend Yield

2024 0,93 0,59 %

2025 0,93 0,60 %

2026 0,93 0,68 %

2027 0,93 0,68 %

(in euros)

🌊 Listed companies with a focus on repair and reconstruction

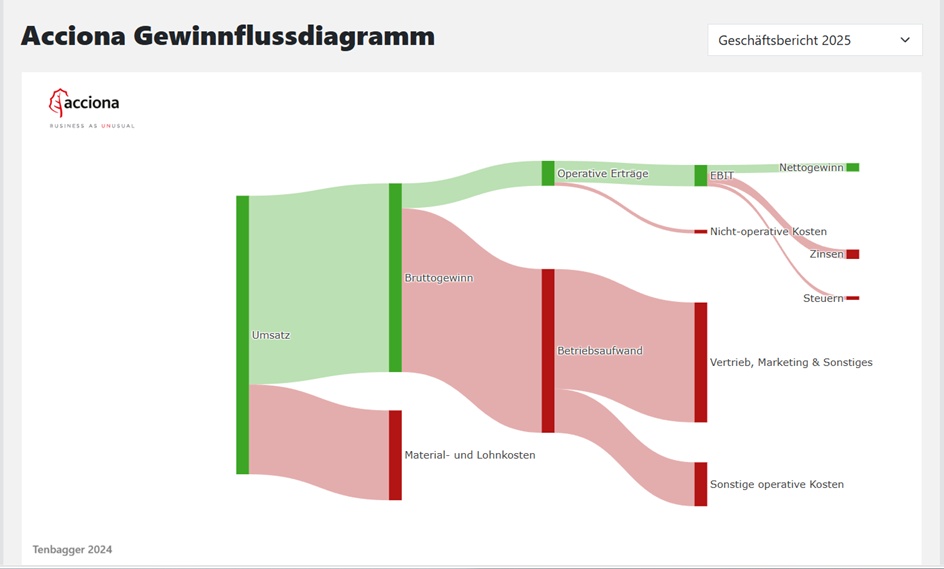

1.💧 Acciona - (Ticker ANA) $ANA (-2.55%)

- Spanish infrastructure and energy group, one of the world's leading providers of water, desalination and sustainable infrastructure.

- Strong EPC player: Acciona plans, builds and operates large seawater desalination plants (RO technology) - in contrast to Tetra Tech, which primarily provides consulting services.

- Very active in the Middle East, especially in Saudi Arabia, the UAE and Qatar; involved in several of the largest RO plants in the region.

- Technology focus on energy-efficient RO systems, often combined with renewables (solar + RO).

- Solid margins and stable demand as water infrastructure is growing strongly worldwide; business model less volatile than traditional EPC groups.

- Market positioning: One of the top 3 global RO desalination providers, with a strong track record in mega projects.

Year Earnings p share Earnings growth

2025 14,74 +90,44 %

2026 8,99 -39,06 %

2027 9,53 +7,23 %

2028 9,83 +2,82 %

Year P/E ratio PEG

2025 12,61 -0,32

2026 25,77 +4,24

2027 24,30 +7,77

2028 23,56 +8,58

Year Dividend Yield

2025 5,54 2,98 %

2026 5,63 2,43 %

2027 5,91 2,55 %

2028 5,93 2,56 %

(in euros)

🌊 Listed companies with a focus on seawater desalination

🔹 1. Veolia Environnement (Euronext: VIE / OTC: VEOVY) $VIE (-0.91%)

- Global leader in water, waste and energy services

- Very active in the Middle East (Saudi Arabia, UAE)

- Major projects in Saudi Arabia, UAE, Oman, Qatar

- Operates and builds large RO desalination plants

Year Earnings p share Earnings growth

2025 1,71 +17,93 %

2026 2,33 +43,37 %

2027 2,50 +9,24 %

2028 2,77 +11,92 %

Year P/E ratio PEG

2025 17,38 +0,48

2026 14,38 +1,88

2027 13,36 +1,24

2028 12,06 +0,72

Year Dividend Yield

2025 1,50 5,05 %

2026 1,62 4,83 %

2027 1,77 5,29 %

2028 1,92 5,72 %

(in euros) ⬆️ @Dividendenopi

2. ecolab (NYSE: ECL) $ECL (+0.56%)

