After the stop loss of $ENPH (+0.77%) has pulled (thanks to the great rise last month even in the plus :-) and the allocation of $CEC (+0.05%) is no longer to my liking, I used the freed-up cash to add a Mag7 to the portfolio for the first time and invested the rest of the proceeds in the $IS3R (-0.56%) put the rest of the proceeds into the I'm pleased that my portfolio looks a bit tidier again, and further adjustments are already planned.

- Markets

- ETFs

- iShares Edge MSCI Wld Mntm Fctr ETF A

- Forum Discussion

iShares Edge MSCI Wld Mntm Fctr ETF A

ETP

ETP

ISIN: IE00BP3QZ825

Ticker: IS3R

IE00BP3QZ825

IS3R

Price

Discussion about IS3R

Posts

45

8Mon·

ETF chaos - how best to merge?

Hello everyone,

I have "some" chaos in my ETF portfolio. I would like to tidy it up a bit and start with the ETF stuff.

I have

Abbreviation / Weighting / Current balance of total portfolio

$DBXW (+0.57%) / 9,68% / +16,39%

$IS3R (-0.56%) / 5,91% / +14,97%

$IWRD (+0.26%) / 5,5% / +13,4%

$500 (+0.92%) / 4,01% / +18,76%

$VWRL (+0.58%) / 1,85 / +17,67%

$INRG (+0.23%) / 0,15% / -22,92%

$IEMA (-0.3%) / 0,04% / +20,20%

I'm already thinking OMG as I write this down :-D

Perplexity says the following

Specific recommendations

- DBXW, IS3R, IWRD, 500, VWRL are all broadly diversified equity ETFs with a focus on the world, MSCI World and S&P500. The largest overlaps are between DBXW (Xtrackers MSCI World), IS3R (iShares Core MSCI World), IWRD (iShares MSCI World) and VWRL (Vanguard FTSE All-World).

- Even your S&P500 ETF already tracks a large proportion of the MSCI World ETFs, as US equities are usually dominant there.

- VWRL is more global and covers not only industrialized countries, but also emerging markets. IEMA specifically covers emerging markets, but is a mini-position for you.

Combine / simplify

- You could consolidate all World ETFs (DBXW, IS3R, IWRD) into a single one, for example IS3R or VWRL, depending on your preference in terms of costs and tracking difference.

- You can also remove the S&P500 ETF if you prefer a global ETF such as VWRL or a World ETF - otherwise the US dominance is doubled.

- You can sell very small positions such as INRG and IEMA or switch to a larger "core ETF", as they have little effect on the overall portfolio and increase complexity.

- In the end, you could work with one or a maximum of two broadly diversified ETFs, e.g. only VWRL or IS3R plus a random favorite for special regions/sectors, if desired.

Model structure after simplification

ETF share after simplification

VWRL 80-100%

possibly INRG/IEMA/Satellite max. 10-20% (optional)

--

- Var. 1 So then actually sell everything and put it in VWRL?

- Var. 2 Alternatively, so that I don't have to pay tax on all the profits now, just save the $VWRL (+0.58%) and stop the rest and just leave it? So that I don't have to pay taxes and lose 25%+ directly for the reinvest.

Or what is your idea for Var. 3?

I find the $IS3R (-0.56%) also exciting in terms of momentum.

11

9Mon·

Feedback on the strategy

Hello everyone,

I appreciate your feedback on my strategy.

I'm in my mid-50s and we currently put aside €2,900 every month. 1,900 goes into

$B161SX (+0.05%) to build up reserves. Current annual return 1.9%.

The aim here is to reach €50k in the next 20 months in order to be able to make the upcoming investments in the house.

As soon as this is achieved, I will reduce the savings in favor of the ETF's and in the next 5 years we will have paid off all debts and the free amounts will also go into asset accumulation.

Dream goal at the start of retirement 500T€UR. 😉

50% of the remaining €1,000 will go into

and 10% each in

$RBOT (+0.48%) and

I want to monitor the performance of the two momentum ETFs to see whether they outperform the MSCI World and the Eurostoxx600. Over the next 12-24 months, I will then switch depending on the results.

I am still holding on to the existing individual stocks in order to sell them at a (larger) profit and have no time pressure here, even with the stocks in the red.

