Hello my dears,

so that you have something to read and analyze for Easter. There's another one for you in the evening:

EASTER special

If this unnecessary war is about the destruction of important infrastructure that ensures the survival of humans and animals. It is certainly not a pleasant and enjoyable topic.

The Pope has taken a stand on this war today and has found clear words.

I hope that these words have reached the right people.

But as investors, we are of course also concerned about this issue. From the perspective of who are the specialists here and who can rebuild this important infrastructure.

Ladies and gentlemen, let's discuss this in the comments. I'm looking forward to it.

Is a war over water looming in the Middle East?

Attacks on water facilities are rather rare in wars, but they have dramatic consequences. In Bahrain and Iran, authorities recently reported an attack on a desalination plant - such facilities are vital for millions of people in the Middle East. Water economist Esther Crauser-Delbourg warns of a war "far more devastating than the current one" in the event of targeted attacks on water.

What is the significance of desalination plants?

The Middle East is one of the driest regions in the world and is therefore dependent on desalination for water production. According to a study published in the journal Nature, 42 percent of the world's desalination capacity is located in the region. In the United Arab Emirates, 42 percent of drinking water comes from such plants, in Kuwait it is 90 percent, in Oman 86 percent and in Saudi Arabia 70 percent, according to a study by the French research institute Ifri. "Without desalinated water there is nothing",

Desalination plants play an important role in Kuwait's drinking water supply. An Iranian attack has now severely damaged two power plants with such facilities.

05.04.2026

Wichtige Kraftwerke getroffen: Schwere Schäden in Kuwait durch iranischen Angriff - ntv.de

On Sunday, an Iranian drone hits a seawater desalination plant in Bahrain. Millions of people in the Gulf States depend on such facilities. An escalation of the attacks would have devastating consequences.

10.03.2026

Entsalzungsanlagen im Visier: Droht im Nahen Osten ein Krieg um Wasser? - ntv.de

🌍 What happens if desalination plants in the Middle East are damaged?

Destruction of such plants leads to:

- Acute water shortage

- Need for emergency supplies

- Need for reconstruction

- Need for engineering expertise

- Need for spare parts, membranes, pumps, control technology

🧩 Industries that are typically in greater demand in such situations

1️⃣ Engineering & consulting companies

They are needed for damage analysis, reconstruction planning and environmental assessments.

Examples (neutral, without rating):

- Tetra Tech

- AECOM

- WSP Global

These companies supply planningnot construction.

2️⃣ EPC companies (Engineering, Procurement, Construction)

They are contracted for repair and reconstruction.

Typical players in the Middle East:

- Doosan Enerbility

- Hitachi Zosen

- Acciona

- Metito (not listed)

- Veolia / Suez (for operation & modernization)

3️⃣ Manufacturer of membranes, pumps, control technology

When RO systems are damaged, components need to be replaced.

Typical global suppliers:

- DuPont Water Solutions (membranes)

- Toray Industries (membranes)

- Xylem (pumps, sensors)

- Grundfos (pumps)

- ABB / Siemens (control technology)

