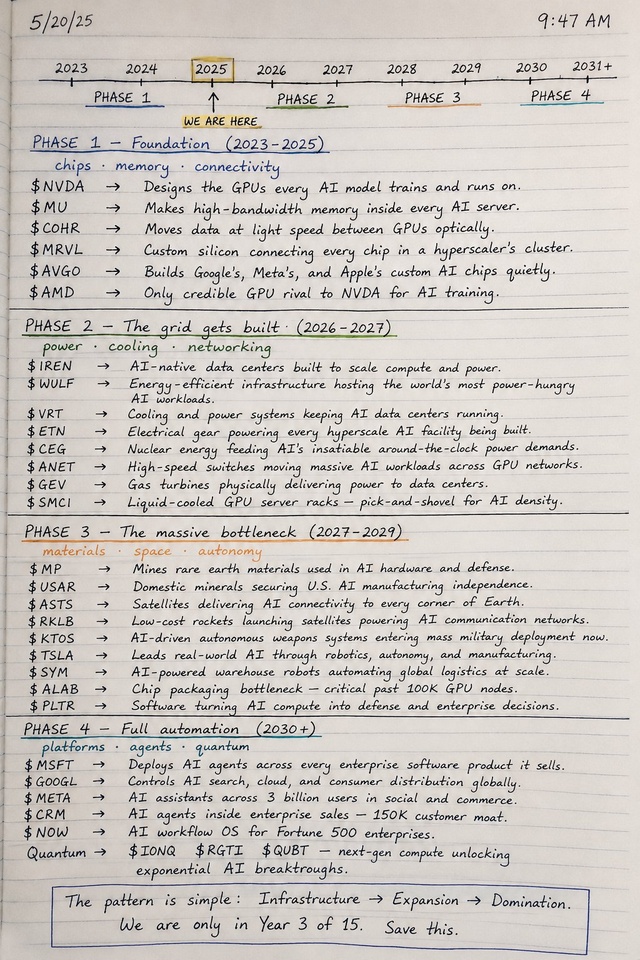

You'd make millions by knowing whats coming and buying dips until 2030+

Pay attention, we just finished Phase 1 2023-2025

chips · memory · connectivity

$NVDA (+2.16%) → Designs the GPUs every AI model trains and runs on.

$MU (+11.34%) → Makes high-bandwidth memory inside every AI server.

$COHR (+3.28%) → Moves data at light speed between GPUs optically.

$MRVL (+10.34%) → Custom silicon connecting every chip in a hyperscaler's cluster.

$AVGO (+2.91%) → Builds Google's, Meta's, and Apple's custom AI chips quietly.

$AMD (+8.03%) → Only credible GPU rival to NVDA for AI training.

PHASE 2 — The grid gets built (2026–2027)

