"Sell in May..." doesn't really apply here and would say the stock market wisdom is over for this year 😅

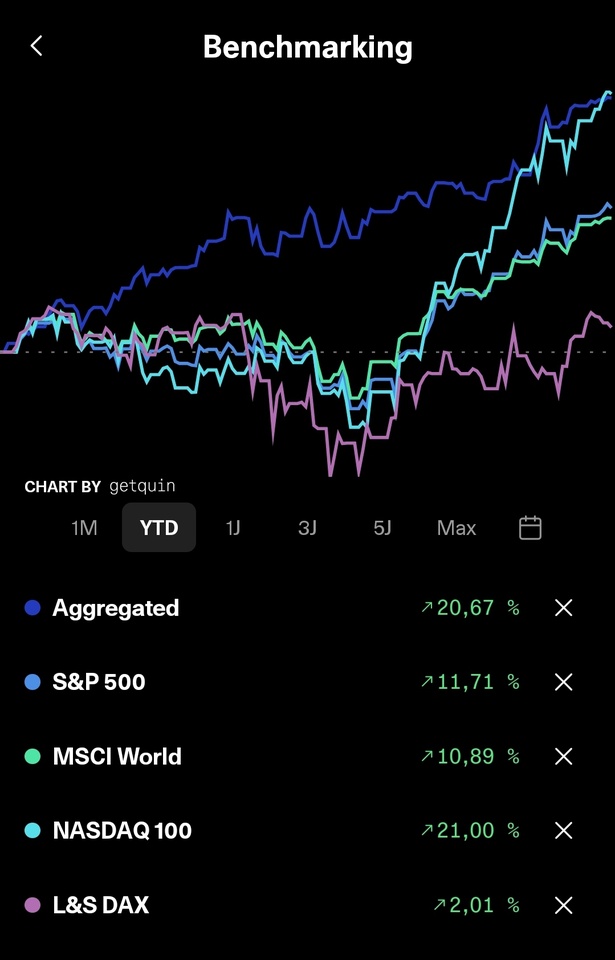

Well, I still had to submit to the Nasdaq this month...

...but to be honest, it doesn't bother me at all, because at the end of the day it's the big picture that counts and nothing happens overnight in the long term...

...because over the year as a whole everything is going as usual and continues to confirm my approach...

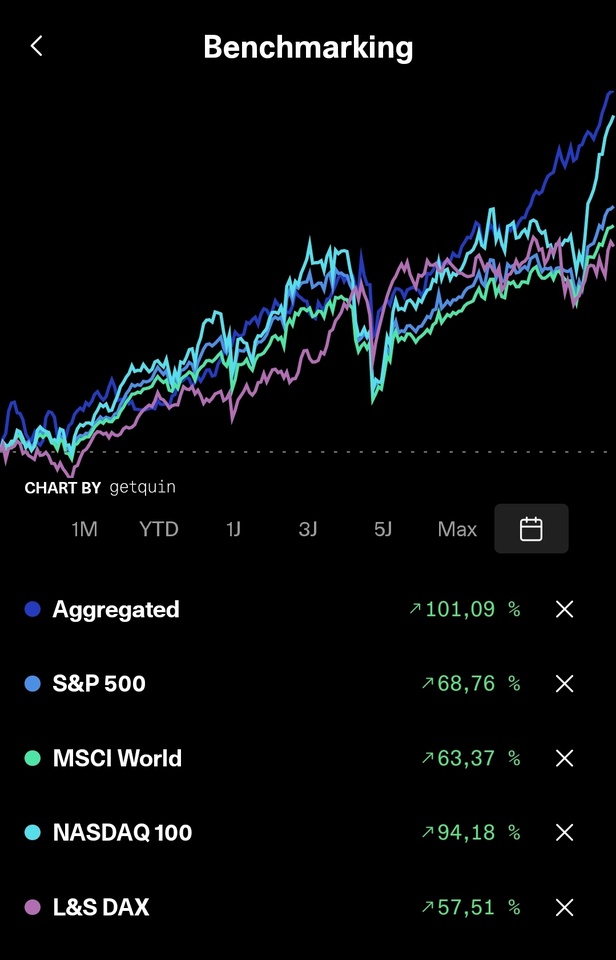

...just as in the long-term view. Even though the Nasdaq is clearly catching up, my portfolio is running much more smoothly and continues to purr consistently 💪🏻

Of course things can always be better, but be that as it may, I'm really happy with my approach so far and continue to enjoy peaceful nights and dividends 🫠

》Dividends《

A pro po, this month with 6 payouts there were 266.37€ net dividends, which means an increase of 129.45% YoY and with a YoC of 6.91% it is slowly leveling off at the desired level of 7%+ despite acquisitions.

The important target here remains the 2k net dividends this year.

》TOP 3《

$3750 (-6,52%) +21,13% (+126,47%)

$ASWM (-1,24%) +18,79% (+27,18%)

$MUX (+0,09%) +12,30% (+21,95%)

》FLOP 3《

$1211 (-3,21%) -11,26% (-15,31%)

$ALV (+1,25%) -0,39% (+12,93%)

$MAIN (+0,72%) +0,10% (-0,08%)

》Acquisitions《

66x $FTWG (+0,01%)

25x $MAIN (+0,72%)

》Disposals《

-

Whereby $1211 (-3,21%) is currently under observation, but until then I will wait for the next figures.

CONCLUSION

None of this is a short-term spurt, but rather long-term ambitions... with this in mind, I wish us all good luck 🤝