- Provider of water treatment technologies, incl. membrane and desalination solutions

Strong in the industrial sector, increasingly also in the Middle East

Year Earnings p share Earnings growth

2025 6,28 -1,22 %

2026 7,06 +15,33 %

2027 8,26 +14,96 %

2028 9,39 +12,41 %

Year P/E ratio PEG

2025 36,06 +2,90

2026 32,29 +1,90

2027 27,59 +2,03

2028 24,29

Year Dividend Yield

2025 2,31 1,02 %

2026 2,51 1,10 %

2027 2,72 1,19 %

2028 3,02 1,32 %

(in euros)

🔹 3. Consolidated Water Co. Ltd (NASDAQ: CWCO) $CWCO (+0.75%)

- Specializes in seawater desalination

- Operates plants in the Caribbean, but is expanding into regions with water shortages

- - Small but growing - increasingly active in regions with water stress

- - Potential beneficiary of GCC outsourcing

Year Earnings per share P/E ratio

2025 1,14 30,85

2026 1,05 32,37

2027 1,54 22,07

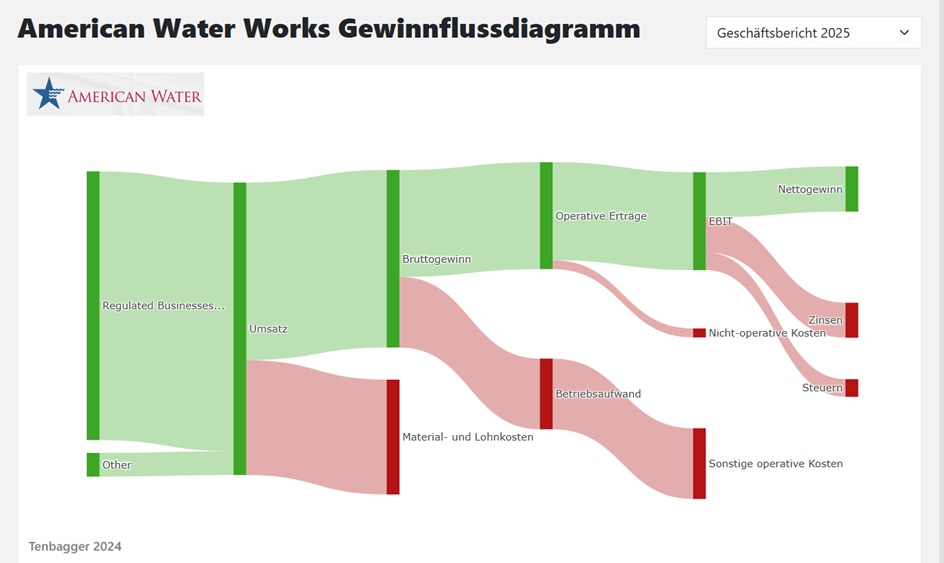

🔹 4. American Water Works (NYSE: AWK) $AWK (+0.58%)

- Largest listed water utility in the USA

- Active in desalination technologies, including for coastal regions

Year Earnings per share Earnings growth

2025 4,91 +5,57 %

2026 5,27 +7,12 %

2027 5,69 +7,79 %

2028 6,17 +8,22 %

Year P/E ratio PEG

2025 22,93 +3,17

2026 22,64 +2,79

2027 20,94 +2,52

2028 19,33 +2,05

Year Dividend Yield

2025 2,86 2,54 %

2026 3,04 2,55 %

2027 3,28 2,75 %

2028 3,53 2,96 %

(in euros)

🔹 5. Hitachi Zosen Corp (TSE: 7004)