My price target is

$AIR (+2.5%) 240-250€

$CCL at 28-30€

$LHA (+1.77%) at 9-10€

and the rest should bring 20-30% when I sell them.

This year I have still been working a lot with direct investments (currently +20% in 2025) but will continue to reduce this. The funds released will then go into the above-mentioned ETFs according to the above key.

I'm leaving out crypto, as the topic doesn't appeal to me, and commodities are too volatile for me, and gold is currently too expensive, even though many people are saying that we'll soon be at 5T€UR.

I look forward to your feedback or questions if something is unclear.

BG

15Positions

€65,549.83

0.73%

55

7 Comments

Kai@Dividenden-Sammler

9Mon

•

55

•Show answer

9Mon·

Just a big thank you to this community!

Hi ,

my name is Karsten . I have lived all the years of my life without paying much attention to stocks and stock markets. At some point I completed my VWL and saved monthly in a European equity fund, then a fund policy was added, which at least put its amounts into a good international equity fund. In 2020, I then started to get to grips with the stock market and saved monthly in ETFs - without going into the typical beginner's mistakes in detail :-) sometimes more, sometimes less, wildly into various ETFs, so that at some point there was an ever-increasing number of ETFs with a savings rate of around € 150 :-) 2024 then gradually gathered more information and for about a year now a consistent monthly savings rate in six ETFs, which I am happy with:

45% $IS3R (-0.56%)

15% $VNRA (+0.89%)

11% $LCUJ (+0.05%)

11% $IEEM (-0.41%)

11% $MEUD (+0.41%)

A few months ago I started to read more and more information about individual stocks, valuations, strategies etc. ..... And here I would just like to say thank you to many people here, for example @BamBamInvest , @Multibagger , @Tenbagger2024 , @Aktienfox and others !

I started investing in individual stocks about 3 months ago - 85% is consistently put into savings contracts, 15% of the capital is for individual stocks. I thought to myself, hey - people spend € 100 on golf or fitness clubs - if you have such expenses, these funds are invested in further stock education :-) The first month was a plus / minus zero game ( so better than the monthly fee for the golf club ), the last two months have averaged € 450 plus with a lot of learning effects and moments - what a pleasant situation : € 300 were put into the monthly savings plans and thus doubled the savings rate, € 150 invested for the family ( food / cinema ) - I am already aware that there are currently strongly rising prices / markets and it requires rather a certain skill not to make these small profits in this momentum. In any case, for the time being I've only looked at momentum / short-term stocks and now with $AMZN (+1.71%) and $QCOM (-0.14%) also invested in two stocks that I see as longer-term investments.

In any case, a big thank you for this community - it broadens my horizons immensely, including the fact that I now know many companies that are, for example, in the $VNRA (+0.89%) and $WSML (+0.42%) are listed !

If I have something meaningful to say, I will be happy to speak up more in the future, but I grew up with the value system "If I can't contribute anything, I'll just shut up" or as Roger Wilhelmsen once said so beautifully ." Where do most people get all their ignorance from"

6666

8 Comments

Thank you for the kind words, the community is really great and it's nice to be able to help each other. Good luck for the future 😊

•

3030

•

1Yr·

Presentation of multifactor portfolio

estimated reading time: 4 minutes

Twenty years ago, the new market crash wiped out my first stock market money and my ego. I swore off the stock market, but my pension certificate showed me that ducking out has an expiry date.

So the first attempts to start again followed. Here on Getquin, I have learned from positive critical voices from e.g. @DonkeyInvestor and @Epi that there is more to it than "just picking something". Since my last post 6 months ago, this was followed by extreme late-night brooding, Excel monsters, AI research, reading Kommer and countless "new agains".

I have tried to read up on modern optimization models such as Mean-Variance, Black-Litterman and Fama-French etc. and implement them in the best possible way.

The result was this portfolio!

As thoroughly tested as you can in a private garage, and coupled with the insight that we only have to leave the uncontrollable to chance.

And one thing first. I am convinced of this and will not change it.

I just want to share my thoughts and ideas about the direction with you. It's difficult to really explain every detail here, I'm sure I could do it better in a conversation, but that's not possible here. I can assure you that the selection and combination definitely makes sense - at least for me and the construct. Among other things, it was important to me to be able to control individual regions separately. I think I have achieved that.