power · cooling · networking

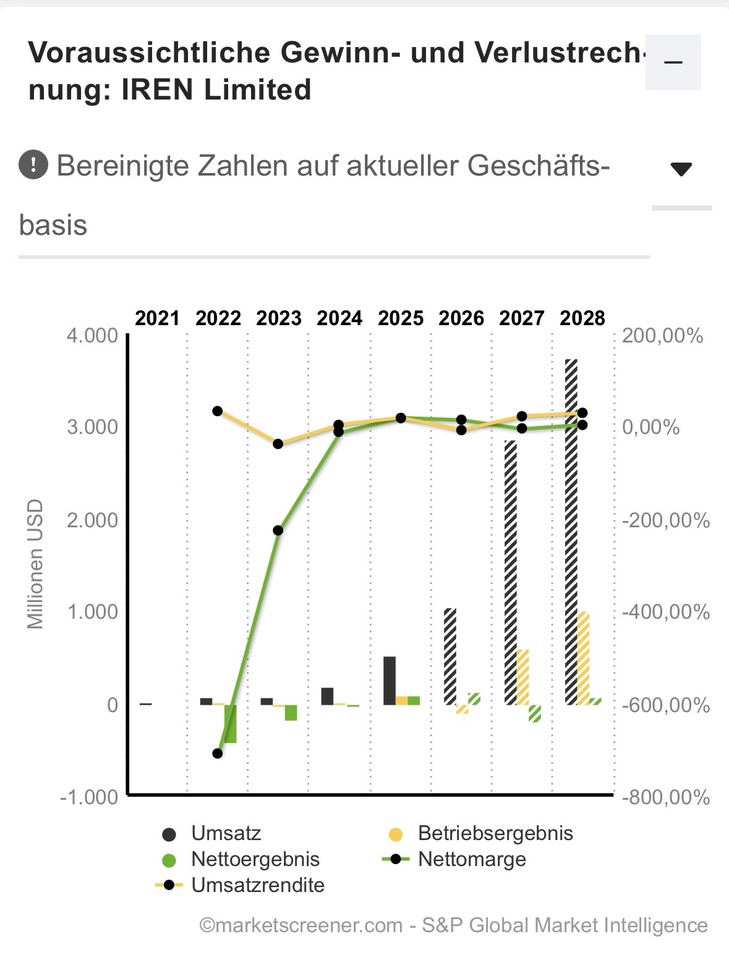

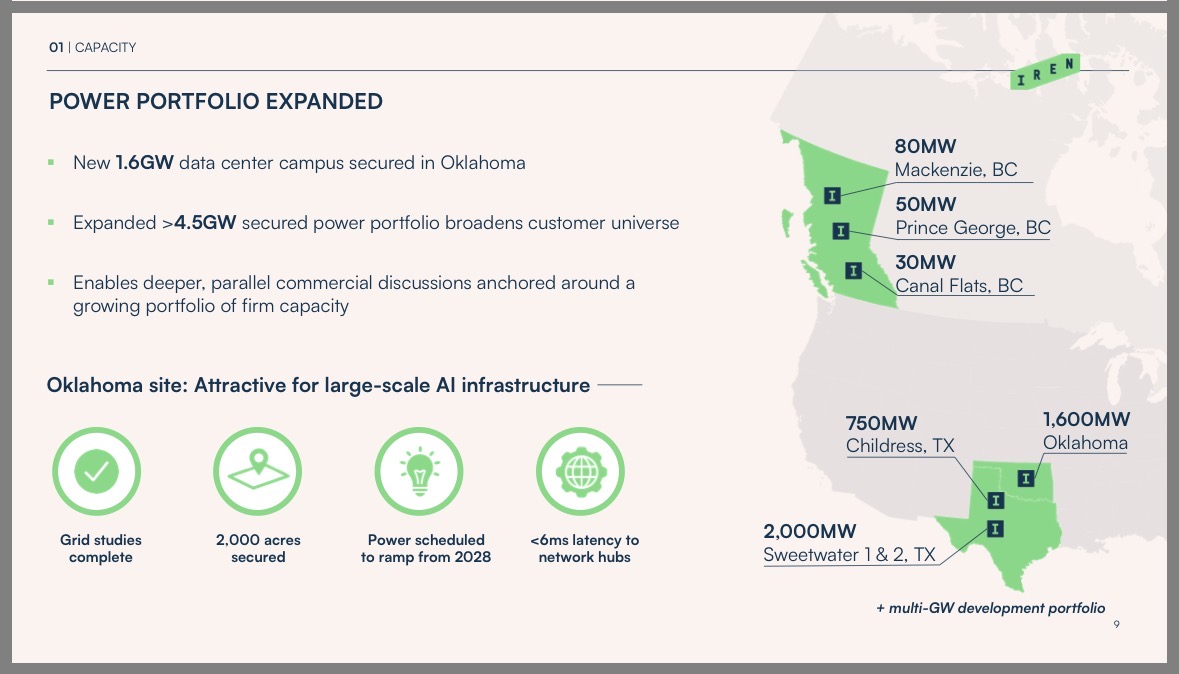

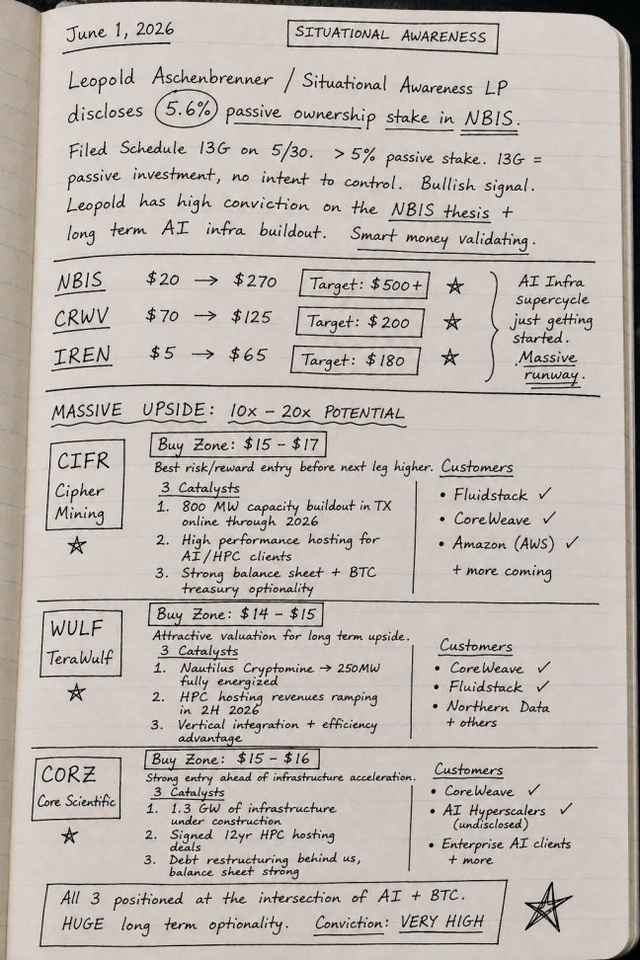

$IREN (+11.81%) → AI-native data centers built to scale compute and power.

$WULF (+9.81%) → Energy-efficient infrastructure hosting the world's most power-hungry AI workloads.

$VRT → Cooling and power systems keeping AI data centers running.

$ETN → Electrical gear powering every hyperscale AI facility being built.

$CEG → Nuclear energy feeding AI's insatiable around-the-clock power demands.

$ANET → High-speed switches moving massive AI workloads across GPU networks.

$GEV → Gas turbines physically delivering power to data centers.

$SMCI → Liquid-cooled GPU server racks — pick-and-shovel for AI density.

PHASE 3 — The massive bottleneck (2027–2029)

materials · space · autonomy

$MP → Mines rare earth materials used in AI hardware and defense.

$USAR → Domestic minerals securing U.S. AI manufacturing independence.

$ASTS (+15.84%) → Satellites delivering AI connectivity to every corner of Earth.

$RKLB (+12.62%) → Low-cost rockets launching satellites powering AI communication networks.

$KTOS → AI-driven autonomous weapons systems entering mass military deployment now.

$TSLA (+3.99%) → Leads real-world AI through robotics, autonomy, and manufacturing.

$SYM (-0%) → AI-powered warehouse robots automating global logistics at scale.

$ALAB (+10.54%) → Chip packaging bottleneck — critical past 100K GPU nodes.

$PLTR (+1.36%) → Software turning AI compute into defense and enterprise decisions.

PHASE 4 — Full automation (2030+)

platforms · agents · quantum

$MSFT (-1.97%) → Deploys AI agents across every enterprise software product it sells.

$GOOGL (+0.28%) → Controls AI search, cloud, and consumer distribution globally.

$META (-0.47%) → AI assistants across 3 billion users in social and commerce.

$CRM (-2.72%) → AI agents inside enterprise sales — 150K customer moat.

$NOW (-1.41%) → AI workflow OS for Fortune 500 enterprises.

Quantum

$IONQ $RGTI $QUBT — next-gen compute unlocking exponential AI breakthroughs.