🌊 Listed companies with a focus on planning

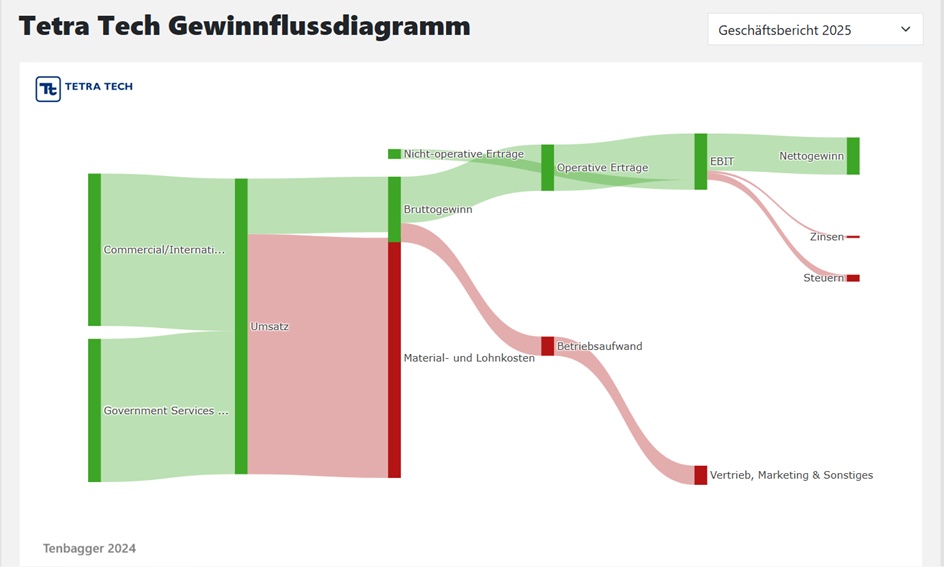

1.🔹 Tetra Tech - (Ticker TTEK) $TTEK (+1.42%) (@Simpson )

- Leading consulting and engineering company focusing on water, environment, infrastructure and high-end engineering.

- Asset-light business model: provides planning, analyses, environmental assessments, digital water solutions - but does not build plants itself.

- Strong in the area of "Digital Water": data analysis, monitoring, SCADA systems, optimization of water infrastructure.

- Active worldwide, including projects in the Middle East (feasibility studies, environmental assessments, technical consulting).

- High margins for the industry (EBITDA ~10-12%) and stable demand from long-term infrastructure and government projects.

- Role in desalination market: enabler/consultant - supports planning & optimization, but not EPC contractor or operator.

Year Earnings p share Earnings growth

2025 0,80

2026 1,33 +65,59 %

2027 1,47 +12,01 %

2028 1,58 +6,09 %

Year P/E ratio PEG

2025 36,08 +0,55

2026 20,11 +1,91

2027 18,20 +2,54

2028 16,98 +1,83

Year Dividend Yield

2025 0,21 0,72 %

2026 0,22 0,82 %

2027 0,26 0,97 %

2028 0,29 1,09 %

(in euros)

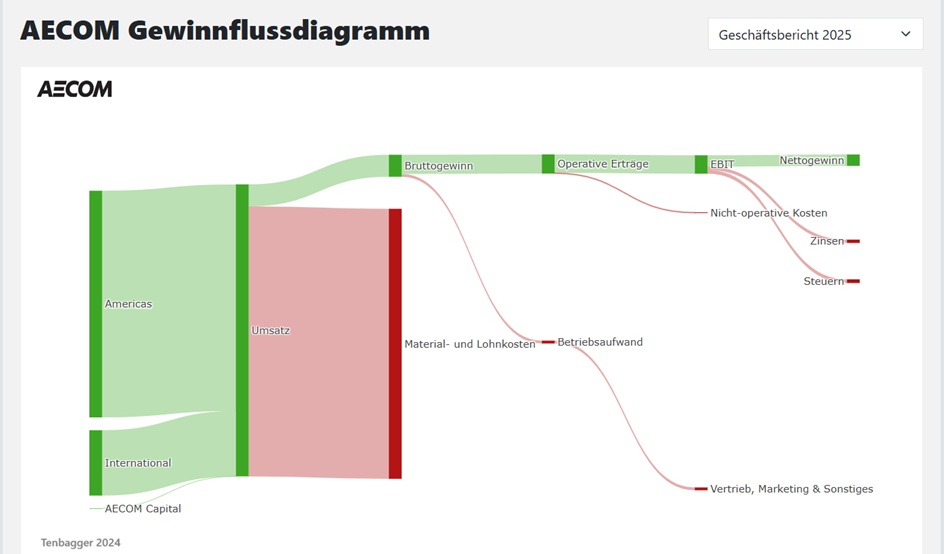

2.🏗️ AECOM - (Ticker ACM) $ACM (-2.49%)

- One of the largest engineering and infrastructure consulting firms in the world, focusing on large-scale projects in water, transportation, energy and environment.

- Strong in water infrastructure, including planning, optimization and modernization of desalination plants, waterworks and distribution networks.

- Not an EPC contractor but, like Tetra Tech, a high-end engineering and consulting player (feasibility studies, design, project management).

- Very active in the Middle East, especially in government and mega projects in Saudi Arabia, UAE and Qatar (water, energy, smart cities).

- Asset-light business model with stable, recurring revenues from long-term infrastructure and government contracts.