Global (30%)

- SPDR MSCI All Country World, $SPYY (+0.74%)

- L&G Global Equity UCITS ETF, $LGGG (+1.16%)

- iShares Edge MSCI World Momentum, $IS3R (-0.56%)

- Xtrackers MSCI World Value, $XDEV (+0.12%)

- Invesco Global Active ESG Equity, $IQSA (+0.62%)

- VanEck World Equal Weight Screened, $TSWE (+0.54%)

- VanEck Morningstar Developed Markets Dividend Leaders, $TDIV (+0.77%)

USA (31.5%)

- L&G US Equity, $LGUG (+0.94%)

- iShares MSCI USA Mid-Cap Equal Weight, $IUSF (+0.85%)

- JPMorgan BetaBuilders US Small Cap Equity, $BBCS (+0.63%)

- SPDR MSCI USA Small Cap Value Weighted, $ZPRV (+1.02%)

Europe (17.5%)

- HSBC EURO STOXX 50, $H50A (+0.86%)

- L&G Europe ex-UK Quality Dividends Equal Weight, $LDEG (+0.2%)

- SPDR MSCI Europe Small Cap Value Weighted, $ZPRX (+0.62%)

Emerging markets (19%)

- iShares Edge MSCI Emerging Markets Value Factor, $5MVL (-0.92%)

- UBS LFS MSCI Emerging Markets ETF, $EMMUSA (-0.35%)

- L&G Emerging Markets Quality Dividends Equal Weight, $LDME (+0.23%)

- SPDR MSCI Emerging Markets Small Cap, $SPYX (+1.63%)

Japan (2%)

- L&G Japan Equity UCITS ETF, $LGJG (-0.02%)

Ø TER = 0.25%

In summary, this gives the following breakdown

Regional breakdown

- USA (North America) ~ 48%

- Asia ~ 22%

- Europe ~ 22%

- UK ~ 3.6%

- Japan ~ 4.4%

Market capitalization

- Large Cap ~ 52%

- Mid Cap ~ 26%

- Small Cap ~ 22%

The portfolio deliberately allocates its capital to the regions and - where possible - to all capitalization classes. The world building blocks provide the global beta; value, momentum and quality satellites add factor premiums. In the USA, a complete large/mid/small stack provides a pronounced size bias, while Europe receives a value bias via quality and small value ETFs. The emerging layer combines large-cap value stocks, quality leaders and a small-cap module - a diversification anchor beyond the developed markets.

Due to the almost equal weighting of the 18 positions, the Herfindahl index of ETF weights falls to ~633; indirectly, the portfolio contains several thousand individual stocks. The weighted TER is ≈ 0.25 % p. a., spreads below 0.1 %. This means that, compared to a $GERD (+0.69%) a favorable multifactor portfolio myself.

The factor tilts (value 42 %, size 35 %, quality/div ≈ 12 %, momentum ≈ 8 %) increase the expected volatility moderately to 18-20 % p.a.; however, historical data on small and value indices indicate 1-2 percentage points additional return over long horizons. Large caps remain present at around 52 %, mid caps at 26 % and small caps at 22 % support the size premium .

With my "multi-factor all-cap portfolio", I combine global market coverage with five proven premiums, without cost or concentration ballast. Of course, I will have to endure additional fluctuations, but I believe that I have created a robust source of returns over the long term.

I have tried to consider everything and leave nothing to chance, except the uncontrollable.

Anyone who has made it this far. Thanks for reading.

I'm looking forward to your feedback.

PS:

YES, I have Bitcoin😉 and also two themed ETFs. They just stay like that.

- ARK AI & Robotics ETF, $AAKI (+0.73%)

- HanETF Future of Defense ETF, $ASWC (+1.58%)

- ETC GROUP CORE BITCOIN, $BTC1 (-0.79%)

---

no investment advice; DYOR

Thanks also to @VPT , @Mister_ultra , @Ph1l1pp , @ShrimpTheGimp , @MoneyISnotREAL , @Staatsmann and @Smudeo for commenting and providing approaches.

2121

117 Comments

Completely overengineered in my view, but that's how you want it 🤷🏻♂️ You might get a little factor bonus, but that's it. You don't have any effective protection against heavy crashes or years of dry spells, for example. It wouldn't be worth the effort for me.

