More customer deposits, but earnings fell short of expectations. For the stock of $DWS (+2,15%) are therefore seeing a significant decline today.

DWS Group

Ação

Ação

ISIN: DE000DWS1007

Ticker: DWS

DE000DWS1007

DWS

Price

Discussão sobre DWS

Postos

42

3Semana·

What an awesome stock… 🤯🤩

$DWS (+2,15%) Dividend + Yield = 👍🏼👌🏼

Why is there so little written or reported about DWS?

Luckily, it's been in my portfolio for 3 years 🥳

1111

6 Comentários3Semana

I bought them in 2024, right before they paid out their special dividend. After that, the price plummeted, and I kept adding to my position.

It’s a little compensation for the fact that my Riester pension with them is doing so poorly.

But it’s not a hype stock like Rocket Labs, Irens, etc.—that’s probably why you don’t read anything about it.

It’s a little compensation for the fact that my Riester pension with them is doing so poorly.

But it’s not a hype stock like Rocket Labs, Irens, etc.—that’s probably why you don’t read anything about it.

•

22

•6Mês·

DWS share: New record achieved - what's next?

The DWS share is one of the biggest winners in the MDAX on Thursday. It is currently up +4.7% to € 62.60. This is due to the good preliminary figures for 2025.

New records achieved

The preliminary annual figures for 2025 published on January 29 set new records. The strong business performance of the previous quarters continued in the fourth quarter. Assets under management increased by €73 billion to around €1.1 trillion - a new record.

Income improved by 14% to just under €3.2 billion, also a new record. At the bottom line, net profit increased by 43% to € 927 million. This results in earnings per share (EPS) of € 4.64. This was above the company's own target of € 4.50.

The cost/income ratio is very positive - compared to the previous year's figure of 65.6%, it fell to 58%. Overall, the business figures were excellent.

6Mês·

Things are going well at DWS

Good figures at $DWS (+2,15%) Nice to see that at least the share is performing, even if my Riester pension is not doing well.

Dividend to be raised to € 3 from € 2.20 in the previous year. And there may be another special dividend next year.

https://trading-treff.de/trading/dws-aktie-rekordjahr-und-milliarden-bonus

66

1Ano·

Earnings update 29.04. 📈

Lufthansa: $LHA (+0,69%)

- Q1 revenue: €8.13bn (expected: €8.04bn)

- Q1 adj. EBIT: € -722 million (expected: € -718 million)

- Passenger airlines weaker than expected.

- Forecast 2025 confirmed: Significantly higher adj. EBIT than 2024.

- Task force for rapid capacity adjustment in the event of weaker demand.

- North American traffic strong in Q1 (+25% US passengers in March).

HelloFresh: $HFG (-1,73%)

- Q1 revenue: € 1.93 billion (-7%), adjusted EBITDA: € 58.1 million (+250%).

- Efficiency program bears fruit.

- 2025 forecast confirmed: Sales -3% to -8%, EBITDA € 450-500 million.

Novartis: $NOVN (-0,35%)

- Q1 net profit: USD 3.6 bn (+33%).

- Forecast raised: Sales growth now expected in the high single-digit percentage range.

Mutares: $MUX (+0,28%)

- Q1 revenue: €1.53bn (+13%), net result holding company: €29.5m.

- Exits planned for 2025 (>€200m gross proceeds expected).

- Partial sale of Steyr Motors generates € 74m.

Symrise: $SY1 (+6,46%)

- Q1 organic growth: 4.2%, sales: € 1.32 bn.

- Full-year forecast confirmed: 5-7% organic growth, EBITDA margin ~21%.

DWS Group: $DWS (+2,15%)

- Q1 revenues: €753m (+3%), net income: €199m (+13%).

- Record inflows: € 19.9 billion.

- Cooperation with Deutsche Bank in the Private Credit segment.

Deutsche Bank: $DBK (+0,93%)

- Q1 pre-tax profit +39%, highest quarterly profit in 14 years.

- Revenue growth and cost reductions drive earnings above expectations.

55

1 Comentar

Hello everyone,

Does anyone know what led to the 5% drop?

