Hi everyone,

I'd be interested to know which stocks are currently at the top of your watchlists. I'll start:

$MSFT (+1,7%) Add to portfolio

$8001 (+1,9%) Additional purchase

$CAMX (-0,32%) Buy more

Messaggi

32Hi everyone,

I'd be interested to know which stocks are currently at the top of your watchlists. I'll start:

$MSFT (+1,7%) Add to portfolio

$8001 (+1,9%) Additional purchase

$CAMX (-0,32%) Buy more

May was dominated by strong figures and a massive rally in the tech and cloud sector. While April was still characterized by a general recovery, excellent quarterly figures and the unbroken AI boom continued to fuel the markets in May. The Nasdaq in particular benefited greatly from this and reached new highs. Even though volatility was noticeable in isolated cases, investors made strong gains in growth stocks.

My portfolio was able to take advantage of this strong momentum and achieve an outstanding performance, but was narrowly beaten by the extremely strong performance of the Nasdaq 100:

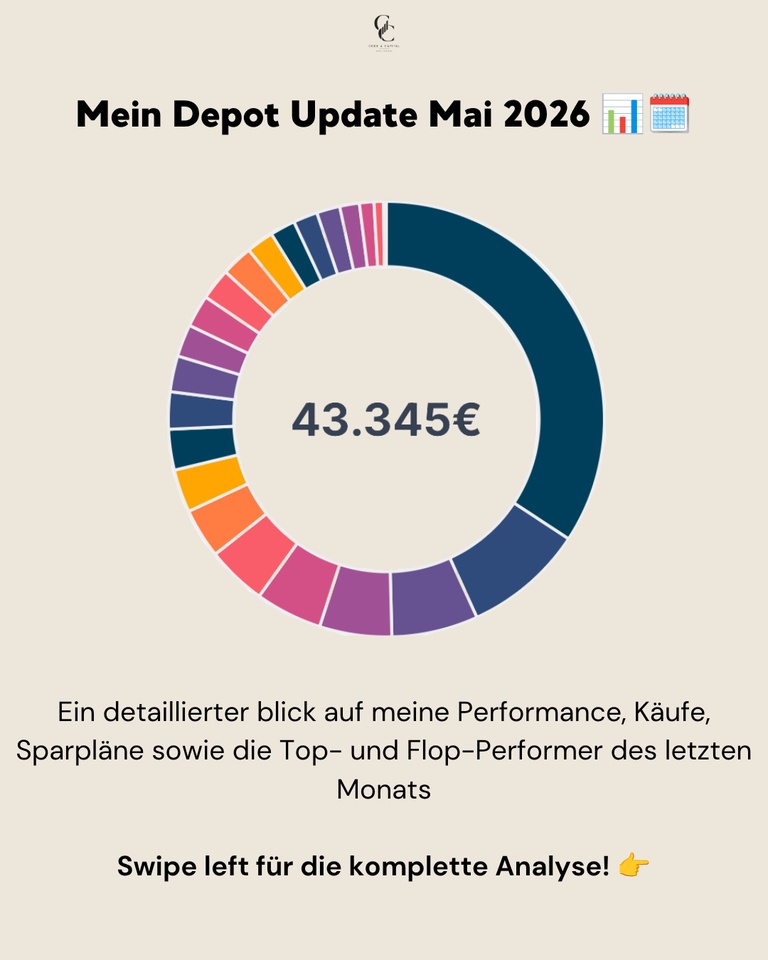

📊 Monthly performance: +9,33%

📊 Portfolio value: ~43.345 €

📊 Performance max. (06.01.2022): +43,84%

📊 Performance YTD: ~+10,44%

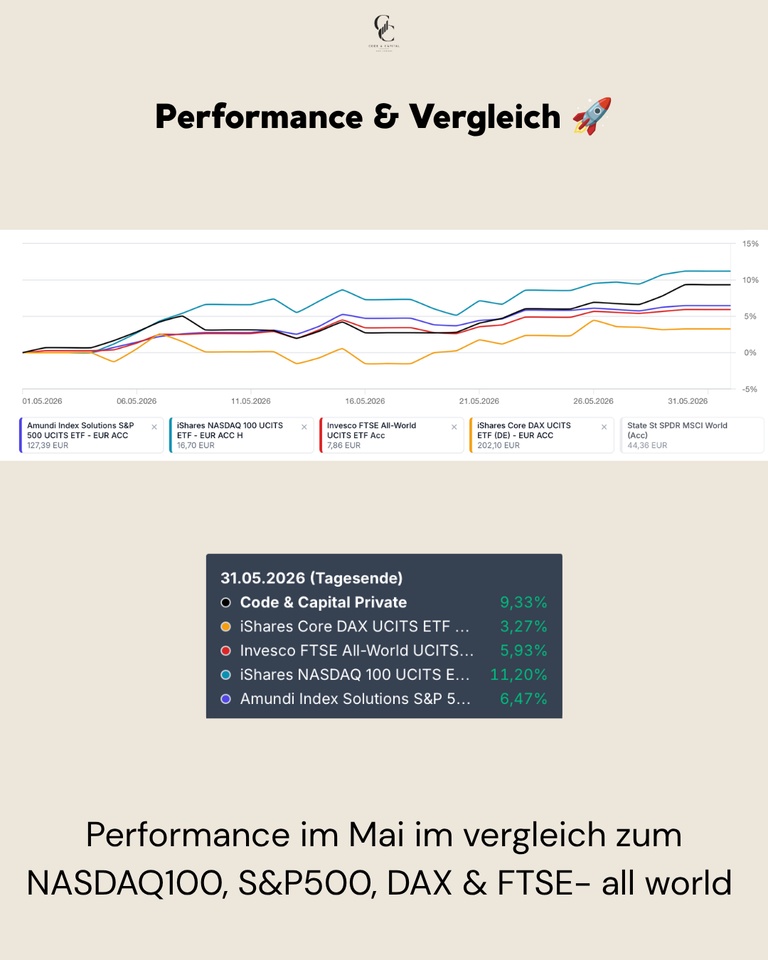

Performance & comparison 🚀

Performance in May was exceptionally strong, driven by my high weighting in US tech stocks. While European indices such as the DAX made rather moderate gains, US stocks dominated the action. My portfolio did extremely well with a whopping gain of over 8 % and clearly outperformed the broad market.

Performance in comparison (01.05.-31.05.2026):

My portfolio: +9,33%

NASDAQ 100: +11,20%

S&P 500: +6,47%

FTSE All-World: +5,93%

DAX: +3,27%

Buying, selling & allocation 💶

In the month of May, € 300.00 flowed into the MSCI ACWI USD (Acc)

$ACWI and € 50.00 in the MSCI World Small Cap

$WSML (+1,58%). In addition, smaller savings plan tranches were invested in Solaria Energia

$SLR (+1,19%) (150,30 €), Rheinmetall $RHM (+1,26%) (14,00 €), Ferrari

$RACE (+0,12%) (€6.00) and Hermes

$RMS (-0,64%) (€ 3.01) were invested.

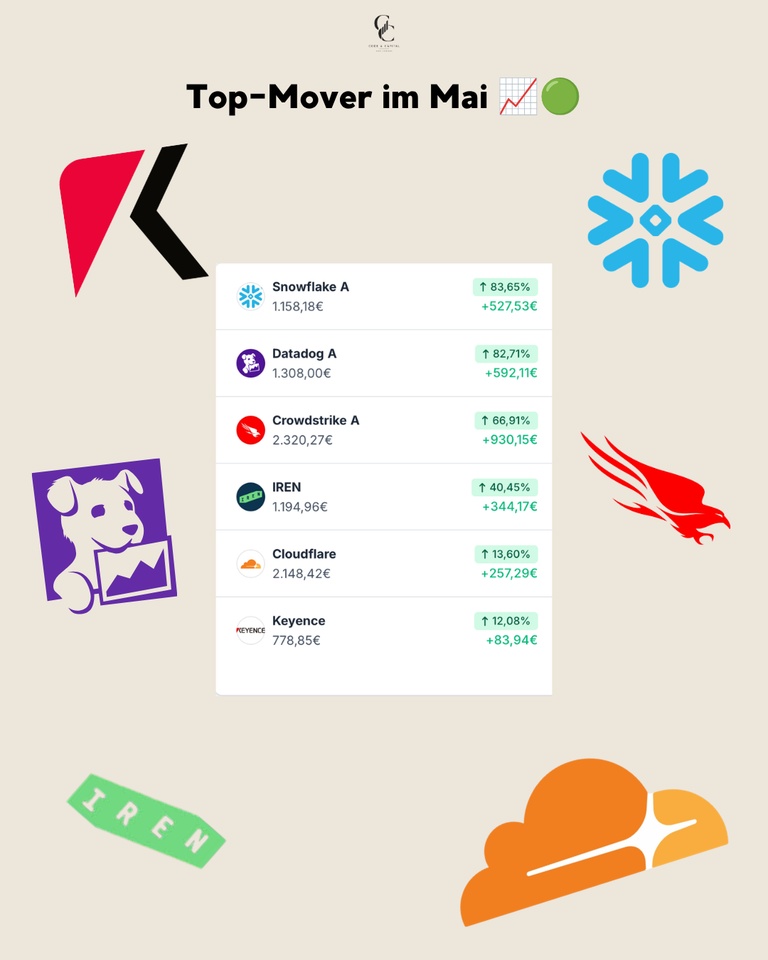

Top movers in May 🟢

The list of winners in May is led by outstanding developments in the cloud and cybersecurity sector - an absolute feast for tech investors.

