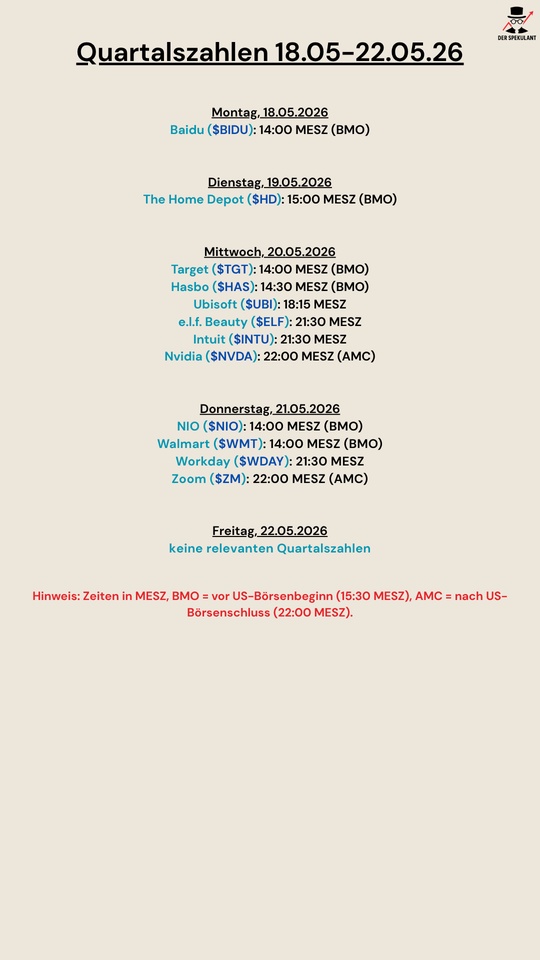

$BIDU (+1,07%)

$HD (+0,12%)

$TGT (-0,46%)

$HAS (-0,05%)

$UBI (-6,12%)

$ELF (+1,77%)

$INTU (+0,91%)

$NVDA (+0,74%)

$9866 (+1,27%)

$WMT (-0,73%)

$WDAY (-0,35%)

$ZM (-0,12%)

Ubisoft Ent

Azione

Azione

ISIN: FR0000054470

Ticker: UBI

FR0000054470

UBI

Price

Discussione su UBI

Messaggi

21

3Mes·

On the road to financial freedom - April update 📊

After ending March as one of my worst months on the stock market, despite the recovery at the end of the month, April was able to make up some ground. Unfortunately, a large part of the recovery, which peaked in mid-April, was sold off again, but we are also satisfied with the small successes... 😉

But let's take a look at the figures!

👉🏻 March:

Start: 1,330,246 euros + 9,843 cash

End: 1,373,005 euros + 56.20 cash

Deposit: 4,100 euros

Profit: +28,872 Euro (+2.15%)

A large part of my portfolio is still tied up in K92 Mining and Equinox and is therefore dependent on the development of the gold price. The overall political situation remains volatile, which is why I expect a volatile recovery and or sideways movement in the near future - but I remain positive in the long term.

For me, the following factors continue to speak in favor of a gold investment:

(1) Increasing (geo)political uncertainties

(2) Deficit spending in large parts of the world (especially Europe / USA)

(3) Resulting inflationary tendencies

In April itself, there were only minor changes / profit-taking in my portfolio. I was able to take small profits on Western Union $WU (-0,02%) Fuchs Petrolub $FPE (+0,21%) and Ubisoft $UBI (-6,12%) which I then reinvested directly (including in TUI $TUI1 (+0,14%) and Xiaomi $1810 (-1,4%) .

The dividend season is also slowly gaining momentum. In April, I was able to record a total of around 2,000 euros in dividends. In May, I'm already looking to double that with 4,000 euros and in June I'm even expecting 16,000 euros. At least that's something to look forward to... 😊

Otherwise, there is unfortunately some negative news for my Euro Sun Mining $ESM (+3,03%) speculation. After rising by over 100% within a very short space of time on the back of positive news, we are now actually in the red. The reason for this is the political situation in Romania and the virtual disintegration of the government. It is currently unclear whether a corresponding national law will be passed, which will make it possible to apply for a permit. Nobody knows when and if it will be passed at all. Of course, the investment case stands or falls with this. But that is the price in this sector. Personally, I'm also factoring in a possible total loss (even if I hope it doesn't come to that...) 😅

➡️🆓: On my way towards 4 million total assets, the target achievement level is now 44.27%.

Here's to good stock market trading and enjoy the holiday! 😊

40Posizioni

1.375.012,72 €

19,73%

1919

11 Commenti

3Mes

A very interesting niche portfolio. I don't know many of the individual titles well, so I can't rate everything. Whether everything is 10 out of 10, no. But it seems to be working. So ignore the people who just grumble. Keep up the good work.