Unfortunately the AGM is hidden behind login data

edit: https://www.wallstreet-online.de/nachricht/19553792-beachtet-symrise-aktie-zeigt-schwaeche-30-06-2025

Does anyone know what led to the 5% drop?

Unfortunately the AGM is hidden behind login data

edit: https://www.wallstreet-online.de/nachricht/19553792-beachtet-symrise-aktie-zeigt-schwaeche-30-06-2025

••

1Ano·

Analyst updates, 13.01.25

⬆️⬆️⬆️

- GOLDMAN raises the price target for SIEMENS ENERGY from EUR 56 to EUR 60. Buy. $ENR (+1,25%)

- BARCLAYS raises the target price for MERCEDES-BENZ from EUR 48.50 to EUR 50. Underweight. $MBG (+1,72%)

- JEFFERIES upgrades SMA SOLAR from Hold to Buy and raises target price from EUR 14 to EUR 20. $S92 (-1,6%)

- GOLDMAN raises the price target for DEUTSCHE BÖRSE from EUR 226 to EUR 231. Neutral. $DB1 (-0,56%)

- BOFA upgrades BBVA from Neutral to Buy and raises target price from EUR 11 to EUR 13. $BBVA (+3,87%)

- WARBURG RESEARCH upgrades FUCHS SE from Hold to Buy. Target price EUR 50. $FPE

- GOLDMAN raises the price target for FLATEXDEGIRO from EUR 17 to EUR 18. Buy. $FTK (+0,82%)

- BERENBERG raises the target price for IBERDROLA from EUR 12.30 to EUR 14. Hold. $IBE (+0,73%)

- JEFFERIES upgrades PVA TEPLA from Hold to Buy and raises target price from EUR 12 to EUR 19. $TPE (+1,79%)

- JEFFERIES raises the price target for FRIEDRICH VORWERK from EUR 23 to EUR 30. Hold. $VH2 (+0,26%)

- JEFFERIES raises the price target for ZEAL NETWORK from EUR 45 to EUR 58. Buy. $TIMA (-2,46%)

- JEFFERIES raises the price target for ADESSO from EUR 75 to EUR 85. Hold. $ADN1 (-0,9%)

- JEFFERIES upgrades NEL from Underperform to Hold. Target price NOK 3. $NEL (+0%)

⬇️⬇️⬇️

- BERENBERG lowers the price target for RWE from EUR 46.50 to EUR 42. Buy. $RWE (+1%)

- GOLDMAN lowers target price for EON from EUR 17.50 to EUR 17. Buy. $EOAN (+1,96%)

- HAUCK AUFHÄUSER IB downgrades AIXTRON from Buy to Hold and lowers target price from EUR 26.40 to EUR 13.80. $AIXA (+1,92%)

- METZLER lowers the price target for DWS from EUR 41 to EUR 40.50. Hold. $DWS (+2,15%)

- GOLDMAN lowers the price target for ASTRAZENECA from GBP 159.55 to GBP 155.58. Buy. $AZN (+0,12%)

- TD COWEN downgrades STMICRO to Hold. Target price EUR 24.50. $STM (+2,84%)

- JPMORGAN downgrades CONSTELLATION BRANDS to Neutral. Target price USD 203. $STZ (-0,87%)

- JEFFERIES lowers the price target for DOCMORRIS from CHF 65 to CHF 39. Buy. $DOCM (-0,89%)

- JEFFERIES lowers the price target for ATOSS SOFTWARE from EUR 112 to EUR 108. Hold. $AOF (-1,48%)

- JEFFERIES lowers the price target for JENOPTIK from EUR 34 to EUR 29. Buy. $JEN (+1,74%)

- JEFFERIES lowers the price target for KONTRON from EUR 29 to EUR 27. Buy. $KTN (-2,61%)

- JEFFERIES lowers the price target for SILTRONIC from EUR 95 to EUR 90. Buy. $WAF (+1,4%)

- JEFFERIES downgrades VERBIO from Buy to Hold and lowers target price from EUR 22 to EUR 11. $VBK (-1,63%)

- JEFFERIES downgrades SGL CARBON from Buy to Hold and lowers target price from EUR 9.50 to EUR 4.40. $SGL (+1,72%)