- Japanese plant manufacturer

- Builds large desalination plants, e.g. in the Middle East

- Long-standing partner in Saudi Arabia & UAE

🔹 6. Suez (formerly EPA: SEV - now part of Veolia, but still active)

- Strong in membrane and thermal desalination plants

- Large projects in Saudi Arabia, Qatar, UAE

7. ACWA Power (Tadawul: 2082) - Saudi Arabia

- One of the most important companies in the Middle East for desalination

- Operates the gigantic RO plants, among others Rabigh, Shuaibah, Jubail

- Focus: water + energy + PPP models

- Very strong regional player

ACWA Power Co. is included in 78 ETFs.

3% weighting in Franklin FTSE Saudi Arabia UCITS ETF (FLXS) $FLXS (+0.92%)

8. Doosan Enerbility (KRX: 034020)

- South Korean large-scale plant manufacturer

- Leader in MSF/MED plants

- Projects in Saudi Arabia, Kuwait, UAE

Doosan Enerbility Co, Ltd. is included in 141 ETFs.

4.98% weighting in UBS Nuclear Economies UCITS ETF USD acc

(BCFW) $IE0009TPHUV6 (+1.91%)

🏆 Summary for investors

- ACWA Power = the GCC champion (direct exposure to Saudi megaprojects).

- Veolia = global water blue chip with stable cash flows.

- Doosan & Hitachi Zosen = EPC exposure, benefits from large projects.

- Xylem = technology supplier, less cyclical.

- CWCO = small-cap growth, but volatile.

🌍 Why the Middle East in particular?

- Region holds over 50 % of the global desalination market

- Saudi Arabia, UAE and Qatar are investing heavily in large-scale RO plants

Dear all, thank you for reading.

+ 4

www.n-tv.deSchwere Schäden in Kuwait durch iranischen Angriff

4141

35 Comments

Divids@Divids

3Mon

•

55

•Show answer

7Mon·

Basic knowledge - reading beta correctly: What your portfolio reveals about its market sensitivity

Reading time: approx. 5–6 minutes

Many of my recent posts have focused on metrics that help clearly classify business models, risks, and valuations. Beta is one such metric—and it plays a particularly important role. It’s widely available and easy to look up, but it only becomes truly meaningful when viewed in the context of an entire portfolio. This is because beta does not describe the company itself, but rather how a stock behaves in relation to the market.

Mathematically, beta measures the relationship between stock returns and market returns. It is based on the covariance of these returns—which is always derived from historical data. However, the interpretation is inevitably forward-looking, because we use past patterns to infer how a stock will typically behave relative to the market in the future.

Formally, the metric is defined as:

Beta = Covariance(stock return, market return) / Variance(market return)

In practical terms, this means: When the market moves, how strongly does the stock typically move along with it? Values around 1 indicate movements similar to the market; higher values indicate greater volatility, while lower values indicate more stable behavior.

The reason beta is often misinterpreted is that it is not stable. It depends heavily on the time period, the market phase, and the chosen index. A company can continue to perform solidly, but suddenly exhibit a different beta due to changes in interest rates or the risk environment. Beta therefore measures behavior—not quality.

To better illustrate how beta affects a portfolio, it’s worth taking a look at my portfolio. It combines robust, high-quality stocks such as Visa, Alphabet, and Honeywell; growth-oriented technology stocks such as ASML, Nu Holdings, and Innodata; defensive infrastructure and water stocks such as Consolidated Water, Energiekontor, and Energy Recovery; the global ETF tracking the MSCI ACWI; and a uranium block as a cyclical play featuring Cameco, NexGen, Denison Mines, Paladin Energy, and Yellow Cake. Bitcoin rounds out the mix as a standalone, significantly more volatile component.

This mix clearly illustrates why beta is useful to me in my day-to-day investing. Different stocks can be fundamentally strong yet contribute very differently to the portfolio’s volatility profile. Some positions smooth out volatility, while others amplify it—regardless of whether the companies are well-managed or highly profitable. It’s about market behavior, not balance-sheet quality.

