In this series, I present companies that have the potential to achieve an annual return (CAGR) of 20% over the next five years. After Constellation software $CSU (+3.84%) Microsoft $MSFT (-0.01%) Mastercard $MA (+1.59%) , Nvidia $NVDA (-0.93%) , service now $NOW (+6.06%) and many others, today we look at a champion that is often overshadowed by the "Magnificent Seven", but has an impressive dominance: Intuit Inc.

What does Intuit $INTU (+5.24%) ?

Founded in 1983, Intuit has grown to become the global market leader in financial software. The goal: to radically simplify complex financial processes for private individuals and small businesses (SMEs). The ecosystem rests on four powerful pillars:

* QuickBooks: the centerpiece for SMEs. From bookkeeping and invoicing to payroll accounting.

* TurboTax: The undisputed market leader for digital tax returns in the USA.

* Credit Karma: A platform for consumer finance (credit reporting and financial products).

* Mailchimp: A marketing automation tool that completes the customer journey.

The quality analysis

With a current overall quality rating of 9.2/10, Intuit is among the absolute elite in the software world.

1. profitability & sales quality (10/10)

Intuit is a highly efficient cash machine.

* Margins: An operating margin of approx. 40% (non-GAAP) is a clear USP in the SaaS sector.

* Recurring revenues: Over 80% of revenues are subscription-based. Since financial data is "sticky" (high switching costs), customer churn is extremely low. Once you have your accounting in QuickBooks, you usually remain a customer for life.

2. economic viability & market position (10/10)

The "moat" is enormous. Especially the network effect via tax accountants is crucial: since almost all US accountants are trained on QuickBooks, they guide their clients into this system by default. In addition, competitive pressure has been eased by free government tax tools (such as IRS Direct File) for 2026, which further strengthens TurboTax's position.

3. management & strategy (9/10)

Under CEO Sasan Goodarzi, Intuit is consistently transforming itself into an AI-supported expert platform.

* Insider signals: Particularly positive: Insider selling has been stopped and management has massively accelerated share buybacks in March 2026. This signals to the market that the management currently considers the share to be undervalued.

* Capital allocation: With a dividend increase of 15% and an authorized buyback volume of around USD 3.5 billion, a massive amount of capital is being returned to shareholders.

4. growth prospects (8/10)

Although Intuit is already a giant, its market penetration in the USD 300 billion overall market is only around 6 %.

* Growth driver: The switch from pure "do-it-yourself" to TurboTax Live (support from real experts) opens up the huge market for assisted tax returns.

* Outlook 2026: Growth of around 40% is expected for the "Intuit Enterprise Suite" segment (SMEs).