1313

1Ano·

Analyst updates, 10.01.25

⬆️⬆️⬆️

- EXANE BNP raises the price target for ALLIANZ SE from EUR 271 to EUR 295. Underperform. $ALV (+0,73%)

- BARCLAYS raises the target price for AIRBUS from EUR 166 to EUR 200. Overweight. $AIR (+0,61%)

- UBS raises its price target for SAP from EUR 237 to EUR 283. Buy. $SAP (-0,65%)

- BERENBERG raises the price target for LVMH from EUR 695 to EUR 720. Buy. $MC (+0,69%)

- EXANE BNP raises the target price for MUNICH RE from EUR 550 to EUR 560. Outperform. $MUV2 (+0,61%)

- RBC raises the target price for SIEMENS from EUR 205 to EUR 225. Outperform. $SIE (+1,82%)

- CITIGROUP raises the target price for STELLANTIS from EUR 12.40 to EUR 13. Neutral. $STLA

- KEPLER CHEUVREUX raises the target price for DOUGLAS from 28.60 EUR to 29.90 EUR. Buy. $DOU (+1,63%)

- CITIGROUP raises the target price for DWS from EUR 43 to EUR 44.70. Buy. $DWS (+2,15%)

- CITIGROUP raises the price target for FRAPORT from EUR 62 to EUR 72. Buy. $FRA (+3,8%)

- UBS upgrades AMADEUS IT from Neutral to Buy and raises target price from EUR 67 to EUR 80. $AMS (+0,47%)

- DEUTSCHE BANK RESEARCH raises target price for PHILIPS from EUR 25 to EUR 26. Hold. $PHIA (+2,48%)

- DEUTSCHE BANK RESEARCH raises the target price for MAN GROUP from GBP 2.65 to GBP 2.75. Buy.

- GOLDMAN raises the target price for RIO TINTO from GBP 67 to GBP 73. Buy. $RIO (+2,04%)

- JEFFERIES raises the price target for SIEMENS ENERGY from EUR 31 to EUR 50. Hold. $ENR (+1,25%)

- RBC raises the target price for SCHNEIDER ELECTRIC from EUR 195 to EUR 210. $SU (+4,72%) Underperform.

- EXANE BNP upgrades HANNOVER RÜCK from Neutral to Outperform and raises target price from EUR 265 to EUR 285. $HNR1 (+0,47%)

⬇️⬇️⬇️

- DEUTSCHE BANK RESEARCH lowers the price target for NOVO NORDISK from DKK 1000 to DKK 900. Buy. $NOVO B (-0,17%)

- BOFA lowers the target price for RWE from EUR 44 to EUR 42. Buy. $RWE (+1%)

- JPMORGAN lowers the price target for NETFLIX from USD 1010 to USD 1000. Overweight. $NFLX (+0,04%)

- MORGAN STANLEY lowers the price target for SYMRISE from EUR 137 to EUR 130. Overweight. $SY1 (+6,46%)

- KEPLER CHEUVREUX lowers the target price for REDCARE PHARMACY from EUR 145 to EUR 138. Hold. $RDC (-3,62%)

- WARBURG RESEARCH lowers the target price for BECHTLE from EUR 51 to EUR 45. Buy. $BC8 (-1,45%)

- STIFEL downgrades WACKER CHEMIE from Buy to Hold. $WCH (+2,25%)

- RBC lowers the price target for DAIMLER TRUCK from EUR 55 to EUR 51. Outperform. $DTG (+0,45%)

1010

1Ano·

Analyst updates, 29.10. 👇🏼

⬆️⬆️⬆️

- JEFFERIES raises the price target for SAP $SAP (-0,65%) from EUR 230 to EUR 255. Buy.

- DEUTSCHE BANK RESEARCH raises the price target for DEUTSCHE TELEKOM $DTE (-0,15%) from EUR 33 to EUR 39. Buy.

- ODDO BHF raises the target price for ALLIANZ

SE

$ALV (+0,73%) from EUR 288 to EUR 324. Outperform. - ODDO BHF raises the price target for DWS

$DWS (+2,15%) from EUR 38 to EUR 39. Neutral. - METZLER raises the price target for LUFTHANSA $LHA (+0,69%) from EUR 5.70 to EUR 6.40. Hold.