For my beta analysis, I use conservative, industry-standard 3–5-year figures from major providers. Most betas are calculated based on daily or monthly returns over precisely these time periods—long enough to be statistically stable and short enough to realistically reflect current market phases. Where official data is unavailable, appropriate sector values are used.

The betas used are as follows:

Large Caps

• $ASML (+0.47%) : 1.25

• $GOOGL (+1.48%) : 1.05

• $V (+0.14%) : 0.95

• $HON (+0.59%) : 1.00

Mid-Caps / Infrastructure

• $CWCO (+0.75%) : 0.80

• $EKT (-0.73%) : 0.75

• $ERII (+1.91%) : 1.20

• $SOP (+2.75%) : 1.10

Small-Cap / High Beta

• $INOD (+2.48%) : 1.80

Uranium Segment (Cyclical)

• $CCO (+1.5%) : 1.40

• $NXE (+0.96%) : 1.60

• $DML (+0.53%) : 1.70

• $PDN (+1.55%) : 1.50

• $YCA (+0.55%) 1.30

ETF

• $ISAC (+0.69%) : 1.00

Crypto

• $BTC (-1.38%) : 2.50

The only factor that matters for the portfolio beta is the size of each position relative to the portfolio.

Here’s how the portfolio beta is calculated:

You look at the size of each position in the portfolio, multiply that share by the beta of the respective stock, and add up all the contributions. Each position therefore contributes to the overall beta exactly in proportion to its weighting.

Applying the weightings of my portfolio in this context yields the following result: The portfolio has a beta of approximately 1.33. This value aligns with the portfolio’s structure: a stable foundation, several growth-oriented components, a deliberately included uranium block, and Bitcoin as a stronger lever.

A beta at this level indicates a fundamentally more aggressive portfolio.

- During uptrends, it outperforms the market.

- During corrections, it reacts more quickly and more sharply.

- The strongest drivers are Bitcoin, Innodata, NexGen, Denison Mines, and Paladin Energy.

- Visa, Consolidated Water, Energiekontor, and the MSCI ACWI ETF provide counterbalances.

This shows that beta is no substitute for fundamental analysis, but it does reveal how a portfolio moves and why. It helps calibrate expectations, contextualize fluctuations, and manage the portfolio’s structure more consciously. A beta of 1.33 is not a judgment on quality—it’s a description of movement. The only thing that matters is whether this dynamic aligns with your own investment strategy.

Finally, two questions for you:

Do you know your portfolio’s beta?

And does it play a role in your portfolio strategy—or not really?

2424

15 Comments

No, I don't actually know the figures for my entire portfolio.

However, my portfolio has been extremely nervous so far. 😂

However, my portfolio has been extremely nervous so far. 😂

•

11

•9Mon·

Water as an investment theme: Why seawater desalination and decentralized treatment are among the most exciting industries of the future

Reading time: 10 minutes

Today I would like to give you a brief insight into what I consider to be an enormously exciting industry of the future.

Water is becoming the strategic resource of our time. While capital flows continue to flow into energy, AI and defense, an industry is growing in the background that is likely to determine security of supply, quality of life and geopolitical stability in the future: the efficient extraction, treatment and distribution of clean water. The combination of seawater desalination and decentralized water treatment in particular is developing into a future sector with considerable structural potential.

According to the World Bank, more than two billion people already live in regions with chronic water shortages. Climate change is further exacerbating this situation: periods of drought, declining groundwater reserves and increasing water consumption due to urbanization and industrial production are pushing existing systems to their limits. Traditional water management is increasingly coming up against physical and ecological limitations. As a result, desalination and treatment are being transformed from an emergency solution into a pillar of modern infrastructure - a market which, according to industry analysts, could reach a volume of up to 250 billion US dollars by 2035. These estimates mark the upper end of the forecast range; realistically speaking, growth is likely to be in the region of 6 to 8 percent annually, driven by public investment programs and private infrastructure partnerships.

