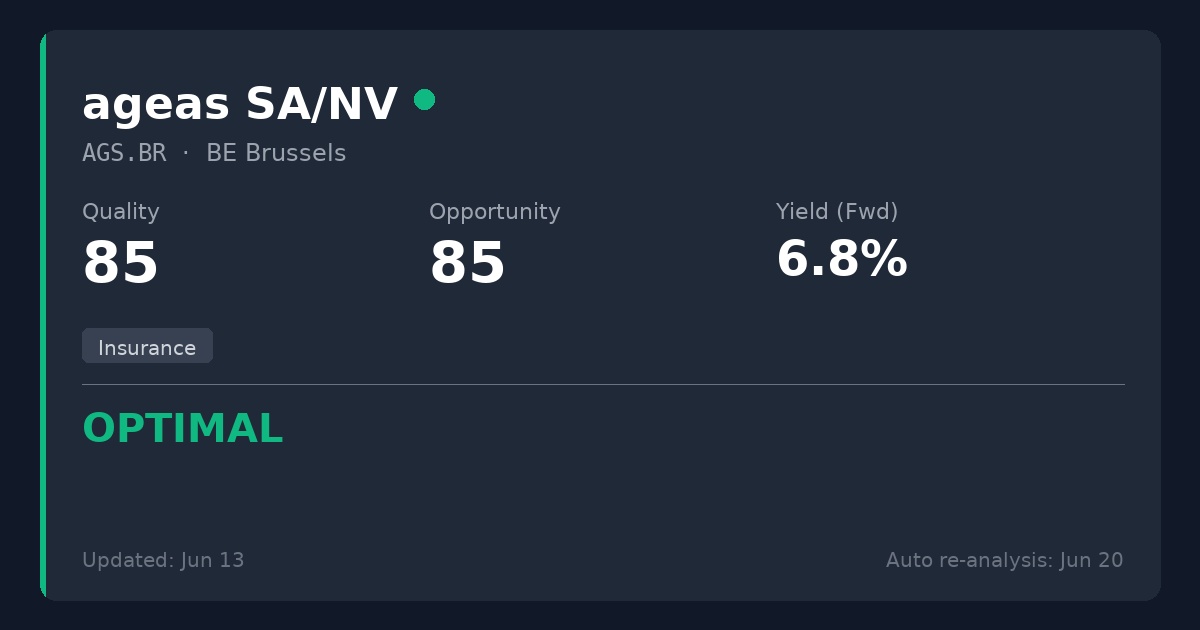

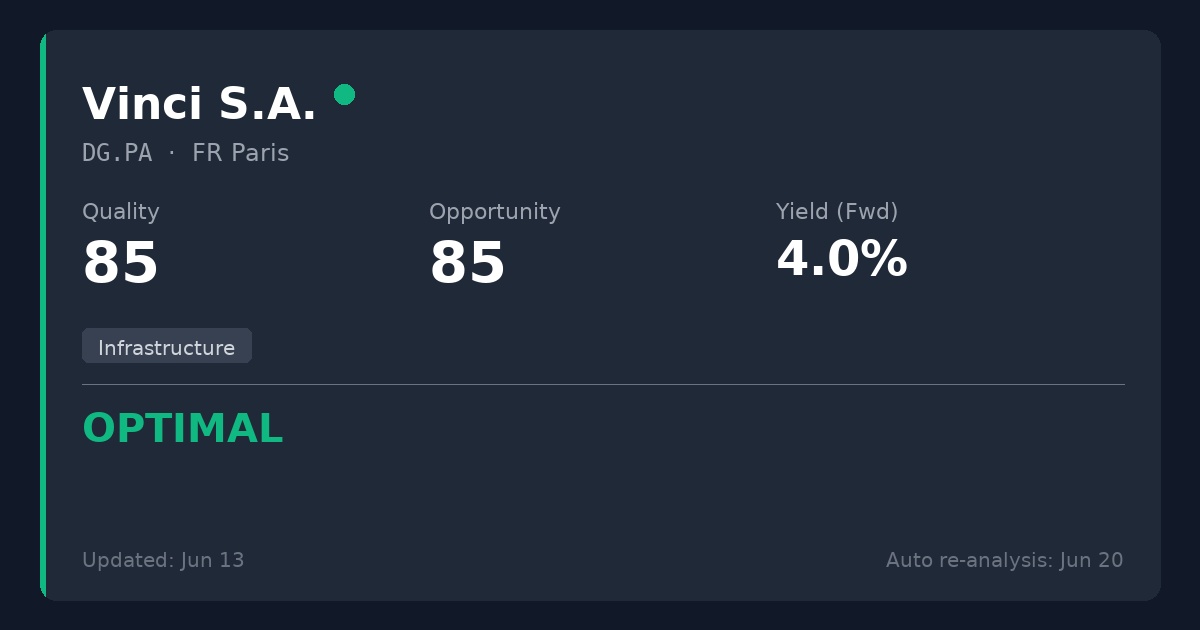

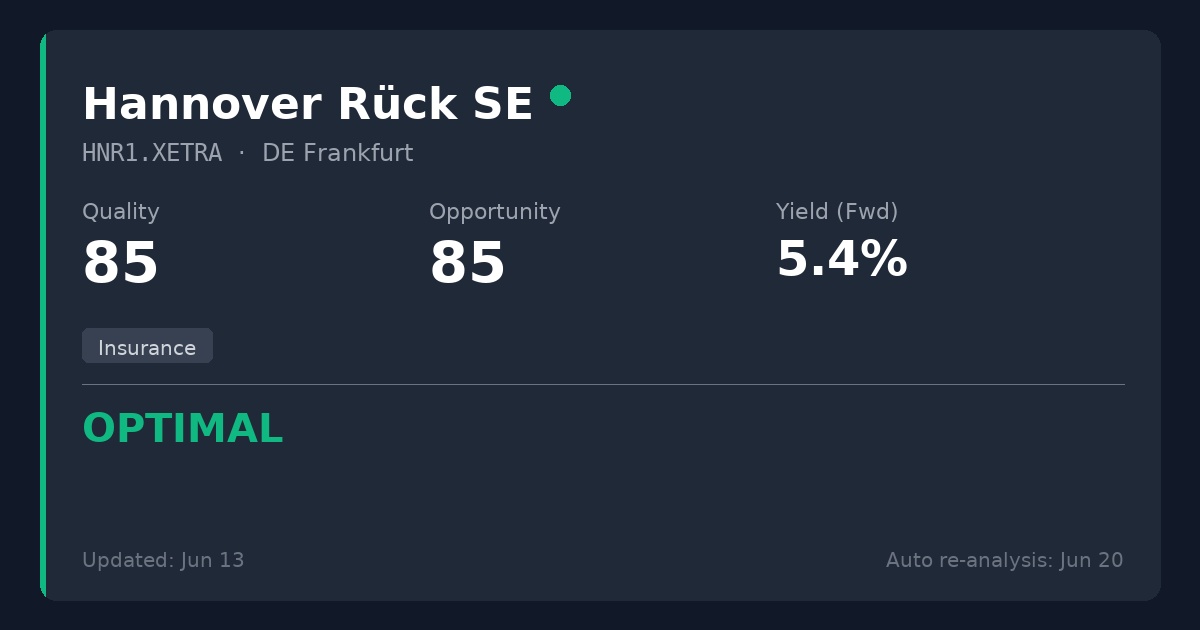

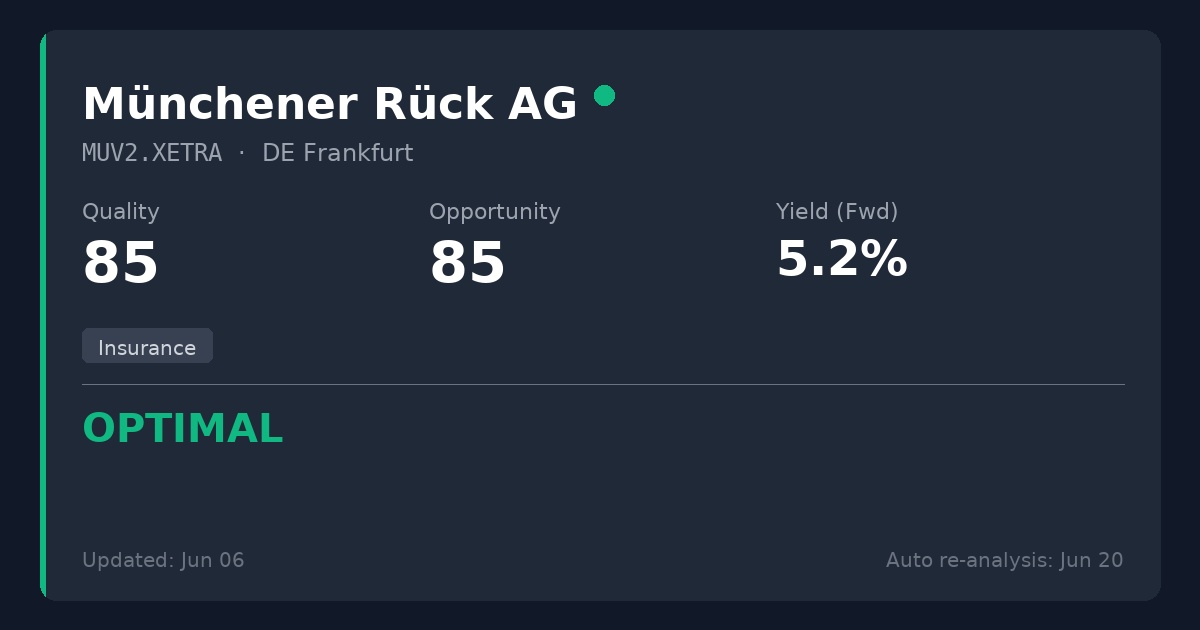

Every Saturday I update my 250+ dividend stock database.

The top 4 best opportunities with the highest qualities this week are:

I believe I have posts on all of them

Puestos

61Hello,

I have a question for you, or rather, I need your advice regarding my core-satellite portfolio.

I’d like to restructure my portfolio. I want to reallocate the weightings and replace SAP.

I’m thinking of a 60/40 weighting.

It should be held for at least 25 years, and dividends aren’t a must since I use up my tax-free allowance every year anyway.

I’ll invest €30,000 to start and contribute €240 monthly to the two ETFs.

I’m thinking of using the Vanguard FTSE All World as the core.

The satellites should be the Amundi Semiconductor ETF, Amazon, Alphabet C, Stryker, Visa, Hannover Re, Hermes, and Rolls-Royce (employee stock).

What do you think?

$VWRL (+0,03 %)

$AMZN (+0,19 %)

$GOOG (+0,35 %)

$V (+0,36 %)

$SYK (+0,36 %)

$CHIP (-0,38 %)

$RR. (-0,85 %)

$RMS (-11,54 %)

$HNR1 (-0,54 %)

