What a wild year so far, one record after another, so it's time for an update and a rough overview of the portfolio.

First of all, some rough facts:

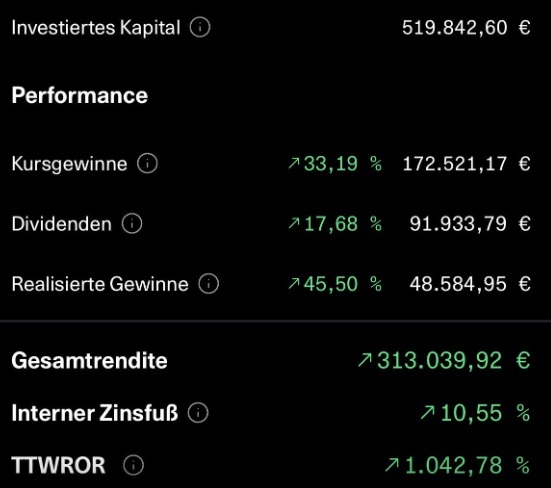

- just under a year ago I was able to report a portfolio balance of 600k euros, now it's already just under 700k ... that's crazy

- I currently have total gains of over 300k (current performance, dividends, sales)

- my total historical gross dividend will crack the 100k mark this year

The portfolio balance is of course only a snapshot and I am therefore particularly pleased about the dividend development. At the end of this year it will be well over 20k. So far, so good ... what do the details say?

Changes in the portfolio:

Ok, what has happened in the portfolio since the beginning of the year?

I have sorted out some low performers, including $MMM (-0,03%)

$COK (-2,34%)

$LAND (-0,76%)

My $INTC (-2,75%) I also sold my position completely in 3 steps, after the last purchases around 20$ this is currently too much euphoria and above all a crazy valuation. $ROP (-0,79%) I have reduced my position a little, which is only possible after a holding period of 4 years, simply to spread it a little more widely. I will also do that from time to time.

The money freed up by the sales has not yet been completely reinvested, but the majority of it has. With $EIX (-4,58%) and $BKW (-1,41%) I have built up a separate energy share and that $DTE (-0,46%) is now also in the portfolio - I'm in. My $XDJP (-0,35%) ETF is doing splendidly and my $XD5E (-0,01%)

$VFEM (+1,17%) and $VAPX (-0,82%) ETFs are doing well and will be expanded further. Otherwise, a lot has flowed into existing candidates (e.g. $ABBV (-2,62%) or $PG) (+0,08%)many US stocks have been increased and $BRK.B (+0,39%) bought a little more. The CHF portfolio was increased by $ZURN (+0,93%) , $SLHN (-0,39%) , $VZN (-2,86%) and the $PGHN (-0,74%) and $BCHN (+0,87%) I have increased my purchases.

Oh and yes, the chip shop $NOVO B (-8,33%) still seems to be alive :-)

My savings plans are continuing as usual, regardless of the current mood. The aim remains to build up a decent passive income with dividends in the long term.

I would say it's going well 🤓