The journey is the destination,

Up the stairs, down the stairs.$NVDA (-0.9%)

$VWCE (-0.19%)

Posts

512The journey is the destination,

Up the stairs, down the stairs.$NVDA (-0.9%)

$VWCE (-0.19%)

Hi everyone! 🤝

Since I’ve been following along here for a while now, I’d like to share my portfolio again today to get your feedback. A little about me: I’m 31 years old, work as a team leader in product management, and have a very clear long-term investment horizon (buy and hold).

I’m currently contributing €800 a month to my investment account.

🔍 The Current Situation

My portfolio is currently quite concentrated and heavily influenced by my convictions in the tech sector:

The foundation: The FTSE All-World $VWCE (-0.19%) ETF, which makes up just under 27% of my portfolio.

The individual stocks: The remaining positions are spread across a handful of selected, high-performing individual stocks (primarily Big Tech and AI infrastructure).

The largest positions in my portfolio are currently held by Amazon $AMZN (-1.76%) (~15%), Visa $V (+0.17%) (~10%), and Microsoft $MSFT (-0.06%) (~9.5%).

Crypto: Bitcoin $BTC (-0.62%) currently accounts for about 8% of the invested capital.

Cash holdings (not visible in the portfolio): I’m currently holding about 10% in cash on the sidelines.

🎯 My plan for the near future

Even though individual stocks have performed well so far, I’d like to make the portfolio structure a bit more defensive for the future, while also diversifying it across sectors. My focus for the coming months:

1. Massively expand the core: I want to gradually increase the FTSE All-World’s weighting well beyond the 30% or even 40% mark to strengthen the global foundation.

2. Reduce Big Tech & rotate satellite holdings: I plan to strategically reduce my significant overweight in the Big Tech sector somewhat. The capital freed up will instead flow into other promising satellite positions to diversify the portfolio beyond U.S. tech.

3. Targeted use of cash reserves (50/50 split): The 10% cash reserve will soon be used for buying on dips. The plan is set: 50% of it will go directly into Bitcoin, while the other 50% will be split between the ETF and selected stocks.

💬 I’d love to hear your thoughts!

As a product manager, I like to critically evaluate my strategies. That’s why I’m asking the community:

1. Cash allocation: Do you think the 50/50 approach for the cash buffer (half crypto, half traditional market) makes sense, or would you reallocate it differently given the sell-off in Big Tech?

2. Looking for exciting satellite investments: When you look at my portfolio—which sectors or themes do you think are completely missing as complementary investments if I reallocate out of Big Tech?

I’m looking forward to an exciting discussion and your honest feedback! 📉📈

#portfolio

#investing

#ftseallworld

#etf

#bigtech

#aktien

#bitcoin

#crypto

#cash

#langfristig

#sparplan

#finanzen

#diversifikation

So far, I have a savings plan in the $VWCE (-0.19%) FTSE All-World ETF for each of my four children (aged 6, 6, 10 and 15).

Would you add anything else, for example $TDIV (-0.46%) or anything else?

Have a great weekend, everyone!

Hi All,

I wanted to share an up date on my portfolio I have just reached a milestone which I had been working towards for years!

a little bit about myself.

I am 33 years old working in finance and started my investment journey just under 3 years ago with an initial starting capital of €3000.

Ever since then I have been consistently investing in $VWCE (-0.19%) but I also held a small position in $BTC (-0.62%) which I sold recently to focus more on my core strategy. I have a very simple portfolio which I like.

My monthly dépôt ranges from €500 - €1000

My next goal is to hit 75k and the magical number of 100k!

Good evening,

I recently turned 19 and have been investing since I was 18. My investment horizon is 50+ years.

Lately, I’ve been thinking about adding a satellite position to my portfolio, for example Microsoft. On the other hand, I’m wondering if that would actually improve my portfolio, or if I should simply continue investing in $VWCE (-0.19%) only.