•

2525

•

1Yr·

How I am now getting back into ETFs (and why I even bought an MSCI World)

Dear community, I have recently and also previously explained from time to time why I find the MSCI World in particular stupid and why I don't enjoy investing in such an ETF. If you want to know the exact reasons for this, you can also read about it here: https://getqu.in/YgdvFh/

Anyway, I have now found the time to take a closer look at ETFs. And I can tell you one thing: Soprano buys the MSCI World before GTA 6. To be precise, it has already happened. What sounds "normal" to some people is definitely not to me. Anyone who has read the old post and knows my opinion on the MSCI World and knows that I only hold 100k in individual stocks - no passive investing, no core satellites - will understand that it may be interesting for some to read the background to my change of heart.

One of the main reasons for my world aversion is that I don't like the weighting of bad assets by market capitalization at all. In my Sturm & Drang days, I once tried to get around this with a self-built portfolio with GDP weighting. In other words, you buy one ETF each for the USA, Euro Stoxx, Switzerland, Japan, UK, emerging markets, etc. and then try to weight them yourself based on their actual economic strength. What sounds like an incredible clusterfuck is actually one. I abandoned this idea after just a few months because, in my view, it combines the worst of active investment and passive investment. Since then, I have only had around 2% of my assets in an India ETF (which is currently under review) and 2% in an active fund and have invested the rest in hand-picked individual stocks.

But enough beating around the bush. I'll tell you which ETF I bought and, more importantly, what I was thinking. It is the $IS3R (-0.56%) (MSCI World Momentum Factor ETF). To explain it briefly: the ETF does not simply invest in all the companies in the MSCI World and weight them according to the question of how big the company is, but prefers to buy the shares that have performed well in the past.

I see three very specific advantages here compared to conventional index investments.

Firstly the main advantage of an ETF is that you can trust the ETF provider to react faster and better to trends than you would yourself. I keep hearing that the 70% USA in the world is not a problem at all, as the ETF would simply "reallocate" everything. If rebalancing is so great, then it's best to trade trends in a fund that was specifically designed for this purpose.

The second advantagel is that momentum (after value and before quality) is one of the factors that can achieve a statistically significant outperformance compared to the broad market. This should not be underestimated either.

The third and final advantage for me personally is that it covers a blind spot in my portfolio. I myself invest mainly in shares that are very profitable but are also growing well. This corresponds to the factors "quality" and "growth". A typical example of this would be Microsoft. And of course I also try to get such companies as cheaply as possible ("value").

However, what I regularly don't do is get into shares that already seem expensive but continue to rise massively. That's why I also miss out on opportunities like $AVGO (+0.05%) and $COST (+0.35%) - is simply because I am relatively cautious and don't use/understand charting techniques. Such stocks typically end up in the portfolios of colleagues like @Dividenden_Monteur while they starve on my watchlist. A momentum ETF gives me the chance to be on board here, and far more so than conventional world investors.

Of course, I should not completely ignore the potential disadvantage that such an ETF is fundamentally more susceptible to fluctuations and therefore more "dangerous" than the index.

For me, this is a test phase for now. I hope I can remain loyal to the investment. But maybe I'll go crazy again and switch back to pure US investments, either with a normal S&P or something more extreme with smart beta factors and leverage.

May the holy Amumbo be with you!

Amen.