The absolute frontrunner was $SNOW (+3,54%) with a veritable price explosion of +83,65% (+€ 527.53), closely followed by $DDOG (+3,95%) with +82,71% (+592,11 €). Both values showed incredible momentum. Also $CRWD (+2,81%) was convincing across the board and delivered a strong +66,91% (+€ 930.15), which was the biggest gain in the portfolio in absolute terms. $IREN (+3,04%) continued its strong trend and recorded a further +40,45% (+344,17 €). The outstanding tech performance was rounded off by $NET (+5,72%) with a solid +13,60% (+€ 257.29), while Keyence also $6861 (+2,96%) with +12,08% (+€83.94) also developed extremely positively.

Flop movers in May 🔴

Despite the generally extremely strong sentiment, there were also some stocks that consolidated or showed weakness in May.

American Lithium was the worst performer, falling by -13,16% (-46.03 €), still unable to find a bottom in the current market environment. With $1211 (-1,51%) the minus of -12,13% (€ -190.62) was due to falling EV sales and the ongoing price war in China. $NU (-0,04%) After the strong previous months, the share price fell by -8,90% (-99.30 €) after the strong previous months. Also $TEM (+1,89%) also recorded a slight setback of -8,49% (-7.90 €), similar to $BABA (+1,45%) with -5,15% (-40,59 €). $RHM (+1,26%) also lost ground and lost -4,60% (-77.14 €), indicating further profit-taking in the defense sector.

Conclusion 💡

May was an outstanding month that impressively demonstrated how much a targeted positioning in the tech and cloud sector can pay off.

❓ Question for the community

This was my month in numbers, what was your best buy in May? Which stock surprised you the most?

👇 Write it in the comments!

➡️ Follow @codeandcapital for transparent portfolio updates!

🔗 Link in bio: Wikifolio, Getquin & Parqet Portfolio

🗞️ Newsletter: codeandcapitalquant.beehiiv.com

+ 2

April was the month of the big recovery. After March was extremely affected by the geopolitical tensions in the Middle East, optimism returned to the markets in April. The feared escalation failed to materialize, oil prices stabilized at a high level and investors took advantage of the lower prices to make a massive re-entry - especially in the tech sector, which catapulted the Nasdaq to new record highs.

My portfolio benefited from this positive sentiment, but lagged behind the massive rally of the benchmarks:

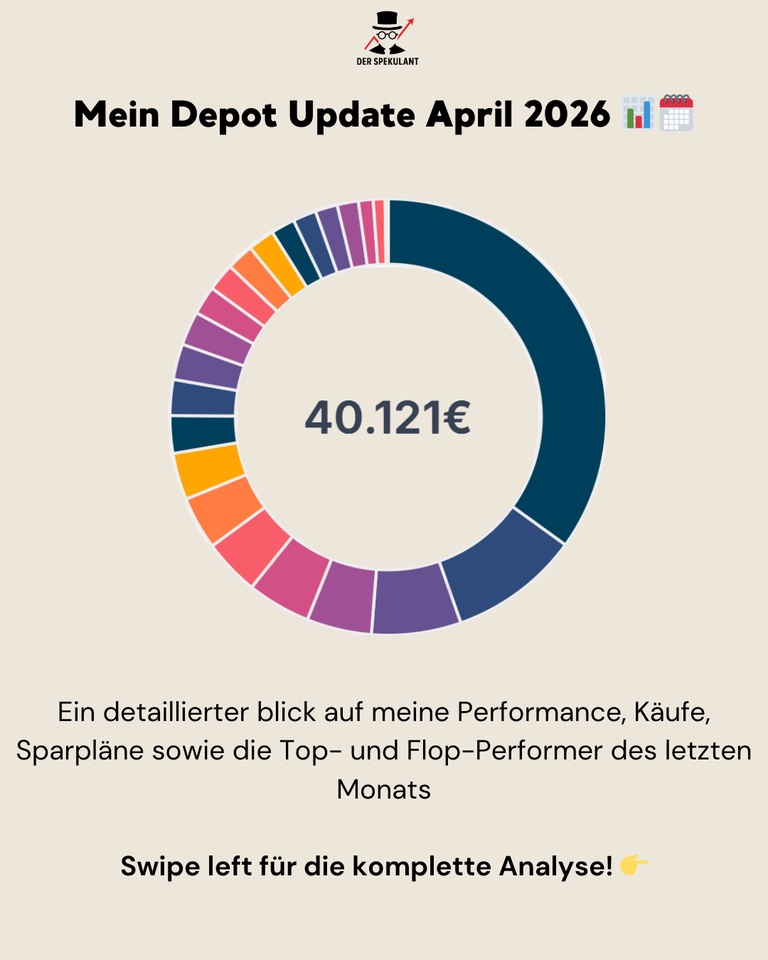

📊 Monthly performance: +6,59%

📊 Portfolio value: ~40.121 €

📊 Performance max (06.01.2022): +35,47%

📊 Performance YTD: ~+4,03%

Performance & comparison 🚀

The recovery in April was impressive, but almost felt "too fast". While the US markets were boosted by strong big tech figures, European stocks were stable but less dynamic. The ECB stuck to its cautious course, which dampened volatility somewhat.

Performance in comparison (01.04.-30.04.2026):

Buying, selling & allocation 💶

No investments were made in April.

👉 After the high volatility in the previous month, I kept my feet still. The strategy continues to be "watch and hold".

Top movers in April 🟢

The list of winners in April is led by stocks that were still underperforming in March - a classic rebound.

The absolute frontrunner was $IREN (+3,04%) with an increase of +31.02% (+€201.45), which benefited massively from the stabilization in the crypto-mining sector. This was closely followed by $6861 (+2,96%) with +29.08% (+€156.56) - an impressive return to relative strength after the severe setback in March. Also $SIE (+0,72%) was also able to shine with +22.78 % (+€153.07), as concerns about exploding energy costs in the industry have eased for the time being. American Lithium corrected the previous month's losses with a gain of +22.58 % (+€ 64.45), while $TEM (+1,89%) with +21.08 % (+€ 16.21) and $2330 +16.32 % (€ +61.10) underpinned the strength in the semiconductor and AI segment.

Flop movers in April 🔴

Despite the generally positive sentiment, there were also stocks in April that didn't get off the ground or even fell.

The strongest correction $SNOW (+3,54%) which continued the negative trend with -9.97% (-€69.87) - the market believes that there are probably opportunities for disruption through AI. Also $RHM (+1,26%) also lost ground after the rally of recent months, shedding -6.14% (-€109.66) as profit-taking dominated the defense sector. $1211 (-1,51%) fell again somewhat after the strong performance in March (-3.56%, -€58.01), and also $BRK.B (+0,33%) was rather flat at -1.19% (-€37.58). Almost ironic: $RMS (-0,64%) (+0.09 %) and the Xtrackers Overnight ETF (+0.15 %) ended up in the "flop" ranking, simply because they simply missed out on the double-digit rally of the overall market.

Conclusion 💡

April was a balm for the soul of every investor, even if my portfolio was unable to fully participate in the benchmark rally.

❓ Question for the community

This was my month in numbers, what was your best buy in April? Which stock surprised you the most?

👇 Write it in the comments!

➡️ Follow @derspekulant.1 for transparent portfolio updates!

🔗 Link in Bio: Getquin & Parqet Portfolio

🗞️ Newsletter: derspekulant.beehiiv.com

+ 2

March was a very weak month on the markets. The Iran war kept global stock markets on tenterhooks - rising oil prices, accelerated inflation and a massive risk-off move across almost all asset classes. The DAX lost over 10%, the Nasdaq slipped into correction mode and even broadly diversified world ETFs fell significantly.