Technological progress is giving this development a boost. Reverse osmosis, the core process of seawater desalination, is becoming more efficient, more durable and more modular. A key role is played here by$ERII (+1.91%) I (Energy Recovery Inc.): With its PX Pressure Exchanger, the Californian company has established a technology that reduces the energy consumption of desalination plants by up to 60 percent. This brings the economic viability of such projects within reach - even in regions that were previously considered too cost-intensive. ERII acts not as an operator, but as an enabler: a technology supplier that brings efficiency and scalability to a traditionally sluggish industry.

$CWCO (+0.75%) (Consolidated Water Co.) stands for the operational implementation of this change. The company plans, builds and operates desalination plants in the Caribbean, Mexico and increasingly also in the USA. The latest project in Hawaiʻi, with a contract value of over 200 million US dollars, shows that desalination is no longer just a niche technology, but is becoming part of modern public services - even in industrialized countries. While $ERII (+1.91%) stands for energy efficiency and technological differentiation, desalination embodies $CWCO (+0.75%) embodies the infrastructural core: physical access to water.

A broad industrial ecosystem is emerging along the value chain. $XYL (+0.64%) (Xylem Inc.) develops digital control and sensor systems for water and wastewater networks, $VIE (-0.91%) (Veolia Environnement) is a global market leader in the treatment and reuse of water, and $PNR (+0.6%) (Pentair plc) serves the filtration and pump technology sector. $AWK (+0.58%) (American Water Works), the largest listed utility in the USA, stands for stability and predictable cash flows. In addition, there are specialized providers such as Forward Water Technologies or Desalitech (DuPont Water Solutions), which develop decentralized, modular treatment plants - an area that is increasingly seen as a driver of innovation for the entire industry.

This decentralization in particular is changing the logic of the market. While mega-projects such as those in Saudi Arabia or Israel dominate the media attention, the demand for compact, scalable systems for hotels, farms, industrial parks or coastal communities is growing. Such modular systems can be operated locally, require fewer permits and can be flexibly adapted - characteristics that are becoming increasingly important in times of geopolitical uncertainty and disrupted supply chains. This is reminiscent of the transformation in the energy industry: once centrally organized, now increasingly distributed.

The comparison with the solar industry is therefore understandable - albeit with limitations. Water infrastructure remains a local, permit-intensive and capital-intensive business. Scaling is not exponential, but gradual. Nevertheless, the direction is right: just as photovoltaics has decentralized access to energy, water technology will increasingly organize access to drinking and process water locally. Increased efficiency, automation and digitalization do not replace speed here, but ensure sustainability and profitability over long periods of time.

This will create a new form of infrastructure that combines economic stability with ecological necessity. Water is not a substitutable good; it is the basis of every industrial activity. Demand is inelastic, supply is increasingly driven by technology. For investors, this results in a rare combination: social relevance, political backing and economic predictability. Water treatment addresses key sustainability goals of the United Nations and is one of the few areas in which ESG capital flows are congruent with real economic benefits.

Of course, the industry remains challenging. Desalination is energy-intensive, the recycling of concentrated brine is ecologically sensitive and approval procedures often take years. Many projects depend on state planning and financing, which harbors political risks. Nevertheless, the structural logic prevails: without investment in water infrastructure, neither agriculture nor industry will be sustainable in the long term.

The sector offers several opportunities for investors: Technology providers such as $ERII (+1.91%) and $PNR (+0.6%) benefit from margin levers through innovation, operators such as$CWCO (+0.75%) or $VIE (-0.91%) offer stable, inflation-protected cash flows, and digital and infrastructure service providers such as $XYL (+0.64%) connect both worlds via data and control technology. This interplay forms an industry that is not defined by cycles, but by necessity.

Water treatment will therefore become one of the key topics of the coming decade - not as a quickly scalable growth story, but as a long-term answer to the most pressing resource issues of our time. Water is the foundation of every economy, and desalination is its silent but indispensable engine. In my opinion, anyone investing in this sector today is not positioning themselves in the trend, but in the substance.