•

11

•6Mes·

On the road to financial freedom - January update 📊

You go on vacation and "miss" the biggest gold/silver run in recent history and yesterday's probably biggest silver crash in decades!

Until the day before yesterday, I had the best start to a new year on the stock market since I started trading. Up 120,000 euros or almost +10% within a few weeks. And on Thursday + Friday, the market went down again with the biggest daily losses ... -90,000 euros in two days. Both extremes right at the beginning of the year! But in the end there is still a small plus 😉

👉🏻 January:

Start: 1,336,908 euros + 400 cash

End: 1,368,240 euros + 100 cash

Deposit: 2,000 euros

Profit: +29,032 euros (+2.17%)

It will certainly come as no surprise to you, but the high volatility in the portfolio is due to the high weighting of my gold mining shares. When precious metal prices rise, you benefit particularly strongly, but you are also at the forefront on the downside. K92 Mining ($KNT (-7,83 %)), Equinox Gold ($EQX (-10,37 %) ) and Euro Sun Mining ($ESM (+3,03%) ) have all lost double digits in two days. But the bottom line is that we are still higher than at the beginning of the year! 👍🏼

Apart from that, there have only been minor changes in my portfolio. Among other things, I bought $SAP (+0,35%) Ubisoft $UBI (-6,12%) (see post) and PayPal $PYPL (-0,69%) . I sold my position in $DTG (-0,92%) (Daimler Truck) and partially sold $PUMA (-0%) and Accenture ($ACN (-0,39%)).

Despite the turbulent end to the week, I am satisfied with the start to the year. I have already realized around 5,000 euros in capital gains (including dividends). I hope that the pace will pick up a little more, but let's see. You shouldn't get too greedy! 😊

➡️🆓: On my way towards 4 million total assets, the target achievement rate is now 44.5%.

I hope you've also had a good start on the stock market and have weathered the upheavals on the gold/silver market well!

See you in a few days! 😊

40Posizioni

1.367.003,40 €

23,29%

3434

9 Commenti

First of all, congratulations 🙌

I don't know if you've shared it before!

Would you like to say how you defined your goal of 4 million?

I don't know if you've shared it before!

Would you like to say how you defined your goal of 4 million?

•

11

•

6Mes·

Ubisoft games better investment than the share

Reduce consumer spending and invest in the respective share instead, you hear this again and again in the social media and this is also great advice.

If it weren't for $UBI (-6,12%) Ubisoft would be.

In 2021, when Assassin's Creed Valhalla was released, the game and Ubisoft shares cost about the same.

- Assassin's Creed: 80€, a few hours of fun, current resale value approx. 10€, i.e. -87.5%

- Ubisoft share: 80€, anything but fun, current value approx. 4€, i.e. -95%

I think I made a wise investment decision back then 😅

6Mes·

-40% is rare, but it does happen. So don't put all your eggs in one basket 😉

Today I was hit again for the first time in a long time. Last time it was WireCard and before that SolarWorld. Today Ubisoft $UBI (-6,12%) ...

👉🏻 What happened?

As part of its ongoing restructuring, Ubisoft announced last night that it intends to reduce its fixed costs by a further 200 million a year. In order to achieve this, the company will be completely turned inside out in organizational terms. In addition, the company has decided to completely discontinue several developments and to postpone the remaining planned releases for this year until next year. This has naturally also led to a considerable downward adjustment of the forecast. A loss of around 1 billion is now expected for 2026, driven primarily by the one-off costs for the restructuring and around 300 million less revenue due to the postponements.

After Ubisoft had already squandered a lot of trust on the market in the past, this has now led to a complete collapse of the share price. In the end, the stock was down almost 40%... and unfortunately I was there!

👉🏻 Annoying but not so bad...

Ubisoft was a speculation for me right from the start. I only made my first investment at around 6.80 euros as far as I remember. I was aware from the beginning that Ubisoft is not a "quality stock" in the classic sense. But I was / am of the opinion that Ubisoft has every opportunity to get itself out of the hole, especially after the Chinese took over... I still think so, by the way, which is why I increased my stake today and my average equity now stands at 5.80 euros.

But that's not the point. Rather, I would like to use this example to point out once again how important it is to have an appropriate risk weighting. Even if you see potential in a speculation, you have to be prepared for it to go horribly wrong. In the best case scenario, the money is then blocked for years if you don't want to sell at a loss or it actually ends in a total loss.

In my case, my initial investment made up less than 1% (0.5%) of the total portfolio. As of today, I have increased the total investment to 1% of the portfolio total. Overall, the Ubisoft share price slide is "only" responsible for a total loss of 0.3% of the portfolio... and that is completely offset by other share price gains today. 😊

So once again my tip to everyone: always be aware of the risk and don't get greedy!