Despite the difficult environment, my portfolio remained comparatively stable and outperformed all major benchmarks:

📊 Monthly performance: -3,69%

📊 Portfolio value: ~38.367 €

📊 Performance

max. (06.01.2022): +24,98%

📊 Performance

YTD: -2,80%

Performance & comparison 🚀

March was characterized by a broad sell-off, triggered by the escalation in the Middle East, rising oil prices and the associated reassessment of inflation expectations. The ECB kept the deposit rate at 2.00%, but signaled increased uncertainty - rate cut fantasies are off the table for now.

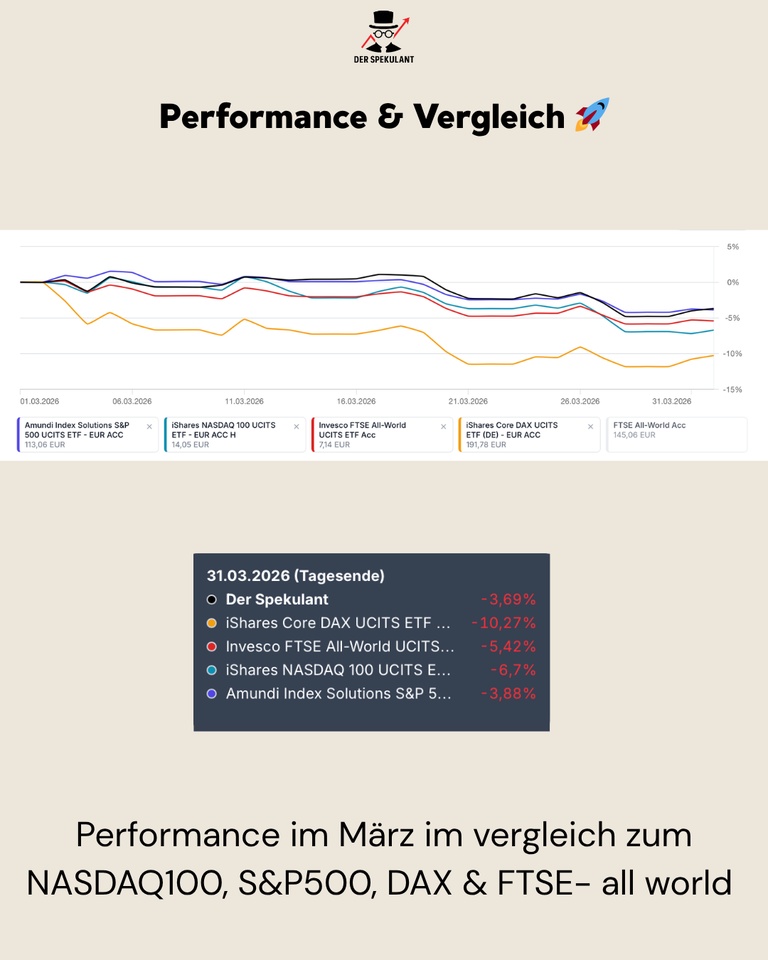

Performance in comparison (01.03-31.03.2026):

My portfolio: -3,69%

NASDAQ 100: -6,70%

S&P 500: -3,88%

DAX: -10,27%

FTSE All-World: -5,42%

👉 The portfolio performed significantly better than all benchmark indices in an extremely weak market environment. Particularly striking: the DAX lost over 10% - driven by the direct impact of rising energy costs on European industrial stocks. The global diversification and focus on quality in the portfolio clearly paid off in this environment.

Purchases, sales & allocation 💶

No purchases or sales were made in March.

👉 In an environment of war, rising oil prices and increased volatility, the conscious decision not to carry out any transactions was part of the strategy.

The existing allocation reflects the conviction - panic selling or frantic buying in times of maximum uncertainty are not part of the approach. Cash is held ready for potential opportunities in the event of further weakness.

Top movers in March 🟢

Despite the weak overall market, individual positions showed significant strength.

The strongest performer was Cloudflare ($NET (+5,72%)) with +22.68% and a gain of +€339.97 - the share benefited massively from the AI edge infrastructure fantasy and strong Q4 figures with 33.6% revenue growth. CEO Matthew Prince is positioning Cloudflare as a central platform for the "Agentic Internet", which is going down well with investors. Also BYD ($1211 (-1,51%)) also impressed with +15.01% (+€212.72) and once again showed relative strength in the EV sector, followed by CrowdStrike ($CRWD (+2,81%)) with +9.47% (+€108.12), which recovered significantly after the previous month's weak performance.

Datadog ($DDOG (+3,95%)) gained +7.82% (+47.22€), while Bitcoin ($BTC (-0,81%)) showed a moderate recovery with +4.00% (+€37.26). Mercado

Libre ($MELI (-1,58%)) rounded off the list of winners with +1.95% (+€12.50) - also a rebound after the weak February with -17.33%.

Flop movers in March 🔴

The weaker side of the portfolio was broadly diversified across various sectors and reflected geopolitical pressure.

American

Lithium ($AMLI) corrected the most with -31.11% (-128.90€) - the commodity sector is under pressure from falling lithium spot prices and weak demand forecasts from China. Hermès Hermès ($RMS (-0,64%)) also came under pressure at -18.09% (€-0.54) - although the position was only established in February as a quality stock, Luxury is currently suffering from the general risk-off sentiment.

Siemens ($SIE (+0,72%)) lost -16.75% (-€135.26) - as an export-oriented industrial stock directly affected by rising energy costs and the uncertainty caused by the Middle East conflict. Keyence ($6861 (+2,96%)) lost -16.43% (-€105.85) - a significant setback after the strong February rebound of +16.21%. IREN ($IREN (+3,04%)) continued the negative trend with -14.54% (-110.45€), already the second weak month in a row after -24.10% in February. The VanEck Uranium and Nuclear ETF ($NLR (+2,25%)) rounded off the list of losers with -13.46% (-150.21€).

👉 Striking:

The setback at Keyence and Hermès shows how quickly relative strength can be lost again in volatile markets. Fundamentally, however, nothing has changed for most positions - the corrections are primarily driven by sentiment and macro factors, not by operational weakness.

Conclusion 💡

March was a stress test for the entire portfolio, but the relative outperformance against all benchmarks confirms the strategic orientation:

➡️ No panic selling - maintain discipline in the allocation

➡️ Relative strength against NASDAQ 100 (-6.70%), S&P 500 (-3.88%), DAX (-10.27%) and FTSE All-World (-5.42%)

➡️ Individual stocks such as Cloudflare (+22.68%) and BYD (+15.01%) as stabilizers in the portfolio

The environment remains challenging:

The Iran conflict, rising oil prices and the associated inflation risks will continue to shape the markets in April. The ECB has raised its inflation forecast for 2026 to 2.60% - interest rate cuts are a distant prospect. The focus remains on qualityglobal diversification and patience. In phases of maximum uncertainty, the wheat is separated from the chaff.

❓ Question for the community

Which stock surprised you the most in March - positively or negatively?

👇 Write it in the comments!

➡️ Follow @Derspekulant1 for transparent portfolio updates! 🔗 Link in bio: Getquin & Parqet Portfolio

🗞️ Newsletter: derspekulant.beehiiv.com

+ 2

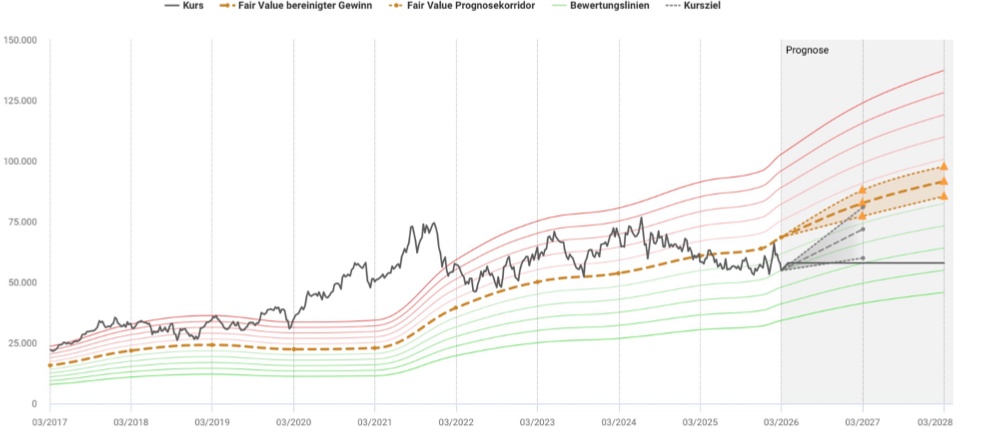

To answer this question, it is first worth taking a look at the chart.