- Market positioning: One of the top 3 global engineering service providers, often leading the planning & management of large water and desalination projects.

Year Earnings p share Earnings growth

2025 3,63

2026 4,61 +34,68 %

2027 5,65 +14,88 %

2028 6,11 +8,66 %

Year P/E ratio PEG

2025 22,64 +0,84

2026 15,84 +0,71

2027 12,94 +1,59

2028 11,97

Year Dividend Yield

2025 0,66 0,80 %

2026 0,74 1,01 %

2027 0,83 1,13 %

2028 1,23 1,68 %

(in euros)

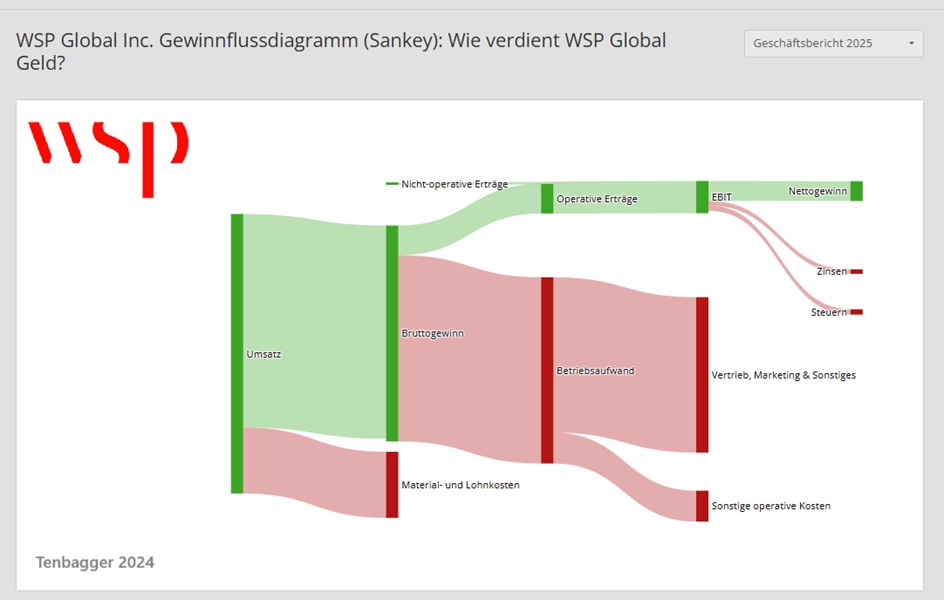

🌐 WSP Global - (Ticker WSP) $WSP (-0.91%)

- One of the largest engineering and consulting service providers worldwide, with a focus on infrastructure, environment, water, energy and urban development.

- Very strong in water & desalination, especially in planning, optimization, hydraulic modelling and technical studies for large scale plants.

- Not an EPC contractor but, like AECOM and Tetra Tech, a high-end engineering and consulting player with a focus on design, project management and technical expertise.

- Active worldwide, including the GCC region (Saudi Arabia, UAE, Qatar), where WSP is frequently involved in mega projects - from water infrastructure to smart city systems.

- Asset-light business model with stable, recurring revenues from government and infrastructure projects; margins typically solid for the industry.

- Market positioning: One of the top 3 global engineering groups, often leading complex water and environmental projects, including desalination.

Year Earnings p share Earnings growth

2024 3,36 22,45 %

2025 4,59 +36,67 %

2026 5,34 +17,26 %

2027 7,08 +34,76 %

Year P/E ratio PEG

2024 48,84 +1,28

2025 33,67 +2,05

2026 25,57 +0,79

2028 19,30

Year Dividend Yield

2024 0,93 0,59 %

2025 0,93 0,60 %

2026 0,93 0,68 %

2027 0,93 0,68 %

(in euros)