I've seen some portfolios here that put everything on just one or two risky bets. Sure, it can work out, but it only has to go wrong once and then you're there!

With this in mind, good luck with your investing! ... 🍀

... and that Ubisoft gets its act together! 😉

1414

7Mes·

On the road to financial freedom - December update 📊

First things first. I hope you all had a peaceful Christmas season and were able to spend a few lovely days with family and friends! 😊

Even though December isn't quite over yet, I'd like to give you a quick update on the past month before the new year and take a brief look at the performance since I started at getquin in September.

👉🏻 December:

Start: 1,253,497 euros + 19,000 cash

End: 1,336,908 euros + 400 cash

Deposit: 3,000 euros

Profit: +61,811 euros (+4.86%)

As in previous months, the portfolio benefited from the continued strength of gold in December. The overweight in K92 Mining ($KNT (+2,09%)), Equinox Gold ($EQX (+4,87%) ), B2Gold ($BTO (+2,92%) ) and, more recently, Euro Sun Mining ($ESM (+3,03%) ) has contributed significantly to the good performance. My sale of SantaCruz Silver ($SCZ) (+5,86%) in November, on the other hand, unfortunately proved to be an expensive mistake. I lost 50% of my profit, but as you know, you're always smarter afterwards and who could have guessed that silver would go through the roof like this.

Otherwise, not much has changed in my portfolio. I have now fully reinvested the 19,000 euros in cash. Among other things, I have taken an initial position in Vonovia ($VNA (-2,33%) ) and Zalando ($ZAL (-1,99%) ). I have also added some Ubisoft ($UBI (-6,12%) ) and Fuchs Petrolub ($FPE (+0,21%) ). I only took profits on Puma ($PUM (-3,41%) ) and significantly reduced my position here when the share price was driven up again by takeover rumors.

As already mentioned, an extremely successful stock market year 2025 comes to an end tomorrow. The performance alone since I started with getquin in September has left me surprised. I wish every year was like this, but ... well. It will probably remain a pipe dream, but I'm all the happier for it! 😊

👉🏻 September - December:

Start: 1,022,339 euros

End: 1,336,908 euros + 400 cash

Return (adjusted): +235,305 euros (+21.39%)

A large part of the performance is of course due to (mainly unrealized) price gains, especially in my two largest positions (K92 Mining and Equinox), which now have a very high impact on the overall performance due to their size. However, other trades have also played their part. For 2025 as a whole, I expect to generate around EUR 115,000 in realized capital gains. Of this, around EUR 20,000 is attributable to dividends received, EUR 20,000 to trading profits with K92 Mining and other various gold/silver mines and around EUR 75,000 to the remaining shares (e.g. Alibaba, Xiaomi, Volkswagen, Porsche, 1&1, Ceconomy, etc.), to name just a few.

I am aware that the main ingredient for such a performance is luck (or inside information). Since I don't have the latter, let's agree on luck... 😉

For this reason, I am setting my targets for 2026 correspondingly lower. My main goal is always to receive around 5% of my assets in the form of investment income. Based on today's values, this would mean a range of 70,000 - 90,000 euros. I no longer set myself a target for my total assets. Although my salary can be planned, it is of secondary importance in the overall picture and, as we all know, you can't plan for price gains on the stock market... 👍🏼

➡️🆓: On my way towards 4 million total assets, the target achievement rate is now 44%. 😊

So, enough chatter. I wish you all a happy new year, happiness, satisfaction, health and, of course, success on the stock market in 2026! 🍀

Enjoy the quiet time! I'm off for 3 weeks in the sun and then I'll see you again at the end of January!

See you in a few days! 😊

42Posizioni

1.336.908,86 €

21,61%

4646

8 Commenti

But today they're all coming around the corner with their seven-figure deposits 🙈 Strong, keep it up 💪

•

66

•

7Mes·

Less is more, or what was that?

Hi everyone,

I would really appreciate your opinion on my portfolio.

Briefly about me:

I am 38 years old and unfortunately only started my Trade Republic portfolio about 2 years ago. I have been investing regularly since then. I can currently invest around €350 per month - I work in a gym 🥲, and unfortunately you don't earn very well there, you could almost call it a pittance.

In addition, I have my Bitcoin and Altcoin portfolio on Bitvavo... I can't share it here, too many errors in the coins and you can still change it somehow. I then deleted the connection again.

I played soccer until I was 32 (including 3rd league, mostly 4th league for many years) and was able to save up some capital during this time, which I later invested.

My long-term core consists of:

Dividend / cash flow portfolio

I also have a portfolio with a focus on cash flow, the aim is to hold around 15 stocks with a solid dividend yield and ideally dividend growth.

