I could definitely see myself $VWCE (+0,51 %) saving $VWRL (+0 %) in the long run—but is that really less of a hassle, especially with ING?

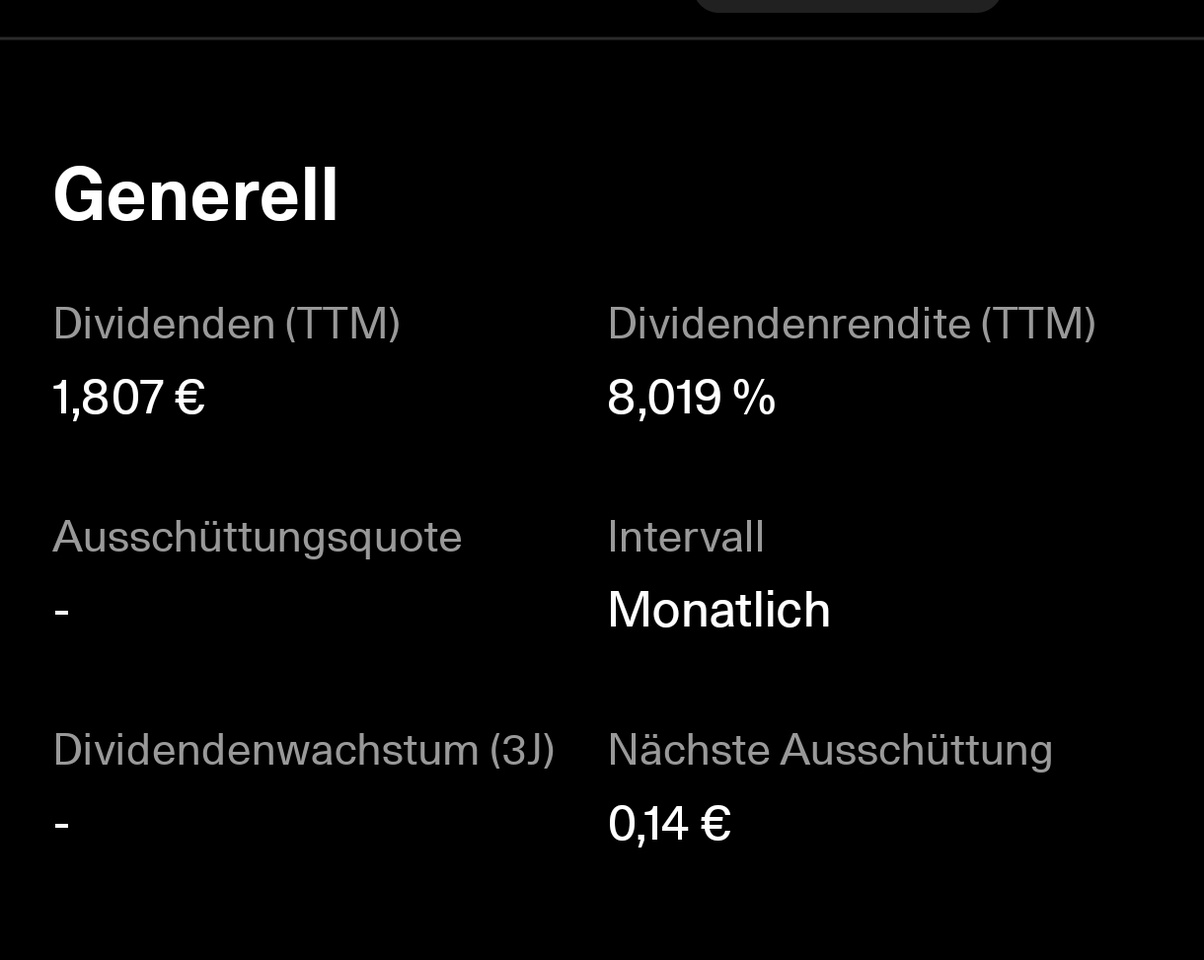

I’m thinking mainly about the annual tax payments, for which I have to set aside (pre-calculated) liquidity. That’s not the case with a dividend-paying fund, is it? Or am I missing something?

I do find the effort involved in timing the sale just right—including fees, etc.—to be significantly greater…

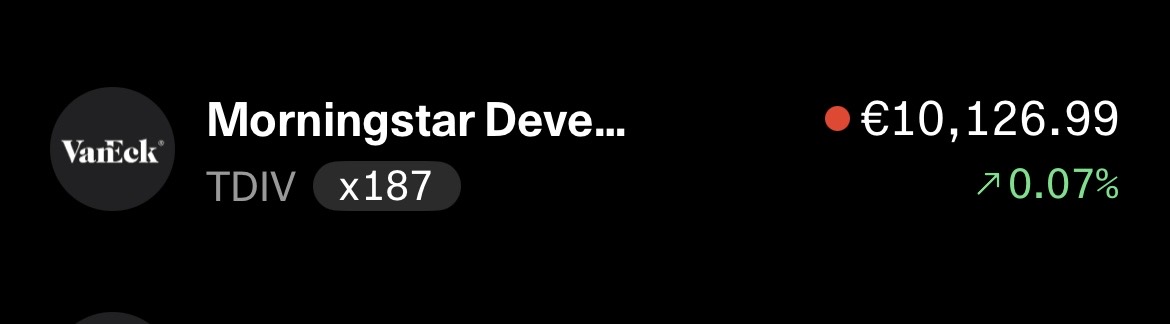

This month, thanks to vacation bookings, we were able to invest 3,000€, of which 2,000€ went into the $VWRL (+0 %) and €1,000 $TDIV (-0,74 %) . Starting next month, I’ll try to put more back in…

This month, thanks to vacation bookings, we were able to invest 3,000€, of which 2,000€ went into the $VWRL (+0 %) and €1,000 $TDIV (-0,74 %) respectively

Hey, I've had the $JEGP for 13 or 14 months—don't waste your money on it; it doesn't work.

If you absolutely want dividends, go with a classic $TDIV or $VHYL, or just put everything into the $VWRL

There are a lot of people here who are really unhappy with the $JEGP and have already closed it out. So don’t make the same mistake. I’m getting rid of mine, too, and will be spreading it out across $LDGL$WINC and $VHYL