🌊 Listed companies with a focus on repair and reconstruction

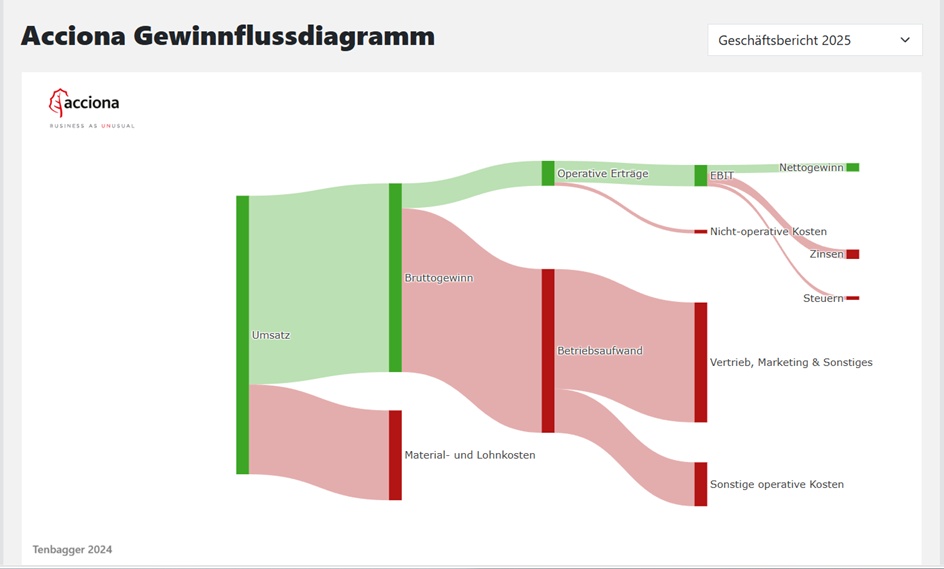

1.💧 Acciona - (Ticker ANA) $ANA (+0%)

- Spanish infrastructure and energy group, one of the world's leading providers of water, desalination and sustainable infrastructure.

- Strong EPC player: Acciona plans, builds and operates large seawater desalination plants (RO technology) - in contrast to Tetra Tech, which primarily provides consulting services.

- Very active in the Middle East, especially in Saudi Arabia, the UAE and Qatar; involved in several of the largest RO plants in the region.

- Technology focus on energy-efficient RO systems, often combined with renewables (solar + RO).

- Solid margins and stable demand as water infrastructure is growing strongly worldwide; business model less volatile than traditional EPC groups.

- Market positioning: One of the top 3 global RO desalination providers, with a strong track record in mega projects.

Year Earnings p share Earnings growth

2025 14,74 +90,44 %

2026 8,99 -39,06 %

2027 9,53 +7,23 %

2028 9,83 +2,82 %

Year P/E ratio PEG

2025 12,61 -0,32

2026 25,77 +4,24

2027 24,30 +7,77

2028 23,56 +8,58

Year Dividend Yield

2025 5,54 2,98 %

2026 5,63 2,43 %

2027 5,91 2,55 %

2028 5,93 2,56 %

(in euros)

🌊 Listed companies with a focus on seawater desalination

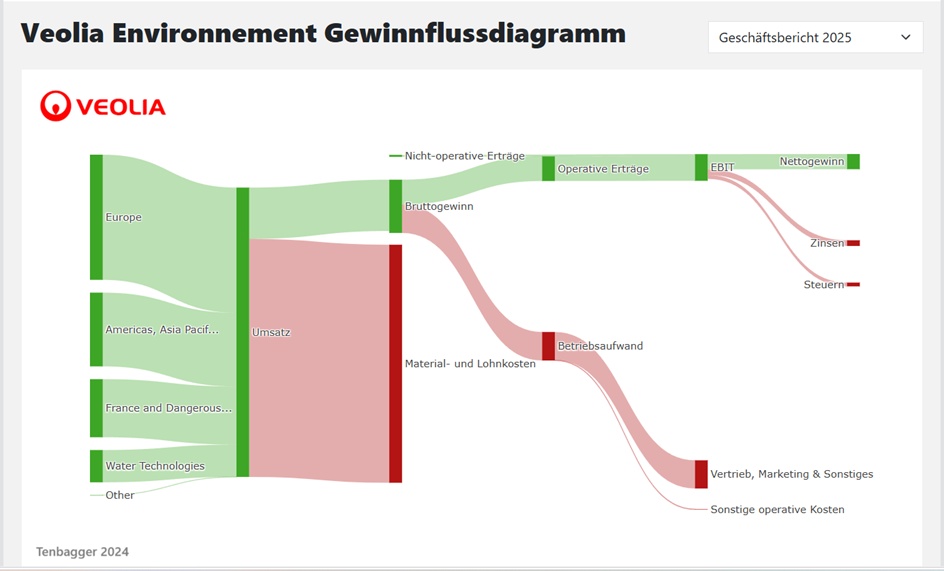

🔹 1. Veolia Environnement (Euronext: VIE / OTC: VEOVY) $VIE (+0.5%)

