Hello, community,

I hope you’ve all managed to “cool off” and get through the heat over the last few days/weeks 🥵

Today, I’d like to introduce you to another company from Japan.

Today’s focus is on Rorze Corp $6323

🦾 Rorze Corp: The Indispensable Robotic Hand of the Chip Boom

Rorze Corp isn’t a traditional semiconductor developer that designs complex circuits or builds machines that etch patterns onto silicon. It is the ultimate mechanical bottleneck in global chip production. While ASML $ASML (-0,26%) builds the lithography giants, Rorze masters the delicate world of contamination-free transport. Rorze builds the high-precision handling robots that must move wafers in ultra-high vacuum and under extreme cleanroom conditions—a task where the slightest error can cost billions.

1. The Business Model: The “Toll Booth” in the Cleanroom 🎢

Rorze $6323 serves as an exclusive and mission-critical supplier to the world’s most valuable factories (TSMC $2330 , Intel $INTC (-3,15%) , Samsung $005930 ) as well as for the leading (Applied Materials $AMAT (+0,4%) , Lam Research $LRCX (-0,68%) ).

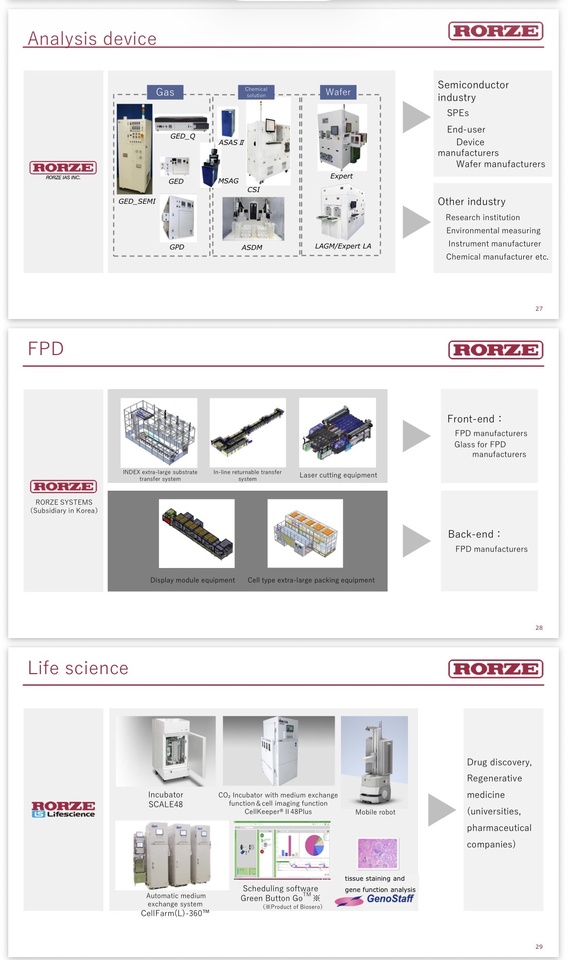

The mechanism: When state-of-the-art semiconductors (3 nm and below) are produced, not a single speck of dust is allowed to touch the wafer. Rorze $6323 makes its money by developing and selling atmospheric and vacuum robotic systems that transfer the wafers back and forth between individual manufacturing steps in a contactless and sterile manner.

The ingenious part: Rorze $6323 has made itself indispensable. The major chip manufacturers physically cannot operate their multi-billion-dollar factories without integrating Rorze’s automation systems. Every new chip factory worldwide—whether in Arizona, Taiwan, or Dresden—means a large automatic order for Rorze.

Recurring Cash Flows: In addition to the pure sale of outrageously expensive robotic systems, there’s a high-margin service and spare parts business. Since the robots operate continuously under extreme conditions, maintenance is a reliable cash cow.

2. Key Figures (as of July 2026) 📊

Market capitalization: approx. 850 billion JPY (approx. 5.4 billion USD).

Stock price: Currently approx. 4,940 JPY (The stock is currently surging sharply after more than doubling from ~2,400 JPY since the beginning of the year).