1717

6 Comments

•

44

•9Mon·

Share presentation according to HQR model - Clean water, clean balance sheet: Consolidated Water as an underestimated quality value

Reading time: 7 minutes

This stock presentation is based on my Hidden Quality Radar (HQR) - a scoring model that identifies companies with strong substance and growth potential that are still flying under the radar despite their high quality. Consolidated Water is one such case. A niche provider of water desalination whose balance sheet quality, project expertise and geographical focus are coming to the fore in an increasingly underserved market environment.

Here is the rating from the model (85/ 100 points):

- Growth & Profitability (17/20): The company shows solid double-digit growth in revenue and earnings (e.g. 3% YoY revenue growth in Q2 2025, 39% EPS surprise), high operating efficiency with ~38% gross margin and stable EBIT margins above 20%.

- Balance sheet & liquidity (16/20): The financial structure is very strong, with an equity ratio above 80%, net cash position and consistently positive free cash flow generation. Debt is minimal.

- Market Position & Moat (11/15): Consolidated Water has a technological edge in water desalination, is the niche leader in the Caribbean and is increasingly establishing itself in the US. The technological and geographical focus ensures a certain moat.

- Valuation & Momentum (11/15): With a P/E ratio of around 35 (2025) and forward P/E ratio of around 24 (2026), the share is trading slightly below the historical average and is therefore moderately valued. The share price momentum is positive, with the share price rising after better Q2 figures.

- Visibility & Radar (30/30): The company has very low analyst coverage and institutional ownership. The under-the-radar character is therefore very pronounced, which offers opportunities for investors looking for small caps and growth stocks that receive little attention.

While other companies focus on short-term technology cycles $CWCO (+0.75%) operates in a long-term, real economic growth area: clean drinking water in water-scarce regions. The combination of decades of experience, a debt-free balance sheet and an upcoming major project in Hawaii makes the share - despite its ambitious valuation - a structurally interesting quality stock.

A solid growth stock with water as a strategic lever

Consolidated Water operates desalination and water treatment plants in the Caribbean (including the Cayman Islands and the Bahamas), in Mexico and in the south of the USA (Florida). Revenue sources include water sales to end customers, operating contracts for government plants and technical services.

An early project that attracted a lot of media attention was the Rosarito Desalination Project in Mexico (Baja California), which was originally planned as a joint venture between CWCO and Suez. The aim was to supply Baja California and Southern California with desalinated water. However, the project has since been effectively put on hold. There has been no active construction activity since 2020-2021. This is due to regulatory uncertainties, political changes and a lack of funding. CWCO still holds the project company NSC Agua, but according to the current SEC filings (Q2 2025) there are no short-term construction plans.

Nevertheless, the project remains strategically interesting - should the political situation in California change and the need for alternative water sources return to the agenda, it could be reactivated.

Active growth driver: the Kalaeloa project in Hawaii

The new major project in Hawaii is much more concrete: Kalaeloa, a 204-million-dollar seawater desalination plant on the island of Oʻahu. Construction is scheduled to start in 2026, with commissioning planned for 2027. Long-term operation will be governed by a 20-year contract with the Honolulu State Board of Water Supply - with guaranteed service revenues.

Analysts are forecasting a significant increase in earnings from the start of construction:

- 2025 revenue (estimated): 134 million $

- Turnover 2026 (estimated): 211 million $ (+57 %)

- Profit growth 2025 → 2026: +47 %

- EPS increase: 1.11 $ → 1.63 $

- Ø growth until 2027: 36.6% sales / 32.1% profit p. a.

Sources: SimplyWallSt, Investing.com, Finanzen.net (as at October 2025)

Strong balance sheet, stable margin, predictable cash flows

In addition to the project pipeline focus, it is the operational basis that makes Consolidated Water so robust. The company operates with an EBIT margin of over 20%, is net debt-free, generates stable free cash flow and has an equity ratio of >80%.