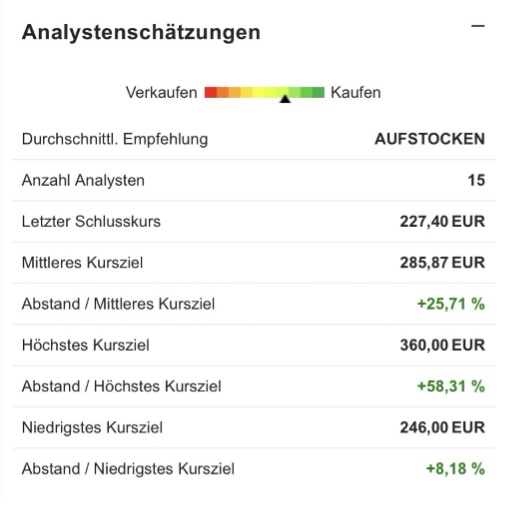

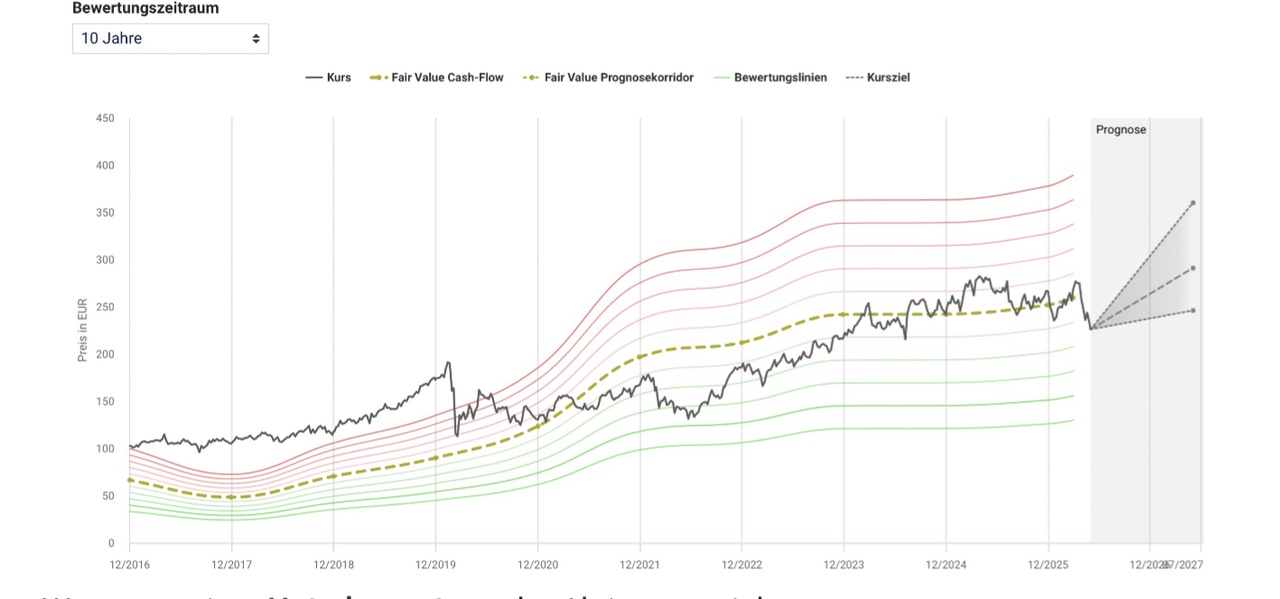

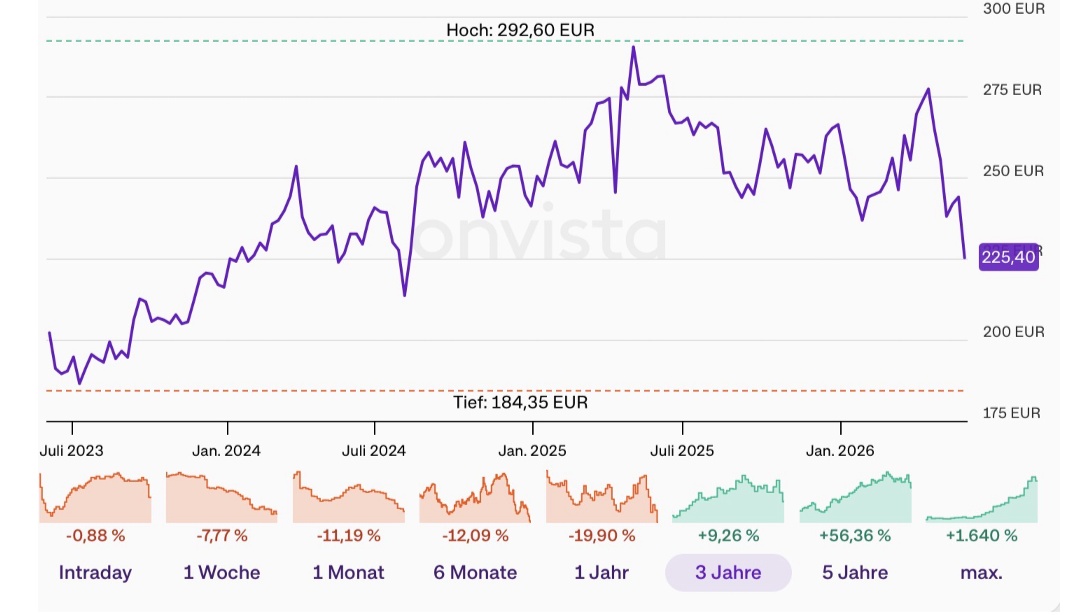

It's been a long time since I've written a stock analysis. But today it's that time again, it will be about Hannover Re $HNR1 (-0,54 %). As always, we will systematically analyze the share and then give a conclusion at the end. Of course, as always, this is not investment advice and only reflects my own opinion.

The share has lost 23% since its high of €292.60 and is currently trading at €225.40.

In terms of the chart, we are now falling from above onto a larger support area. If this holds, the price could stabilize and perhaps even end this correction. However, if we fall below it at the end of the week, the probability of further losses increases. Looking only at the chart, I would put Hannover Re on my watch list and keep a very close eye on it. In principle, however, I can imagine that we have not quite reached the end yet.

