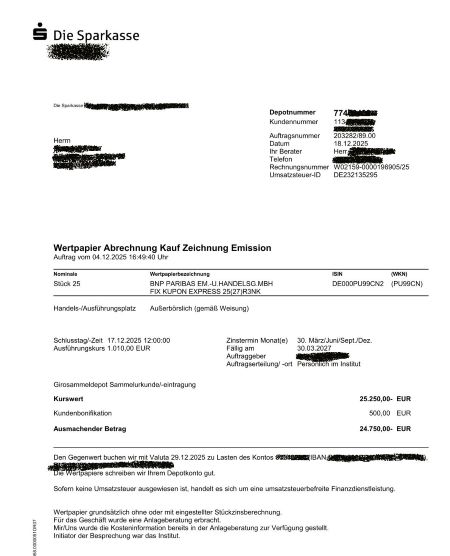

Press release from $EKT (-1.66%) dated 31.03.2026. Light at the end of the tunnel? At least for today, a clear plus again, after the share price had already risen yesterday.

- Group EBT at the upper end of the adjusted forecast

- Sales and earnings up on previous year

- Dividend proposal doubled to EUR 1.00 per share

- Challenging market environment - increasing visibility expected over the course of the year

- Significant earnings potential for the coming financial years

Bremen, March 31, 2026 - Energiekontor AG ("Energiekontor"), one of the leading German project developers and operators of wind and solar parks based in Bremen and listed in the General Standard, has met the forecast for the 2025 financial year, which was adjusted in October 2025, at the upper end of the range and, from today's perspective, expects a further improvement in consolidated earnings in the 2026 financial year. In addition, Energiekontor confirms its multi-year growth target, taking into account the changed framework conditions.

Adjusted forecast for 2025 met at the upper end of the range - dividend proposal doubled

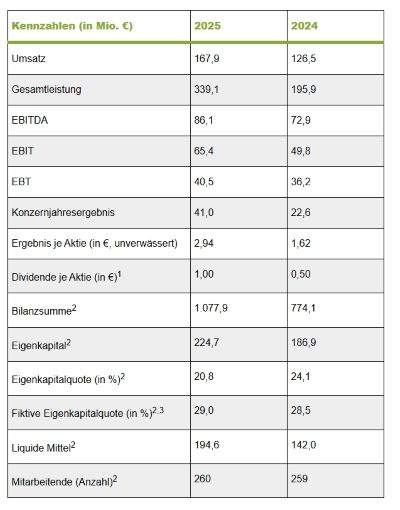

In an increasingly complex and challenging market environment, Energiekontor generated increased consolidated revenue of EUR 167.9 million in the 2025 financial year (2024: EUR 126.5 million). Total operating performance amounted to EUR 339.1 million (2024: EUR 195.9 million). In particular, the increase in project planning activities recognized in profit or loss led to a higher consolidated operating result (EBIT) of EUR 65.4 million (2024: EUR 49.8 million), which corresponds to an EBIT margin of 38.9% (2024: 39.4%). Adjusted for higher interest expenses, Energiekontor generated consolidated earnings before taxes (EBT) of EUR 40.5 million (2024: EUR 36.2 million) and an EBT margin of 24.1 percent (2024: 28.6 percent).

The year-on-year increase in Group EBT thus meets the earnings forecast adjusted in October 2025 for Group EBT in the 2025 financial year at the upper end of the range, which envisaged consolidated earnings before taxes of around EUR 30 to 40 million. Previously, Energiekontor had assumed a higher range of around EUR 70 to 90 million. The main reason for the reduced profit forecast was the postponement of key closing conditions for upcoming transactions, which could therefore no longer be met in the 2025 financial year. This related in particular to project delays caused by the authorities and the resulting deadline extensions as well as the postponement of the announcement and updating of grid connection commitments as part of the ongoing grid reform in the UK.

In the 2025 financial year, Group taxes were positive in the amount of EUR 0.4 million (2024: EUR -13.6 million), resulting in a Group net income for the year of EUR 41.0 million (2024: EUR 22.6 million), which was therefore slightly higher than the Group EBT. The positive tax effect mainly resulted from favorable tax conditions for a project sold abroad and the reversal of deferred taxes. Basic earnings per share amounted to EUR 2.94 (2024: EUR 1.62).