The existing water contracts - e.g. in the Cayman Islands - run for years, are inflation-indexed and often government-backed. This structure enables the company to take on new projects without dilution or external financing. At the same time, the model can be scaled gradually - through new markets, not necessarily through larger volumes.

Valuation: ambitious, but underpinned by growth potential

The share of $CWCO (+0.75%) shares are currently valued at a P/E ratio of around 35 - based on expected earnings for 2025 (EPS: USD 1.11). This is not a bargain, but already reflects part of the expected growth.

However, the full potential of the Kalaeloa project from 2026/27 is probably not yet fully priced in. Based on the 2026 EPS estimate of USD 1.63, the forward P/E ratio is reduced to around 24. In relation to the expected earnings growth of over 30% p.a., this results in a moderate PEG ratio - an indication that the share is not overpriced despite its ambitious valuation, but still has room for upside if the pipeline is successfully implemented.

Risks: project risks, regulation, visibility

Despite the operational quality, there are risk factors:

- Project-relatedness: the company is heavily dependent on a few, large projects. Delays or disruptions at Kalaeloa could have a direct impact on growth and valuation.

- Regulation: Desalination plants are politically sensitive, particularly in the USA. Opposition from environmental groups or delays by authorities are always an issue.

- Low visibility: The share is hardly liquid, ETFs are not involved, analysts are hardly active - this makes a quick revaluation or larger allocations difficult.

However, CWCO's conservative structure, clear financing, project transparency and low operational complexity noticeably mitigate these risks.

Peer group: smaller, but superior in terms of balance sheet

In comparison with the large utilities such as $AWK (+0.58%) (American Water Works), $WTRG (+0.58%) (Essential Utilities) or its European counterpart $VIE (-0.91%) (Veolia), Consolidated Water stands out due to the strength of its balance sheet. While many large caps are highly indebted and hardly grow organically, CWCO combines solid operating performance with a financially flexible starting position.

Compared to specialized engineering companies such as $XYL (+0.64%) (Xylem) or $TTEK (+0.94%) (Tetra Tech), CWCO has significantly higher margins and is less cyclical. Scaling is achieved through regional expansion - not through aggressive cost programs or risky margin levers.

Quality that delivers, not shines

Consolidated Water is a prime example of the HQR model: structurally strong, financially sound, strategically well positioned - but operationally underestimated. With the Kalaeloa project (Hawaii), a real growth catalyst is in the starting blocks. The impact on sales and profits is substantial and already easy to plan.

I am therefore building up an initial position - not as a momentum trade, but as a long-term investment in a genuine quality stock with a clear operational perspective. If water is the new oil, then CWCO may not be the drill - but the infrastructure pipeline through which it flows.

Sources:

- Company website: https://www.cwco.com

- Share price data: 10/20/2025

- Analyst estimates: Simplywall.st, Investing.com, Finanzen.net

- SEC filings Q2 2025: https://www.sec.gov/edgar/browse/?CIK=928340

1919

1 Comment

9Mon

I'll read it tomorrow during my break, but thanks in advance Voraus👍🏼.

•

22

•11Mon·

Successful together

As promised, I have listed the monthly performance of the reported stocks.

I hope it will inspire you to find new companies.

And a little added value.

1 to 10

$ONDS (+1.7%) 172,70 %. $IREN (+3.07%) 79 %

$NB (-0.81%) 67,48 %. $LMND (-0.22%) 37,24 %

$BMNR (-1.84%) 28,85 %. $UUUU (+2.42%) 24,70 %

$NBIS (+3.07%) 23,64 %. $GILT (+2.35%) 22,64 %

$UNH (-1.67%) 20,74 % $VLA (+0%) 19,61 %.

$ETH (-2.24%) 19,05 %

10 to 20

$APP (+1.43%) 18,69 %. $RDDT (-0.04%) 18,41 %

$MP (+1.67%) 13,81 %. $HOT (+0.2%) 13,37 %.