What would you do in my situation?

(please ignore vwrl, it is an experiment)

This is my first post. I have this four positions to mantain for 20 years.

I invest 100€ every month and in June and December 300€. I have this since January 2026. How can I improve this invest?

$VWCE (-0.19%) 35%

$CHIP (-0.49%) 18%

$XNAS (-0.47%) 40%

Hi everyone,

I'm currently thinking about selling my SAP shares and $VWCE (-0.19%) , since SAP has been a real drag on my portfolio’s performance over the last few weeks.

The loss allocation would also come in handy, since I’ve already used up my tax exemption allowance and am still expecting some dividends.

What are your thoughts on this?

Thank you very much!

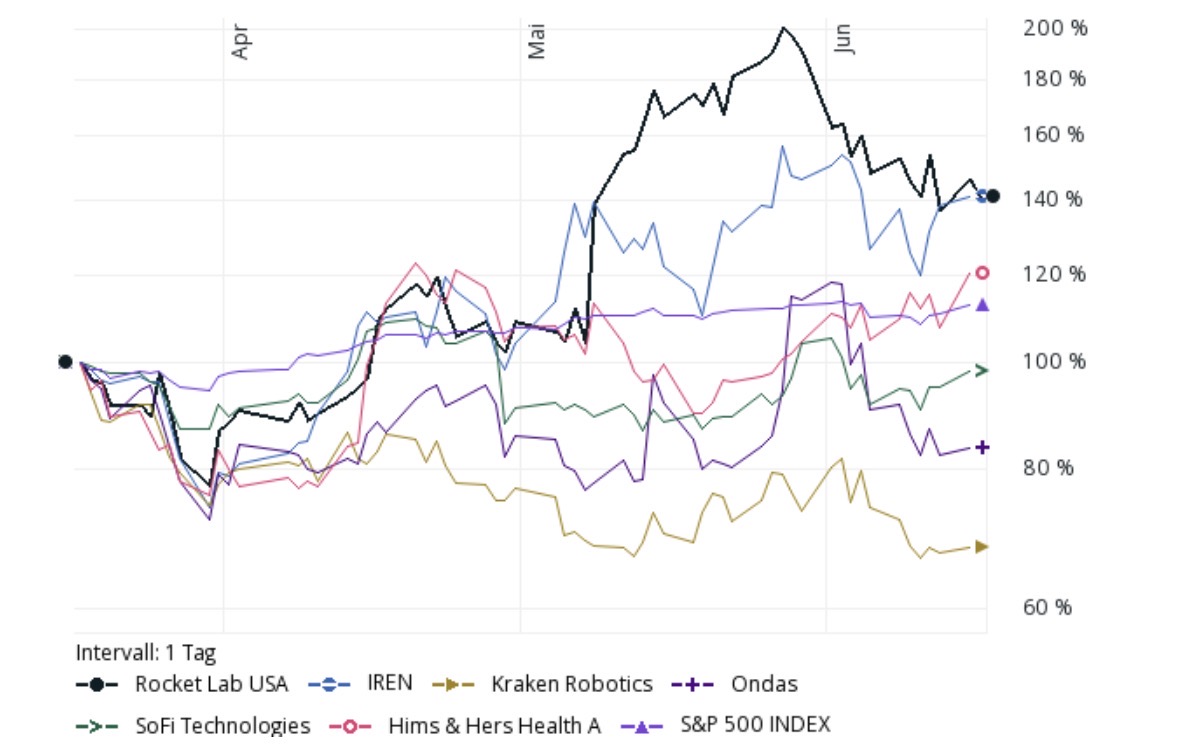

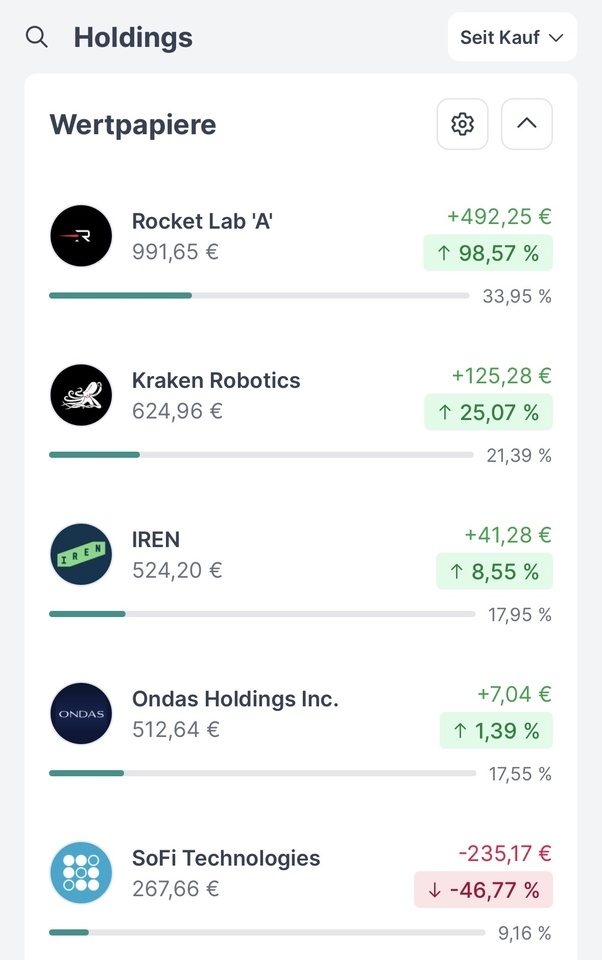

Compared to the previous month, $RKLB (-0.82%) last month, it apparently headed back toward Earth instead of toward the Moon. $IREN (+1.94%) In contrast, its recovery continued this month as well.

Let’s take a look together at the current status of the project Tenbagger der Zukunft :

As a reminder: The project started with approximately €2,500, which was divided almost equally among the five securities in the portfolio.

$HIMS (+0.22%) was sold at a loss of almost exactly 50%. For the new stock, $ONDS (-0.35%) was topped up to €500 again—ultimately resulting in 64 shares in the Tenbagger portfolio.

Below are the five stocks you selected for the project and their performance to date since November 12, 2025:

Since inception:

Last 30 days:

_________________________

The beta value is: 2.48 (previous month: 2.03)

A stock’s beta (β) measures its

Marktvolatilität relative to the overall market: A beta of 1 means the stock moves in tandem with the market; a beta > 1 means it fluctuates more (e.g., at 1.5, it rises or falls by 1.5% when the market rises or falls by 1%); a beta < 1 indicates lower volatility, while a beta < 0 indicates a movement opposite to that of the market. It helps investors assess a stock’s systematic risk (market risk).

_________________________

Due to the sometimes high volatility, the values are as follows:

Rocket Lab: 34%

Kraken Robotics: 21

Ondas Holdings: 18%

Iris Energy: 18%

SoFi Technologies: 9%

_________________________

Return:

Since the start of the project:

The portfolio's return is (taking accounting for the loss of $HIMS (+0.22%) ) currently positive and stands at +6.6% 📈, compared to+17.5%📈.

The return hit its low point on November 21 at -17.7% 📉, and its peak on January 16 at +23.7% 📈.

For comparison:

Since the start of the project, the return on the

S&P 500 has been: +11.75%📈 $VUSA (-0.29%)

FTSE All World: +14.25%📈 $VWCE (-0.19%)

Since the beginning of the year (taking accounting for the loss of $HIMS (+0.22%) ):

+6.6% 📈

_________________________

Below is the performance over the last three months, including the previous value$HIMS (+0.22%) as well as the $VUSA (-0.29%)

As always, I’d love to hear your thoughts! :)

+ 1

Top creators this week