app.getquin.comWarum ich mich mit ETFs und dem MSCI World schwer tue

1Yr·

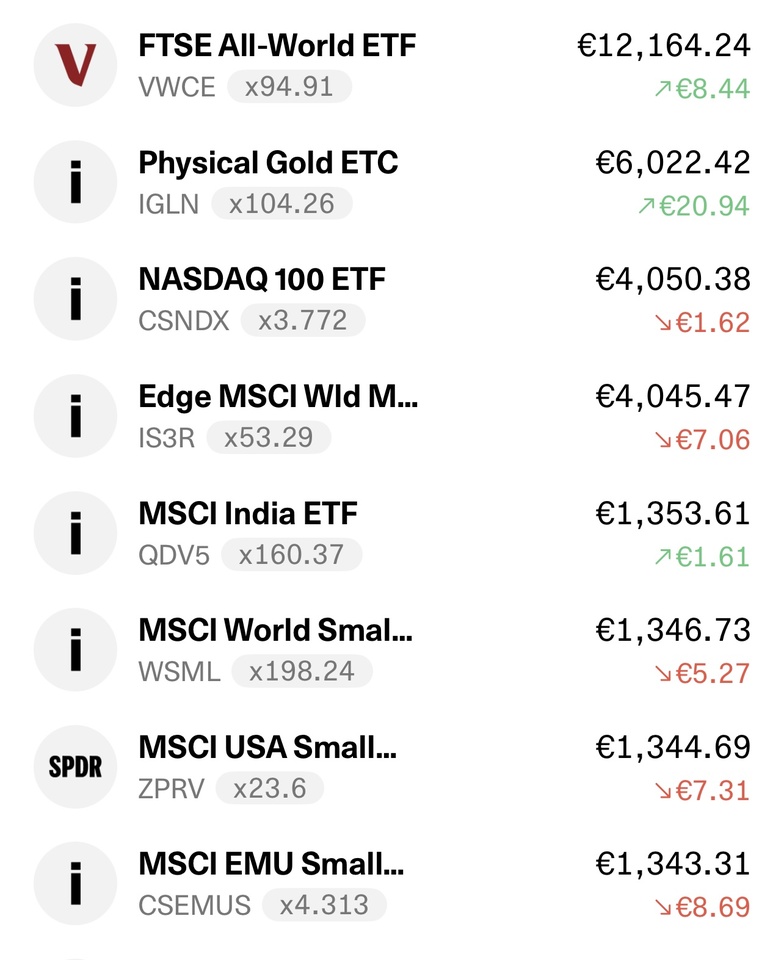

In 3, 2, 1… Off you go, money 🚀 See you in 20+ years 👋🏼

Did the most scared thing ever with my money… but also the most exciting. I’ll (hopefully) thank myself for someday! 💸

While the first 33K is invested now, I’m just waiting for a ‘good’ moment to jump into Bitcoin for 45% of my portfolio.

$VWCE (+0.09%)

$CSNDX (+0.13%)

$IS3R (-0.56%)

$IGLN (+0.05%)

$ZPRV (+1.02%)

$WSML (+0.42%)

$CSEMUS (+0.45%)

$QDV5 (+1.06%)

1Yr·

Fidelity Global Quality Income ETF - debate on position.

Hi all, I'm keen to understand your thoughts on the following. When would you consider $FGEQ (+0.88%) instead of $VWRL (+0.58%) as the core of a portfolio? What would be the benefit of one above the other? I used to have $VWRL (+0.58%) as core, but have switched over to $FGEQ (+0.88%) with $TDIV (+0.77%) on the side and a little of $IAPD (-0.45%) .

I know they track different indexes, as $FGEQ (+0.88%) track high quality companies from developed markets, while $VWRL (+0.58%) tracks stocks from both developed and emerging countries.

$FGEQ (+0.88%) while lacking emerging countries, still has decent growth.

Would you consider $FGEQ (+0.88%) vs $GGRP (+1.1%) or go for a more quality oriented ETF such as $IS3R (-0.56%) to try to grab a little more return?

I'm reconsidering my positions and wondering if I should move some of them around and/or back to where they came from. I've done some DYOR, which has for now lead me to the conclusion to keep $FGEQ (+0.88%) as the main position and expand a bit into $IS3R (-0.56%) on the side.

Wondering what your thoughts are :)

88

3 Comments

I‘m having both. Even added further ETF to get a monthly dividend and still get nice growth

•

55

•

1Yr·

Feedback for a beginner

Hello, GQ community!

I'm 50 years old and I'm very new to this interesting world of investments.

I believe it's never too late to learn something and start a new journey.

I plan to travel for about 15 years 🤞🏼🙂

I watched a lot of YouTube videos before deciding to switch to ETFs from simple deposit accounts. Actually I don't have knowledge yet to invest in individual stocks, so I'll go all-in on a few ETFs, trying to diversify a little bit. They say is good not to be entirely exposed to the US market, even though it should be every portfolio's core.