+ 1

📊 𝐄𝐫𝐠𝐞𝐛𝐧𝐢𝐬𝐬𝐞

- Consolidated net profit: €710.6M (previous year €480.5M)

- EBIT: €971.1M (previous year €696.5M)

- Reinsurance sales: €6.5B

- Return on equity: 21.2% (previous year: 16.1%)

- Return on investment: 3.6%

- Earnings per share: €5.89 (previous year €3.98)

- Solvency II ratio: 254%

⠀

🎯 𝐀𝐮𝐬𝐛𝐥𝐢𝐜𝐤 𝐀𝐮𝐬𝐛𝐛𝐥𝐢𝐜𝐤

- Group net profit of at least €2.7B expected in 2026

- Combined ratio below 87% expected

- Return on investment of around 3.5% targeted

- Life and health reinsurance to achieve ~€925M service result

⠀

📌 𝐖𝐢𝐜𝐡𝐭𝐢𝐠𝐬𝐭𝐞 𝐏𝐮𝐧𝐤𝐭𝐞𝐭𝐞

- Group profit increases by 48% despite challenging market conditions

- Major claims well below budget at €206.9M

- April renewals with strong premium growth of +18.8%

- Property and casualty reinsurance with combined ratio of 83.6%

- Life and health reinsurance continues stable development

- Capitalization and Solvency II ratio remain very strong

- Investment result above full-year target

- CSM portfolio increases to €8.7B

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭-𝐀𝐮𝐬𝐬𝐜𝐚𝐠𝐞𝐞

"Our consolidated net profit for the first quarter once again confirms the strength of our diversified business model."