The share has lost around 45% since its high of around €590 and is currently trading at €317. If the question arises as to why the share has been sold off so strongly, this is due to a real exaggeration on the upside, which in my view has caused an exaggeration on the downside. You can see how, according to the share finder, it was well above fair value for a long time. Recently, however, it has come back significantly.

1. the "fabless" miracle: assets without ballast

Keyence develops sensors, microscopes and vision systems for factory automation. Yet they do not own a single factory.

- The effect: they have almost no tied-up capital (asset-light). If the economy falters, they do not have to close any factories or lay off workers.

2 The direct sales monopoly

Normally, companies sell through intermediaries. Keyence does the opposite:

- On-site problem solvers: Keyence engineers go directly to customers' factories. They don't just sell a product from the catalog, but solve a specific problem (e.g.: "How do I detect this micro-crack at 200 km/h belt speed?").

- Pricing power: Since they offer a solution that saves the customer millions in downtime costs, the price of the sensor hardly plays a role. This leads to a gross margin of over 80%.

This is the biggest moat there is. They have a virtual monopoly in this area of automation and problem solving.

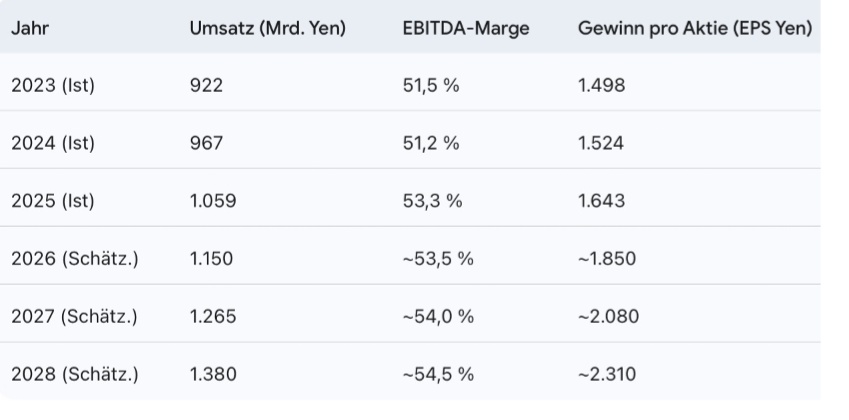

The EBIT margin is a legendary 53% and the net income margin is around 37%. This means that almost half of every euro of turnover remains as pure profit. And that for an industrial company.

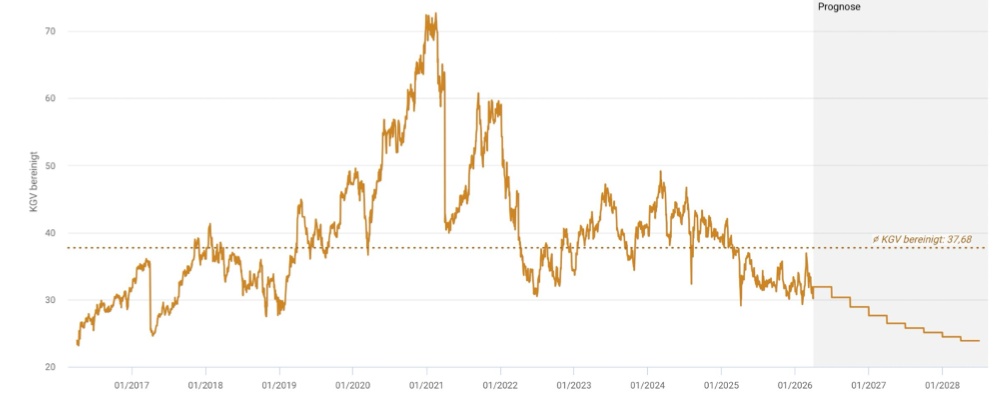

The current P/E ratio is around 30, which is 7.68 points below the historical average of 37.68 for the last 10 years. The 5-year average is even 45. From this perspective, the Keyence share appears to be reasonably valued.

favorably valued from this perspective.

Keyence is also sitting on a high cash mountain and is practically debt-free.

What about the risks?

China exposure & geopolitics

Keyence is heavily dependent on the global propensity to invest.

- Problem: A significant proportion of sensors end up in Chinese factories (e-car production, batteries, electronics). If the trade conflict between the USA and China escalates in 2026 or China makes access for foreign high-tech even more difficult, Keyence will be directly affected.

- Currency risk: The weak yen has visually inflated profits. If the yen appreciates massively in 2026 (e.g. due to interest rate hikes by the Bank of Japan), foreign income will be lower when converted into yen.

Opportunities:

The labor shortage.

This is the biggest opportunity for Keyence. In almost all industrialized nations (Japan, Germany, USA) and even in China, the working population is shrinking.

- From "nice-to-have" to "must-have": in 2026, companies will no longer automate just to save costs, but because they can no longer find people.

- Keyence advantage: As Keyence sensors are extremely easy to install, companies can automate their factories faster than with the complex individual solutions of the competition.

Scalability: Since Keyence has no factories, they can roll out software updates for their AI sensors worldwide and charge subscription fees or higher margins. This makes the business model even more "software-like".

Finally, if we look at the heuristics, the following picture emerges.

The majority of analysts also recommend buying with a premium of almost 30% to the average price target.

Conclusion: I personally see Keyence as a good stock for diversification. The margins are also outstanding and you are still buying a quality company at a high price, albeit well below its historical average. Looking at the heuristics, my model also shows a good risk/return ratio. I don't think you can do much wrong with the share, as the company has a huge cash reserve and also holds a monopoly-like position in Japan.

What do you think of the company? Are you already invested?

Feel free to write your opinion, also with regard to the current market risks.

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Raketentoni

@PikaPika0105 etc......

+ 2

Hello to the GQ community ✌️

My first post after being kicked about 4 weeks ago - who would have thought that solidarity towards one of the members (@Klein-Anleger ) would lead to a ban so quickly? But the goodwill of getquin was so BIG (and above all "on trial") that they graciously let me back into the holy grail of the GQ community 😉

So guys, learn from my mistakes: the goodwill here is not an Infinite Money glitch ! Save your solidarity, reduce your commitment to other members to zero and the most important thing 🚨: No surreptitious advertising for alternative financial platforms like "Cisdord" 😉😂.

Sorry, the side blow after 4 weeks of abstinence had to be 🤝

so joking aside...

⏳The first three months of 2026 have passed. Time for a brief interim summary of the current status of my reconstruction.

Before I started rebuilding the portfolio, I naturally thought about what strategy I wanted to pursue in the coming months and years - especially with regard to stock selection and weighting.

To be honest, my original plan was to keep a portfolio with a maximum of 20 shares. In the course of time, however, I realized that it will probably not stay at 20 stocks, but that the number is more likely to increase to around 30 positions (+/-).

♟️Mein Focus & my strategy:

In a nutshell: The clear focus is on growth 🚀. Dividends tend to play a subordinate role. Here I show you my shopping list and what my portfolio should look like in the future. The stocks I have already bought are marked with a green tick and without a tick, I'm still waiting ⏳

🤖TECH:

🏦💸FINANCE:

🏥🩻HEALTHCARE:

🏭🏗️INDUSTRIE & REST:

------------------------

this is my extended watchlist:

IN TECH:

RAMBUS $RMBS (+8,78%) , QNITY ELECTRONICS $Q (+2,99%) ,

INNODATA $INOD (+9,93%) , NETFLIX $NFLX (-0,8%) ,

VERTIV $VRT (+2,8%) , PALANTIR $PLTR (+15,02%) , VAT GROUP $VACN (+3,32%) , BROADCOM $AVGO (+6,91%) , AMADEUS IT $AMS (+2,11%) , DISCO CORP $6146 (+2,06%) , A10 NETWORKS $ATEN (+4%) , RORZE $6323 , CAMTEK $CAMT (+6,39%)

FINANCE:

APOLLO GLOBAL $APO (+2,2%) / BLACKSTONE $BX (+1,95%) , ALLIANZ $ALV (+0,32%) , FIRSTCASH $FCFS (+2,21%) , BLACKROCK $BLK (+0,74%) SKYWARD SPECIALITY INSURANCE $SKWD , VERISK ANALYTICS $VRSK (+0%) PRIMERICA $PRI (+0,73%) , ERIE INDEMNITY $ERIE (+0,98%)

HEALTHCARE:

MERIT MEDICAL SYSTEMS $MMSI (-1,33%) , REGENERON PHARM $REGN (+0,59%) , UFP TECHNOLOGIES $UFPT (+24,29%) , COLLEGIUM PHARM $COLL (+0%) , LIGAND PHARM $LGND (+2,77%) , HOYA CORP $7741 (+2,82%) , SHIONOGI $4507 (+0%) , IRADIMED $IRMD (+3,47%)

REST:

MISUMI GROUP $9962 (+3,67%) , KANEMATSU $8020 (+1,29%) , APPLIED INDUSTRIAL TECH $AIT (+1,01%) , BADGER METER $BMI (+1,01%) , CEMENT ROADSTONE HOLDING $CRH (+0,3%) , KADANT $KAI (+2,84%) , INTERTEK GROUP $ITRK (-0,25%) , IDEX CORP $IEX (+1,68%) , ORLA MINING $OLA (+0%) , NEWMARKET CORP $NEU (+3,02%) , ROTORK $ROR (+0%) , POWER INTEGRATION $POWI (+5,54%) , LINDE $LIN (-0,31%) , GAZTRANSPORT & TECHNIGAZ $GTT (-1,34%)

This is not yet my final stock selection/watchlist. Of course, there can always be changes if, for example, the @Tenbagger2024 continues to present such undiscovered gems 🙏🏽🧐

------------------------

What should the sector/country weighting look like?

