Hi to all the getquin community!

Even though I have been a very active reader, this is my first post here. I just wanted to introduce my portfolio and get as much feedback as possible. First, some personal background:

I am 21, just graduated my bachelor and I’m starting my master’s degree in September. At the same time, I work in research, and I just got a contract extension which guarantees income for the whole length of my master. I manage to invest around 700€ per month, as my salary more than covers my living expenses, while my parents (investors themselves) help me cover rent, as an encouragement for me to invest. I acknowledge I’m very lucky with them and I’m very thankful to have it this easy compared to my peers.

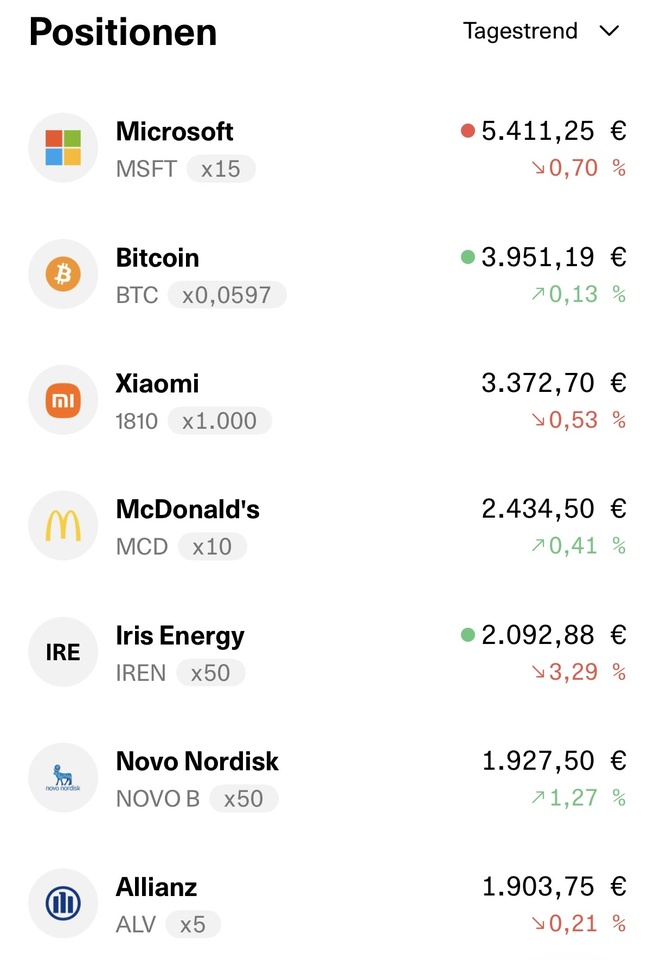

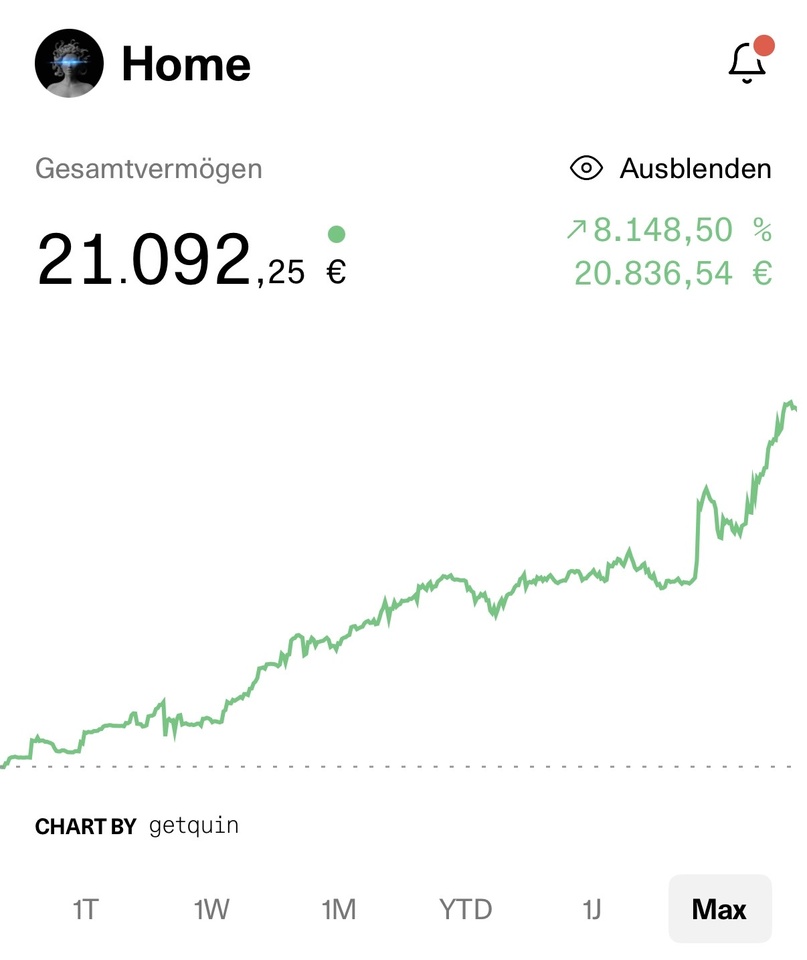

Regarding my investment strategy, since I am young and have a long time horizon ahead of me, I have always preferred a very aggressive portfolio. After making some mistakes with riskier individual trades in the past, I decided to shift toward a more balanced but still growth-oriented approach by integrating ETFs. The goal is to use a monthly savings plan to build a solid foundation while keeping a cash buffer on the sidelines to pick up individual stocks when good opportunities come up.

Starting this month, I am putting 650€ per month into a new automated savings plan. I decided to restructure the ETF side of things by introducing two new funds (instead of only $WEBN (+0,11 %) and $EIMI (+0,49 %) ): $WIRE (+0,8 %) and $IEFM (+0,54 %).

Here is why I made this switch:

First, I chose $WIRE (+0,8 %) because I want to invest in the massive increase in energy and infrastructure demand coming from the tech sector. I deliberately wanted to avoid just buying more semiconductor companies, as I already have plenty of exposure to them in my individual stock picks. $WIRE (+0,8 %) lets me target the clean energy and grid infrastructure side instead. Second, I added $IEFM (+0,54 %) to give the portfolio better geographic balance. The individual stocks I own are heavily concentrated in the US market, so adding a European momentum fund helps diversify that risk while still maintaining an aggressive growth focus. The rest of the savings plan runs with $WEBN (+0,11 %) and $EIMI (+0,49 %) . I am aware that $WEBN (+0,11 %) has exposure also to emerging markets, hence why the monthly share in $EIMI (+0,49 %) is now the smallest, just to have the possibility to only sell part of the EM exposure in the future if needed.

I would really appreciate any feedback or critiques on this setup, the balance between the ETFs and single stocks, or how you would manage the cash sideline. Thanks a lot to anyone who takes the time to reply!