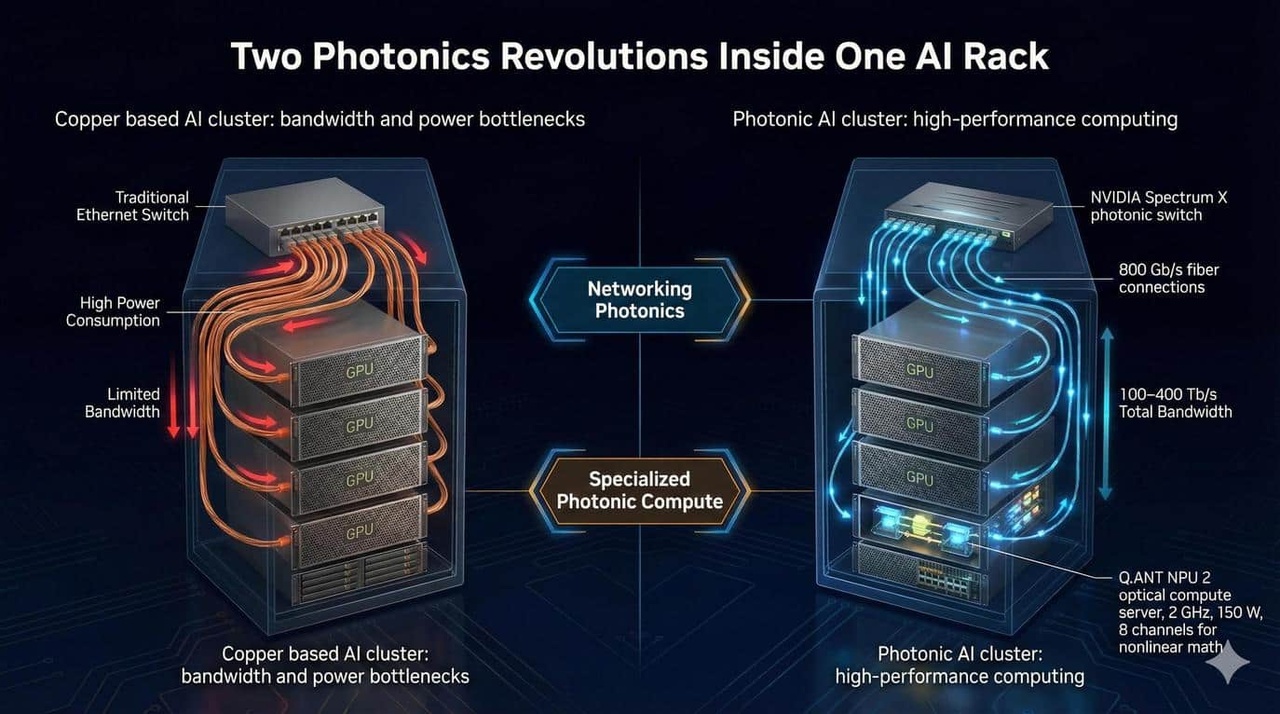

The photonics industry has virtually completed its first major cycle - some players are still taking the last leg, others are already making corrections.

One basic idea is the difference in weight between electrons and photons, which massively reduces the energy required to transmit a datum in transmission lines - keyword fiber optics.

The more interesting part, however, is the spreading of the binary logic in light wavelengths in the CPU in order to be able to calculate in a defined space/frame with a higher base than 2. These analog protocol options are physically unlimited, as there is no longer a base number.

In my view, this is one of the most disruptive markets of the next few years.

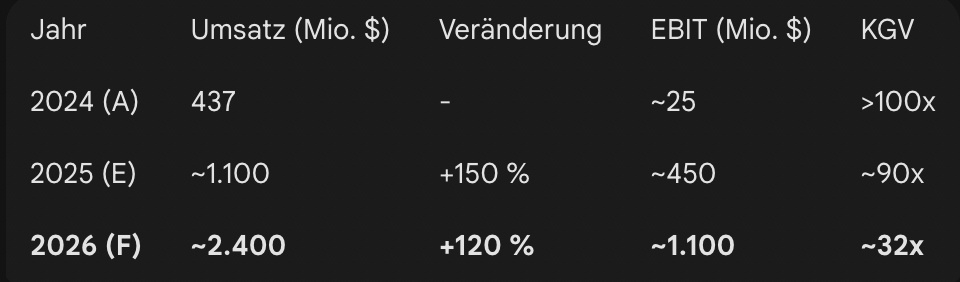

For the watchlist

Q.ANT (IPO pending) https://qant.com/de/

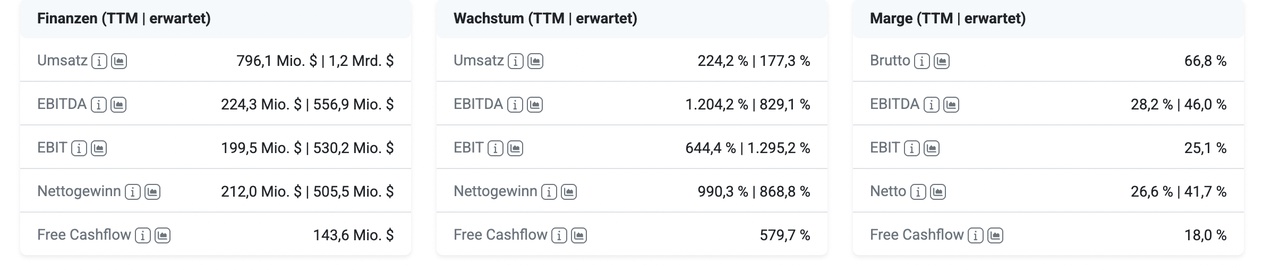

From a chart technical point of view $CRDO bottoming out since the beginning of February, accumulation is still possible. Average price target $199 (+86%).