Let's start with the "desired"

🌍country weighting:

🇺🇸🇨🇦USA ~60%

🇪🇺EUROPA ~20%

🇯🇵JAPAN/ASIA ~15%

Rest ~5%

Sector weighting should be as follows:

💻TECHNOLOGY: ~30-35%

💸FINANCE: ~ 20-25%

HEALTHCARE: ~ 10-15%

🏭INDUSTRY: ~ 10-15%

REST: ~ 5-10%

So, what has happened since the beginning of the year?

Of course there were no sales 😬

There have been a few purchases where I have a finger in the pie.

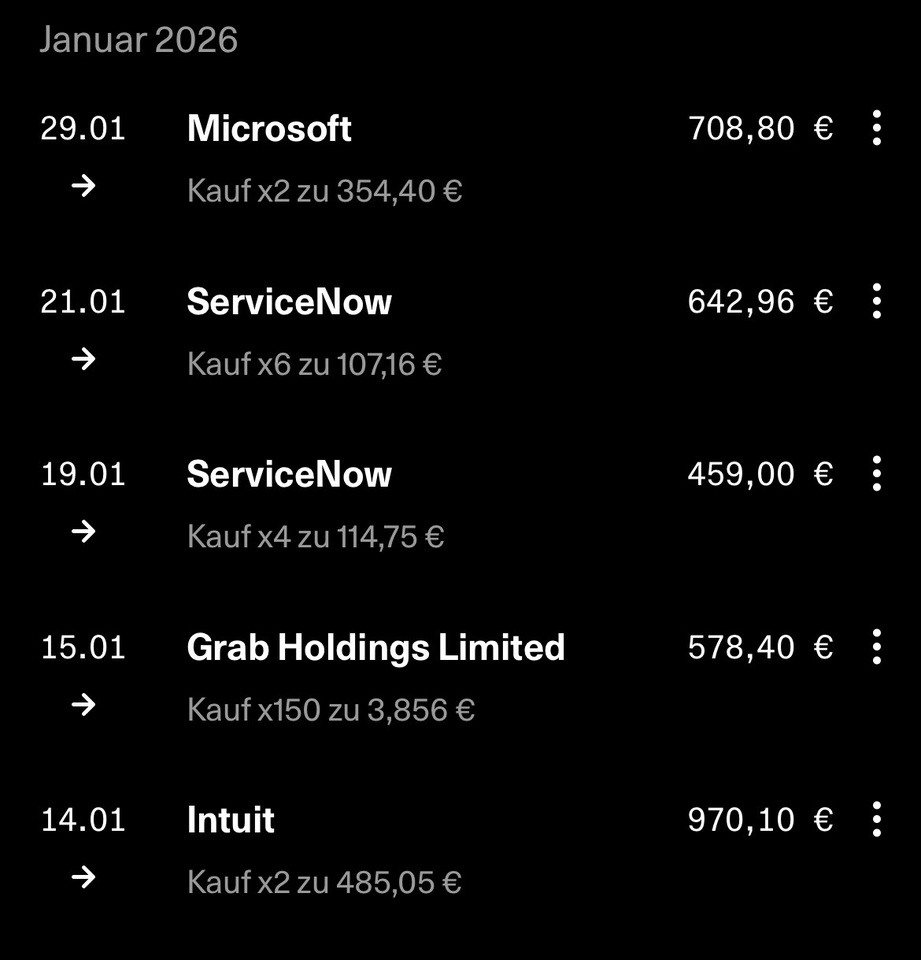

JANUARY PURCHASES

$INTU (+0,78%)

$GRAB (+2,08%)

$NOW (-0,1%)

$MSFT (+1,7%)

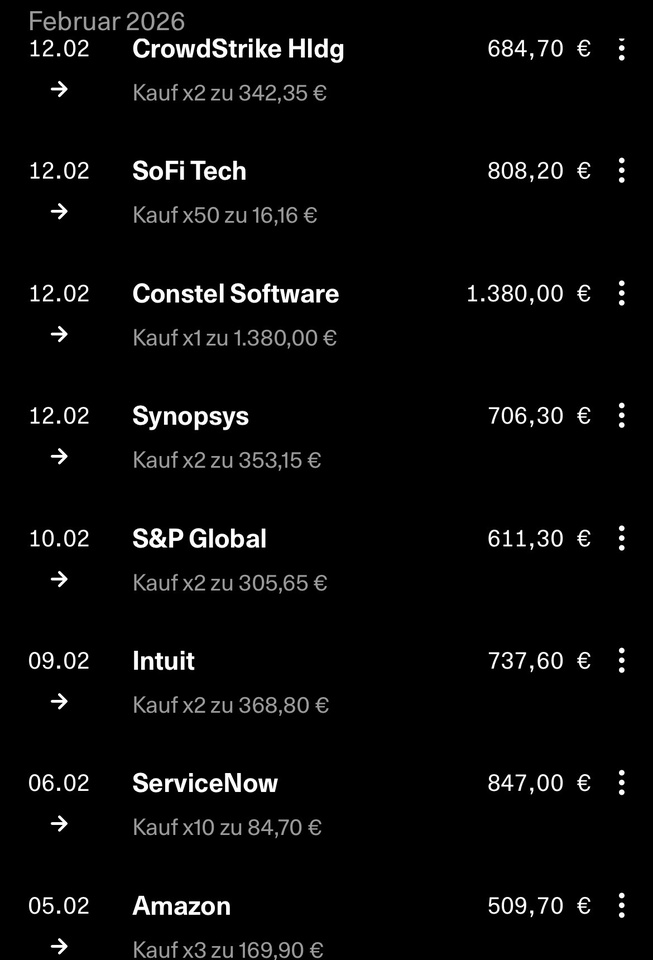

FEBRUARY PURCHASES

$NOW (-0,1%)

$INTU (+0,78%)

$SPGI (-0,82%)

$SNPS (+2,05%)

$CSU (+4,03%)

$SOFI (+2,7%)

$CRWD (+2,81%)

