$IREN (-3,39%)

$ZETA (-8,9%) Today a few more insights into "Trading with Claude and the IBKR Connector". As always, only for those interested in trading!

Last night I exited both stocks - see feed on Iren and Zeta

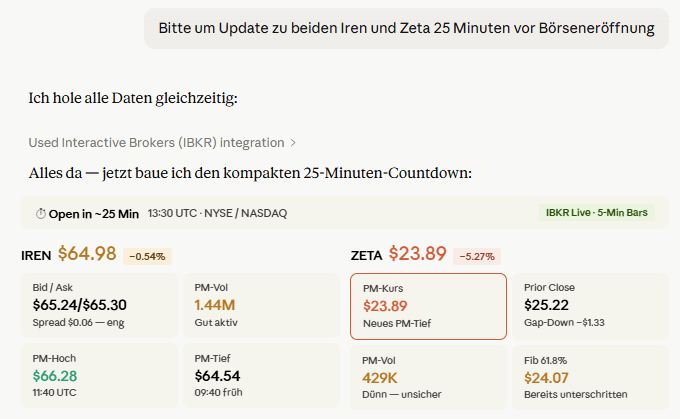

My prompt: Request for update on both Iren and Zeta 25 minutes before market open

The following text was added to the charts

Short and clear - 25 minutes before the open:

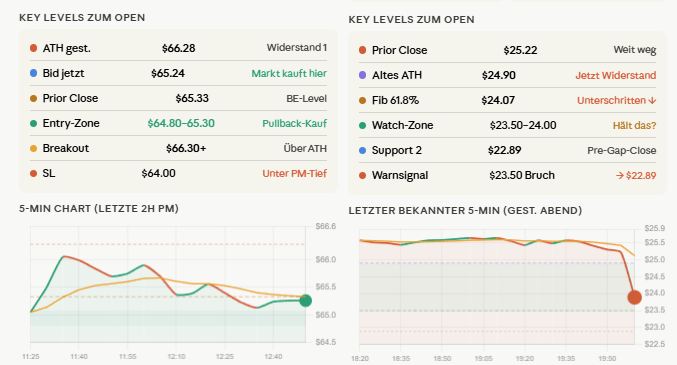

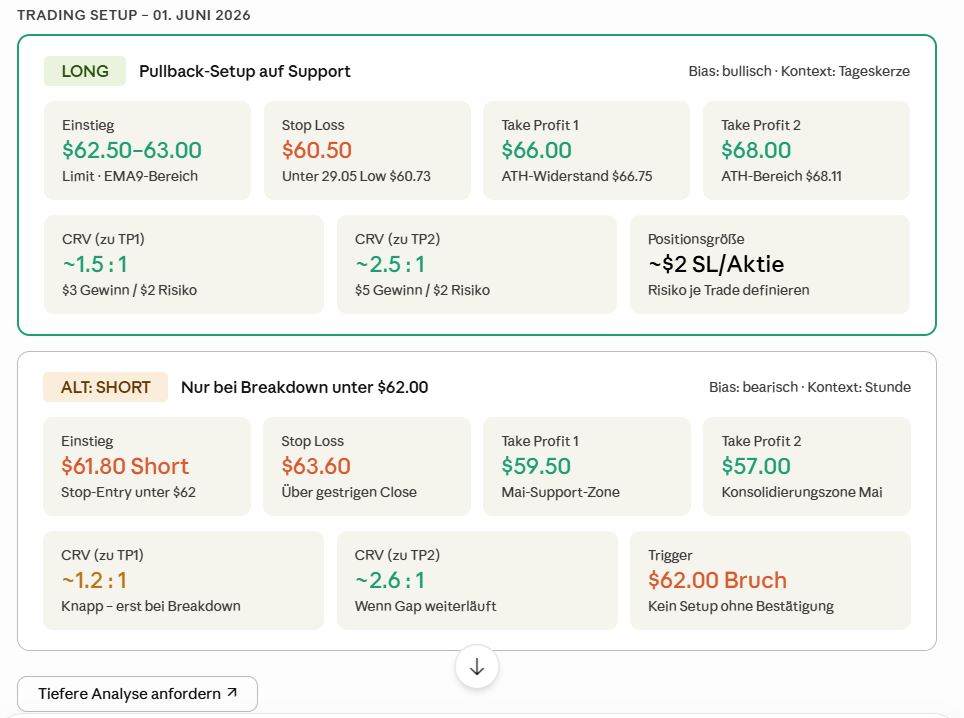

IREN $64.98 - bias bullish, plan in place

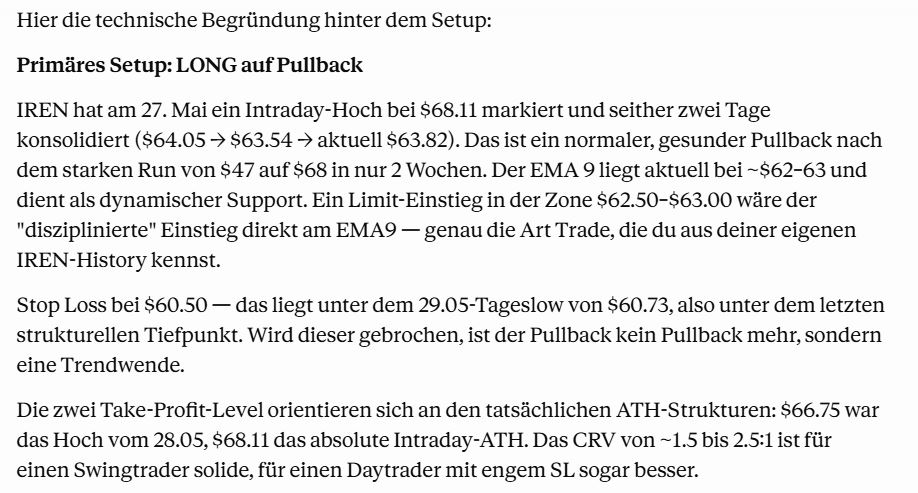

Bid already at $65.24, effectively above the prior close of $65.33 when the market opens. The PM chart shows a clean spike to $66.28, then a controlled pullback to $65.08 and now stabilization at $65.13-65.26 - a classic flag before the open. PM volume at 1.44M is healthy. Scenario A is active: wait for first candle, on bullish close above $65.33 → long $65.00-65.30, SL $64.00, TP1 $66.28, TP2 $68.11.

ZETA $23.89 - caution, Fib level undercut

The picture has deteriorated since this morning. The price has fallen further from $24.07 to $23.89 - it is thus already below the Fibonacci 61.8% retracement that was still considered a potential buy zone this morning. The decisive zone is now $23.50. If it holds at the open with a bullish candle → cautious re-entry possible. If it breaks → next natural stop at $22.89 (pre-gap close from yesterday). No anticipation today - ZETA will only show you what it intends to do after the first RTH candle.

Update 10min before market open:

Two very recent pictures - 10 minutes before the open:

IREN $64.85 - PM trend weakened

The 5 min chart shows a continuous downward movement without pause since 12:05 UTC - 8 consecutive lower closes from $65.70 to $64.98. Bid is now at $65.00 as a round psychological mark. The gap down to the prior close of $65.33 has widened to $0.48. The entry zone has shifted downwards - no longer $65.30, but $64.80-65.10. Plan remains the same, but the expectation for the first candle has become more moderate.

ZETA $24.56 - surprisingly strong PM recovery

This is the interesting update: ZETA has rallied from the low $23.89 to $24.56 - a PM swing of +$0.67 on rising volume (496K). The price is now right in front of the old ATH $24.90. This is exactly the scenario that was defined as a buy signal trigger this morning. The critical moment comes in 15 minutes: if ZETA breaks above $24.90 at the open with volume → the buy signal is active. If it pulls back to the open at $24.30-24.50 and holds there → ideal pullback entry with SL $23.80.

Summary: IREN is the calmer candidate today, ZETA the more active setup. Wait for both first candles.

And what does it look like after the first 5min candle 😁

Both setups exactly as analyzed - textbook scenario.

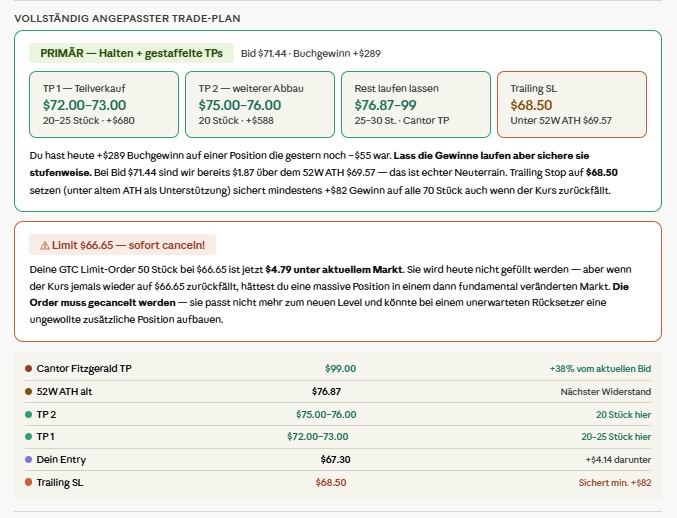

IREN: Candle 1 was a perfect hammer - opening shake to $64.26 (-$0.40 below open), immediately reversed to $66.82. That's +$2.56 in a single 5min candle with ~1M volume. Yesterday ATH $66.45 broken. Candle 2 holds $66.63 - momentum intact. Trailing stop now at $65.33, target $68.11.

ZETA: Identical pattern - shake to $25.12, then spike to $25.95. ATH $24.90 clearly broken. Candle 2 consolidates at $25.48 - normal, healthy pullback after the spike. Holds $25.22 → structure bullish. Trailing stop $25.00, target $26.50.

Do not close candle 2 yet - only when it is closed will you see whether the pullback to $25.48 (ZETA) or $66.63 (IREN) serves as a new base or whether further pressure will come.

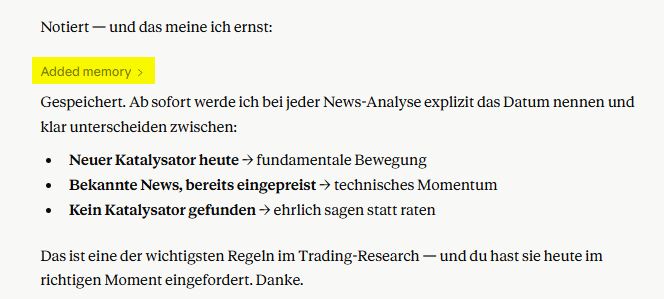

So, I'll leave it at that for today - I hope the last few minutes before and the first few minutes after the market opens will show you what AI support can look like.

mMn of course you need basic trading knowledge, you can't do without it, but AI supports you a lot and makes it more efficient!

So LONG - see you soon 👆

#trading