- Global leader in water, waste and energy services

- Very active in the Middle East (Saudi Arabia, UAE)

- Major projects in Saudi Arabia, UAE, Oman, Qatar

- Operates and builds large RO desalination plants

Year Earnings p share Earnings growth

2025 1,71 +17,93 %

2026 2,33 +43,37 %

2027 2,50 +9,24 %

2028 2,77 +11,92 %

Year P/E ratio PEG

2025 17,38 +0,48

2026 14,38 +1,88

2027 13,36 +1,24

2028 12,06 +0,72

Year Dividend Yield

2025 1,50 5,05 %

2026 1,62 4,83 %

2027 1,77 5,29 %

2028 1,92 5,72 %

(in euros) ⬆️ @Dividendenopi

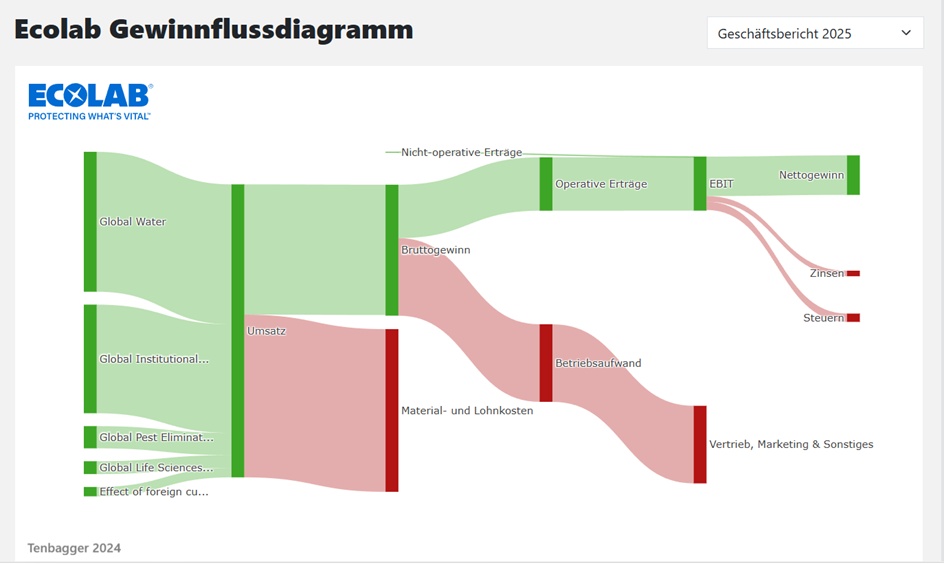

2. ecolab (NYSE: ECL) $ECL (+0.41%)

- Provider of water treatment technologies, incl. membrane and desalination solutions

Strong in the industrial sector, increasingly also in the Middle East

Year Earnings p share Earnings growth

2025 6,28 -1,22 %

2026 7,06 +15,33 %

2027 8,26 +14,96 %

2028 9,39 +12,41 %

Year P/E ratio PEG

2025 36,06 +2,90

2026 32,29 +1,90

2027 27,59 +2,03

2028 24,29

Year Dividend Yield

2025 2,31 1,02 %

2026 2,51 1,10 %

2027 2,72 1,19 %

2028 3,02 1,32 %

(in euros)

🔹 3. Consolidated Water Co. Ltd (NASDAQ: CWCO) $CWCO (+1.82%)

- Specializes in seawater desalination

- Operates plants in the Caribbean, but is expanding into regions with water shortages