The shareholders of Energiekontor AG should participate in the development of the company even in challenging financial years. The amount of the dividend payout is based on the net profit generated. The Management Board and Supervisory Board will therefore propose to the Annual General Meeting on May 27, 2026 in Ritterhude that around 35 percent of Energiekontor AG's net retained profits be used for the dividend distribution. The proposed distribution corresponds to a dividend of EUR 1.00 per share, which is double that of the previous year (2024: EUR 0.50).

Significant increase in earnings in the Project Planning and Sales segment

In the 2025 financial year, the Project Planning and Sales segment generated increased external revenue of EUR 94.9 million (2024: EUR 52.4 million). At EUR 20.8 million, segment EBT almost tripled compared to the previous year (2024: EUR 7.3 million).

In the 2025 financial year, Energiekontor sold seven wind projects with a total generation capacity of around 209 megawatts (2024: 51 megawatts), of which one British wind project and one German repowering wind project contributed to the segment result for the 2025 financial year. The remaining five turnkey wind projects that have been sold and are currently under construction will be recognized in profit or loss when they are commissioned in the 2026 and 2027 financial years.

As of December 31, 2025, a total of 21 projects with a total generation capacity of around 640 megawatts were under construction or financial close had been reached for these projects (December 31, 2024: 368 megawatts). In addition, Energiekontor commissioned two solar parks and one wind park with a total generation capacity of around 83 megawatts in the reporting year (2024: 124 megawatts). As of the reporting date, there were also 34 building permits with a total generation capacity of almost 1.2 gigawatts (December 31, 2024: 1,129 megawatts). In terms of total nominal capacity, the majority was attributable to the UK project business, followed by Germany, while the remaining share was predominantly attributable to the French market.

Stable earnings in the electricity generation segment with further expansion of the proprietary portfolio

In the 2025 financial year, external revenue in the Electricity Generation segment from the Group's own wind and solar parks was roughly on a par with the previous year, with the segment generating external revenue of EUR 68.6 million (2024: EUR 69.4 million). The segment result (EBT) amounted to EUR 17.1 million (2024: EUR 26.0 million). The lower earnings are mainly due to one-off special effects recognized in profit or loss, which were included in the previous year and which were primarily based on receivables in connection with the compensation of earnings shortfalls at various wind farms in Germany. Apart from this, the segment result in the 2025 financial year showed a comparatively solid development.

The total generation capacity of the Group's own portfolio of wind and solar parks increased to around 448 megawatts in the course of the 2025 financial year (December 31, 2024: around 395 megawatts). The expansion of the proprietary park portfolio was driven forward in particular by the commissioning of new solar projects. Further projects with a total generation capacity of more than 230 megawatts, which are intended for the proprietary portfolio, are currently under construction. The aim is to expand the proprietary park portfolio to over 680 megawatts, with this target figure rising continuously as further financial closures are achieved.

Electricity production from our own parks amounted to around 617 gigawatt hours in the reporting year and was therefore slightly above the previous year's level despite a significantly below-average wind year. Additional generation contributions from newly commissioned solar parks had a stabilizing effect.

Operating Development, Innovation and Other segment makes solid contribution

The Operational Development, Innovation and Other segment recorded revenue and earnings development slightly below the previous year's level. External revenue decreased slightly to EUR 4.4 million (2024: EUR 4.6 million). The segment result (EBT) reached EUR 2.5 million (2024: EUR 2.8 million).

Project pipeline continues to grow - share of advanced projects increased again

Energiekontor was again able to expand the high level of its project pipeline in the 2025 financial year. As of December 31, 2025, the project pipeline amounted to around 11.6 gigawatts (excluding US project rights) compared to 11.2 gigawatts in the previous year. Including US project rights, it amounted to around 12.2 gigawatts (31 December 2024: around 12.1 gigawatts).

At the same time, the proportion of projects in advanced development phases increased again. Their total generation capacity amounted to around 3.1 gigawatts (December 31, 2024: around 2.7 gigawatts) and forms the basis for short and medium-term growth while maintaining the high quality of the project pipeline. Technological diversification was also driven forward. Solar projects now account for around a third of the project pipeline.