- METZLER raises the price target for NEMETSCHEK

$NEM (-6,52%) from EUR 89 to EUR 91. Hold. - METZLER raises the price target for FRIEDRICH

VORWERK $VH2 (+0,26%) from EUR 29.20 to EUR 38. Buy. - GOLDMAN raises the price target for SYMRISE $SY1 (+6,46%) from EUR 127 to EUR 131. Neutral.

⬇️⬇️⬇️

- BOFA lowers the price target for MUNICH

RE

$MUV2 (+0,61%) from EUR 550 to EUR 535. Buy. - WARBURG RESEARCH lowers the price target for WACKER

CHEMICALS $WCH (+2,25%) from EUR 136 to EUR 133. Buy. - WARBURG RESEARCH downgrades STEICO

$ST5 (+0,16%) from Buy to Hold and lowers target price from EUR 42 to EUR 29. - METZLER lowers the price target for SALZGITTER $SZG (-3,35%) from EUR 17 to EUR 15.50. Hold.

- DEUTSCHE BANK RESEARCH lowers the price target for SGL

CARBON $SGL (+1,72%) from EUR 10.80 to EUR 10.60. Buy. - LBBW downgrades PHILIPS $PHIA (+2,48%) from Buy to Hold and lowers target price from EUR 30 to EUR 26.

- GOLDMAN downgrades ABB

$ABBNY (+2,24%) from Buy to Neutral. Target price CHF 52. - UBS lowers the price target for CARL ZEISS MEDITEC $AFX (+2,64%) from EUR 71 to EUR 65. Neutral.

- JPMORGAN lowers the price target for STMICRO

$STMPA (+2,82%) from EUR 42 to EUR 35. Overweight.

88

1Ano·

DWS Group - currently a good opportunity?

DWS Group is a global asset manager with assets under management of more than EUR 790 billion and a subsidiary of Deutsche Bank.

In a nutshell:

14.3% - that was the dividend yield of the DWS Group this year.

This year, the asset manager enticed investors with a substantial special distribution.

Even without this, the dividend yield remains high (around 5.49%). The share price currently stands at €38.50 and a realistic target price of

40.57 (that would be an increase of + 5.38%).

In addition, the annual reports are due on October 23, when analysts expect revenues to be slightly higher than in the same quarter of the previous year.

In addition to the dividend, the valuation is also attractive with a P/E ratio of 13.23.

The asset manager should also benefit from the ECB's continued turnaround on interest rates, even if sales have fallen in the past year.

What do you think of DWS Group? Does it currently offer a good opportunity to expand my dividend portfolio?

44

5 Comentários

1Ano

I joined the company in June at € 35.61 and so far everything is going well. I continue to see potential and look forward to the dividends.