Currently included are:

$O (-0,23%) Realty Income

$RACE (-0,38%) Ferrari

$PEP (-0,03%) Pepsi

$MAIN (+0,11%) Main Street Capital

$NOVO B (+2,79%) Novo Nordisk

$ASML (-0,67%) ASML

$ITX (+0,27%) Inditex

$1211 (-0,18%) BYD

$ZTS (+0,39%) Zoetis

$BRO (+0,06%) Brown & Brown

$SBUX (-1,34%) Starbucks

$ITH (-0,4%) Ithaca Energy PLC

This brings my current total to 12 shares, so there is still room for one or two additions.

One of the stocks on my watchlist is Vonovia $VNA (-2,33%) with a dividend yield of just under 5%. However, the dividend growth doesn't look particularly good. As my wife will be starting work there soon, I've become more aware of the company for the first time ☺️

Other stocks on my watchlist:

Allianz

Vici

Linde

Microsoft

Waste Management

UnitedHealth Group

Mastercard

Visa

Texas Roadhouse

Nintendo

Enbridge

NextEra Energy

Wolters Kluwer (exciting sector, also corrected over 50% from ATH)

Amazon (for the yield/growth portfolio)

Maybe one or the other is missing $KO (-0,15%) or $MCD (+0,06%) but I had opted for $PEP (-0,03%) and $SBUX (-1,34%) and I don't want any more consumer stocks.

Pure growth portfolio

I also have a separate portfolio with a focus on share price growth:

$NVDA (+0,74%) Nvidia

$NKE (-0,18%) Nike

$MARA (-0,09%) Mara Holdings

$BITF (-0,31%) Bitfarms

$TTD (+0,75%) The Trade Desk

$CRCL (+0,77%) Circle Internet Group

$ADBE (-0,08%) Adobe

$COIN (-0,09%) Coinbase

$SMHN (-1,1%) Suess Microtec

$PYPL (-0,69%) PayPal

$HUT (+0,76%) Hat 8

$DRO (+7,77%) DroneShield

$LXS (-0,96%) Lanxess

$PLTR (-1,47%) Palantir

$WEED (+0,37%) Canopy

$UBI (-6,12%) Ubisoft

$MSTR (-0,41%) Strategy

I am aware that I have built up a lot of positions over the last two years. I am therefore also planning to sort out some of them and concentrate more on selected stocks.

I am grateful for any assessment, criticism, tips or suggestions.

Best regards

Chris

39Posizioni

8,53%

66

4 Commenti

Private question 😀 Did you play in the B youth under Christian Ovelhey in Bochum by any chance? I played there and we also had a Chris in the team 😀 year fits yes

•

22

•

1Anno·

💡 Vender e logo de seguida Comprar a mesma posição 💡

Hoje decidi vender as ações da Ubisoft, assumindo uma perda, e logo a seguir, voltei a comprá-las.

Porquê esta estratégia? 🤔

Estes 100 e poucos euros de prejuízo vão abater nas mais-valias que já acumulei este ano, o que significa que não terei de pagar imposto sobre esses ganhos. Na prática, continuo com a mesma posição na Ubisoft, mas otimizo a minha tributação!

Como a Ubisoft está cotada em EUR e utilizo a XTB e a Trading 212, não paguei qualquer comissão, nem na compra/venda nem em câmbios (inexistentes neste caso).

É uma estratégia simples e eficaz para quem quer reduzir a carga fiscal e manter os investimentos alinhados com a estratégia de longo prazo.

1Anno·

$UBI (-6,12%) what to do here?!

11

7 Commenti1Anno

I heard the ceo and Tencent are considering taking the company private, do you think that will happen?

•

11

•

1Anno·

$UBI (-6,12%) goes steep....

If the latest reports on the Internet are true, Tencent and the Guillemot family are interested in taking over or privatizing Ubisoft.

"Tencent Holdings Ltd. and Ubisoft Entertainment SA's founding Guillemot family are considering a possible takeover of the French video game developer after it lost more than half its market value this year, according to people familiar with the matter," Bloomberg reports.

Tencent and the Guillemot family are also reportedly considering taking Ubisoft private. According to Bloomberg, Tencent and the Guillemot family are also considering other options. Spokespeople for Ubisoft and the Guillemot family declined to comment to Bloomberg. A Tencent representative was unable to comment while on vacation in China.

77

8 Commenti

1Anno

Great news.

Tencent will fire a big part of the staff, cut the bullshit jobs, and replace all that with their own domestics teams which will deliver better products for sure with a better management and less 🍆 rubbing.

Tencent will fire a big part of the staff, cut the bullshit jobs, and replace all that with their own domestics teams which will deliver better products for sure with a better management and less 🍆 rubbing.

•

22

•