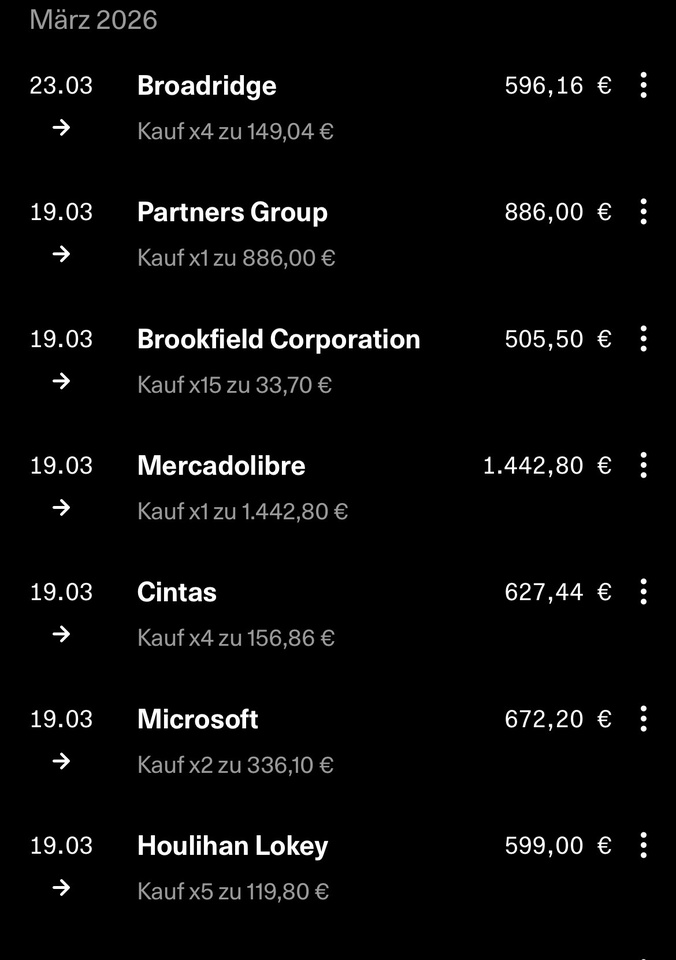

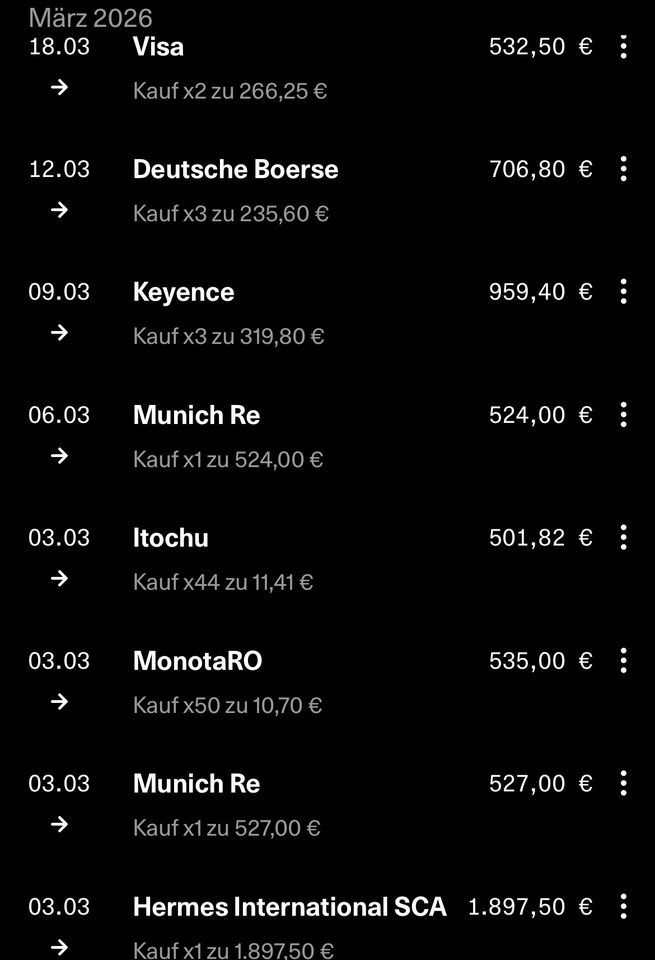

MARCH PURCHASES

$MUV2 (-1,42%)

$3064

$8001 (+1,9%)

$6861 (+2,96%)

$DB1 (-0,88%)

$V (+0,8%)

$HLI (+2,48%)

$MSFT (+1,7%)

$CTAS (-0,22%)

$MELI (-1,58%)

$BN (+2,11%)

$PGHN (+3,17%)

$BR (+7,42%)

Due to the global political situation - especially because of this 🍊 in the White House, whose tweets cause more tsunamis 🌊than real natural disasters - and the current drawdown in the S&P 500 (which is very convenient for me right now and gives me a lot of pleasure 🤩), I am accordingly under water💦🫧 with some of my purchases so far.

but hey, we're investing for the long term, aren't we? So easy going, all relaxed 🥱 I will most likely not make any more purchases in the next few days or weeks, park my cash position elsewhere or put it in overnight money and wait and see which zone the market settles in or wait for it to stabilize.

What do you have on your watchlist?

Are you currently waiting or how are you dealing with the current situation?

@Get_Rich_or_Die_Tryin

@Tenbagger2024

@Max095 and of course all other members

Ok, that's enough now 😂

that's it from me for now ✌️

your stock master

February was a challenging and volatile month.

A strong start to the year was followed by a significant sector-rotationtriggered by risk-off-flowsa reassessment of growth stocks and the need to consistently address operational weaknesses in the portfolio.

Despite the volatility, it was a month of strategic realignment:

📊 Monthly performance: -3,15%

📊 Portfolio value: ~39.144 €

📊 Performance max: +27,58%

📊 Performance YTD: -1,32%

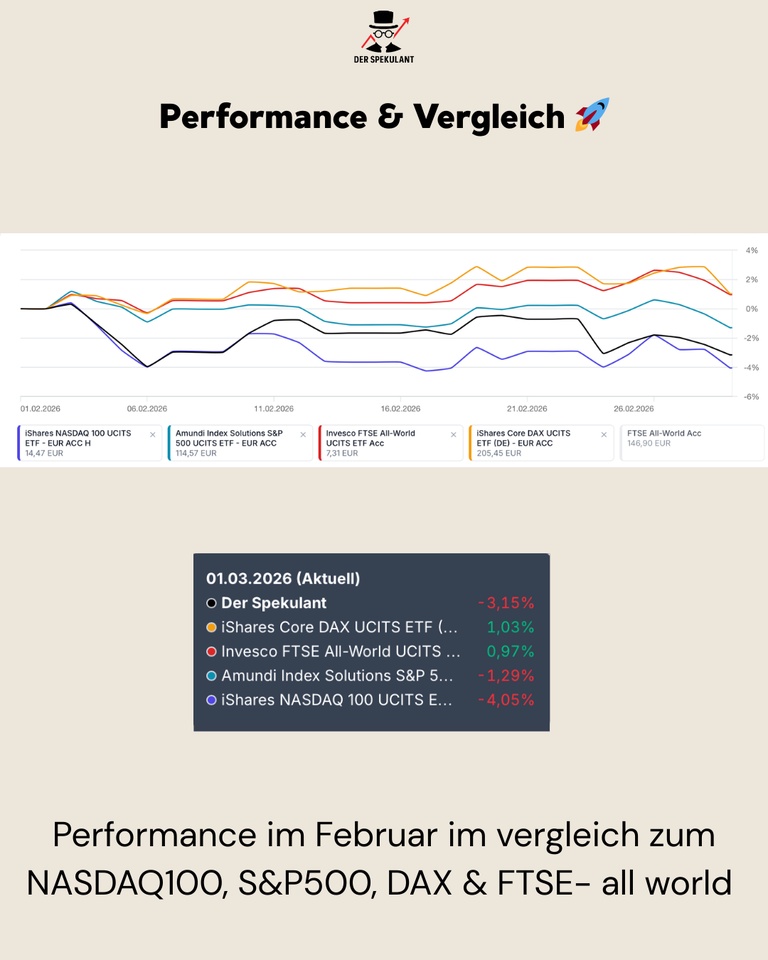

Performance & comparison 🚀

February was characterized by a clear sector rotation:

Software & high-beta tech corrected under pressure, while selected hardware stocks and broadly diversified value stocks showed relative stability.

Performance in comparison (01.02-28.02.2026):

My portfolio: -3,48%

NASDAQ 100: -4,05%

S&P 500: -1,29%

DAX: +1,03%

FTSE All-World: +0,97%

👉 The relative underperformance is due to the high growth exposure, although the portfolio just managed to outperform the NASDAQ 100, which was under heavy pressure.

Purchases, sales & allocation 💶

The focus in February was clearly on portfolio streamlining and strategic shift:

Acquisitions 💰

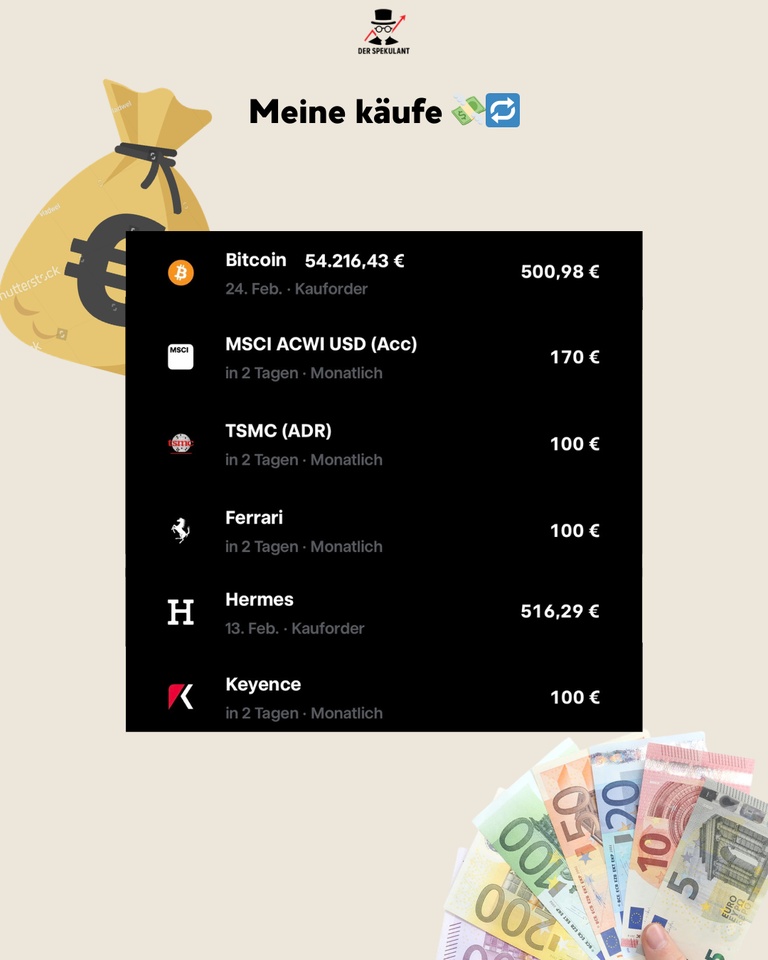

Hermes ($RMS (-0,64%)) targeted expansion in the quality segment. TSMC ($2330) tactical entry due to the observed shift on the stock market from software to hardware. Bitcoin ($BTC (-0,81%)) - purchase of € 500 from the Euro Overnight Rate Swap ETF ($XEON (+0,02%)) at € 54,216 to lower the average price to € 63,000.

Sales ❌

Complete separation of Tomra Systems ($TOM (-0,15%)) and Novo Nordisk ($NOVO B (-6,01%)), as the companies have been operationally disappointing in recent quarters and there were no clear signs of a turnaround from management.

👉 The cash ratio is currently being used dynamically for opportunities through targeted acquisitions.

Top movers in February 🟢

Despite the market environment, February was driven by quality stocks and successful rebounds.

The strongest performer was Keyence ($6861 (+2,96%)), which showed massive relative strength with +16.21%. Another strong performer was Ferrari ($RACE (+0,12%)) was also strong with +13.45%, followed by Berkshire Hathaway ($BRK.B (+0,33%)), which acted as a stable anchor with +6.22%.

The iShares MSCI World Small Cap ($WSML (+1,58%)) gained +3.61%, while the iShares MSCI ACWI ($ACWI) formed a solid base with +0.70%. The Xtrackers II EUR Overnight Rate ($XEON (+0,02%)) rounded off the picture with +0.15% and served as a source for the Bitcoin investment.

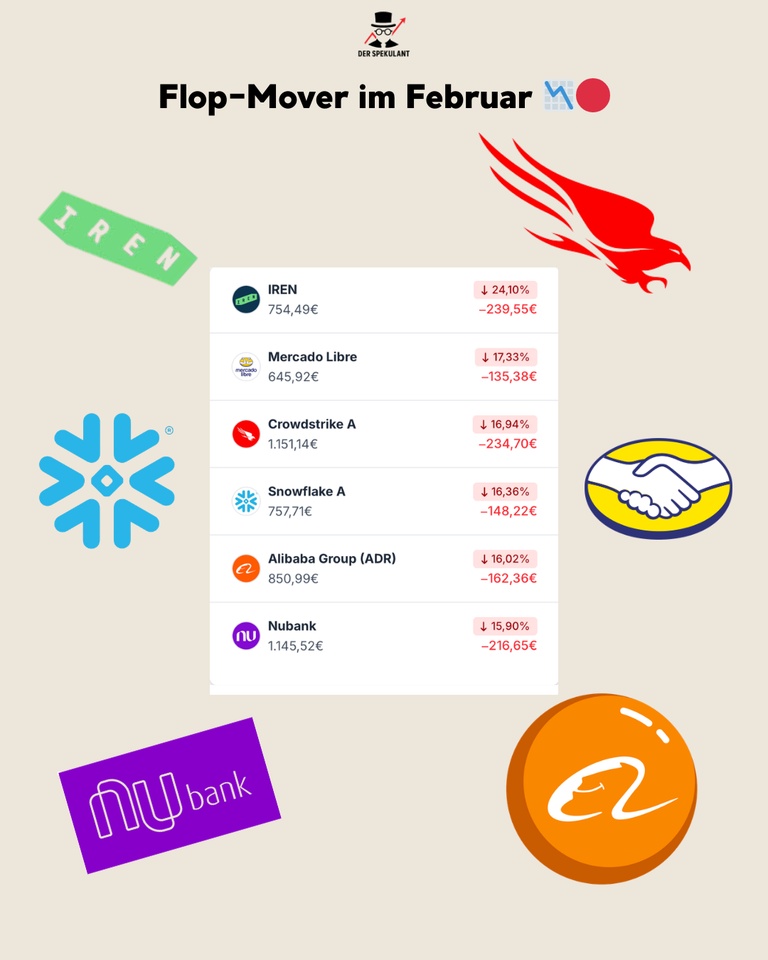

Flop movers in February 🔴

The weaker side of the portfolio was clearly to be found in the growth and crypto segment.

IREN ($IREN (+3,04%)) corrected by -24.10% after the strong previous month. Also Mercado Libre ($MELI (-1,58%)) also came under significant pressure at -17.33%. CrowdStrike ($CRWD (+2,81%)) -16.94% and Snowflake ($SNOW (+3,54%)) -16.36% suffered from the general shift in sentiment in the software sector.

Also Alibaba ($BABA (+1,45%)) also gave back the gains of the previous month with -16.02%. Nubank ($NU (-0,04%)) rounded off the list of losers with -15.90% due to the poor sentiment among payment providers.

👉 Important: These are primarily valuation and sentiment moves, not fundamental breaks - nevertheless, the lack of operational momentum made it necessary to sell positions.

Conclusion 💡

February was not an easy month, but a necessary for rebalancing:

➡️ Strategic separation of stocks without operational momentum

➡️ Focus shiftFrom software/high growth to hardware (TSMC) and focus on quality (Hermes)

➡️ Volatility deliberately used to lower the average Bitcoin price

The environment remains challenging:

Interest rates, Fed expectations and the rotation into hardware stocks will continue to shape the markets in March. The focus remains on quality, operational excellence and liquidity.

❓ Question for the community

Which stock surprised you the most in February - positively or negatively?

👇 Write it in the comments!

+ 2

Keyence ($6861 (+2,96%)) is not a classic hardware trade, but a structural bet on the total automation of global industry and its unstoppable need for efficiency.

Industrial automation is only the tool here. The real value comes from a unique fabless model, radical direct sales and unrivaled pricing power. pricing power.

Margin instead of mass, problem solving instead of product sales, cash flow instead of capital commitment.

⚙️ What does Keyence do?

➡️ Core Business & FA (factory automation):

World market leader in sensors, measuring systems and machine vision solutions. Keyence provides the "eye and brain" of the modern smart factory. The products are essential for autonomous production.

→ Technology leadership + Indispensability.

➡️ The fabless model:

Keyence does not produce itself. By outsourcing production, the company makes massive CapEx savings and remains extremely agile. The capital flows primarily into R&D and sales.

→ Maximum scalability + asset-light structure.

➡️ Direct sales as a moat:

No middlemen. middlemen. Highly specialized engineers advise customers directly on site at the factory. This creates deep trust and secures the highest margins in the entire industry.

→ Deep customer understanding + enormous pricing power.

➡️ The innovation machine:

Over 70% of new releases are world firsts. Keyence anticipates industry problems before customers have even identified them themselves.

→ continuous competitive edge + high barriers to market entry.

