$XEON (+0,01 %)

$XEOD (+0,01 %) What interest rates are you currently paying on loans that you use to buy shares?

This question occurred to me yesterday when I used the recovery to sell some positions. As usual, I parked the freed-up cash directly in the XEON.

Why did I link this thought to the XEON?

In day trading, I always short stocks, but only on an intraday basis. By shorting the XEON, I could theoretically "borrow" money very flexibly at currently around 2% p.a. and invest it specifically in weak phases in the event of market distortions. As the XEON is currently rising at a stable rate of around 2% per year, this value basically corresponds to my "financing costs".

Fees? For smaller amounts, the borrow fee and interest on sales proceeds almost balance each other out, so that essentially only the spread costs remain. At the same time, the whole thing would be extremely flexible, as the XEON can be traded at any time.

As long as I have enough cash available, this is not relevant for me! It was more of a theoretical thought experiment.

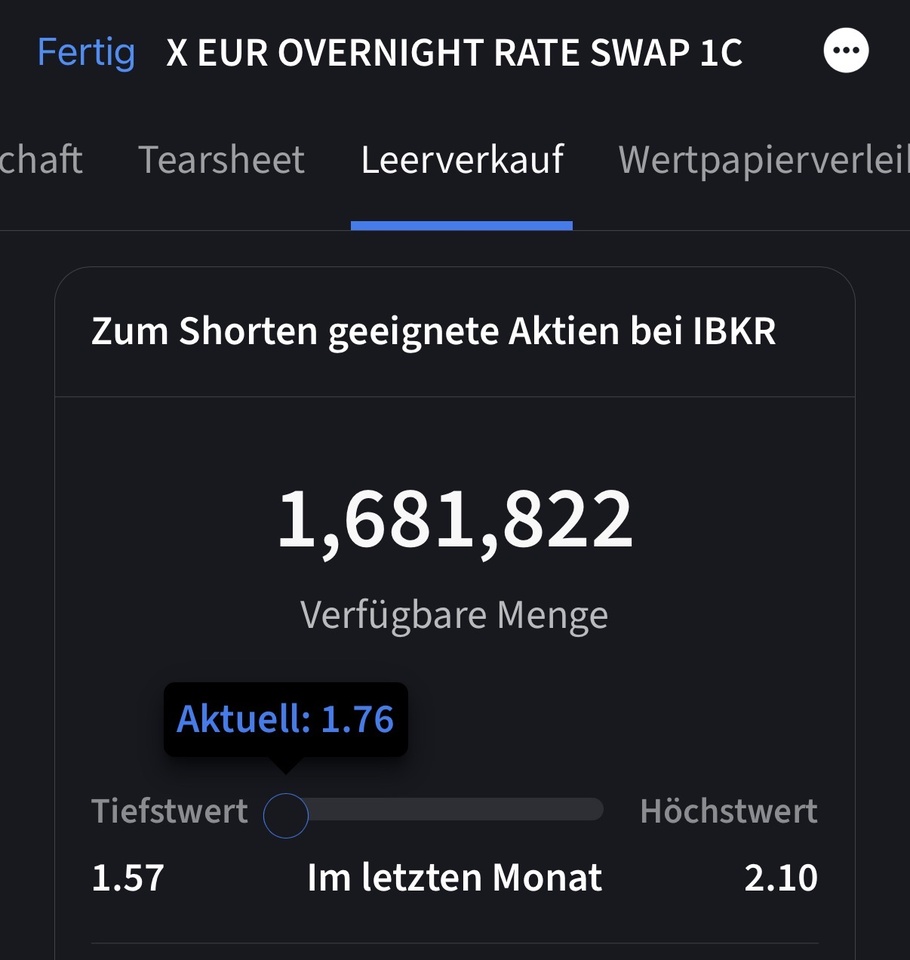

I then also checked this with IBKR: The XEON is actually short-sellable there, currently with a holding of approx. 1.6 million shares.

Sounds like a kind of hack to get "credit cash" flexibly and cheaply at any time, provided you have a broker like IBKR with a margin account. Or have I made a mistake somewhere 😵💫

Have any of you ever taken the same approach and shorted STR overnight?

@GoDividend Alternative to your building society project?