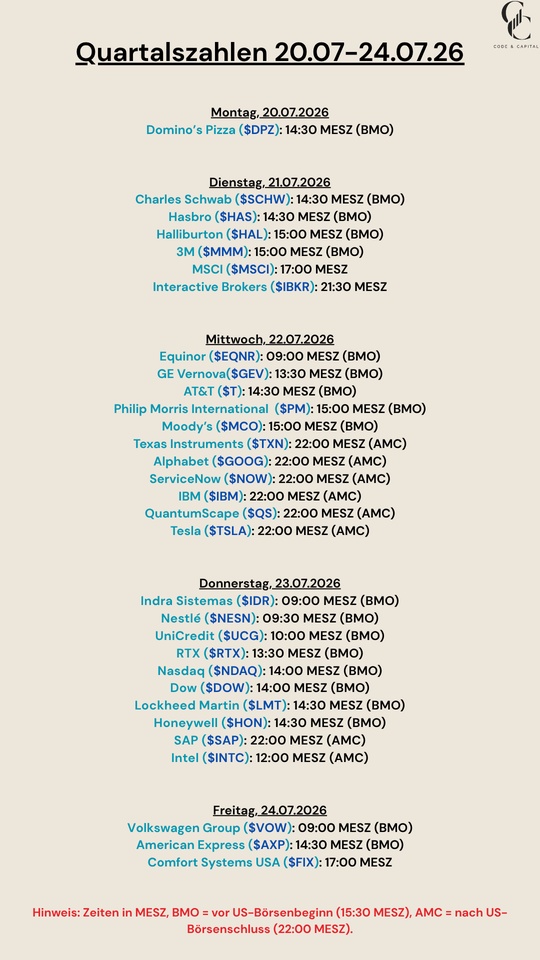

Hello, everyone,

I'm staying invested in my software stocks. How about you?

$SAP (+0,62 %)

$NEM (-2,24 %)

$ADBE (-3,91 %)

$INTU (-1,95 %)

$ADSK (-0,5 %)

$ROP (-0,29 %)

$CPRT (-2,29 %)

$SNPS (-0,78 %)

$MSFT (-1,78 %)

Many investors have already written off software stocks. But what if artificial intelligence doesn’t destroy their business models—but instead makes them more valuable?

The days of software companies like Adobe, SAP, and Nemetschek are numbered, and their business models will become obsolete—this narrative has recently dominated the stock markets. The result: billions in market value were lost. Adobe fell 43 percent within a year, SAP 48 percent, and Nemetschek as much as 56 percent.

But recently, there have been increasing signs that call this view into question. Denis Machuel, CEO of Adecco, the world’s largest staffing agency, told the Reuters news agency that artificial intelligence (AI) will not trigger a job apocalypse or lead to massive job cuts. Nvidia CEO Jensen Huang also considers the assumption that so-called AI agents will render traditional software obsolete to be unfounded.

This raises the following question, particularly for investors who have recently had to absorb heavy losses in software stocks: Are the supposed losers of the AI boom poised for a comeback?

Software Companies Could Now Follow in the Footsteps of Chip Winners

Stefanie Dyballa, portfolio manager at KSW Vermögensverwaltung, sees a good chance that software companies will now catch up after chip manufacturers. AI does not render software obsolete, but rather enhances its utility. “AI agents require applications, data, and processes, making powerful software more important than ever. Established providers stand to benefit from this,” says Dyballa.

So far, investors have primarily favored companies that provide the technical infrastructure for AI—such as Nvidia, Micron, Taiwan Semiconductor, Marvell, Seagate, Western Digital, and Dell. These companies are considered the “shovel makers” of the AI boom because they provide the chips, memory, and hardware on which AI applications run.

With share price gains of more than 500 percent in some cases within a single year, they were among the biggest winners. SAP, on the other hand, has been among the weakest DAX stocks since the start of the year, down about 35 percent. But according to Dyballa, there are growing signs that the tide could be turning.

Why AI Doesn’t Work Without Software

The decline in share prices of many software and data analytics companies—such as Adobe, Intuit, Thomson Reuters, Autodesk, Roper, Copart, and Synopsys—stems primarily from concerns that AI will eventually take over tasks for which companies previously required software subscriptions. Fewer subscriptions would mean lower revenue and profits. The result would be the loss of thousands of jobs.

Jensen Huang disagrees with this assessment. He emphasizes that the markets are underestimating the impact of AI on the software industry. AI will not replace software, but rather enhance it and even increase its use. Companies will need more software in the future, not less—but it must be developed in such a way that AI agents can use it.

In this context, Dyballa points to the transition to so-called agent-based AI systems. These do not operate in isolation but access enterprise software, databases, and existing workflows. Software will not be replaced as a result, but will become the operating system for AI agents.

Why Data Is Becoming a Decisive Competitive Advantage

This trend is particularly evident in the example of the German software manufacturer Nemetschek. The company sells software for highly specialized applications in the fields of architecture, structural engineering, physics, construction management, and building management. Many investors fear that AI will eventually generate construction plans and 3D models at the push of a button, thereby rendering specialized software obsolete.

However, analysts at Deutsche Bank and JPMorgan consider this assessment too pessimistic. They cite three key reasons.

- First, with platforms such as Allplan and Bluebeam, Nemetschek has proprietary CAD and BIM data built up over decades. AI is only as good as its training data. Open AI models cannot simply replace this sensitive industry data.

- Second, the company is already integrating AI into its own products, for example through the Bluebeam Max features or the acquisition of the AI planning tool mbue. Rather than being displaced, Nemetschek is using AI to make its own offerings more attractive.

- Third, liability and precision play a crucial role. In the construction industry, AI systems cannot afford to make mistakes. Incorrect structural analysis or design data can cost millions and endanger human lives. Nemetschek’s software therefore remains the authority that verifies AI-generated designs.

Investors Are Rediscovering Software Stocks

The first reactions are already evident on the stock market. Following recent statements by Nvidia CEO Huang, numerous software stocks rose significantly. “Investors are realizing that AI not only increases the demand for computing power but also gives rise to new generations of software,” says Dyballa.

Companies such as Adobe, SAP, and Nemetschek have recently benefited from this revaluation. There is another advantage: AI tools boost the productivity of software developers. According to the expert, this reduces development costs, brings innovations to market faster, and could increase profit margins—a combination that is often viewed positively by the stock market.

Despite new opportunities, the risks remain high

Nevertheless, caution is still warranted. AI-native startups are increasing competitive pressure, and established providers must consistently adapt their products to the new agent-driven world. “Those who miss this shift will lose market share,” warns Dyballa.

For investors, therefore, careful selection remains crucial. Especially in markets with high barriers to entry and where sensitive customer data is processed, established providers such as SAP, Microsoft, and Nemetschek are likely to maintain their strong positions for the time being.

Added to this are compliance, liability, and security requirements that limit the use of autonomous AI systems. If Denis Machuel and Jensen Huang are correct, the next phase of the AI revolution is therefore unlikely to take place solely in data centers, but rather primarily in the software that companies use every day.

https://www.t-online.de/finanzen/boersen-news/id_101356350/sap-adobe-nemetschek-stehen-software-aktien-vor-dem-comeback-.html