Continued focus on growth strategy 2023 to 2028

The 2025 financial year was characterized by a very dynamic market environment. In particular, extended project realization times, limited availability of systems and infrastructure as well as delays in grid connection confirmations and tendering processes - especially in the UK - affected the timing of project sales. In Germany, too, there are currently still uncertainties with regard to the future structure of the EEG subsidy system from 2027 and the specific design of the announced grid package, the effects of which cannot yet be conclusively assessed. It can be assumed that these framework conditions will initially remain in place for the rest of 2026. Energiekontor expects that planning certainty will gradually increase over the course of the year as soon as the regulatory requirements in the core markets of Germany and the UK become more concrete.

In this context, the operational development of the business remains robust. At the same time, the market mechanisms in project development have changed noticeably. An increasing number of approved projects is coming up against continued high costs for plants, infrastructure and financing as well as falling award values in the Federal Network Agency's tenders, which is increasing the economic pressure on individual projects. Energiekontor is countering these developments with consistent project selection and focused management of the project pipeline. The company is benefiting from its lean organizational structure and high operational efficiency.

Against this backdrop, earnings performance remains largely determined by the timing of individual project sales and realizations. At the same time, the continuous expansion of the proprietary portfolio strengthens the basis for stable, recurring income and increases the resilience of the business model. At the same time, despite the high level of investment activity, the company has a robust liquidity position and a solid equity base that financially secures the implementation of the project pipeline and the expansion of the proprietary portfolio. This further increases the stability and predictability of the Group's earnings base. In addition, Energiekontor is continuously working on further strengthening its competitive position through targeted technological and innovative improvement measures, including in the areas of smart wind farm controlling, proactive maintenance, hybrid parking concepts, battery storage solutions and other measures to improve project profitability.

Based on current project planning and taking into account the remaining uncertainties with regard to regulatory and market conditions, Energiekontor currently expects consolidated earnings before taxes (EBT) in a range of EUR 40 to 60 million for the 2026 financial year (2025: EUR 40.5 million). The forecast deliberately reflects the current uncertainties regarding the timing of project implementation. The main contributions to earnings are expected to be generated from several ready-to-build sales in the UK market, from the commissioning of the three German turnkey wind farms sold in the 2025 financial year and from the company's own wind farm portfolio.

With increasing planning certainty regarding the regulatory and infrastructural conditions over the course of the year and the resulting confirmation of previous project planning, Energiekontor sees significant potential for additional earnings contributions in the coming financial years. Against this background, the growth strategy 2023 to 2028, which aims to achieve Group EBT of EUR 120 million in the 2028 financial year, remains focused on sustainable and profitable growth and will be further specified and sharpened with increasing clarity over the course of the year, actively taking into account the market and general conditions that have changed in the meantime.

"In the 2025 financial year, we created a solid earnings base in a very challenging environment and met the upper end of our forecast, which was adjusted in October 2025. Even if the currently communicated forecast range for 2026 may appear cautious at first glance in view of the existing project portfolio, it deliberately reflects the remaining uncertainties regarding the timing of project implementations. However, with increasing clarity regarding the regulatory and infrastructural framework conditions, we expect significantly improved predictability and continue to see considerable potential for additional earnings contributions in the coming years," says Peter Szabo, CEO of Energiekontor AG.

The Annual Report 2025 contains further information on Energiekontor's business development, financial position, economic and market environment and outlook. It is available for download at https://www.energiekontor.de/investor-relations/finanzberichte.html for download.

1For the reporting year 2025 subject to the approval of the Annual General Meeting on May 27, 2026.

2As at the reporting date (31.12.).

3More details on the notional equity ratio in the Annual Report 2025 on page 81.

The Energiekontor AG share (WKN 531350/ISIN DE0005313506/General Standard) is listed on the SDAX of the German Stock Exchange in Frankfurt and can be traded on all German stock exchanges.

contact

Julia Pschribülla

Head of Investor & Public Relations

Phone: +49 (0)421-3304-126