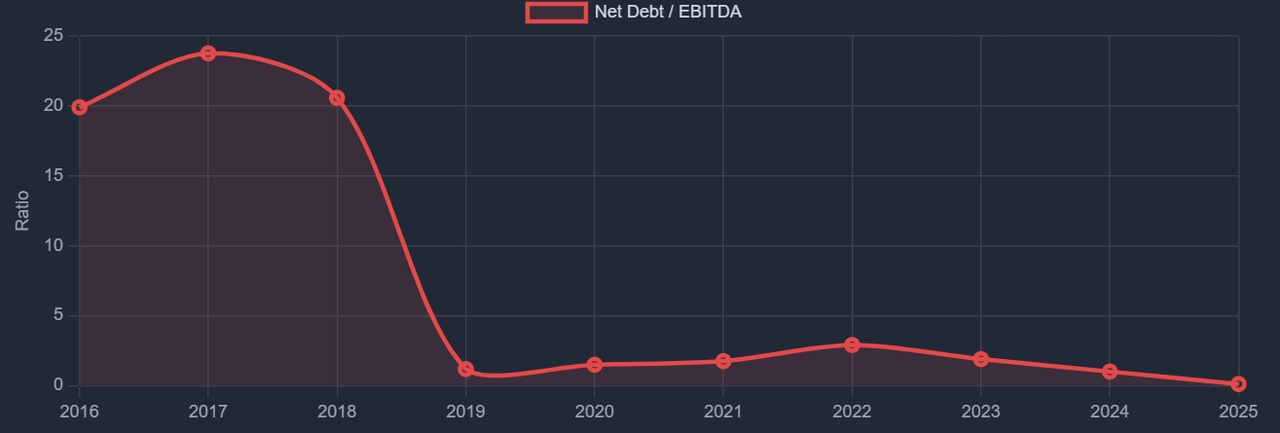

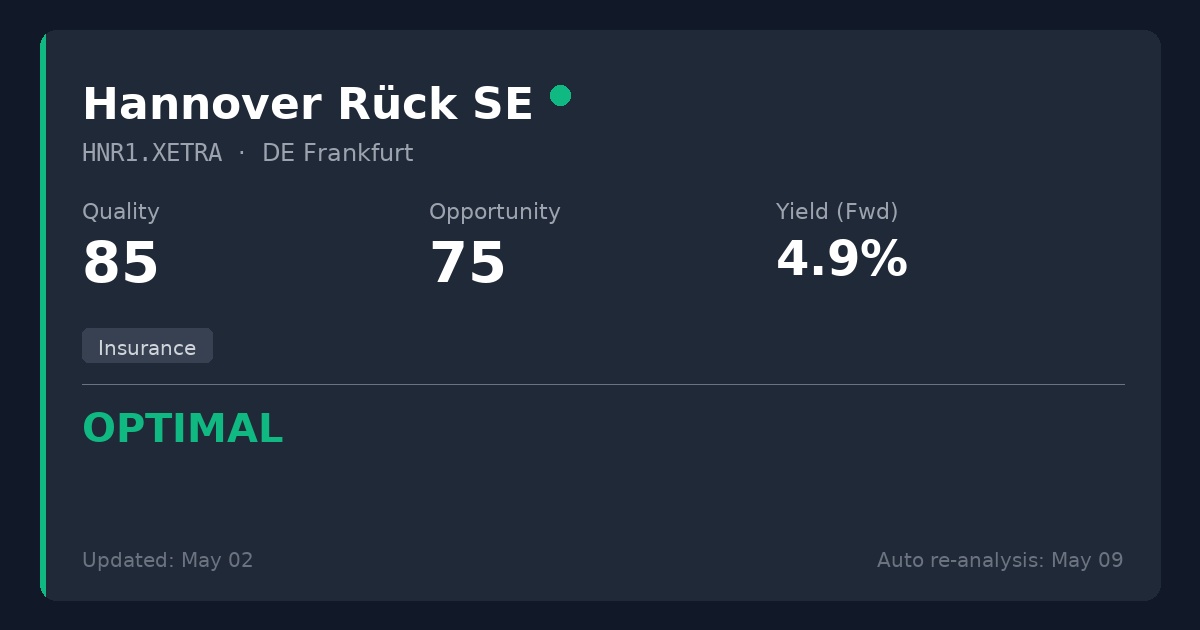

Sharing some current data and context on Hannover Re $HNR1 (-0,54 %) , which is sitting in the 🟢 OPTIMAL quadrant on DividendQuad.

The Quantitative Picture:

• P/E Ratio: 11.74x

• Dividend Yield: 4.88%

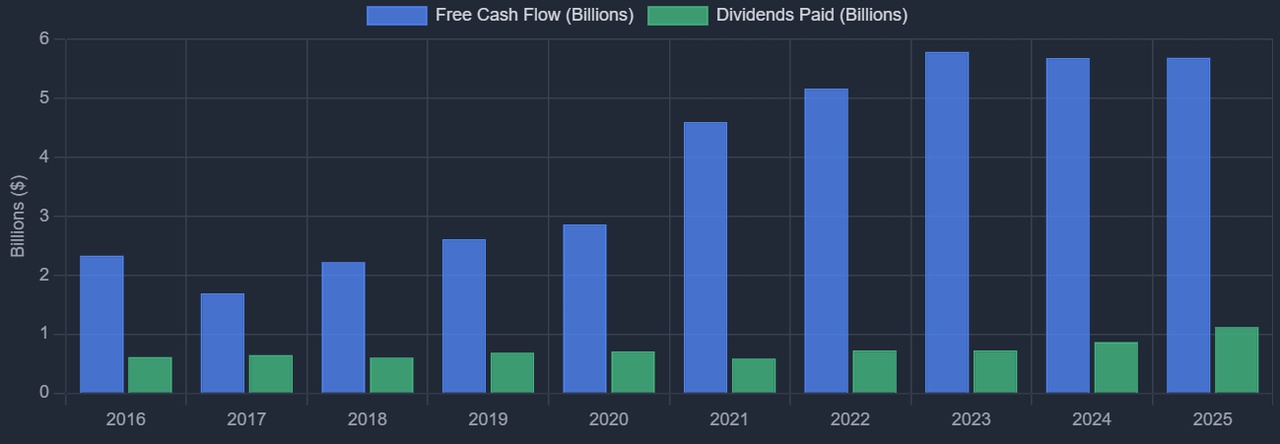

• FCF Payout Ratio: 19.7% (Showing the dividend is well-covered by cash flow, despite standard screeners showing a distorted GAAP payout of >100%)

The Market Context:

The low multiple reflects some specific industry headwinds. The market is pricing in caution due to reports of a slightly softening environment during the 1/1 renewals. Additionally, Hannover Re's strategy of taking on more tail-risk compared to peers (like SCOR) has kept some investors on the sidelines following heavy catastrophic loss years recently.

