Accenture

Price

Discussione su ACN

Messaggi

69

Wow, another green month 🫢

My biggest drivers of price movements in July were $ACN (+2,2%)

$MSFT (-0,08%)

$BMY (+0,78%)

in the past few months I have aggressively invested $MSFT (-0,08%) and tried to drawdown to my advantage. I closed out several positions and invested in MSFT . It remains to be seen whether I made the right move.

The stock is trading following the earnings at around €16,500 , and I feel very good about it.

What do you think after the results from $MSFT (-0,08%) ?

Portfólio update!

Hello getquin community!

I just added $NOW (+3,41%) and $ACN (+2,2%) to my portfolio and I’m thinking about starting a position in $MSFT (-0,08%) next. However, adding $MSFT (-0,08%) would bring my total to 18 positions.

Am I over-diversifying or overlapping too much in tech? Would love to hear your thoughts

Out with Verizon, in with McDonald's & Co.🫡

Just yesterday I was a customer… today I’m an $MCD (-0,94%) an investor. Life goes round and round like a merry-go-round… 🙃

Joking aside, since I think that SpaceX

slow-moving companies like $VZ (-0,1%) will slow down even more in the future than they’re already slowing themselves down, I’ve by half and reallocated it to good dividend compounders such as $MCD (-0,94%)

$PAYX (-0,4%)

$MDLZ (-0,66%)

$ACN (+2,2%) .

In my be , things will be more exciting here in the future than with $VZ, and Verizon’s 6.6% dividend yield will be surpassed in 10 years anyway by the dividend growth of the new holdings.

Will the falling knife cut my hands? 😅

It's just a guess, but I'll give it a try… Longrun

Just under 5% dividends with

over 10% annual dividend growth

The stock was sold due to AI fears ...

The bookings from $ACN (+2,2%) are weaker than in previous years, which is why the stock has fallen even further since the earnings report.

Payout Ratio stands at below

50% and, in terms of dividends, is not something to criticize but rather to admire.

Overall, the financial figures were $ACN (+2,2%) always been solid… but that’s no guarantee for the future.

The company is in good financial shape and will carry out a share buyback program totaling $7.5 billion by August 2026.

So far, it’s unclear whether AI will be more of a tailwind or headwind in the future.

Since I usually go against the grain and don’t follow the crowd, I’m giving up on this stock and will act based on the company’s future results.

Temporary Slowdown or Structural Problem?

Over the past few days I’ve been taking a deep dive into $ACN (+2,2%) , and there’s one question I can’t seem to answer with certainty.

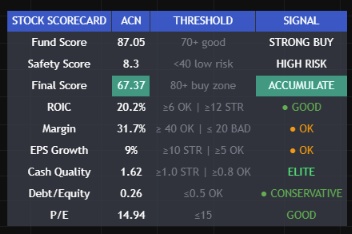

The market has punished the stock by more than 60% since the beginning of 2025, yet the fundamentals still look remarkably strong. Over the last five years, revenue has grown from around $50 billion to nearly $70 billion, net income has increased to almost $8 billion, ROE has remained close to 30%, ROIC has stayed above 20%, and the company generated $10.9 billion in free cash flow in 2025. On top of that, Accenture continues to reduce its share count through buybacks while consistently increasing its dividend.

There are clearly some headwinds. Bookings have slowed, growth has moderated, and the market is questioning how AI could reshape the traditional consulting business. On the other hand, Accenture also appears to be one of the best-positioned companies to help enterprises implement AI at scale.

For now, I’ve set my price alerts at €100 per share. At that level, I believe the margin of safety becomes much more attractive, and there’s a strong chance I’ll start building a position, provided the fundamentals remain intact.

So I’m curious to hear your thoughts.

Am I missing a structural risk here, or is this simply another case of an outstanding business being punished by short-term market sentiment?

They are attribuing to it god-like power when in reality is just a probalistic model with a fancy name attached to it.

Accenture: Good dividend and value

$ACN (+2,2%) Hi everyone! $ACN (+2,2%) has a solid dividend history, I see it as a solid giant in the IT and consulting sector with strong cash flows, and historical valuation right now. Is it a good long-term hold or are you staying away? Let me know your thoughts!

Looking at the chart right now, if you strongly believe in the company, it looks like that now is a very good entry/reinforcement point 👀

Do you have any explanation on why it’s down 55% over the past year though?

The Winners and Losers in AI—From Goldman Sachs' Perspective

After Accenture $ACN (+2,2%) fell by 18% (the stock dropped yesterday to its lowest level since 2017), the entire (consulting) industry was dragged down with it. Capgemini

$CAP (+0,39%) lost 11 percent. Cognizant, Infosys, Wipro, EPAM and Globant were trading lower. Why? Accenture’s business model is based on billable hours. It deploys talented professionals who implement software, restructure processes, and maintain systems at client sites. It is precisely these hours that AI is taking over.