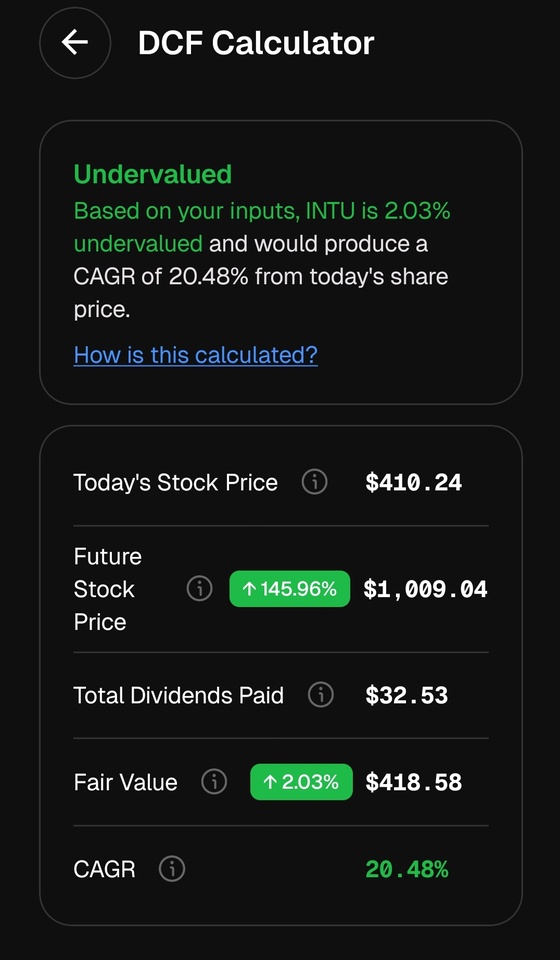

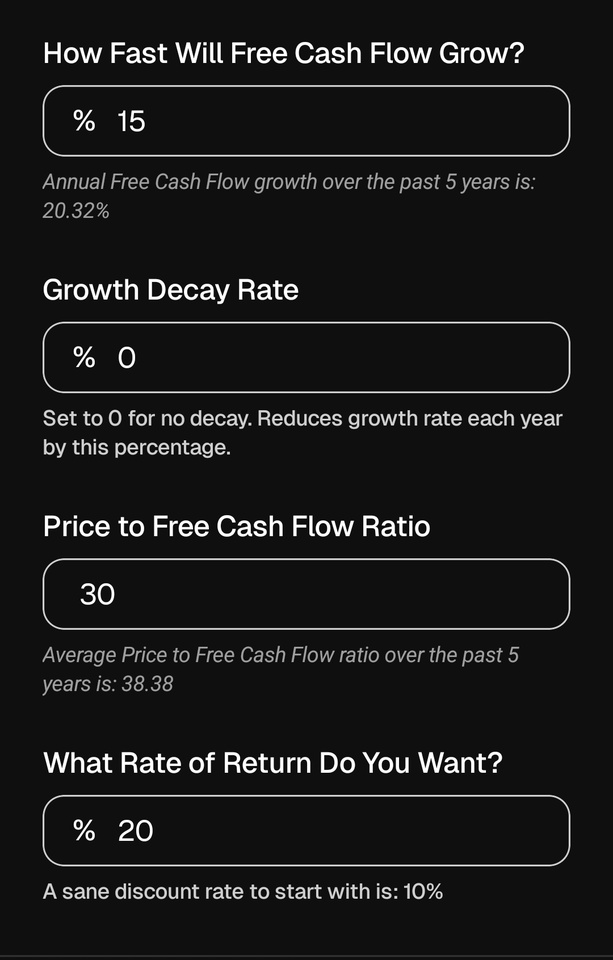

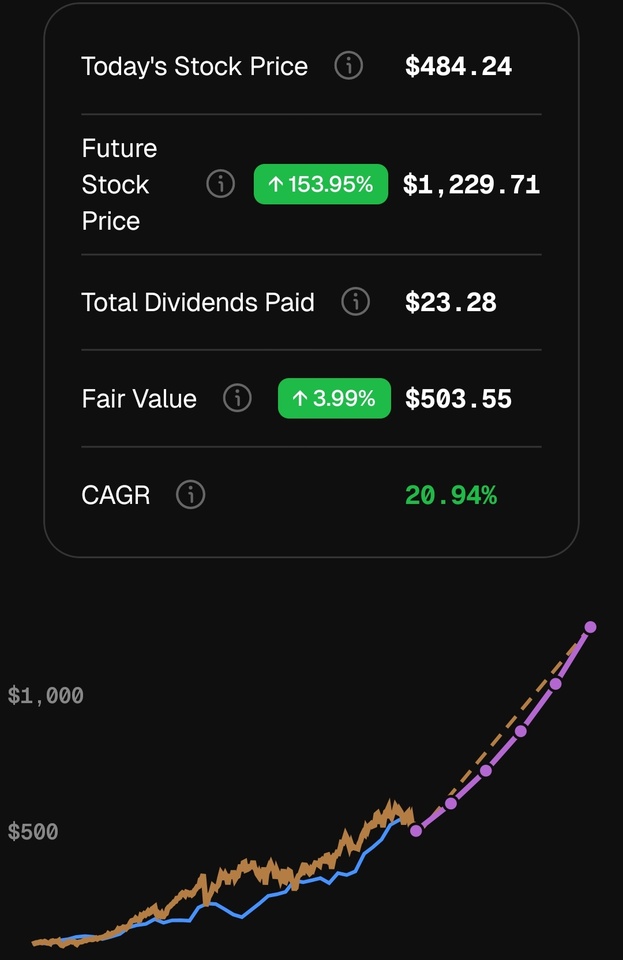

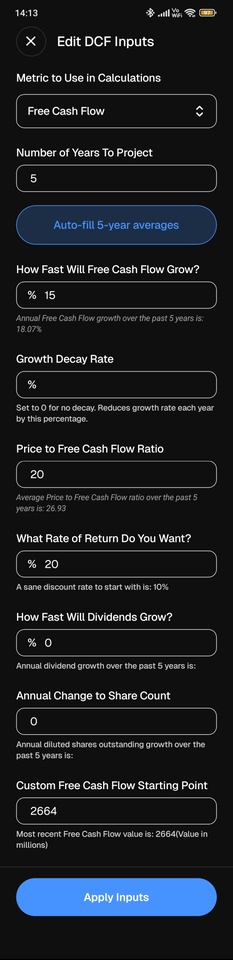

The 20% CAGR calculation: where is the journey going?

Based on the current data from StockUnlock, the following scenario emerges:

* Current share price (as at 31.03.2026): approx. USD 407.67

* Forecasted FCF (2026): approx. USD 7.4 billion

* Weighted 5-year price target: USD 876.25 (+115% potential)

* Forward pe is 17

To achieve a 20% annualized return, Intuit needs to steadily increase its free cash flow and earnings per share. The combination of double-digit organic growth (approx. 12-15%) and the aggressive share buybacks makes this target absolutely mathematically achievable.

Conclusion

Intuit is a quality company with an extremely robust business model and high visibility. The current valuation is particularly exciting: the share is currently trading at one of the lowest valuation levels in recent years, although hardly anything has changed in terms of fundamental strength.

The combination of stable, recurring sales, strong free cash flow growth and consistent capital repatriation results in an attractive risk/reward ratio for long-term investors.

What do you think? Is Intuit a clear buy at the current price or do you see regulatory risks in the US tax market? Let us know in the comments!

I am not invested.

https://youtu.be/sxM55ihFKNg?is=W6k_lVYnHOvpMdSN

A detailed analysis in English