•

22

•

1Ano·

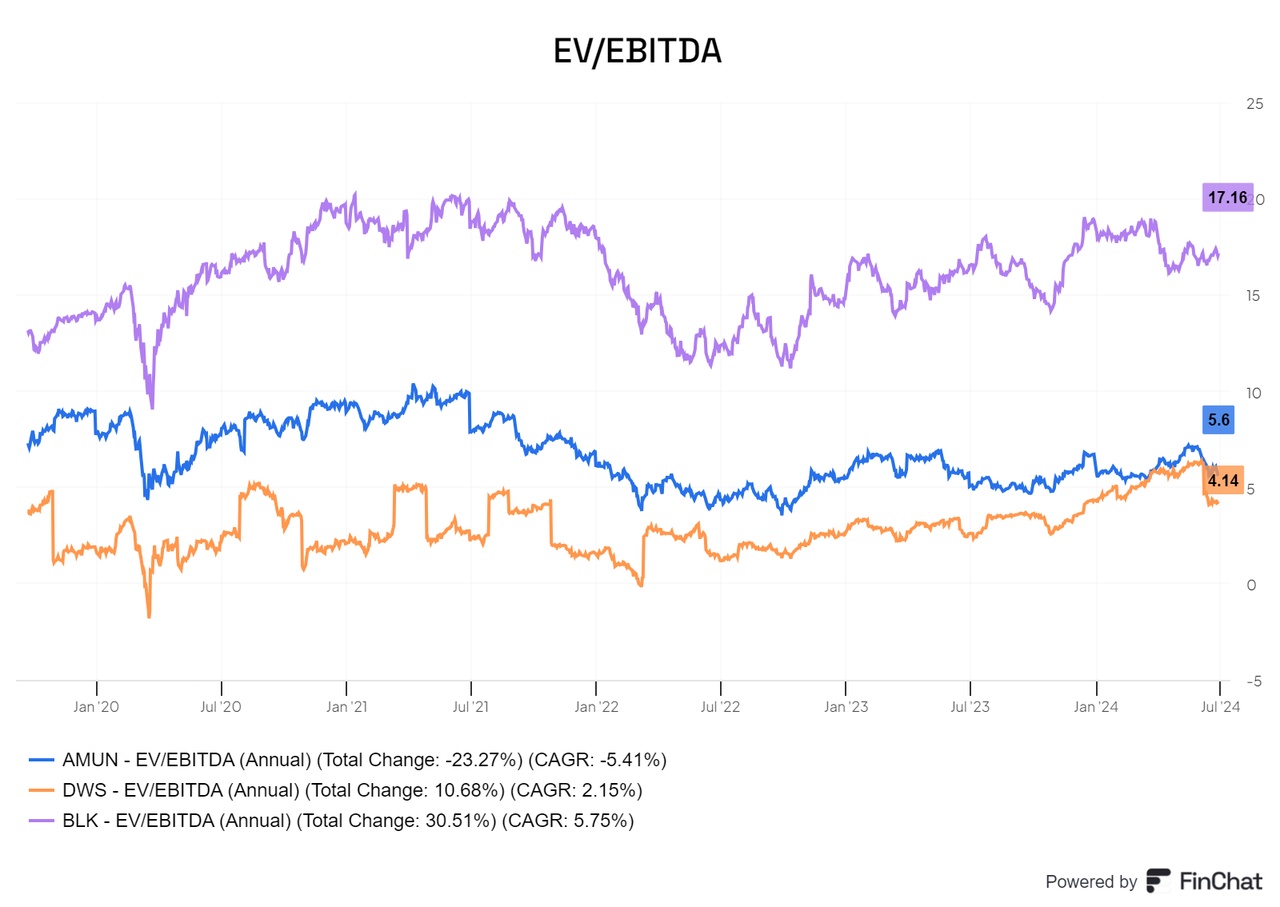

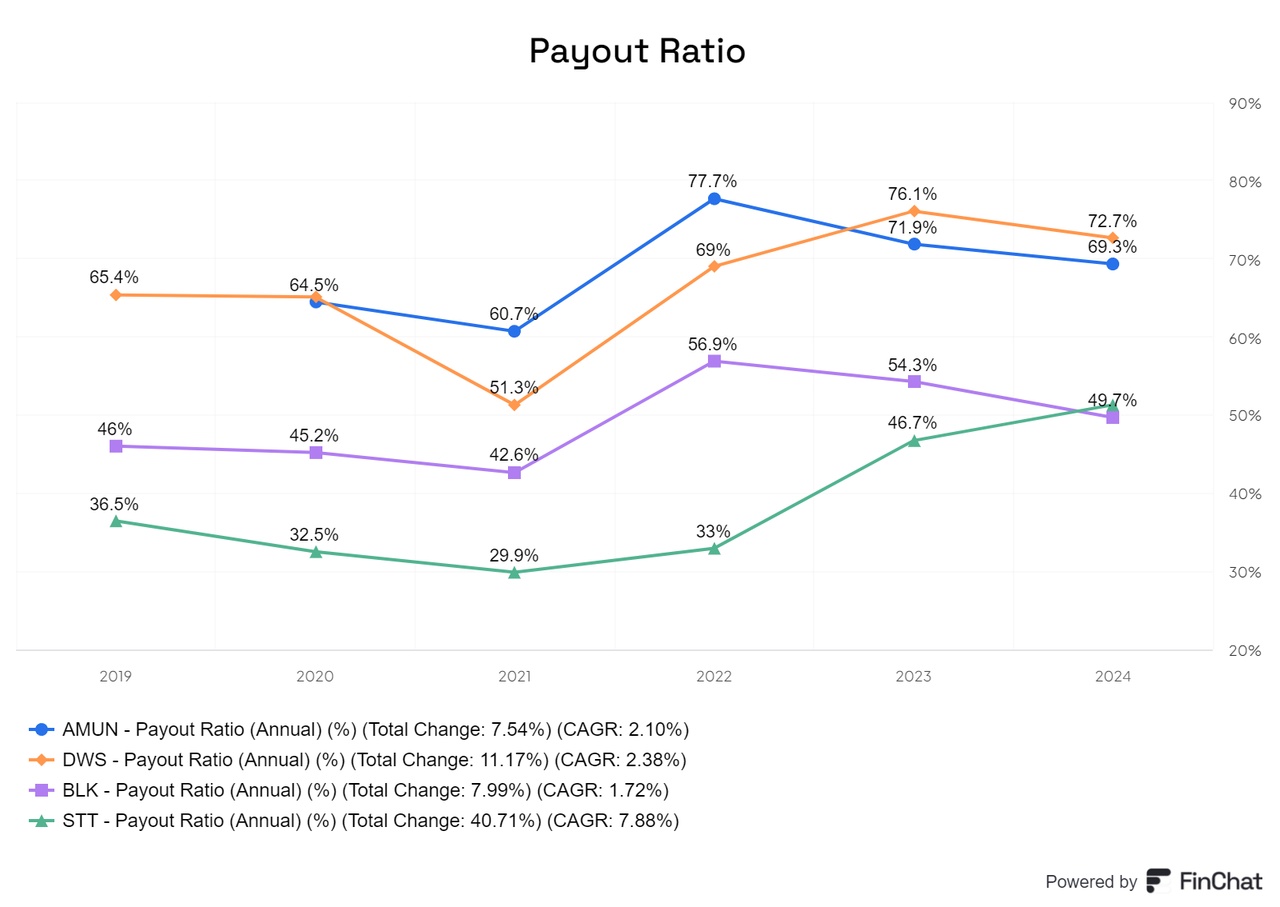

💶 Amundi: Europe's financial architect - Does he build the most solid assets? 🏗️ Part 1: https://getqu.in/Erlpxb/

Looking at the EV-to-EBITDA ratio, one would expect much more from BlackRock despite its size. Amundi is above DWS, but both companies are at a very low level overall and are actually very poorly valued.

Amundi performs best in terms of shareholder yield, followed by DWS.

The payout ratio is quite high for Amundi and DWS, but seems quite acceptable for the current models.

BlackRock also leads by a wide margin in terms of dividend per share (DPS).