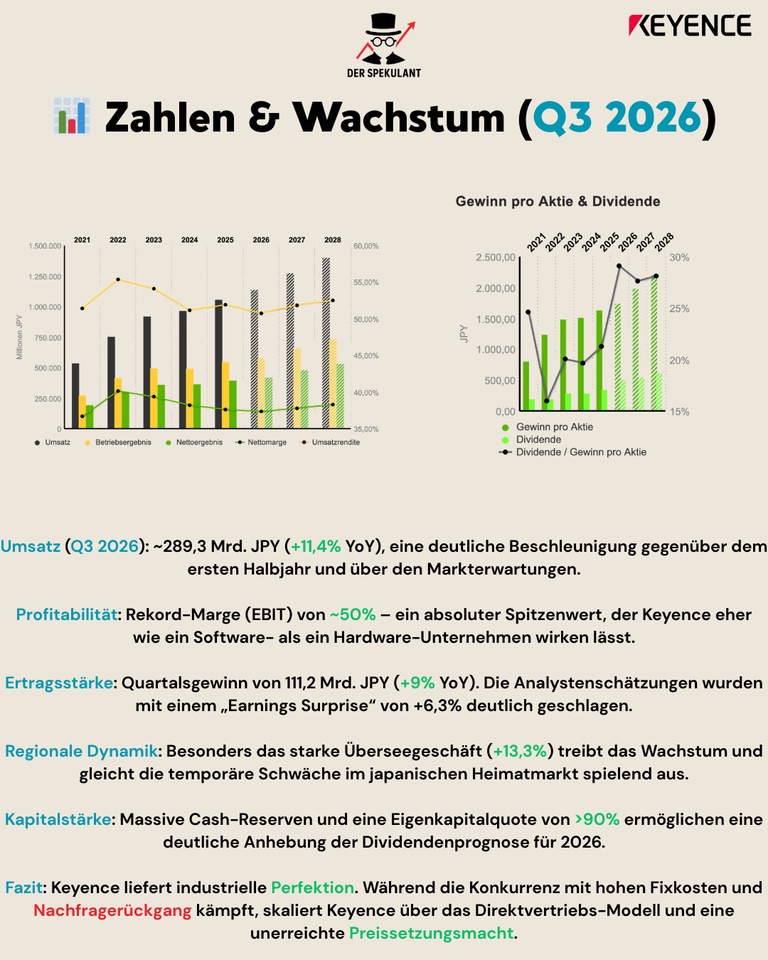

📊 Figures & growth (Q3 2026 - reported 29.01.26)

📈 Quarterly sales Q3:

~289.3 billion JPY (+11,4% YoY) → significant acceleration and outperformance compared to market expectations.

📊 9-month sales:

At JPY 834.6 billion (+7,7% YoY), the company is heading unerringly towards a new record year.

📈 Profitability:

Record operating margin (EBIT) of ~50% → An absolute peak value that makes Keyence look more like a software company than a hardware company.

👥 Regional dynamics:

The strong overseas business in particular (+13,3%) is driving growth and easily offsetting the temporary weakness in the Japanese domestic market.

💰 Capital strength:

Massive cash reserves and an equity ratio of >90% enable a significant increase in the dividend forecast for 2026.

Conclusion: Keyence delivers industrial perfection in numbers. While competitors struggle with fixed costs, Keyence scales through efficiency and desirability.

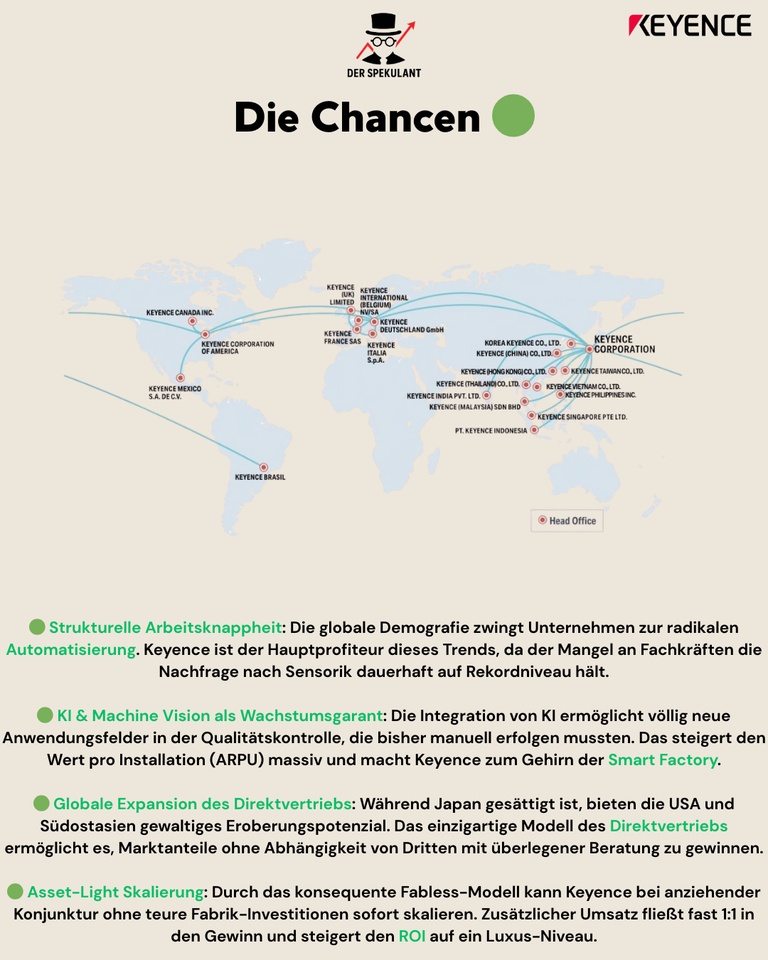

🟢 The opportunities

🟢 Structural labor shortage:

Global demographics are forcing companies to automate. Keyence is the natural beneficiary of the skills shortage in Japan, China and Europe.

🟢 AI & machine vision as a guarantee for growth:

New vision systems with AI support increase the value per installation (ARPU) and open up new markets in automated quality control.

🟢 Asset-light scaling:

During an economic upturn additional turnover flows almost 1:1 into the profit, as no expensive investments in own factories are necessary.

🟢 Global expansion:

The unique direct sales model still offers enormous potential for conquering traditional retail in the USA and South East Asia.

🔴 The risks

⚠️ Cyclical dependency:

Keyence depends on the investment cycles of the automotive and semiconductor industries. A global recession puts a direct brake on demand.

⚠️ Currency headwinds (yen):

As the majority of growth is generated outside Japan, a strong yen leads to negative translation effects. translation effects on earnings.

⚠️ China cluster risk:

A significant proportion of demand comes from China. Geopolitical

tensions or local phases of weakness have a direct impact on international momentum.

⚠️ Sporting assessment:

Quality has its price. The high

P/E RATIO leaves room for corrections in the event of the slightest operational disappointment or slower growth.

💡 Conclusion & outlook

Keyence is not a short-term hardware trade, but a structural bet on global automation of the next decade.

🔹 Short term:

Sensitive to the general valuation level (P/E ratio), global currency effects and market sentiment towards quality stocks.

🔹 Long-term:

ROI machine with a deep technological moatextreme pricing power and an operating marginthat is unparalleled worldwide.

🎯 Investment case:

Leverage on skills shortage + smart factory + AI sensor technology + maximum margin efficiency→ Structurally value-enhancing, operationally highly profitable, the gold standard for the portfolio in the long term.

💬 Community question:

👉 Japan's most profitable tech champion as a defensive anchor in the portfolio

or

👉 currently too expensive for a new entry at this P/E ratio?

I am curious about your assessment 👇

+ 2

I actually had individual stocks like $6861 (+2,96%)

$6920 (+7,76%)

$7012 (+5,87%)

$2802 (-0,04%) on the screen. Why has it now become the $XNKY (+2,7%) become?

ETF instead of individual stocks:

Instead of having to choose between the Japanese tech giants, I wanted to reduce the complexity by adding the 225 largest stocks to my portfolio.

Momentum affinity:

Since I am a fan of momentum (also have Europe Momentum in the core), the price weighting of the Nikkei 225 suits me more than the classic market capitalization.

Although Japan is already included in the $FWRG (+1,64%) I am now deliberately overweighting it. I believe that Japan still has a lot of potential to develop.

My aim is to realize gains from my individual stocks such as $ASML (+3,15%) and $GOOGL (+1,55%) as soon as a return of 200% has been achieved. Then I take the stake out and shift into the ETFs. This is how I prepare myself for times when I have to worry less about my portfolio and it becomes a self-runner.

I've realized that I spend too much time on the stock market and I want to reduce that.

My core should consist of 75% in future

Satellite with the mentioned profits and individual assets or altcoins at 25%.

My USA share is currently 40%, Europe 16%, Asia 12%, gold 12%, crypto 8%. I have the rest in $XEON (+0,02%) lying around.

The USA share should not exceed 50%, as I believe in Europe, emerging markets and Japan.

Good morning,

I find Japanese companies and culture extremely exciting 🧐. During my research I came across Keyence $6861 (+2,96%) as there isn't much about it here yet, so I thought I'd summarize the points I found.

I hope that one or the other will be interested.

Activity:

Industry:

product:

Customers:

The P/E ratio is around 35, historically it is lower than in the past, the company is not valued favorably but rather fairly.

Anyone interested in a profitable company from Japan with high margins and a broad range of customers in almost every sector should take a look at the company.

This is not investment advice. I would like to hear your opinions and assessments.