$9868 (-3.73%) 13,18 %. $XPEV 12,87 %

$LOTB (-1.34%) 12,78 %. $CWCO (+0.75%) 11,76 %

$TUI1 (+3.87%) 9,41 %. $AHT 7,66 %

Remainder

$PRY (+0.08%) 7,47 %. $MU (+2.19%) 6,82 %

$AAPL (+0.01%) 6,87 %

11Mon·

Momentum strategy, being successful together.

Hello my dears,

What do you think of the idea that we might share our weekly winners once a week.

This way we discover all the stocks that are currently showing high momentum.

These might be suitable for a short-term trade.

But we might also discover a long-term investment.

Stocks that are just breaking out due to a story, good figures, new innovations, approvals, etc

And are perhaps not yet on the radar of the community.

What do you think of my idea?

Who's in and which day do you think makes sense?

3737

25 Comments

Here is the whole thing through macro glasses:

1. world small cap value $AVWS +8.19%

2. world value $XDEV +5.49%

3. world small caps $WSML +5.19%

4. Japan $LCUJ +4.71%

5. emerging markets small caps $SPYX +4.06%

It can be seen that small companies outperformed large ones around August and cheaper ones outperformed expensive ones:

And cheap small companies did best. 😁

Bonus:

Gold/USD +3.49%

ETH/BTC +35%

SOL/BTC +30%

1. world small cap value $AVWS +8.19%

2. world value $XDEV +5.49%

3. world small caps $WSML +5.19%

4. Japan $LCUJ +4.71%

5. emerging markets small caps $SPYX +4.06%

It can be seen that small companies outperformed large ones around August and cheaper ones outperformed expensive ones:

And cheap small companies did best. 😁

Bonus:

Gold/USD +3.49%

ETH/BTC +35%

SOL/BTC +30%

•

55

•11Mon·

Successful together

#momentum Strategy week 33

Hello my dears,

stocks mentioned so far were

$MP (+1.67%)

$NBIS (+3.07%)

$LMND (-0.22%)

$AAPL (+0.01%)

$BMNR (-1.84%)

$ELF (-0.08%)

$9868 (-3.73%)

$XPEV (-3.55%)

$UCG (+1.6%)

$PRY (+0.08%)

$G1A (+0.77%)

$LOTB (-1.34%) +10% $UFPT (+0.45%) +9,34%. $AHT 7,15%. $UNH (-1.67%) 20,26%

$ETH (-2.24%)

$NB (-0.81%)

$VLA (+0%)

$HOT (+0.2%) +13%. $CWCO (+0.75%) +14%

$ALV (+0.02%) +6,4 %. $MAIN (+1.21%) +5,3%. $TUI1 (+3.87%) +18,3%

$RDDT (+0.82%) . $GUBRA (-1.74%)

$ONDS (+1.7%)

$IREN (+3.07%)

My shares would be

$MU (+2.19%) +17%. $GILT (+2.35%) +20%. $APP (+1.43%) +17%

The shares are for identification purposes only.

And does not constitute a buy recommendation.

An analysis and evaluation of the multiples should definitely be carried out here.

You are also welcome to share your results with us.

I look forward to hearing more about your performers.

11Mon·

Momentum strategy, being successful together.

Hello my dears,

What do you think of the idea that we might share our weekly winners once a week.

This way we discover all the stocks that are currently showing high momentum.

These might be suitable for a short-term trade.

But we might also discover a long-term investment.

Stocks that are just breaking out due to a story, good figures, new innovations, approvals, etc

And are perhaps not yet on the radar of the community.

What do you think of my idea?

Who's in and which day do you think makes sense?

1919

25 Comments

I use this strategy in a passive way with the ETF "iShares Edge MSCI World Momentum Factor"

•

33

•Trending Securities

Top creators this week

Real-time data from LSX · Fundamentals & EOD data from FactSet