The Counter-Balance:

Despite those concerns, the underlying financials remain robust:

• 2025 closed with a strong combined ratio below 90%.

• Management is projecting net income of at least €2.7 billion for 2026.

• They actively mitigate their tail-risk exposure by sharing a significant portion of large losses with ILS (Insurance-Linked Securities) investors.

Between the strong cash generation and disciplined underwriting, it's an interesting setup.

(Charts from DividendQuad. Data powered by EODHD).

The shareholders of Hannover Rück SE $HNR1 (-0,54 %) can rejoice: today's Annual General Meeting approved a drastic increase in the dividend to EUR 12.50 per share - an increase of 39%.

Behind this leap lies a historic record result. With a profit of EUR 2.6 billion, the company closed 2025 more successfully than ever before in its 60-year history. CEO Clemens Jungshöfel sees the company in top defensive form despite difficult markets.

For investors, the message remains clear: profitable growth meets an extremely strong balance sheet and a new, generous dividend policy.

15 increases

13 unchanged

7 reductions

Insurance companies

Banks

Utilities

Car stocks

Type here if you like collecting dividends: https://shorturl.at/83W8R

$MBG (-0,16 %)

$ALV (-0,95 %)

$VOW3 (+2,06 %)

$MUV2 (-0,68 %)

$BMW (+0,07 %)

$AIR (-0,4 %)

$CBK (-1,68 %)

$523232

$DTG (+0,65 %)

$DHL (+0,38 %)

$FME (+1,64 %)

$FRE (+0,96 %)

$HNR1 (-0,54 %)

$MTX (+0,01 %)

$RHM (+3,73 %)

$SAP (+0,71 %)

$ENR (-0,18 %)

$BAS (+4,18 %)

$BAYN (+0,19 %)

$BEI (-0,89 %)

$DBK (+4,07 %)

$DTE (-0,93 %)

$EOAN (-0,84 %)

$GEA (+1,01 %)

$IFX (-1,45 %)

$RWE (+0,04 %)

$SY1 (-0,13 %)

$ZAL (+0,17 %)

$ADS (+0,19 %)

$BNR (+1,65 %)

$HEN (-0,52 %)

$MRK (+1,24 %)

$SIE (+0,84 %)

$SHL (+2,83 %)

In 2025, the Talanx Group increased its insurance sales by 5 percent at constant exchange rates to EUR 49.0 billion and consolidated net income by 25 percent to EUR 2,480 million, thus achieving the profit target, which was raised to more than EUR 2.4 billion in the course of the year.

The operating result (EBIT) rose to EUR 5.3 billion, the return on equity to 19.7%, and the Management Board and Supervisory Board are proposing a 33% increase in the dividend per share to EUR 3.60.

Highlights Sales growth: Insurance sales 2025 adjusted for currency effects +5% to EUR 49.0 billion (in euros +2%). :

Jump in consolidated profit +25% to EUR 2,480 million, above the original target of >EUR 2.1 billion and in line with the forecast, which has been raised to >EUR 2.4 billion.

Key operating figures: EBIT +8 percent to EUR 5.3 billion, underwriting result +11 percent to EUR 5.7 billion, return on equity 19.7 percent. :

Proposal to increase the dividend per share by 33% to EUR 3.60; dividend growth thus stronger than the Group result. :

Profit contribution All business divisions contribute to profit growth, primary insurance and reinsurance each make an equal contribution. :

Claims experience Despite the largest natural catastrophe loss in the Group's history in the first quarter, the Group benefited from an unusually low number of natural catastrophes in the following three quarters. :

Strategy Diversification, decentralization, cost leadership and a culture of trust are highlighted as key success factors.

Outlook2026: Confirmation of the profit target of around EUR 2.7 billion and expectation of a return on equity of around 19%; the target originally announced for 2027 should therefore be achieved and exceeded one year earlier. :

Risk information Targets are subject to stable currency and capital markets, expected major losses and a geopolitical and macroeconomic situation that does not escalate further.

Conclusion Talanx shows a very strong and high-quality result in 2025 with significant profit and dividend growth, supported by operational strength, good claims development and a broad, diversified positioning.

The optimistic outlook for 2026 with a targeted consolidated result of EUR 2.7 billion and a high return on equity underlines the ambition to even exceed the company's own medium-term planning, but remains dependent on market and claims developments as well as geopolitical risks.