P/E Ratio: approx. 42–45. Due to the recent surge in the order book and the market’s revaluation, the stock is no longer a bargain, but it does reflect its massive growth potential.

Return on Equity (ROE): Outstanding ~25–28%. For a capital-intensive mechanical engineering company, this level of efficiency is absolutely staggering.

Debt: Extremely solid balance sheet. High net cash reserves protect the operating business from interest rate risks.

3. Why is this stock exciting? 🚀

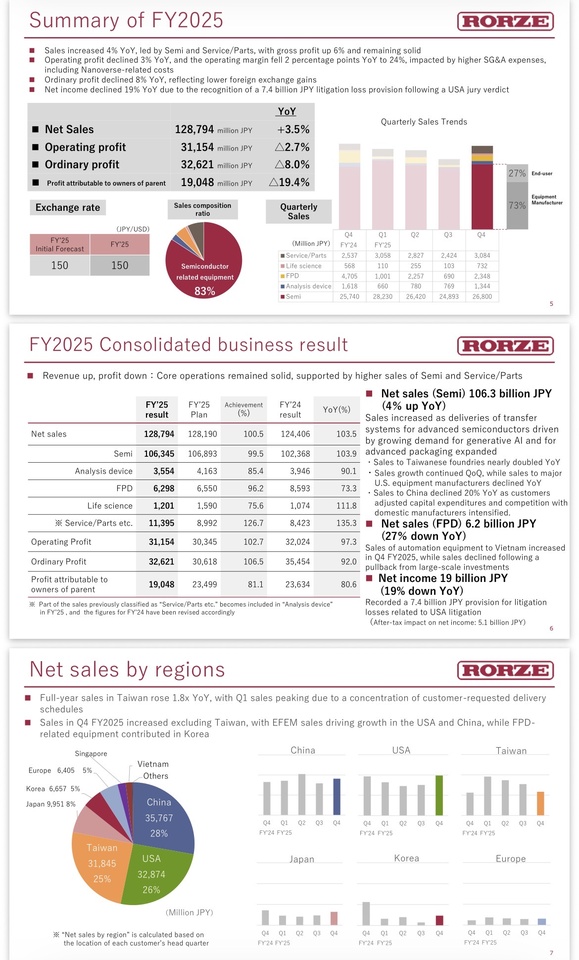

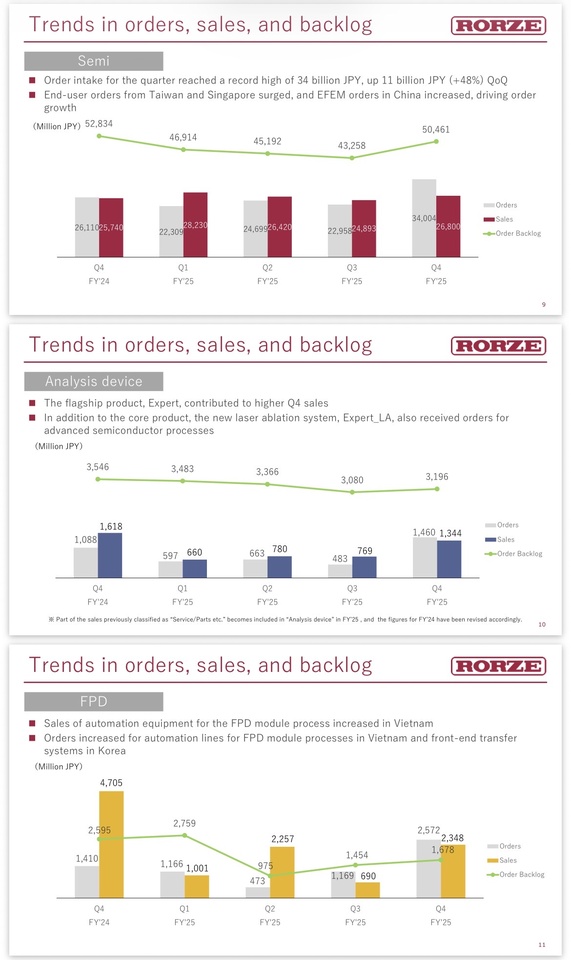

✅1. An explosive surge in orders wipes out the “profit warning”: In April 2026, Rorze $6323 reportedly posted a slight decline in earnings for the past fiscal year—triggered by one-time costs related to a U.S. lawsuit and high upfront investments in its subsidiary Nanoverse. The market, however, looked deeper and saw record order intake in the fourth quarter and a forecast of 46% profit growth for the coming year. The stock subsequently shot up to the daily limit.

✅2. The Advanced Packaging Lever: Due to the AI boom, memory chips (HBM) must be stacked in extremely complex configurations. Rorzes’ U.S. subsidiary Nanoverse is developing next-gen equipment specifically for this purpose. Rorze is evolving from a mere “wafer pusher” into a key player in physical AI infrastructure.

✅3. Geopolitical tailwind: The U.S. 🇺🇸, Europe 🇪🇺, and 🇯🇵 are subsidizing the construction of local semiconductor factories with hundreds of billions. Who equips these factories is irrelevant—Rorze’s robots are needed in nearly every one of them. They win, no matter which chip manufacturer comes out on top.

✅4. A unique competitive moat through cleanroom validation: Chip manufacturers are extremely risk-averse. Once a Rorze robot is certified and validated for a TSMC production line, it’s never replaced—out of fear of production downtime. The barriers to switching are astronomical.

✅5. Index knighthood: Rorze $6323 was recently included in the prestigious JPX Prime 150 Index . This continuously attracts fresh institutional ETF and fund money to the stock.

5. Risks ⚠️

❗️Extreme dependence on the semiconductor cycle: If the tech world were to slip into a deep recession and the tech giants were to freeze their new factory construction (Capex), Rorze—as a cyclical equipment supplier—would feel the impact with a time lag, but it would hit hard.