I started with a 5k allocation and I chose $IWDA (+0.35%) as my core, $SMEA (+0.34%) for the European market and $AASI (-0.3%) for a share of emerging markets ( 👉🏼 I wanted them to be Asian only, but then I realized $AASI (-0.3%) overweight US 🙄 Why its name is so deceiving?)

In short guys, by next week I plan to allocate another 20k to boost my portfolio and then saving every month.

I'd make $IWDA (+0.35%) at least 50% of my position, I'm considering the purchase of some $EIMI (-0.12%) shares (more focused on EM) and maybe soon a crypto ETN/ETC (I still have to understand which is the best offered solution from my broker).

I wouldn't exceed 10% for $WGLD (+0.05%) and 5% for the crypto.

- Do you have any tips?

- Do I already have overlaps?

- Does make sense to save on some $IS3R (-0.56%) shares just to get a tiny boost to my returns?

- Which would be the ideal % for every allocation?

[👉🏼 If I get a negative feedback about $IS3R (-0.56%) and $AASI (-0.3%) I won't sell them, but just let run as it is]

Thanks in advance for any precious opinion!

5Positions

€5,247.72

1.29%

55

5 Comments

1Yr

At first: Welcome to the community ✌🏻

You always have to look what kind of replication your ETF does. It can be physical (the etf buys real stocks) or synthetic (the ETF does Swaps). Your EM ETF has a synthetic replication. That’s why getquin shows you different stocks, then the ones that are really part of the ETF. So don’t worry, your EM ETF does not invest into US stocks. You can choose a different EM ETF with physical replication to see the real allocation.

I have some questions for you, so i can give you some advise:

What is your main goal with your portfolio? Do you want to build wealth or a passive income?

Why do you invest in gold? The return not exceedingly high but some people want it as a security. But those buy physical gold.

Are you familiar with the distribution of Bitcoins and how so called whales effect the BTC price?

My answers to your questions:

Yes you have some overlap between the MSCI World and the Europe ETF but this is totally fine because your aim here probably isn’t mainly a greater diversification but a higher weight on european stocks and thereby less weight on US stocks.

In my opinion the Momentum ETF is not a good choice. It invests into stocks that had a high performance in the past but that doesn’t guarantee future returns.

The ideal allocation depends on your opinion on what’s the best ratio of risk and return.

Maybe create some test portfolios here on getquin with different allocations and look at the region and sector allocation. This way, you can adjust it and compare until you find your personal ideal allocation.

You always have to look what kind of replication your ETF does. It can be physical (the etf buys real stocks) or synthetic (the ETF does Swaps). Your EM ETF has a synthetic replication. That’s why getquin shows you different stocks, then the ones that are really part of the ETF. So don’t worry, your EM ETF does not invest into US stocks. You can choose a different EM ETF with physical replication to see the real allocation.

I have some questions for you, so i can give you some advise:

What is your main goal with your portfolio? Do you want to build wealth or a passive income?

Why do you invest in gold? The return not exceedingly high but some people want it as a security. But those buy physical gold.

Are you familiar with the distribution of Bitcoins and how so called whales effect the BTC price?

My answers to your questions:

Yes you have some overlap between the MSCI World and the Europe ETF but this is totally fine because your aim here probably isn’t mainly a greater diversification but a higher weight on european stocks and thereby less weight on US stocks.

In my opinion the Momentum ETF is not a good choice. It invests into stocks that had a high performance in the past but that doesn’t guarantee future returns.

The ideal allocation depends on your opinion on what’s the best ratio of risk and return.

Maybe create some test portfolios here on getquin with different allocations and look at the region and sector allocation. This way, you can adjust it and compare until you find your personal ideal allocation.

•

22

•1Yr·

Dear Community,

I have finally managed to convince my wife of the benefits of the stock market.

She will start with 30k and has decided on the following ETFs, which she will save a total of 3k over 10 months. After that, she would like to invest at the same rate with a fixed monthly savings rate of around €500. She does not want to start directly with the full 30k.

The breakdown is as follows:

$JGOR (+0.66%) 20%

$ETLZ 10%

$ A40C74 20%

$IS3R (-0.56%) 50%

We are aware that the USA represents a cluster risk...

Thank you for your feedback.

55

8 Comments

•

77

•Trending Securities

Top creators this week

Real-time data from LSX · Fundamentals & EOD data from FactSet