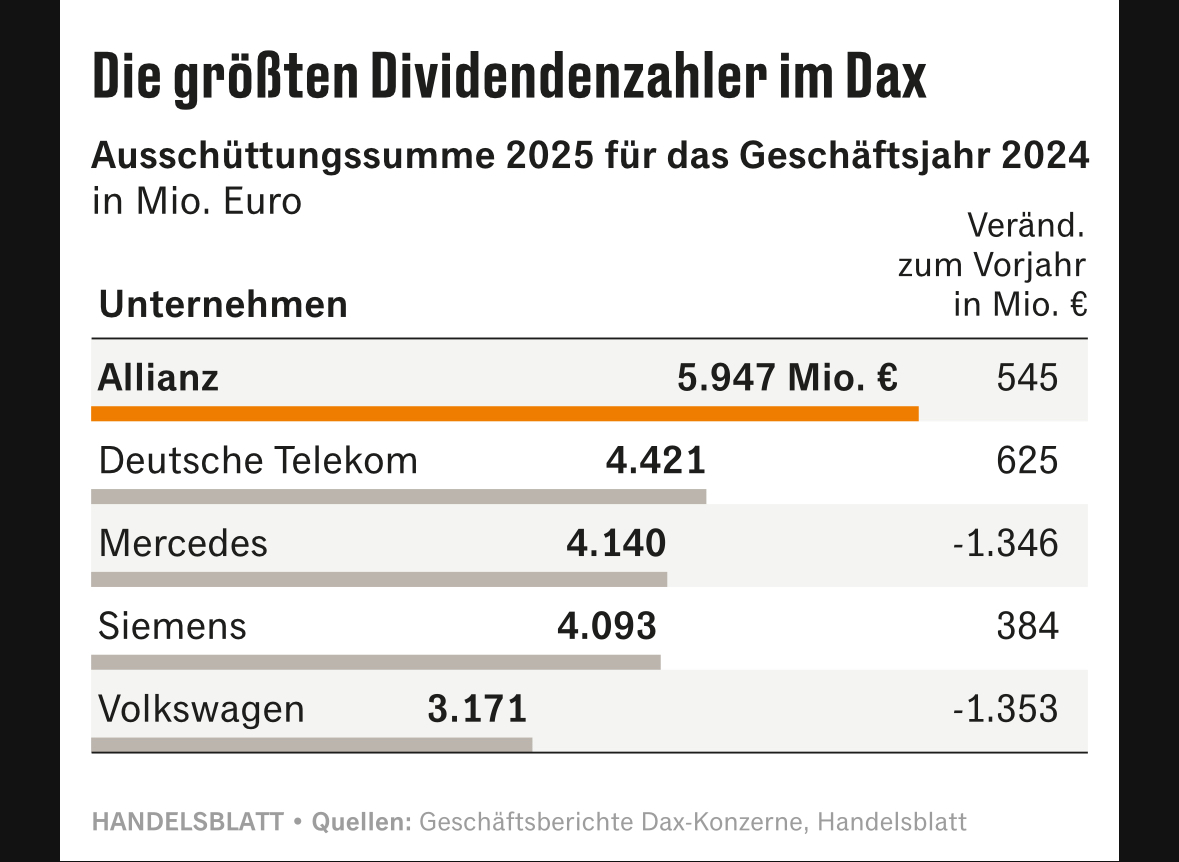

15 of the 40 DAX companies are expected to achieve record profits in 2025.

However, five shares of the record profit groups are trading at least 20 percent below their previous high. This makes these stocks interesting because it reduces their valuation. One share is even trading 75 percent below its record high.

Handelsblatt profiles these five shares with a view to the companies' share valuations and business prospects.

75 percent below record high: Zalando

Zalando is currently trading $ZAL (-0,99 %) is currently 75 percent below its all-time high, although the company is expected to earn more in the current financial year than ever before.

23 out of 31 analyses recommend buying the share at the current reduced price level, only two recommend selling.

However, shareholders should not be blinded by the supposedly favorable valuation, as the high average P/E ratio of 60 is distorted by losses and very meager profits from the early days as well as the brief euphoria for online retail shares during the pandemic.

42 percent below record high: Symrise

Analysts forecast for Symrise $SY1 (+0,64 %) on average 514 million euros net profit, after the previous record profit of 478 million euros in the previous year. The operating profit before interest and taxes is expected to be 21.5 cents per euro. The previous forecast was 21 cents.

16 out of a total of 24 analysts recommend buying the share. One argument is the high dividend continuity. In spring, the payout increased for the 15th time in a row. Nothing stands in the way of another increase in 2026 in view of rising Group profits.

39 percent below record high: Beiersdorf

With a price loss of 30 percent over the past six months, the shares of consumer goods manufacturer Beiersdorf $BEI (-0,97 %) is one of the worst performers in the DAX.

Nevertheless, Beiersdorf is on the verge of another record profit. After a net profit of 912 million euros in the past financial year, analysts are forecasting an average of just under one billion euros for 2025.

17 out of 26 analysts recommend buying the share, two recommend selling. Despite imminent record profits, the share is trading more than a third below its record high. With a P/E ratio of 20 based on the profits expected in the next four quarters, the share is still not cheap. However, it is valued 20 percent lower than the average of the past 20 years.

30 percent below record high: Siemens Healthineers

Hardly any other DAX-listed company is as globalized as the Siemens medical technology subsidiary. Siemens Healthineers generates 95 percent of its sales abroad. $SHL (+0,83 %) abroad. This makes the company independent of the German market.

The manufacturer of surgical robots, computer tomographs and radiotherapy equipment posted a net profit of 1.9 billion euros last year. Analysts are forecasting a record profit of 2.2 billion euros for the current financial year.

With a P/E ratio of 18.8 based on the profits expected in the next four quarters, the share is moderately valued and 15 percent lower than the historical average. However, the Siemens subsidiary has only been listed on the stock exchange since 2018.

23 out of a total of 25 analysts who regularly analyze the Group recommend buying the share. None recommend selling. This gives Siemens Healthineers by far the best rating of the shares portrayed here.

20 percent below record high: SAP

In the past quarter, SAP's earnings before interest and taxes (EBIT), adjusted for special effects $SAP (+2,59 %) earnings before interest and taxes (EBIT) adjusted for special items rose by around a third to 2.6 billion euros compared to the same period last year. The cash inflow, which is important for investors, increased by 83 percent to just under 2.4 billion euros.

For the year as a whole, analysts are forecasting an average net profit of 6.8 billion euros. That would be more than ever before and more than twice as much as in 2024. In the previous year, however, provisions worth billions of euros for employee severance programs distorted the balance sheet.

27 buy recommendations are offset by four hold and three sell ratings. One reason for the fairly strong vote despite the high valuation is the high level of resilience: a good 85% of revenue is based on recurring and therefore reliable business. This makes the IT group virtually independent of economic fluctuations.

Source text (excerpt) & graphic: Handelsblatt, 23.09.25