❗️The competition never sleeps: Players such as Daifuku $6383 (-2,91%) or Brooks Automation are also making inroads into the field of factory automation. Rorze must absolutely maintain its technological lead in the vacuum sector.

❗️Investment Rating: With a P/E ratio above 40, the potential for an earnings surge over the next 12–24 months is already largely priced in. Setbacks in the volatile semiconductor market are possible at any time.

6. Personal Conclusion & Reaper Bonus 🧐

Rorze Corp $6323 is the ultimate “shovel stock” for the global semiconductor and AI frenzy. They don’t build chips; they make production possible in the first place. Following the explosion in order volume in the summer of 2026, the market has finally realized what a gem has been lying dormant here in the Japanese small/mid-cap sector. It’s on my watch list 👀

💀Jack’s Verdict:

"If ASML builds the priceless high-tech camera for a Hollywood blockbuster, Rorze supplies the indispensable tripod: Without its vacuum robots, the entire chip production process would be thrown off balance. The market has underestimated this unassuming monopolist for years, which is why the stock is now delivering its well-deserved payoff at 4,940 JPY. Don’t be put off by the seemingly high P/E ratio of 42—as soon as the latest record orders are fully reflected in the income statement and the projected profit growth of nearly 50 percent kicks in, the valuation will shrink rapidly. Those who missed the entry point should lie in wait for the next collective semiconductor hiccup, pick up shares on the pullback, and let the robots in the cleanroom work for them."

Reaper Rating: 🔥 BUY ON DIPS (Fundamentals are extremely strong, but the chart has become overheated after the stock doubled in price).

Reaper Score:

8/10 (Quality anchor 8–9. The fundamental monopoly position deserves a 9, but the current valuation pushes the score down slightly to a well-deserved 8)

I’m curious to hear your thoughts🙇♂️

@Get_Rich_Or_Die_Tryin @Tenbagger2024

@PikaPika0105

@Raketentoni

@Multibagger

@schlimmschlimm

@Stocktective

@Dividendenopi and, of course, everyone else ✌️