The AI revolution already has its winners and losers. Goldman Sachs has created two thematic portfolios. In the GS US Broad AI includes 94 companies benefiting from AI. The GS AI at Risk contains companies vulnerable to AI, comprising a total of 45 stocks.

Both portfolios start from the same starting point—late November 2022 —after ChatGPT had taken the world by storm—to the present.

The result is clear: The winning portfolio is up 410 percent. That translates to an annualized return of 59 percent per year. The Loser basket stands at minus 26 percent over the same period. That’s a loss of 7 percent per year. The gap between the two stands at around 440 percentage points.

The big winners are the fiber-optic specialist Applied Optoelectronics , up 7,200 percent, SanDisk , up 6,000 percent, and the hard drive manufacturer Western Digital up 2,600 percent, Seagate up 1,900 percent, and Micron up 1,900 percent.

Next up is data center hardware. Celestica rose 3,200 percent, and the cooling and power specialist Vertiv up 2,300 percent, and the equipment manufacturer Argan rose 1,800 percent. Even the laggards in this group of winners are barely in the red. They are the energy providers NextEra, Dominion , and Xcel.

On the other hand, the losers are Globant , down 84 percent, Concentrix down 80 percent, and the payment service provider Bill Holdings down 73 percent, DXC Technology down 71 percent, and the data giant Gartner down 64 percent, the recruitment firm Robert Half and ManpowerGroup each down about 60 percent, and the learning platform Coursera down 62 percent, and Accenture down 57 percent since the end of 2022.

Among the losers, however, there are a few standouts—and they offer valuable lessons. One language AI specialist, SoundHound AI

$SOUN gained 456 percent. Duolingo

$DUOL rose 80 percent, and Verisign

$VRSN (+0,39%) rose by 32 percent. These companies didn’t just put up with AI—they turned it into their own driving force. Duolingo uses AI to make language learning cheaper and more effective. SoundHound has become AI itself. The lesson is: You have to reinvent yourself—and do so faster than AI can eat away at your old revenue.

Source: "Welt" (excerpt), June 19, 2026

Seized the Opportunity: Follow-On Purchase of Accenture

1. Market Leader with a Massive Moat

Accenture isn’t just any consulting firm.

They’re often deeply embedded in:

IT systems,

transformations,

cloud projects,

ERP,

and operations.

Large corporations don’t switch such partners easily.

2. AI Could Help Rather Than Harm

The market is afraid:

“AI is replacing consulting.”

The counterargument:

Many companies don’t even know:

what AI to use,

how to restructure processes,

how to integrate data.

That’s exactly where Accenture makes its money.

3. Less risk than many software companies

Compared to:

Rocket Lab,

Quantum,

Nebius,

MSTR,

Accenture has:

profits,

cash flows,

dividends,

a stable balance sheet.

4. Historically strong compounder

Accenture hasn’t been a hype stock for many years.

But:

High revenue,

high profits,

high dividends,

share buybacks.

Many fortunes are built precisely with companies like this.

5. A Weak Phase Could Be an Opportunity

If the market fear is:

“IT spending is weak.”

and this normalizes in 2–3 years,

then market leaders often benefit disproportionately.

6. AI Valuation Without an AI Multiple

Many AI winners are trading at extremely high valuations.

The bull case is:

Accenture benefits from AI without being valued at 50–100x revenue.

7. Virtually No Survival Risk

A very important point, in my view

With Accenture, the question is rarely:

“Will the company survive?”

But rather:

“Will it grow 5% or 10%?”

That’s a different risk category.

Always tag people—that way, it’s easier to find the post and you can check out the company right away :)

I also think consulting firms will be back on track in 2–3 years!

I work with consulting firms a lot myself, and here’s what I can say:

You always need consulting, no matter what the latest hype is.

24 year old student PF

Hey community,

I am 24 years old, a student and have been actively investing for almost two years. Like many people, my goal is simply financial freedom and not to depend on the pension system later on

I follow a hybrid strategy: a stable ETF core combined with concentrated individual stocks where I have real conviction. No active trading, but buy and hold, unless I notice that a share is getting hot, then I sell and buy again at a lower price when it has corrected.

My underlying strategy:

in the first few years, I blindly followed many trends and other "finfluencers" and didn't always make good and wise decisions as a result. When I invest in individual stocks now, I do so with conviction and that they are future-oriented and will bring me long-term returns.

I would like to reduce the USA share to ~55% in the medium term

I have around €2,500 in cash that I would like to invest now. On my watchlist: $ISRG (+0,97%) Intuitive Surgical , $ACN (+2,2%) Accenture, Space X and $POET (+4,67%) Poet Technologies $AXTI (+19,06%)

I know it's not an exciting portfolio rather basic but maybe I would like to change that :)

I am grateful for any honest feedback, even if it is uncomfortable.