- - Small but growing - increasingly active in regions with water stress

- - Potential beneficiary of GCC outsourcing

Year Earnings per share P/E ratio

2025 1,14 30,85

2026 1,05 32,37

2027 1,54 22,07

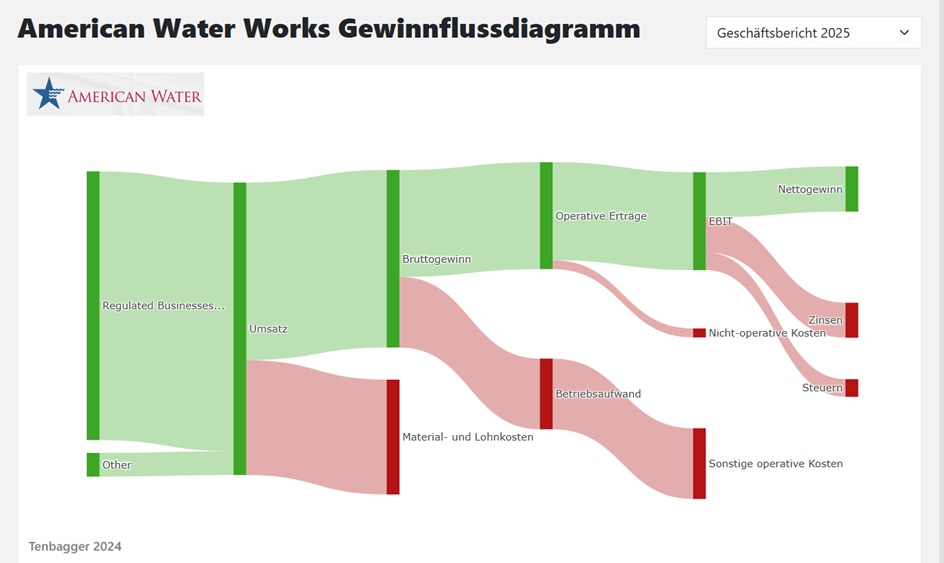

🔹 4. American Water Works (NYSE: AWK) $AWK (+1.93%)

- Largest listed water utility in the USA

- Active in desalination technologies, including for coastal regions

Year Earnings per share Earnings growth

2025 4,91 +5,57 %

2026 5,27 +7,12 %

2027 5,69 +7,79 %

2028 6,17 +8,22 %

Year P/E ratio PEG

2025 22,93 +3,17

2026 22,64 +2,79

2027 20,94 +2,52

2028 19,33 +2,05

Year Dividend Yield

2025 2,86 2,54 %

2026 3,04 2,55 %

2027 3,28 2,75 %

2028 3,53 2,96 %

(in euros)

🔹 5. Hitachi Zosen Corp (TSE: 7004)

- Japanese plant manufacturer

- Builds large desalination plants, e.g. in the Middle East

- Long-standing partner in Saudi Arabia & UAE

🔹 6. Suez (formerly EPA: SEV - now part of Veolia, but still active)

- Strong in membrane and thermal desalination plants

- Large projects in Saudi Arabia, Qatar, UAE

7. ACWA Power (Tadawul: 2082) - Saudi Arabia

- One of the most important companies in the Middle East for desalination

- Operates the gigantic RO plants, among others Rabigh, Shuaibah, Jubail

- Focus: water + energy + PPP models

- Very strong regional player

ACWA Power Co. is included in 78 ETFs.

3% weighting in Franklin FTSE Saudi Arabia UCITS ETF (FLXS) $FLXS (+0.91%)

8. Doosan Enerbility (KRX: 034020)

- South Korean large-scale plant manufacturer

- Leader in MSF/MED plants

- Projects in Saudi Arabia, Kuwait, UAE

Doosan Enerbility Co, Ltd. is included in 141 ETFs.

4.98% weighting in UBS Nuclear Economies UCITS ETF USD acc

(BCFW) $IE0009TPHUV6 (+2.92%)

🏆 Summary for investors

- ACWA Power = the GCC champion (direct exposure to Saudi megaprojects).

- Veolia = global water blue chip with stable cash flows.

- Doosan & Hitachi Zosen = EPC exposure, benefits from large projects.

- Xylem = technology supplier, less cyclical.

- CWCO = small-cap growth, but volatile.

🌍 Why the Middle East in particular?

- Region holds over 50 % of the global desalination market

- Saudi Arabia, UAE and Qatar are investing heavily in large-scale RO plants

Dear all, thank you for reading.