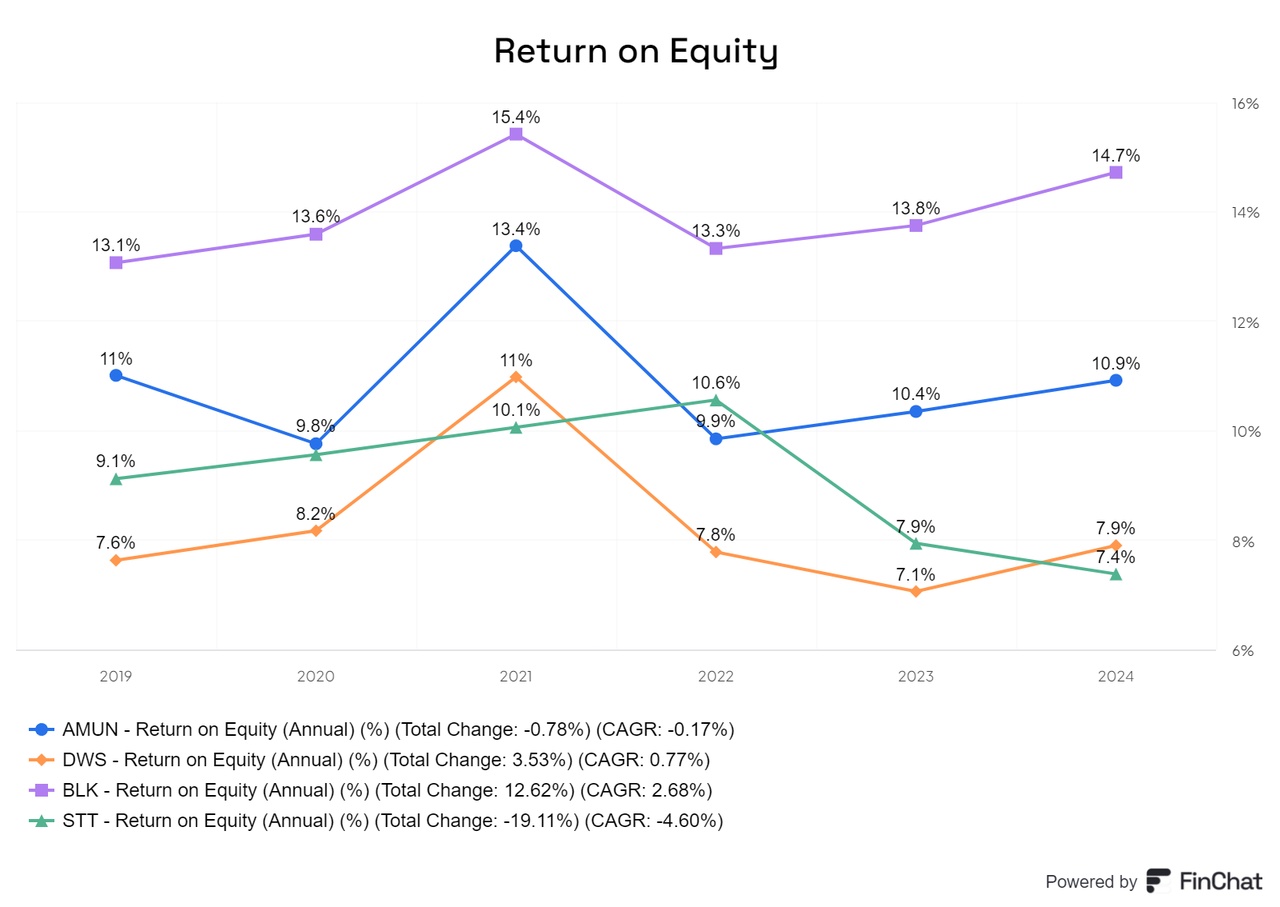

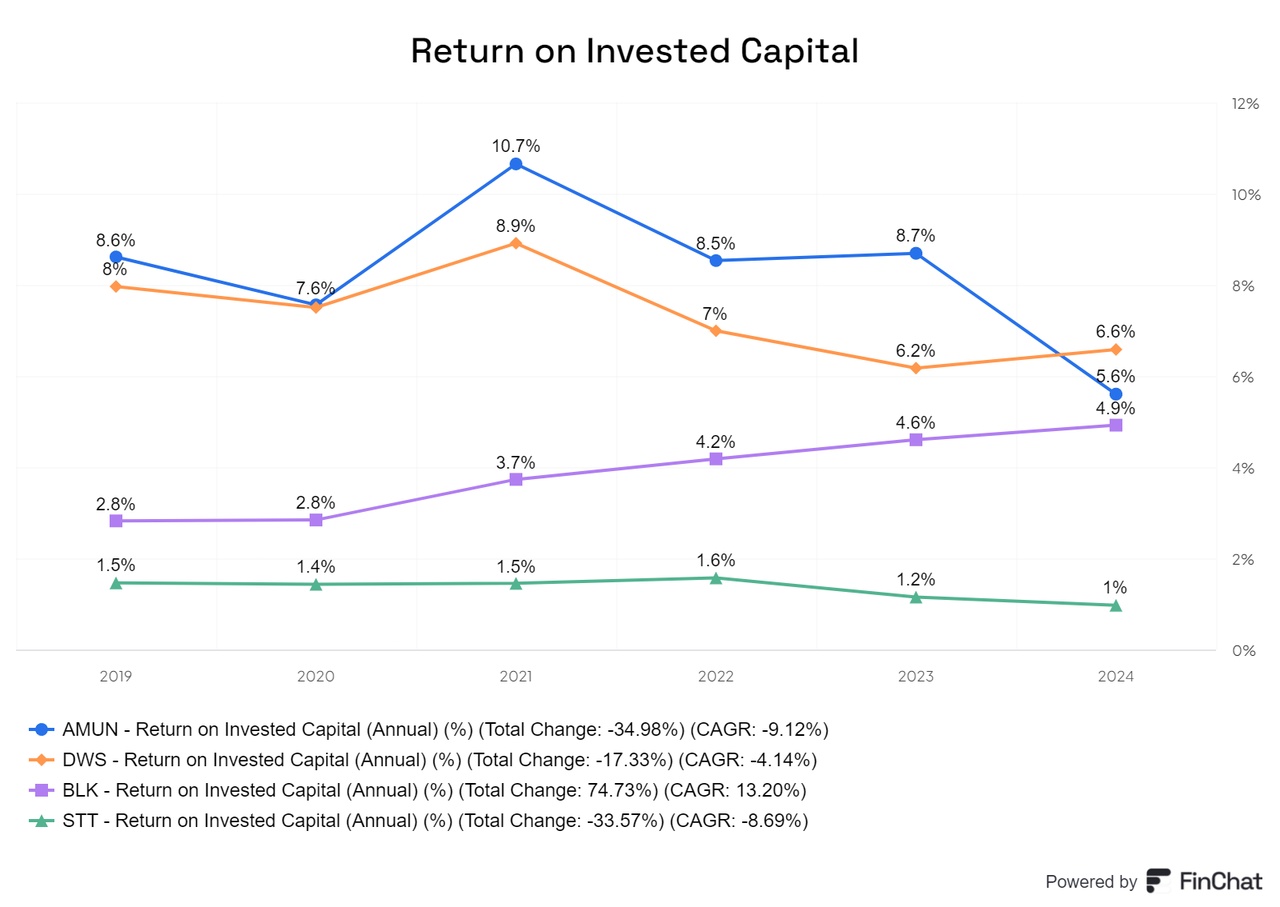

In terms of return on invested capital (ROIC), none of the companies exceed 10%.

In terms of ROE, Amundi and BlackRock are above 10%, with BlackRock consistently above it.

DWS is best positioned in terms of return on invested capital (ROCE) and has been above 10% for some time.

Conclusion

The asset management industry is a growing and highly lucrative industry, and in Europe it is still at the beginning of its development. It is clear that $BLK (+1,38%) is the leading provider and the first choice for any investor who wants to cover this area with a single share. However, the ETFs from $AMUN (+5,34%) are hardly any worse and are also attractively valued. In addition, Amundi offers many undiscovered opportunities that have great potential.

What I like about Amundi are several factors, some of which are not purely rational. As a European provider, Amundi differs from $DWS (+2,15%) and Blackrock because, unlike DWS, it has a better reputation and a better shareholder structure. There is no$DBK (+0,93%) bank in the background, but the interesting holding company SAS Rue La Boetie, and with it there is not a scandal every two weeks. In addition, Amundi offers incredibly cheap ETFs that should tie up capital in the long term and works closely with the German provider Solactive. Anyone familiar with Prime ETFs knows that they are exceptionally cheap. Although they are not yet recognized by many, they have already had an excellent start. Amundi also offers ALTO, an in-house financial technology that, while not quite at the level of BlackRock, is cheaper and just as helpful in its field. Amundi is also a leader in the ESG market and is one of the pioneers in the field of sustainable investments.

The cheap valuation, proximity to us, a good dividend, low-cost ETFs and solid values alongside BlackRock make an overall investment in Amundi attractive to me. It's not for everyone, mainly due to the withholding tax, but for me it's a good source of dividends that I can also support with my own ETFs.

Overall, I can only recommend buying more European provider ETFs. It doesn't always have to be Amundi - have a look here:https://getqu.in/5nb3cO/

+ 3

Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet