June marks the end of my second-worst month on the stock market since I started keeping records... It’s not all sunshine and rainbows. But hey, you’ve got to be among the worst performers sometimes so that things can get better again in the future! 😉

Here’s an overview of the portfolio in May:

👉🏻 June:

Starting balance: 1,398,020 euros + 72.39 cash

End: 1,219,254 euros + 428 cash

Deposit: -3,000 euros

Loss: -175,410 euros (-12.55%)

The loss is mainly due to the continued decline in the price of gold and the associated drop in mining stock prices. For this reason, I remain calm about this situation, because anyone who has been investing in mining stocks for a while is familiar with these fluctuations. At this point, there’s no need to worry about it yet.

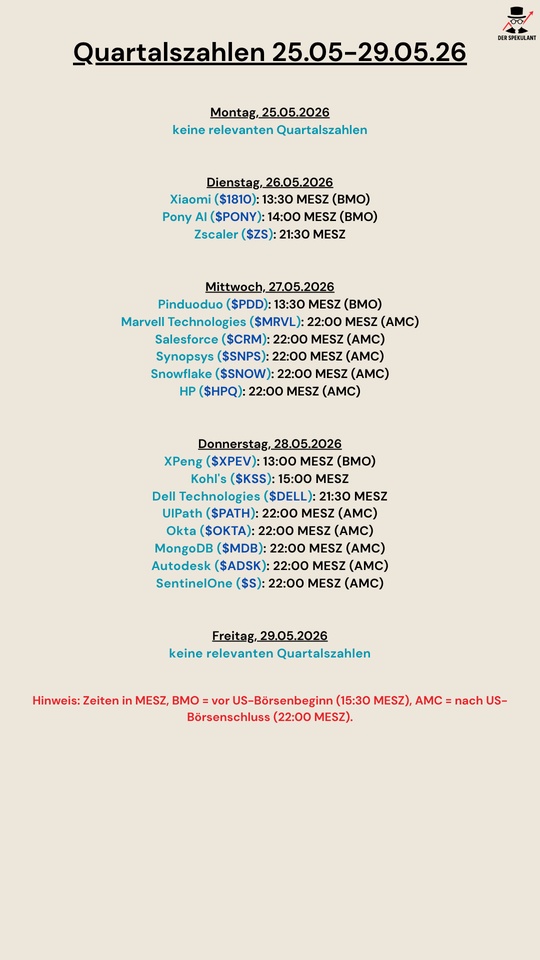

In addition to mining stocks, however, automotive stocks $P911 (+0,07%) (Porsche) and $VOW (-0,27%) (Volkswagen), as well as Chinese stocks $BABA (+0,51%) (Alibaba), $PDD (+1,93%) (PDD Holding), and $1810 (+7,5%) (Xiaomi). I selectively bought more shares in these.

In addition to the (unrealized) price losses, there were also a few instances of profit-taking here and there this month. On the bright side, this month also marked my strongest dividend month of the year—and of all time. All in all, I received 16,600 euros in gross dividends. The main contributors were Volkswagen, Porsche, and—by far the best dividend payer— $BIJ (+0,95%) (Bijou Brigitte) 👍🏼

I’d say I’ll check this month off my list and look forward to July—after all, it seems to be off to a reasonably good start. If that isn’t a good omen... 😊

Bad months are just part of the deal!

➡️🆓: On my way toward 4 million in total assets, I’m now 40.35% of the way there.

Here’s to successful stock market trades! 😊